More banks are falling into line with carded rate cuts to home loans.

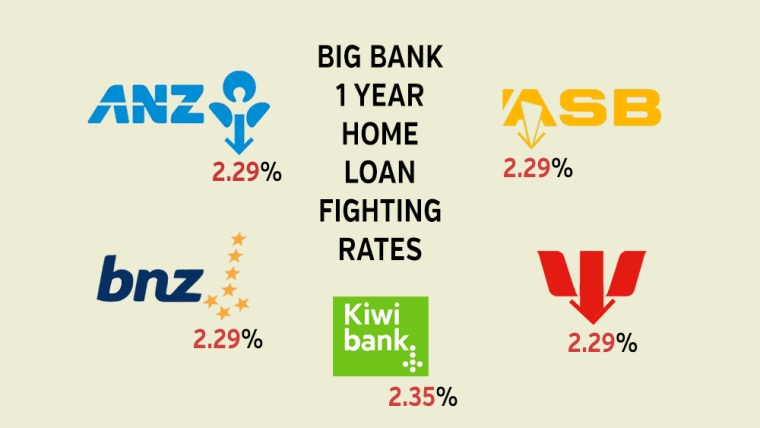

BNZ is the latest. They have adopted the 2.29% one year fixed rate first claimed by Westpac.

But they have also trimmed their two year rate to 2.59% and matching ASB for that term.

It is starting to look like trailing banks are going to do the minimum to remain competitive.

We are awaiting rate change announcements from ASB and Kiwibank, which will surely come soon.

Update: ASB has also now cut its one year fixed rate, also to 2.29%.

Further update: Kiwibank have announced their one year fixed rate will reduce to 2.35% on Monday, January 25, 2021.

Carded rate changes are one thing, but on the front lines, most banks will match the market lows of their main rivals if you ask them (provided your financials are attractive enough).

Currently, the lowest one year rate is from Heartland Bank at 1.99%.

The lowest 18 month rate is from HSBC at 2.25%.

The lowest 2 year rate is from Heartland Bank and HSBC at 2.35% and TSB's 2.49% also undercuts the main bank levels.

Remember, the RBNZ's Funding for Lending program is in place, allowing banks to access money at the OCR's 0.25%.

If banks use that funding line, they can still keep their margins intact with rates down to about 2%.

Only one bank has drawn $1 bln in the FLP line late so far, doing so late last year. $1 bln is enough to fund about 2000 home loans.

In today's move, BNZ did not change any of its term deposit offers at the same time.

One useful way to make sense of these new lower home loan rates is to use our full-function mortgage calculators.

And if you already have a fixed term mortgage that is not up for renewal at this time, our break fee calculator may help you assess your options.

Here is the updated snapshot of the lowest advertised fixed-term mortgage rates on offer from the key retail banks at this time.

| Fixed, below 80% LVR | 6 mths | 1 yr | 18 mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| as at January 22, 2021 | % | % | % | % | % | % | % |

| ANZ | 3.39 | 2.29 | 2.55 | 2.69 | 2.79 | 3.90 | 3.99 |

| 3.39 | 2.29

|

2.49 | 2.59 | 2.65 | 2.99 | 2.99 | |

| 3.39 | 2.29

|

2.49 | 2.59

|

2.79 | 2.99 | 2.99 | |

| 3.55 | 2.35

|

2.65 | 2.65 | 3.09 | 3.19 | ||

| 4.15 | 2.29 | 3.25 | 2.69 | 2.79 | 2.99 | 2.99 | |

| Bank of China | 3.45 | 2.55 | 2.65 | 2.65 | 2.75 | 2.85 | 2.95 |

| China Construction Bank | 4.70 | 2.65 | 2.65 | 2.65 | 2.80 | 2.89 | 2.99 |

| Co-operative Bank | 2.49 | 2.49 | 2.69 | 2.69 | 2.79 | 2.89 | 2.99 |

| Heartland Bank | 1.99 | 2.35 | 2.45 | ||||

| HSBC | 2.79 | 2.25 | 2.25 | 2.35 | 2.65 | 2.79 | 2.89 |

| ICBC | 2.89 | 2.89 | 2.45 | 2.45 | 2.65 | 2.89 | 2.99 |

| |

3.39 | 2.49 | 2.49 | 2.59 | 2.65 | 2.89 | 2.99 |

| [incl Price Match Promise] |

2.89 | 2.29

|

2.49 | 2.49 | 2.65 | 2.99 | 2.99 |

In addition to the above table, BNZ has a unique fixed seven year rate of 5.20%.

Fixed mortgage rates

Select chart tabs

42 Comments

And coincidentally my last PIE term deposit of many before it at BNZ matures today. It will be going to Harbour's Enhanced Cash Fund with all the others.

I now have less than a tenth of the deposits I had in BNZ and Westpac 18 months ago left. By 1 April every TD will be elsewhere and not with the banks.

I got pretty annoyed with the low interest rates but decided to put a good chunk in Kiwi Bonds-why? The returns are near similar but they are guaranteed by the Gov. We've left some in normal accounts so that should we want to move quickly eg deposit on house, stick some into ETFs as per March this year, we have that facility.

So the market leaders are dropping their 'prices'.

An indication of slowing 'sales' and the fight for fewer customers perhaps?

They're trying to appear competitive, more or less they are one in the same though - making huge profit for their shareholders at the expense of kiwis.

But where is that profit coming from? Lower interest rates = less revenue for the banks!

Volume.

All happens in the margins....

Lower costs of borrowing, 0.25% FLP for example. Paying $2,500 to RBNZ to borrow $1m and getting $23,000 for on lending has got to be profitable.

So is the RBNZ subsidising bank revenue?

Not wanting to insult your maths, but that does oversimplify it. Remember the ONE bank has taken $1b in RBNZ money. But these banks have hundreds of billions of home loans... but the low rate is offered to all.

gypsy, the profit comes from the banks borrowing the money cheaper from the RBNZ (courtesy of A Orr), lower revenue for the bank yes but not lower profits

"Reserve Bank figures showing the amount of interest charged on residential mortgages go back to the September quarter of 2014. These show the $2.6 billion charged in mortgage interest in the September 2019 quarter was the lowest it has been in any quarter during that period, and was well below the peak of $3.11 billion in the fourth quarter of 2017."

https://www.interest.co.nz/property/108685/once-threat-covid-recedes-we…

Sort of indicates falling revenue from mortgage lending, it would be interesting to see that graphed.

Lower revenue but not profit (as per my post above). I assume you know the difference

I do hence why I used the term revenue rather than profit, but your theory about the flp falls down because only one bank has dipped into it in any significant way.

I got 2.3% from Bnz in November. Hopefully it will be circa 2.1% by year's end.

Yep locked mine in early dec, fingers crossed they stay this low for another 11 months ae.

Think it might be prudent to lock some up for 2-3 years then just based on historical trends

Yeah it might be ey. Although my view is the OCR is unlikely to go up much at all in the next few years

Fritz, I thought you were concerned about inequality et all? surely you hoping for lower interest rates is not consistent with your moral compass?

You can hate the game but still play it.

Yep. The herd may be stampeding for no reason, but running with them is often the safest strategy to avoid being trampled underfoot. Just make sure you're not the last one to stop running.

Is it acceptable then to be be so judgemental and critical of the herd when you're part of it? Sounds hypocritical to me

It does sound hypocritical, yes. That's why I try to remain non-judgemental. Personally I'm not running with the herd, I'm just along for the ride.

My investment property is being built and ready for prime time selling in March, when I hope the interest rates from the major banks will be closer to 2.0%. You can't get a better time than this to sell! FOMO + lowest interest rates in history + lack of stock = win win win. Yes, I will be taxed but hey, it's nothing compared to the gains.

Come Feb, and should Labour release a policy that makes it harder to get into property, it would be even better for me personally considering the FOMO levels will be elevated further just prior to any new policies being applied.

Thought... what happens if there's a lot of investors selling at the same time as you with the same thinking. There's got to be quite a few investors getting out of the market around that time due to the new tenancy laws. Could be a lot of stock which could push down prices. Perhaps not the best time to sell after all?

Would be pretty hilarious to see this sort of scenario pan out. A bunch of dunning-krugers all flooding the market at once.

Every stampede has a tail end, and it wouldn't be surprising if the pent up demand is satisfied a lot quicker than people expect.

As our tenants' whims change and if they decide to move we'll consider what to do about renting them out. All the tenants are good now, mostly sickness beneficiaries who'll never do formal paid work again. They mostly look after the property and we get maintenance done promptly which they said was unusual in previous rentals. Unlikely they'll now find somewhere cheaper than what they currently pay which is below market, particularly a rental they can take their pets, but if any move I'll have to consider options like air bnb in view of new rental laws.

Can see rental scenario turning into full blown crisis after 11 Feb. Had a young mother, about 18 calling desperate to move in to our rental this week with a new baby, father not on birth cert get more benefit, already got bad credit too so no, sorry, move along.

And who are you going to be renting these Air BnB's out to? International tourists won't be here for at least another year and domestic tourists aren't compensating for them.

Albert, how do you know domestic tourists are not compensating ? How many Airbnb's do you own to make such a statement? I own accommodation that I rent out to guests on Airbnb and others platforms and from my experience there are a lot of Kiwis with lots of money to spend on domestic holiday accommodation

If you think how many buyers there are right now vs listings, I don't think it will change over the next 3 months.

Edit: This is in reply to Nifty1.

Well aware of the current situation but I also know of family and friends that are being kicked out of their rentals in February so that the landlord can sell. Could be alot of ex rentals hitting the market end of Feb/March.

Is this responsible RBNZ regulatory oversight?:

Banks extending 60 % of their lending to one third of already wealthy households to speculate in the residential property market because the RBNZ offers them an RWA capital reduction incentive, to do so.

{kind=link}

Or this:

RBNZ cutting OCR in half five times since July 2008, causing the rich to capitalise rising discounted present values of future asset cash flows.

{kind=link}

So you call building something with the intention to sell within 6 months an investment? I think this is the perfect scenario where it is actually a trade and capital gains should apply

@Uh Oh - yes, I would be paying tax on the gains, I am not saying tax wouldn't apply. However, when I am making over 100k, who cares what tax I have to pay. This is the reality folks, I am not the only one.

The country actually needs more of this. Investment needs to assist in building the housing stock if the crisis is going to be resolved. Investors pricing up existing stock is a recipe for disaster, especially when they're competing with FHB.

Hopefully RBNZ don't take away the punch bowl.

Don't worry they won't, they have made it abundantly clear, so has the government

I guess we will not see the 1.5% that I predicted several months ago in March 2021 but I'm still a bit surprised to see them still dropping at this point in time, I mean the MSM is banging away on how well our economy is going and how little Covid has affected us right ? So why are the rates still falling. If everything was peachy they would be going up not down to try and rein in house price hyperinflation.

Banks want market share at the end of the day. I am predicting we will see the major banks go down to 1.99% for 12 months fixed at some stage over the next 3-4 months just for publicity.

More mortgage war are on the way for most part of this year, as most Kiwis secretly already known. As the only safe heaven for investment, with assurances by the authorities clearly shown.

If this is not a signal to buy now, increase your portfolio or rebalancing your holdings, I don't know what is. Opportunities are rare, it takes a prepared mind to size it.

I had a loan come off fixed 2 days ago and had a wee feeling this might happen so floated for a couple of days. Hooray.

People will soon take money out of the bank so there will be zero lending. Dave Chaston wrote in December that banks were full of customer deposits as deposits have risen sharply... Now I'm confused.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.