By David Hargreaves

It honestly could be a coincidence that has nothing to do with KiwiBuild. But maybe not...

Like a few interest.co.nz commenters my first thought on seeing the sharp drop-off in both the amount and proportion of total borrowing by first home buyers for June was that it may be due to a large number deciding to 'wait' for a KiwiBuild house.

However, it should be pointed out that the Government didn't release the eligibility criteria till the start of THIS month. Although of course the opposing point to that is that the level of buzz around the KiwiBuild initiative has been rising, so, it's possible some people were deciding to wait.

Maybe also, there was an element of pent-up demand in the market that has been to some extent absorbed in recent months following the RBNZ's relaxation of the loan-to-value-ratio (LVR) restrictions at the start of this year.

The banks can lend to more high-LVR buyers now, so, maybe that's what they are doing. And now maybe there will be a natural drop off in the demand from FHBs once that pent up demand has been satisfied.

Either way there will be a lot of interest in the mortgage figures for July and onwards I think and we should get a clearer picture of what's going on.

Because having said what I've just said in the way of qualifying myself and the situation - I think it is entirely possible a lot of people have decided to hang out in the hope of winning the KiwiBuild lottery.

This makes me uncomfortable.

The fact is you do wonder if the people who have registered for a KiwiBuild house have their eyes fully open about how long it might take to get one - if indeed they get one at all.

The Government's promised 100,000 of them in a 10-year period, with about half of those in Auckland.

Already of course according to the most recent official update, over 35,000 people, with nearly 23,000 of those in Auckland, have registered interest in getting a home.

To reiterate, the plan at this stage is for 1,000 KiwiBuild houses by June next year, another 5,000 in the year to June 2020, 10,000 in the year to 2021 and 12,000 a year after that till completion of the 100,000.

So, to extrapolate a point I've made previously, even if just half (17,000 to 18,000) of those registering interest take their KiwiBuild interest to the next step, they could be waiting into 2022 to get a house.

For young couples with for example, ambitions of starting a family, a lot could happen over the next four years.

Should we wait or should we buy?

Inevitably we come back to that agonising point of should people wait or should they buy now, if it's at all possible to do so?

The simple answer, and it's wonderfully simple is this: If you know the house market is going to stay flat for the next four or five years then wait. If you know it's going to go up again buy now. And if you know either of those things for certain then you are more gifted than any real estate agent, politician, economist, interest.co.nz columnist, etc, etc.

If people are deciding to wait then the pressure is definitely on the Government. Any disappointment with the roll out of KiwiBuild houses (and let's face it that's entirely possible) or any re-ignition of the housing market and the loud howls of complaint will start.

With this in mind I just had a quick trawl through the figures to try to get a bit of a layperson's understanding of the challenge for the FHBs at the moment.

As previously reported the FHBs borrowed $803 million in June. Now this amount of money was taken out by 2039 borrowers. Averages of course can be somewhat deceptive and are invariably blown out by the 'Auckland effect', but that works out to $394,000 for the 'average' FHB mortgage. The previous month, May, when total borrowed by the FHBs roared to over $1 billion saw an average mortgage size of in excess of $400,000.

When you imagine that some mortgages in the regions would be considerably less than that well, there's some FHBs with some pretty damn big mortgages out there.

I wondered how much worse things had got over the past few years.

Some numbers

Regrettably this excellent information now provided by the RBNZ was not available till August 2014, so, the first apples with apples comparison I can give is for June 2015, when the FHB grouping borrowed $577 million, with an average mortgage size of just $313,500.

So, that average has gone up quite a bit, with most of the rise actually occurring in 2016, when the average mortgage size according to these RBNZ figures shot up to $375,000 - presumably in a fair reflection of what was happening in the market at the time.

The affordability has therefore got tougher, but not astonishingly so, really.

Using the interest.co.nz mortgage calculator we can work out that an FHB on a then-market average floating rate of 6.47% would on a $313,500 mortgage for 30 years be paying about $23,700 a year.

The amount our hypothetical average-mortgage FHB would have to pay has gone up since 2015 by nearly 18%, which largely represents the need for the bigger mortgage, given that the market average floating rate is now 5.85%. But at just under $28,000 a year that's probably doable for a reasonable number of people.

As a matter of interest, doing the same sums on 'the rest', those mortgage holders who are either owner occupiers or investors, shows us that as of June 2015 the average mortgage size for new borrowers was $189,000 and now as of June 2018 it's $221,000.

Using the same interest rate calculations gives us annual mortgage payments back in 2015 of $14,300 for the owner-occupiers/investors, now rising to $15,600 as of June 2018, with the rise again due to the increase in the size of mortgage.

Thank goodness for low interest rates, and one shudders to imagine what happens if there is some sort of horrible shock that sends those rates up again to the sort of historic levels we have had.

If we assume not though, it all boils down to the question of whether - particularly the FHBs - should wait or if they should move now.

As indicated earlier up this column, we'll know the answer to that question in say 2022-3 when maybe some of those who 'wait' are getting a KiwiBuild house.

It's all leaving a lot to chance.

Government needs to be realistic

I for one hope that the Government is upfront on how long the KiwiBuild homes will take and is realistic in spelling out what people's chances are of getting one.

Because the backlash could be extreme if people are left hanging and waiting for years and if house prices start rising again appreciably (and/or interest rates too for that matter).

It's not really advice because I don't give advice because I'm not a financial adviser. But generally in life I think you are best to depend on yourself and what you can do.

I wouldn't be depending on the Government to deliver if it was me, let's put it that way.

It's a difficult situation though and I don't envy people trying to make these choices at the moment.

All I would say in closing is to reiterate that the Government is going to have to be up front and on the front foot telling this as it is. It can't create unrealistic expectations because that's just not fair, not when people are making huge life/financial decisions that involve a Government initiative.

I still have a horrible feeling that a lot of people if they do depend on the Government to deliver for them may be left horribly disappointed.

I sincerely hope I'm wrong.

Life experience has, however, taught me to have fairly low expectations of what government can do and then be pleasantly surprised if the outcomes are better than expected. Come on then Government, pleasantly surprise me.

148 Comments

C'mon, all these national supporters are making a mockery of the 650 price cap on KB, but the reality is what do you currently get for 650 in Auckland? Answer: a shitbox

For 650 you can get a one way ticket to melbourne and a 3 bedroom apartment to live in.

Provincial NZ has its charms but Auckland is a mugs game - it's just an inferior version of an Australian capital.

Goodbye saving_for_aussie, enjoy OZ

You left that statement unfinished.. A shitbox in ,Papakura, Manurewa or Ranui

FOMO is out of fashion.

Why buy mutton today when lamb is on special tomorrow.

Yes FOMO has been replaced by FOBE which means Fear Of Buying (too) Early

A famous and very rich guy (Warren B) recommends to be fearful when others are greedy and greedy when others are fearful.

The latter seems appropriate for right now.

.

I wouldn't say the majority of people are 'fulled with fear' just yet.

If these people wait until a Kiwibuild home is available, they will have a bigger deposit so that is not a bad thing at all. And if house prices crash in the meantime, that is not a bad thing for them either. In which case they could just buy privately at that time.

Yep I am very confident KB is deterring FHBs from buying. I have no data, but plenty of anecdotes.

As I said a week or two back, regardless of how many KB homes are actually built it is likely to have a significant impact on the market.

Define "significant"?

"sufficiently great or important to be worthy of attention; noteworthy"

there you go!

if at least 25% of FHBs deferred purchasing as a result of interest in KB then I think that would be significant

apologies let me be more specific, you stated;

"regardless of how many KB homes are actually built it is likely to have a significant impact on the market "

But what does that mean? Are you saying that because KB is over subscribed and FHB will build up over the next year or so while they wait for these houses once they enter the market we will see price sky rocket as there will not be enough "affordable houses" to go around? That seems to be what you are implying and I totally disagree.

No.

I'm saying it will contribute to house price falls as the FHB component of the non-KB buying market will be subdued.

Surely the informed writer need only look at housing by tenure data from Stats NZ ,which covers a period somewhat more than one month,to ascertain what first home buyers are unable to or wish not to do on a rather longer time frame. Given that Census data has been delayed and will need to be extrapolated ,future Stats NZ data estimates may be more insightful regarding the plight of first home buyers. David one factor that appears to be overlooked in your reasoning is the role of migration and credit growth as the majority by default are FHB and the possibility that many may be in a stronger financial position to obtain a mortgage by nature of their visa type than the home grown variety.

Kiwibuild?

Maybe the combination of high prices, relatively static market, and worldwide economic uncertainty is also playing a part. At the moment people haven't really lost anything by waiting longer. In Christchurch, prices have decreased. Parts of Auckland are down on last year (and volumes continue at their low levels).

Maybe it's not KiwiBuild they're waiting and seeing for?

This. Almost everywhere in NZ has house prices falling at the moment, so not the best time to buy. Most FHB's will have someone in their life counselling them to wait until market bottoms out, and- with economic storm clouds gathering internationally and here there is unlikely to be significant price rise anytime soon. More chance of a sizeable drop.

Almost everywhere in NZ has house prices falling at the moment

No they don't.

https://www.interest.co.nz/charts/real-estate/median-house-price-growth

Hi David.

Now I am fairly new to Interest.co.nz and I believe that you and the team provide excellent information and a superb forum for discussion on a number of key issues that effect NZ. I also admire the openness that allows people to make comment. However, in the above article you state.

'The simple answer, and it's wonderfully simple is this: If you know the house market is going to stay flat for the next four or five years then wait. If you know it's going to go up again buy now. And if you know either of those things for certain then you are more gifted than any real estate agent, politician, economist, interest.co.nz columnist, etc, etc.'

This completely fails to even consider mentioning the fact that house prices can and do fall, and even though it may not have happened for many years and be beyond the memory of some of our commentators from either Australia or New Zealand, they are now in Australia and recent monthly data points to the same now taking hold here.. The year on year stats that you highlight above will, in many many places turn negative by the end of 2018 if what we are seeing in recent monthly falls continues for the next few months.

You also highlight the concern to first-time buyers should a shock in world events (Facebook produced a 20% stock price decline last night - which could be considered a shock) lead to higher interest rates. Could it not be possible that First-time buyers are not as stupid as the banks and media would like them to be and that maybe they to are well aware of the considerable risks of entering such an inflated market at this juncture.

In my opinion, kiwibuild is just a tiny part of the puzzle as to why first time buyers are holding back. Credit availability, concern over Australia, concerns over interest rates 2-3 years from now (when taking on a 30 year commitment), limited wage growth, stories from those that are heavily indebted and already struggling, The Royal Commission, Overseas buyer ban, possible removal of negative gearing, impacts of switch to repayment only mortgages in Aussie and how that will effect default rates, credit availability, Slowdown in China, trade tariffs etc etc are all huge factors that first time buyers are hearing and seeing for themselves. There are also a few experienced parents who like me won't be funding the deposit for their offspring at this point in the cycle when the downside risks are as great as they are.

All that being said I think that it is fantastic that 'interest.co.nz' is providing a platform for this debate to be intelligently brought to the public because in my opinion the mainstream media are far too reliant on the revenue stream from the banks ((as we saw with the advertising spend increase in the first half of 2018 of 38% by the banks and who have a vested interest to replace the mortgage free with new heavily indebted generation of bank income stream) and as a result the cacophony of voices in the media does not provide an unbiased platform for discussion about the genuine risks that New Zealand has not faced for some considerable length of time.

FYI Nic, I think you are getting your Davids confused...

An eye for detail he does not have. Nor facts, nor nuance.

Bit harsh BLSH, but you forgot...

'Nor any leveraged or negatively geared assets to cloud his judgement on offering advice to the young'

Yes, leveraged or negatively geared assets are not clouding your judgement. Property envy is.

Gareth. I have indeed,

My sincere apologies to Mr Chaston and Mr Hargreaves. Rather than me edit and change the original can we just assume my response is a collective response to Interest.co.nz.

@Nic J

..kiwibuild is just a tiny part of the puzzle as to why first time buyers are holding back. Credit availability, concern over Australia, concerns over interest rates 2-3 years from now (when taking on a 30 year commitment), limited wage growth, stories from those that are heavily indebted and already struggling, The Royal Commission, Overseas buyer ban, possible removal of negative gearing, impacts of switch to repayment only mortgages in Aussie and how that will effect default rates, credit availability, Slowdown in China, trade tariffs etc etc are all huge factors that first time buyers are hearing and seeing for themselves

out of the aforementioned reasons, what all do an average aspirant FHB heard of or known of ? Its only Kiwibuild kiwibuild kiwibuild . May be slightly about negative gearing and foreign ban( but they will not trust the political will , assuming that even if these happens, will be with enough loop-holes). For them its just buying their home and settling down; to add to that its more of peer pressure or peer influence ; as in the other guy who are just like us buying house, lets buy too.

I am still renting and I came to know about all these 'external' economic activity after landing on interest website.

Hi Greg

I guess the question that I'd ask you then is do you feel better informed to make a judgement having read interest.co.nz and if so should you promote it as a platform to other people in a similar situation to yourself? (Disclaimer.. I have no financial interest in the site but have found it to be the most impartial provider of NZ news and information)

As for peer pressure... Human behaviour often leads to others following the herd into a mess. Anyone who bought Bitcoin in December at $20,000 is today nursing heavy losses as it hovers around $8000. I would say that the people who are talking it up the most today are likely to be those that bought into it December. Facebook was great too and you could have made 20% since May, until it dropped 20% yesterday, but some were talking it up (whilst selling out the day before). Houses are different but they also tend to carry long term leverage but I have seen markets fall 25% -30% over a twelve month period when conditions were similar to how they may be viewed in NZ today and I'm not saying that that will happen here.. but it could.

Just keep reading. There are some great commentators on Interest.co.nz and you'll get some competing views, but as you go along you'll decide that some are worth listening to on housing and others not. The big thing you have in your favour is that you don't have to rush to make a decision because prices haven't been going up over the last 3-4 months, in many places they have been falling.

.I guess the question that I'd ask you then is do you feel better informed to make a judgement having read interest.co.nz and if so should you promote it as a platform to other people in a similar situation to yourself?

I doubt if its worth or if i can educate others about all these. I'm finding it hard even to 'inform' my wife about all these .. LOL

I have a fear, the more the people take debt and fall into the mortgage market, its getting very difficult to prove economic principles.. As people with debt increases, debt will become a bit of 'norm' and interest rate will have to be kept very low because of politics and so called monetary policy. So people who saves will be missed out. I think savers have lost a lot compared to debtors in the past 10 years

As for bitcoins, most of the 'home buyers' we talk about are against bit-coins. They only believe in buying something 'tangible'. You buy house, try to sell it at a profit, if you can't sell rent it , increase rent as much as u like, as the govt is bringing in more people to live here.. so you can't win an argument with them at the moment. Only thing I conclude is lets wait to see if the interest rate increase(hoping for US Federal); but not sure when that happens. The trade-war will cause a currency-war between China and US and some say that china could cause Federal reserve to reduce interest rate.

Right now , just one thing in mind.. work hard to earn my daily bread :-)

Greg, a true FHB aspirant (ie, someone that is realistically somewhere near meeting lending criteria) will know of credit availability, even if they don't think of it in those terms. They will know they need a deposit and ability to service a mortgage, and likely they will have friends that have tried to get a mortgage. Chances are they've been on bank website and used the mortgage calculators so have some idea of whats realistic.

@Pragmatist

Yes ; I agree. What I was saying is reduction in the FHB share compared to May will be just because of Kiwibuild.

And judging 'the ability to service mortgage' differs from person to person, or even bank to bank. A FHB having 10% deposit turned down by 2 banks, but a third bank (ANZ) sanctioned them loan. They may know that the payment could increase in future; but their counter-argument is rent is also increasing

Prices are stable or rising across the country. Sometimes the blatant disregard for facts in this comment section is depressing.

The "wise counsel" to be found by commentators here goes something like this -

When prices are rising - don't buy because this is unsustainable and a crash is just around the corner.

When prices are steady - don't buy because this plateau is a sign of market weakness and a crash is just around the corner

When prices are declining - don't buy because only a fool would catch a falling knife.

How about you people look at actual data, historical trends and a little thing called the property clock?

...property clock ...ha ha..time bomb more like it.

"How about you people look at actual data, historical trends and a little thing called the property clock?"

Ok, let's use data then to show historical trends. Download the spreadsheet back to 1979 and put it in a graph.

https://www.rbnz.govt.nz/statistics/key-graphs/key-graph-house-price-va…

Let me know if by historical data trends you still want to advise FHB's that house prices never comes down? By the way, its been +6 years since the last fall, and I'd say we are due! TICK,TICK

Hi Boet,

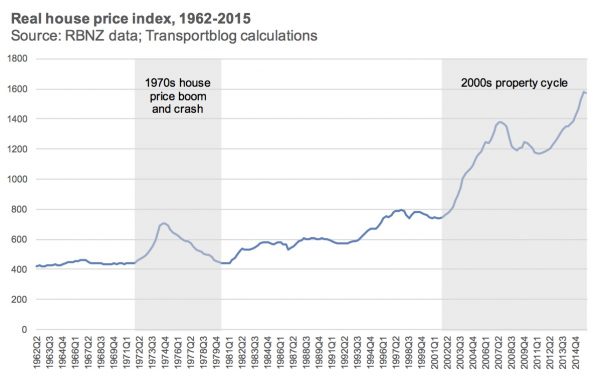

Here you go - http://www.greaterauckland.org.nz/wp-content/uploads/2016/07/Real-house…

{kind=link}

Property prices certainly do go both up and down. The property clock is just a representation of the property cycle through which prices rise and fall. Since records began, prices have gone up and down, but the overall trend has been very positive. There is no reason this trend will change going forward.

Even during the GFC prices fell less than 10%, and recovered shortly thereafter. There has only been one major period of price decline, which was after 1973 when the UK joined the common market.

We are due for a slowdown. We are currently in the second longest period of economic recovery without a downturn. I think we are at 5 o'clock on the property cycle. After that there will be a recovery, as there always is. I expect this to start in 2021/22.

If you are interested in the history of NZ property prices, here is a great talk - https://www.youtube.com/watch?v=0pfbLdp1tlA&t=616s

That real house price index graph really highlights how much more affordable homes were for Kiwis when the government was encouraging and facilitating supply to match the population, huh?

Hi Rickstraus

Yep that graph highlights how silly it's got. Alan Greenspan has subsequently apologised for failing to see the impact of this and how keeping rates as low as he did for as long as he did created a few issues but anyone can see that the last 2 decades massively out of kilter with reality. Except of course people who haven't yet qualified to receive a ruler during school lessons. Thanks for the graph BLSH

Now if you draw a line from the early years through the middle of the graph... and compare it to where it is today you can probably see that there is a big crash coming.. Often these crashes go well below the trend line before recovery takes root.

Hi BLSH - Not to many people on here will believe you and it is sad to see comments about anything with smart arse replies that the likes of HO Nic J often put on here. I have mentioned the property cycle or clock before and been ridiculed. I learnt about this in 1972 when I witnessed property double as a teenager and people said the same thing then that it was wrong and would never happen again.Well it did so I took notice and learnt more about it and made sure I was part of the next one and became an investor in 1983.I find most people can not just accept that it happens and go into ridiculous detail why it shouldn't happen but the market doesn't care what people think. My clock has the next up cycle starting 2020/2021. That's not far away so for all the doubters lets check in then rather than sling shit. Watching and believing in this cycle has increased my capital enormously so I can say for 35 years it has been positive for me, that is a fact rather than a wishlist most people work on here. Some will think this talk naive but not following the history of proven cycles is really naive.

Shoreman...... I couldn't resist having seen your comment above... but given that past performance is no guarantee of future returns and you may get back less than you originally invested (or borrowed to invest more likely).. I have a question for you... while you stand at the 'shore's edge shoreman' are you fully covered and is your modesty protected if the tide goes out?

Please also read some of my comments before you take a pop... you never know you may learn something.. or maybe you won't... but if I tell a different story to the brainwashing you've had so far who know's it may make you a better investor or at least make you sound smarter than predicting 2020/21 as the turn... Is that what they are currently chanting at the seminars?

NJ and HO Oooch ! I don't understand why you guys are so anti, if property is not your thing let it go how you feel about the market makes no difference, For your info NJ I hold 9% debt on total assets in property. I don't set the market I follow the market perhaps you guys haven't there is real anger there. I have also made a killing in Tourism is that a crime too ? I also have large holdings in forestry, just like property I could see great gains ahead when I invested in the past. Property has it's dips I personally thought we would be in one now, I expect a dip up to 10% before we go up again. You may like to know that I made more on property in the Labour/Clark error so only bagging National is silly. If you want to see what the future of bluechip Auckland property will look like in the future go to Sydney for the weekend.And HO really amateur ? Investing in TD as your best shot at investing is very average, thats ok if your risk adversed but would that be your recommendation to FHB ? mine would be if you need a house have a good deposit, satisfy the bank,have a solid income stream, have been realistic in your choice and not over committing buy now and move on with your life avoid negative people. NJ I've never been to a 'seminar' I assume you mean a property one ? End of the day guys smart people have the money look around the others have envy and anger because they missed out.

It's about the right thing, property at the moment is unproductive to the economy, it's overvalued and the market is turning, which you fools are refusing to accept

Clearly people like you are fake hence profile names to circumvent your situation..

HO - I'm real sorry, worked hard for 37 years, saved hard, went without to have spare cash to invest to have a comfortable life later in life.I wish you well putting silly comments on here doesn't help ie the editor felt the need to remove some of your comments above. Look there are opportunities out there for anyone, with time and effort rewards can be had. Everyone started small somewhere. My name well I'm a man that lives on the shore of a lovely beach. Thanks

[ Unacceptable insult. Removed. Ed ]

HO Rather heavy handed, I see in a latter post your are a FHB, how arrogant I have 35 years experience in the market you probably have none, use your time and energy to assist your future rather than be bitter, tap into people who have successfully invested. I wish you well in you're future being critical of others will hold you back.

[ Unacceptable insult. Removed. Ed ]

Hey "Ed", can you renamed Houses Overpriced to Ad Hominem?

Isn`t it wonderful that since 1983 you have been investing your money in nonproductive assets while simultaneously contributing to a situation where we have the lowest rates of home ownership in over 3 decades. We need more people like you in this country. Thanks.

Nonproductive? Not in the sense that a stock/equity is productive, but the roof that protects you from the rain is performing a fairly essential service. The land that provides you with a place to eat and sleep is performing a fairly essential service.

Ngrrk - Assuming is a terrible thing, you have assumed I have only invested in property, for your info I am an investor in Tourism and Forestry and the Sharemarket at times, an attitude of blame doesn't do anyone any good what have you contributed to with investing ? Thanks

Hi Shoreman, thanks for sharing your experiences and your foresight in using the property clock. We are long term investors too. We haven't worried about timing our investing according to the property clock, and have bought when able and sold depending on our needs at the time. This has kind of coincided with the market swings so we have still done well enough but I take your point about the property clock and how effective it is. There is another phenomenon which investors should be aware of and many are now. I always knew it as the ripple effect with a wave of investment spreading from the centre to the edge, and the ripple is now hotting up smaller centres. It has also been called the halo effect which is a good description. As for us we don't bother to chase those gains, it isn't really our focus but it is good for owner occupiers and new landlords....cue the stupid responses

Hi Shoreman. Very true. My biggest complaint is that these people refuse to learn from the past. They instead rely on their feelings, but as you point out, facts don’t care about feelings.

you nailed it on the head, the facts now show that the market is reversing the glorious days of capital gains, but you guys prefer to ignore that and go with the story of the past.. you'll are only fooling yourselves

The market is steady in Auckland. Rising nationally.

Please refer to my previous comment -

Property prices certainly do go both up and down. The property clock is just a representation of the property cycle through which prices rise and fall. Since records began, prices have gone up and down, but the overall trend has been very positive. There is no reason this trend will change going forward.

Yeah, MAYBE in 10 years

2021/22

Sweet see you in 3 years then, nice knowing you

'a little thing called the property clock'

That sounds like a magical instrument. Is it like the clock from Captain Hook's crocodile and it ticks louder and louder as it gets closer to gobbling up the over-leveraged, giving them a warning to bail out of the market before they're eaten alive? Where do I get one? can I buy them in Farmers or do I have to pay an annual subscription to the NZPIF to get one?

Property Clock. Brilliant.. No need for rational economic understanding and knowledge of Credit Cycles, just buy a 'Property Clock' and if it stops working you can buy 'Property Tea Leaves and a Property Crystal ball'

BLSH, I hope that you haven't paid too much and bought a 'knock off' Rolex there mate.

Nic can u elaborate on what you mean by credit cycles..??

For myself, It was only when I began to understand Monetary systems, that I started to make sense of macroeconomics.

In that regard, I subscribe to Ray Dalios' views.

In regards to Real Estate , I see that there is a relationship between continually increasing money supply and continually rising house prices..

There are only 3 places that new money can go :

1/ productive investment

2/ Consumer spending

3/ Speculation.

Iin NZ, most new money (credit) goes to the household sector ,because most of us love to invest in Real Estate...

I consider that House buying is mostly "consumer spending" and also some "speculation"...when the cycle is "hot "

eg.http://inflationmatters.com/wp-content/uploads/2015/01/011.jpg

{kind=link}

just my way of seeing it..!

Roelof

Don't agree with some of that albeit it would take more time to explain the expansion of credit and contractions but in essence;

'There are only 3 places that new money can go :

1/ productive investment

2/ Consumer spending

3/ Speculation.'

Agree on that but returns on 1 have to cover the costs of servicing debt on 2 and 3. If they don't you eventually have a credit imbalance where production gains don't service interest costs on 2 and 3, which the market will ultimately address. Our credit balance has been skewed by capital/credit flight into the country forcing prices up and locals have overleveraged on 2 and 3 which is now well out of kilter with 1. A return to 1 being able to support 2 and 3 is the only way to cure the imbalance which will mean tightening of criteria to 2 and 3 and redistribution to 1..... Or, we keep selling ourselves to foreign credit but I think society has shifted against that now and the bank balances in Aus and NZ are too heavily weighted to 2 and 3 without the foreign capital. So we will cycle round (after a fair amount of pain) to a heavier weighting in 1. Pretty simple really but using your terms to explain the wheel. Aussie banks are already finding it harder to access foreign capital (they are our banks too) so its just a matter of time.

Very well put together the relation between 1,2 & 3. Thanks Nic

But these are theory ; but since more money gone into '3' , I see only two possibilities..

a) Let this go on 'somehow', by manipulating 'something'

b) a collapse, where everyone suffers :-( ; including people who have not availed any credit

As i mentioned in an earlier comment, I don't know what/how of the somehow/something. People with power will manipulate that, as they may also be part of the over-leveraged system

Hi Greg

I think we have pretty much run out of options on a) but it has been fun while it lasted - the last throw of the dice is John Key trying to lobby for no foreign buyer ban which is the credit that fuels our overleveraged system. Other policy tools are already exhausted. Loan to value ratios are maxed out as are Debt to incomes and interest rates costs are more about International costs. Therefore prepare for b) remembering that a lot of those that run the system / banks / media / government have already given themselves 9 or 10 months to get out whilst keeping it quiet from the masses... b) will follow fairly soon but will likely be a gradual collapse because people who haven't seen this before (most property owners under the age of 50) won't want to believe it and will hang on and on, until they can't.

I don't think it will be too much fun but recessions and creative destruction is just the capitalist way and will lead to a wave of new opportunities for the next generation. Human beings are also quite resilient really and will muddle through

Can NZ Govt/RBNZ not do a quantitative easing of its own ? may be devaluing NZD , but help to serve the debt better / longer, by keeping interest rate lower ?

They could try but I can't see that doing anything to help other than making our debt payments from foreign based financing more expensive in dollar terms. It would re-ignite or encourage foreign speculation in our housing assets as people could get more dollars for their currency but I believe that that door is slowly creaking shut and if it doesn't close then NZ is no longer a genuine democracy - it is just a play thing of the banking elites.

So in essence, our currency may devalue anyway as all the hot foreign money is prevented from relocating itself into the Auckland housing market and there will be less demand for NZ dollars anyway.. So whether we like it of not NZ dollar will probably devalue and cost of funding will rise. Slowly that reality will balance things away from 2 and 3 and back towards our number 1 (see Roelofs Credit cycle above). Beneficiaries will be the export market/tourism and credit will move across to those areas of the economy and the other areas that are over the top in the credit cycle, ie. leveraged housing, fast cars, boats and loose women will devalue.

Greg, Of course they will.. The 2 most powerful economic forces are Govts and Central Banks.

NZ will do this in a heartbeat... The precedents have been set. Our Great leaders will simply mirror the responses of the Ero zone and USA ..etc.

The only thing that might limit them is a resurgence of CPI inflation, and/or a collapsing $NZ.

Just look at the ECB balance sheet... Over $4 trillion euros in assets ... which is about 40% EU gdp.. Mind boggling, and extraordinary stuff..

https://fred.stlouisfed.org/series/ECBASSETS

The powers that be will cling to this model of "debt Capitalism".... until they can't.

ie.. Economic growth depends on credit growth... When the next recession comes interest rates will be lowered, even more, to stimulate demand for credit.. Govt will step in and run massive deficits...etc..

( floating mortgage rates will probably become cheaper than fixed rates, like they used to be )

I think NZ can easily handle another business cycle..

Roelof

I understand why you'd think this is an option but it isn't for us. We're just too small.

It's a different game here ... That's like comparing Premier League Football and we're the Wairarapa over 40's league. You can't try and put the little old Reserve Bank of NZ alongside the USA, BOJ, ECB and Bank of England for QE comparison. We try QE here and we will get laughed at and punished by the markets... more likely to turn us into Argentina overnight and they have quite a big one dimensional dairy based economy as well..

Don't believe for an instant that we can swallow the same sort of medicine as the big boys without becoming very sick indeed.

Nic, Its one of the big reasons that Central Banks exist in the first place.... To provide Liquidity when required..

If a Bank in NZ were to become insolvent, the Reserve Bank would enact the OBR, take over the bank ( shareholders would have no equity left) , and be open for business the next day.. The reserve Bank would provide whatever liquidity that is required.

This would not be of a magnitude that you must think, in comparing NZ to Argentina.

If the Shit hit the wall here, I would also expect the FED to step in and provide foreign exchange liquidity.

NZ is NOT an Argentina, nor an Italy or a Greece..

Also, no bank in NZ is as imprudently run as RBS or Northern rock were.

Our Banks are in better shape than pre GFC.

Thats why I asked about your ideas on the credit Cycle.

I get the sense that you think NZ is on some kind of precipice..???

Are u expecting a deep recession , sometime soon..??

Hi Roelof

Precipice. I hope not. Recession, Yes. Deep for me means double dip. but I'd guestimate at by end of Q3 2019 we'll have had 2 negative quarters of GDP already which would constitute the recession term. Looking at the speed of negative movement in asset prices in Australia and the subsequent impact on spending and credit availability it will have there and subsequently on us, I'd say we'll be looking at 4-5 quarters of negative growth as first hit

It's just an opinion but I believe our banks are in a pickle which is why we have the extent of lobbying against the foreign buyer ban. without that cash injection the system collapses.. But for society and democracy it has to happen for the good of the long term future of the country.

Like I said it's just an opinion and for the sensible, good businesses thrive in a recession anyway so it will only raise the bar.

Nic

Roelof

I don't believe that our banks (the Aussie banks) have been any where near as prudently run as you seem to think they have been. And regulation has been sadly lacking. The multiples of lending and quantity of interest only credit has been very similar to the generosity of the UK banks that no longer exist. Mortgage stress in Australia (and lack of a household savings buffer) is likely to create challenges within the next six months.

We'll see I guess.

Look, if prices were a bit saggy, or a bit toppy, I agree you would be pointless to try to time the market and you should just buy a home if you needed one. But this market isn’t “toppy”,it’s bat sh!t crazy. Us, Australia and parts of Canada are just off the charts in terms of affordability. All the lights are flashing red for an unsustainable credit bubble. And looking in the rear view mirror we have some prime examples of where unsustainable credit bubbles can lead. So it seems entirely rationale to me that a purchaser would take pause in this market and bide their time. I know some people talk the about the futility of timing the market, and in normal markets I agree, but stand back and look at this thing happening here, it’s a massive credit bubble, it is far from normal. Even if you could afford to buy, at current yields it is be materially cheaper to rent in the short to medium term, so if you are in a rental that meets your needs it would be reasonable and rationale for someone to decide to stick with that for now.

After having been in the residential property leasing business in Auckland for over 20 years, that is the reason for exiting that business in March 2017. What were the early warnings of elevated house price risk and vulnerability in Auckland you may ask?

1) July 2016 ANZ NZ's CEO, David Hisco's warning - when someone who has an informed viewpoint and is speaking out against their own financial interests, it is definitely time to take note.

2) the numerous news stories of bidding frenzies at property auctions in Auckland and the fear of missing out in June - September 2016, where property buyers were purchasing regardless of price and valuation considerations (reminded me of similarities of buying behaviour during the internet price bubble)

The current financial economic conditions in the Auckland residential property leasing business are at extreme levels where the current level of risk is much higher than the current level of potential reward.

So many in the residential property leasing business in Auckland who are highly leveraged are looking at the misleading metrics (population growth, undersupply of residential housing, extrapolation of historical property price growth) and arriving at misleading conclusions about the future potential rewards in the residential property leasing business in Auckland. How would highly leveraged property owners deal with a credit crunch? or a liquidity crunch? High debt levels mean reduced financial flexibility to handle this possible scenario - many may be unprepared.

If I were a potential first home buyer in Auckland, then I would not be looking to buy until property prices were at much more affordable price levels, given that renting is cheaper than owning in many suburbs in Auckland. By renting and avoiding buying at current property valuations in Auckland, and taking on high debt to income levels, you reduce your risk of being collateral damage. Keep building that deposit for that buying opportunity.

Property leasing/investment vs buying a home are two different worlds. I don't think you should confuse the two because each has its own motivations. There are more personal reasons for buying a home to live in and what type of home to buy and where. This decision should not come down to straight financial return of the cost of rent vs the cost of ownership. Furthermore property prices as a whole have rarely if ever dropped in nominal terms so homebuyers don't need to worry about that. Get a home, pay off the mortgage and over the long term that is a recipe for success.

Agree with you that buying a house for owner occupier is different than for a property investor. There are many other non financial considerations, however the risk and vulnerability to house prices in Auckland is very high in my opinion.

It really depends on the owner-occupier buyer's opinion and expectations of future Auckland house prices and their ability to hold on and continue to service the mortgage in all economic conditions. Under normal conditions, this would be a mute point, but under current conditions in Auckland, this assessment needs to be made to avoid being collateral damage. The house is normally the family's largest asset and forms the base for retirement assets for most retirees.

Many owner occupiers of property in Auckland are comforted and gain confidence from history over the last 50 years whereby nominal property prices in Auckland have not declined by much if at all. While nominal property prices in Auckland have rarely declined, it doesn't mean that they won't decline - they declined 10% on average in Auckland in 2009 during the GFC (and current conditions in Auckland are at higher vulnerability than they were back then). They are also about 5-8% off their current highs in a very strong economic environment - so what could happen to property prices in Auckland if there is a very weak economic environment? In other property markets around the country, residential property prices have fallen quite dramatically at some time in the past (e.g. West Coast, Hawkes Bay, Tokoroa, Northland, Southland). Commercial property prices in Auckland fell significantly in the early 1990's. Also residential property price bubbles and credit bubbles form over very long timeframes (many many decades) as banks slowly relax their lending standards and as senior bank executives change so that those that experienced the property bubble hand over the reigns to those who have never experienced a credit bubble - New Zealand had a land price bubble in the 1870's and it is possible that property prices in NZ fell in the Depression of the 1930's. (note the period between property price bubbles was about 60 or so years)

1) If owner occupiers or potential owner occupiers believe that they will not fall much further from these levels in Auckland and the owner occupier can continue to service the mortgage under all economic conditions, then please stop reading any further.

2) For those who believe that Auckland house prices could fall further, or an owner occupier who may be unable to continue to service mortgage payments under all economic conditions and changes in personal circumstances, this is the collateral damage it can have on owner - occupiers. It can set back an owner-occupier's financial security many many years and sometimes the damage can be permanent and non financial. This is the reason that I highlight risks to highly leveraged first home buyers and highly leveraged owner-occupiers in Auckland - the non financial toll can have many long lasting effects, sometimes even life lasting.

a) https://www.npr.org/2016/05/22/479038232/a-decade-out-from-the-mortgage…

b) https://abcnews.go.com/Health/MindMoodNews/story?id=4873943&page=1

c) https://www.youtube.com/watch?v=BfcSWLJBIRg - and the other side of the story - https://www.youtube.com/watch?v=m25FXP9O7dE&feature=youtu.be&t=3m44s

Property clock, did you get that from one of your property investment courses you went on? How is Ron Hoy Fong?

You're on the money there Rick.

As a FHpotential buyer with a 20% deposit I'm sitting back looking as auction rates flounder in the outer burbs of Auck, prices have peaked and some sellers are dropping prices below what they thought their home was worth last year.

So why rush in now?

What effect will the overseas buyer ban have on existing houses in central and oh so popular dgzs, and as prices rise from there and ripple out isn't the same true if they fall?

We have registered with the KB program but will not necessarily purchase one if offered. But it creates options where before there was none. We couldn't buy a Mcmansion so that leaves competing with speculators, mumndad investors and other fhbuyers for a shitbox on the outskirts.

Funtimes right?

How long have you been a FHB for, Randomman?

It's getting harder to distinguish between 'the smart enough to act stupid, or the just stupid' efforts of this Govt.

The announcing of Kiwibuild, and then asking for registration is a dangerous tactic, which I don't think the Govt. have considered, or care about if they have.

That is, when you advertise about a future event, what you are effectively doing is pulling future demand into the present. This is a good marketing tactic to grab more of tomorrows market share from your competitors.

You are effectively saying, 'while you cannot buy of me at present, don't buy elsewhere, wait until I am ready because my offering will be better.'

As a business, you are creating supply for your product, but it is not adding more supply as it just moving demand from your competitor to you. Your competitor will lose business, or will lose control by having to become subservient to you as a sub contractor.

Further when you develop and sell off the plan for multi unit developments like apartments, as they take years to be develop, and always take longer than expected, the free market is at risk of you not only taking that future demand, but locking it up, ie freezing the market in other words. The purchaser is locked into all the delays - and the broken promises. And your sub contractors take on a lot of the risk for delays that they have no control over.

We are already seeing this happening with projects being delayed by years, if starting at all.

This can have very negative effects, as affordability in a stable market is contingent on supply meeting demand in developer real time (within 6 months from the demand signal).

The effect of locking up demand, not adding to over all supply, and not delivering when it's needed, if at all , in a housing market that as serious speed wobbles, will not be pretty.

Dale Smith

You've got that completely wrong way around. What has just happened is that short and medium term demand has just evaporated.. Supply however is quite healthy already and is likely to rise even further still as Spring arrives.

Anyone holding a leaky dog-box that they were hoping to get over 650K for is going to have to dramatically adjust their selling expectations because medium term buyer expectations have just been re-calibrated towards something that is New, well insulated, doesn't leak and smell of damp. That's why some of the Auction results this last couple of weeks have been woeful - what was it 0 from 16 in one location this week.

Think about it again and what I've just said will make some sense.

You need to read my post again. I am saying that demand has 'evaporated', by Kiwibuild locking up that demand with a promise that many won't qualify for, or won't want to qualify for, at the end of the day.

And yes, as a relative option, older housing stock may lower their expectations to successfully compete with the kiwibuild stock. And this could happen just because of what kiwibuild is promising - not because it has or will deliver on their promises.

The kiwibuild process is adding further instability into a market that is already unstable.

The irony is the process (as opposed to needing to build more affordable housing) could cause house prices to fall before they every get around to (or needing to) supplying the market with housing.

There is two ways to have affordable housing, you either have a command and control non presumptive right to build restrictive land zoning that causes boom and bust housing cycles (like we have) and that makes housing more affordable for some in the bust phase, OR you have a presumptive right to build, less restrictive land zoning that causes a stable market with no boom or bust and prices are consistently affordable.

You can't get more much more command and control than Kiwibuild.

Outstanding post, Dale, it's great having some commenters with brains on this site

[ Unacceptable insult. Removed. Ed ]

That’s rich coming from the poster that coined their Houses Overpriced moniker when median house prices in NZ were 67% of what they are now. Immeasurably worse if you were looking to buy in Auckland. How wrong can someone be? That’s a life changing call. No wonder you post so often full of bitterness.

The elephant in the room is:

"Thank goodness for low interest rates, and one shudders to imagine what happens if there is some sort of horrible shock that sends those rates up again to the sort of historic levels we have had."

Yeah; They say for the same reason the bankers, politicians and policy-makers will keep the rates low, by manipulating something. Too much debt is not good, we all know. But If most of us are in debt.. then it becomes a normal thing to have

Hi Greg

Don't be fooled into believing that our banks or our Reserve bank have any genuine control over what happens with Global interest rates and what we can do. We are a tiny economy and I think I read somewhere that 'Apple' is bigger than NZ economy.

Joe

Don't be fooled into believing that our banks or our Reserve bank..

Its not like I get 'fooled' by banks / policy makers; I'm actually scared of them making debts 'normal', which would make debtors winning and savers losing...I like to see the principles of economics proved correct i.e debt should be paid back .. :-)

A question considering our economic principle: (Theoretically) suppose a bank collapse happen . Who will suffer more ? A saver with $150K in his account ? or a debtor with $250k mortgage on a property he bought for $400k .. with the OBR and haircut thingy ??

Thanks in advance

Greg

You've got me there. and to be fair for someone who suggested a shortage of knowledge this morning, you're far better informed than you give yourself credit.

I was in the UK when the UK banks got bailed out and in the long term savers suffered for years I(as they have worldwide) but no one got a capital haircut in UK. Greece, Cyprus different story.. A lot of overleveraged borrowers however lost tens and sometimes hundreds of thousands off the capital in their houses though and some, to this day have never recovered that value or are still underwater..

I don't think that the NZ government would dare enact the OBR, however it's the Aussie banks that are in the hock for our debt and they have just gone ahead and added an OBR to their system too so in essence NZ$250 billion and AU$1.7 trillion in housing debt is on the banks books if something goes wrong.. It is already going wrong in Aussie. and unlike UK, NZ is in a precarious position in this instance in that we don't actually control our banks or really the regulation of them (I don't buy that the sharp practice didn't transcend the Tasman Sea) . So, If one goes... it is quite likely that a larger international bank would gobble them up and depositors would be okay (government structured buyout with a guarantee to them on behalf of depositors.. No one will care about the leveraged but old retirees with savings will always be looked after as they don't have time to make up the losses).

I'm glad you've understood the risks though and that was a thoughtful question.. If I were you and saving cash for my first house today and wanting a return but not wanting to risk it in the markets then what would I do? I would probably be dividing it in equal balances between all the banks to reduce my cash risk to a failure by one of them. if that helps. And remember if a bank goes pop I would be saying all bets are off on housing, buyers will disappear and houses are overnight 20% cheaper by default. 40% cheaper if 2 banks go in quick succession.

Oh yes and those that get this right over the next couple of years will trim a decade off their mortgage commitments.

You know that the young whizz kids and not so young sceptics here will question what you have to say Dale Smith, whilst they look at the housing supply problem and ask why it would take years to create the promised supply. Personally I know the councils are crazy about regulation. And they are just too slow to respond to the needs of developers so developers and builders just say "too hard, I won't bother". And that's what's happening, there are less developers to get things moving. Good example is the Eden park baby incubator concert. Everyone recognises the problem but the cost and process stymies the response.

I read somewhere that the resource concent process , to get permission to have the concert was going to cost $750,000 + lawyer fees..

AND... It would take till Oct to get a ruling..

(Its' not as if Eden Park does not already exist..and is actually already a stadium...)

This pretty much sums up the insanity of things .... of bureaucracy..

This bullshit is a cancer that is choking NZ... A Public Sector that has lost perspective....that thinks it is King rather than servant. ( In the old days they were called public servants )

They are disconnected from practical, commonsense, economics

https://www.stuff.co.nz/auckland/105700049/Eden-Park-Trust-to-meet-on-w…

No, the insanity was throwing 100s of millions of dollars into a stadium that is in the middle of a residential area and which is an absolute dog. It’s not a great venue for rugby, it’s too big for most uses (it is hardly ever filled or even close to filled). I can entirely understand residents of what is overwhelmingly a residential neighbourhood not wanting to put up with concert nights where they essentially lose the amenity value of their own homes. It has nothing to do with”bureaucracy” and everything to do with dumb decisions made so we could host a 3 week rugby tournament. Who cares. The money poured into Eden park and pretty much wasted is an absolute scandal

I can entirely understand residents of what is overwhelmingly a residential neighbourhood not wanting to put up with concert nights where they essentially lose the amenity value of their own homes.

You would have to question their level of entitlement (or intelligence) if they moved next to the stadium then started complaining about it. The stadium has been there for a long time.

So have most of the motorsport venues in NZ, and they all get more and more restrictions on them. Pukekohe racetrack, Western Springs etc.. Ditto with noise complaints about noise from the airport or motorways.

Instead of restrictions we should be nailing up "Harden up, sunshine" badges on houses whence these shrieks spring. If they're grown up they should be able to evaluate an area they're moving into...and it's hard to miss a big, hulking stadium.

Oh dear, please try keep up. No one has a problem with rugby and crickets matches, although there is i think a restriction on the number of night matches. Anyway, it seems to me the big rugby and cricket night matches can get played as they wish. But people do quite rightly object to pop concerts. A venue like that needs to be multi use, and it’s can’t be as it is slap bang in the middle of a residential area. Repeat after me.....it’s a dog. Time to be intellectually honest, bowl it over and build a smaller multi use venue.

That's fine with Eden Park, no need to use it for pop concerts. However, be honest - shrieking occurs next to Western Springs regularly too, and that has long been used for speedway and concerts, before the shriekers moved in. And are there really no complainers around Eden Park sports matches, traffic etc?

It's certainly a phenomenon of folk moving next to stadiums, farms, rifle ranges etc. then having quite some level of entitlement when it comes to trying to move those venues out.

I wouldn't say Eden Park is a dog. Pretty good sports stadium, in my experience. Wouldn't make financial sense to shift it out because of the odd anti-libertarian resident moaning.

It’s a very second rate stadium for rugby, it is not a purpose built rugby stadium and in many parts the seating is too far away from the playing field. Look at SA for what a purpose built rugby stadium needs to look like

It's a crap stadium in a poor location. Bowl it and build 2000 apartments

Please, we need to be more precise, it is a sacred cow to the hoi de poloi of Auckland.

Ill leave the ruminating on milking it to others.

Yeah, but it was purely a rugby and cricket stadium, no concerts. Nor were nights games a feature in the distance past. It’s the wrong thing in the wrong place, it’s too big and the things it needs to do to break even like concerts it can’t do without significant restriction due to its location. It’s a complete dog and the money that has been sunk into it is a total scandal

Like saying (in relation to the stadium), I have a house but because I don't like something about it I won't use it. I will stay out in the cold where I'm likely to die. Great logic bobster, some of the best I've seen from you.

Wot? Nonsensical.... Oh dear, engage brain, then post.....that’s normally how it works

That's your tactic when you haven't got an answer

Err, no, it’s that what you said didn’t even make sense. Just for a change.

I will spell it out for you then. The asset is Eden park. You say it's in the wrong location. It's there already. So then don't use it? Maybe you are one of those pushing the new stadium agenda

Because the use they are proposing (pop concerts) is a new form of use which imposes unacceptable adverse effects on local residents. We need to take some note of these effects, right? This stadium just cannot be the multi use venue it needs to be to pay its way. To be honest, it’s a pretty ordinary rugby venue as well. It was well known as the time this money was sunk into the stadium that it was not clear that it would be able to perform this function, but the money still went in so we could get 3 weeks of a rugby tournament. Woopy doo

And no, I’m not pushing a new megastadium agenda. Eden park is a dog. There should be a new medium sized multi use stadium on the isthmus (30,000 pax or so) but it should be purpose built for rugby and league and should be somewhere we it can be used whatever night of the week is needed. And cricket could go to an oval somewhere with substantially reduced capacity, something like a smaller Adelaide oval. I would be happy to see cricket at something like that, I have no interest in watching cricket at Eden park. It deserves to be bowled and turned into a residential area

Just as well you are not a ratepayer then so that you dont have to pay for that wish list of wants.

Haha, nice troll

As far as I know, its been there since the early 20th Century .. it is where it is.

If I bought a house near Eden Park, I would take for granted that the Stadium will be used.... and will be noisy.

I pretty much agree with agree with u thou. ie... should have been shifted etc..

My argument is that it should cost $750,000+ and take 3 mths to say ya or nay...

Personally I know the councils are crazy about regulation.

I cannot see the problem getting better without some level of reversion to demanding a level of personal responsibility and integrity from the construction sector.

Take the leaky building saga. We allowed the construction sector to dodge responsibility for creating leaky buildings by saying "But the council didn't stop us from building them leaky. They should have stopped us. It was technically legal for us to build them leaky. Sue them."

They took the profits, socialised the costs, and have incentivised the council to put more and more regulation in place. The combination of limited liability-based walking away with profit, and socialising of the risk and cost, can only ever end up in more and more complex attempts by the council to avoid future similar costs.

Rick... I think its more subtle and complex than that... Read linked article, for me it was very imformative

http://pc.blogspot.com/2009/11/leaky-homes-part-1-myth-of-deregulated.h…

THE BUREAUCRAT WHO BEARS the greatest guilt is a know-nothing called Bill Porteous whose agitation for more building regulation and an “Integrated Building Code” leveraged him into the job as head of the new bureaucracy set up to oversee the building industry, the Building Industry Authority.

Good article, thanks Roelof.

Good link roelof thanks

Yes leaky buildings has added to the complexity, although there are more catalysts than just leaky buildings but that is one. Possibly another that councils will take note of will be the Bella Vista saga. And councils are becoming more risk averse. Instead of either insuring the risk or living with a level of risk they are trying to de-risk completely. Everyone I know from developers to REAs to contractors are complaining a lot about the regulations and delays. Even after getting consent just getting inspections is frighteningly slow, it didn't use to be this bad. The downtime is frustrating and unaffordable for the smaller companies.

Does anyone know of the progress of the foreign buyers ban of existing houses. What date would this likely take effect. If I was a first home buyer in Queesntown or Auckland I would wait until a few months after this comes in to make any move. The effect of this policy seems to be one of the hardest things for experts to predict, but either way it's not pushing prices up.

Are you a fhb somewhere else or why the interest Jamin?

Hi houseworks. I'm a kiwi who was born and raised in Queenstown who takes a keen interest in real estate. I feel anyone who thinks this ban will have no effect hasn't seen what I have seen. Queesntown more than anywhere needs this policy to be passed un-watered down.

Bless you jamin. Queenstown really does look like a disastrous failure of public policy. Foreign sales and air bnb have had a major adverse impact on the quality of life of locals who struggle for accomodation. The tourism boom has also drastically increased the demand for middle to lower quartile accomodation in Queenstown. I think both central and local govt need to take drastic steps to sort out the mess in Queenstown.

I can understand your viewpoint as a (former) Queenstown local. I don't agree that the legislation will have the effect you are hoping it will though. Without the "foreigners" buying, other NZers, Australians and Singaporeans will still buy in Queenstown. Thats right, the legislation does not apply to all those groups and it's a small market with strong demand from Aucklanders (a kind of foreigner). Also the foreign buyer ban will have to be totally watertight to stop foreign buyers completely.

Hi house works. I still live in Queenstown btw. My point is that with no real reliable data on this subject, we really won’t know until it’s implimented. Wait and see then.

The biggest effect will be at the higher value properties as foreign buyers really are setting the values there. Short term economic benefits for the builders ect, but the long term effect has been to take the best locations out of kiwis hands permanently. Is this a good outcome for New Zealanders? I don’t think it is.

Janin, it's a real hoot when Houseworks, a late comer to Hamilton's peaking property market, can predict Queenstown better than a local! (Thinks he can)

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

You duffer. I've told you before we are longtime investors yet you continue to distort the facts like it's a sick joke. No one should believe a word you say.

Houseworks, nice try at deflection - it's no sick joke. You bought a neglected rental in Hamilton a little over a year ago, refurbished it and now pine for 2015/16 days again. Stop changing your story by coming across as a long term experienced investor now that the boom is over buddy. The point is, for the sake of returns, you no longer have a choice but to remain committed financially and prey for sunshine.

Instead of worrying about me and what I have done why don't you focus on yourself. Early in the decade you followed the flawed advice of "guru" Bernard Hickey. Where has that got you?

Houseworks, like TTP, masking embarrassment is not one of your strong points. Many like yourself discovered they paid top dollar. It's just not your time zone that's all.

Thanks retired poppy for your eventual reply, but why didn't you answer the question? Maybe it's because as my wife describes you, you are a half wit talk wannabe polly.

Houseworks, try not to become so aroused next time I fail to dignify such a stupid question with a matching answer. Yet again a comment posted by you that illustrates a primitive individual having a (play). Try not to be so hard on yourself!

Now here's your answer. Now ya ready? I've never hung on the words of individual economists. Its instinct and open mindedness that got me where I am. Suggest you refrain from those property seminars once and for all. You're a bit of a financial hazard to be honest.

RP...sounds like you are creating marital strife fro HW. Cut it out....

Aaah .... the sound of silence when retired poppy is muzzled.

Houseworks

Now really, think about this some more.

'a small market with strong demand from Aucklanders (a kind of foreigner). Also the foreign buyer ban will have to be totally watertight to stop foreign buyers completely.'

Houseworks seems to think that Aucklanders will have anything near the buying power they've had when the foreign injection of hot money is removed!

For every injection of cash, three, four, five maybe more transactions take place off the back off that initial transaction as the chain of events leads to others trading up and down the market. Remove them and you rely on good old average Kiwi's Joe's and Jane's earning enough money to get a mortgage to buy a house.

You really have no idea how this ban will massively impact the market liquidity do you? Let try and explain it as simply as I can..

Bob sells in Remuera to Mr Chan for $2,000,000 cold hard NZ dollars. M Chan gets a leg into the NZ market.

Bob uses the money and buys in Hastings for $1,000,000 and another place in Queenstown for $1,000,000.

Jane (Bob's purchase in Hastings) buys a smaller place in Hastings for $600,000 and a buy to let in Wellington region for $400,000.

Derek (Jane's $600,000 purchase in Hastings) - downsizes in Hastings and buys house for $400,000 and puts $200,000 in the bank for retirement

Abigail (Jane's purchase in Wellington) moves into a nursing home and gives her kids $150,000 each to pay off some of their mortgage.

Trudy (Bob's purchase in Queenstown) - realises that this is all madness and sells to Bob and moves into rented to watch the carnage.

And without Mr Chan buying Bob's house....... Well in pure and simple terms none of them are worth anywhere near what they think they are worth today as the banks can't plug the capital shortfall. Why else do you think John Key sold out when he did?

Hopefully that helps explain things

Nic, we have already seen that you cannot get your Davids straight so this is not a good example for you to use. BuyLow identified that's because you have property envy, which of course stands out like a wart on the end of your nose

Houseworks

Does your mother know that you're still awake, using the computer and talking to adults that you don't know on-line?

Have a good weekend kiddo

Nic

The bill is in a committee consisting of all MP's that haggles over its contents for an indeterminate time.

But if the goverment gets sick of them it can force closure, I believe and the bill will go to a final vote.

We will wait....

In June the minister has said that the bill should pass in July but may be have to wait till next month August.

Very good question!

David Parker claimed it was going to be law by the end of this month.

https://www.interest.co.nz/property/94195/associate-finance-minister-da…

FHB as have already been said earlier also have already missed the bus (This time) so why rush.

FHB should buy for long term but now is the time to wait and watch and if something suitable comes ones way that one feel is a deal should buy but should be for long term.

To answer your headline: There is no liquidity left in the market. Prices can't be sustained because the gap between deposits and finance is too great.

"the gap between deposits and finance is too great"

I don't think that's true, do you have data to substantiate your claim please?

I don't think...

There's your data.

[ Unacceptable insult. Removed. Ed ]

Strong rumours that kiwi build houses are going to be very small (no information on this?) and are being stripped out to keep cost down. Also possibly stand a lone houses are unlikely to be built in Auckland -more likely apartment type builds. Also that the extent of the possible savings from pre fabrication building could be raising false expectations. Along with the mix of "social" and kiwi build houses may make for some interesting neighbours with Labours enthusiastic approach to rehabilitation. Check out Alexanders latest BNZ news.

Look forward to Labour providing more detail to their plans to reassure FHB.. Admire Labours efforts to try and do something about awful FHB situation.

[ Unacceptable insult. Removed. Ed ]

Maybe more than a rumour than you think. Don't get me wrong, hope labour comes through but withholding basic information like floor area while 31,000 people sign up is just not a happy situation.

[ Unacceptable insult. Removed. Ed ]

As one of those that has signed up I have no idea why you think it is not a happy situation? We basically put our names on a mailing list, we will get more information as the houses are built and are ready to be "marketed". We will certainly know a lot more about them by the time it comes to make any sort of decision that would tie up our resources.

Its no different from signing up on a developers website to be kept up to date on the progress of a new subdivision development in the early stages.

probably. do you

[ Unacceptable insult. Removed. Ed ]

Ronn, don't bother engaging with them. There is no profit in it. Your comment seemed okay to me.

I hear your anger and frustration. Least Phil is trying.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.