It's bad news and good news from ASB economists regarding household living costs.

Yes, they say, costs are going to keep going up - but it will be at a slower rate. And they say, unlike in recent years, the next year's cost increases will be beaten by rises in income.

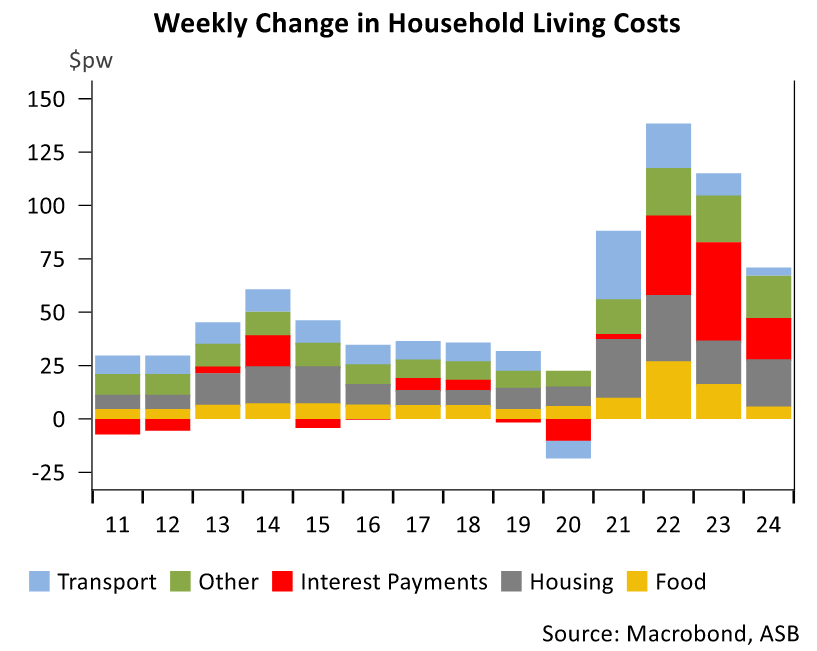

In a household cost of living outlook for next year, ASB senior economist Mark Smith is estimating that for 2023 average household living costs for Kiwis will have risen by $115 a week.

Weekly cost increases for the average household peaked at just under $140 in 2022, he says "and again look set to top the $100 per week mark in 2023".

"In both of those years, rising living costs were higher than gains in household incomes, reducing household saving buffers. Households have been acutely feeling the cost of living ‘squeeze’.

"The outlook is uncertain, but signs for 2024 are brighter, with our estimates suggesting the average weekly cost increase for households will ease to $70 per week. This is expected to be below the weekly rise in household disposable incomes."

Smith says cost increases for 2024 are likely to be the lowest annual increase since 2020, but they are still elevated relative to pre-covid times where the low inflation environment kept overall cost increases in check.

"We caution that these are average figures, with fortunes differing by household. Rising living costs will be a struggle for many households."

Smith says higher living costs are a significant headwind, but to date the household sector has coped reasonably well overall. In part he says this is a consequence of the covid-19 period when overall household incomes benefited from government support.

"Record low household borrowing costs and the resilient economic backdrop have also played a role, with household disposable income growth at solid rates. Kiwi households are not dissaving in aggregate. Kiwi households have built up a circa $30 billion nest egg of savings since the COVID-19 pandemic. The amount of saving is being eroded as growth in household expenditures has outpaced income growth. Still, households in aggregate are still saving."

But Smith says the concern is that the households who have built up the savings will not be the ones who need to find additional funds to cover higher living costs.

"It will mean considerably reduced funds available for households after paying down the mortgage, with discretionary spending likely to be pressured lower. The Christmas mood is expected to remain sombre for many this year and we envisage 2024 will still be difficult for many households."

Smith says the battle to lower inflation back to 2% is far from over.

"We don’t expect further OCR hikes but acknowledge that the [Reserve Bank's] patience is wearing thin. Tangible progress will need to be made in lowering domestic inflation. While households do not set prices, their actions will have a tangible influence. The battle on inflation is not yet won and the RBNZ will be looking for restraint on the part of firms, consumers and government to reduce inflationary pressure. If not, higher OCR settings may result."

Lowering inflation needs to be a team effort, he says.

"Firms, policymakers and households will need to play their part. Ongoing consumer restraint and increased consumer resistance to paying higher prices are key pre-requisites to cooling domestically generated inflation. If households decide to pop the champagne corks too soon, they might discover a nasty interest rate induced hangover will result."

42 Comments

Quite interesting ...

- In the graph, note the substantially lower interest payments (red) in '24.

- talking up further wage increases and rising costs (inflation still a thing?)

Put the two together and something doesn't add up. Or am I missing something?

Economists are certainly paid lots to make rich assumptions. Interest costs reducing in 2024 are they?

Economists looking forward have to make assumptions. But they should be consistent. And clearly laid out.

And the conclusions should be logically consistent with the assumptions ... Which doesn't appear to be the case in this instance. Or am I missing something?

No they are saying that the increase in interest costs in 2024 will be slower than 2023/22. They are probably right on this. The majority of households have already refined and the average mortgage rate is 5.6% now, so not much to grow.

OOOPS, my bad - thanks Baptist.

Yes. That could explain it.

"But Smith says the concern is that the households who have built up the savings will not be the ones who need to find additional funds to cover higher living costs."

Good to know that ASB economists, like me, realise the OCR at high levels creates inequitable outcomes based on age and wealth.

Not that they have any interest in raising this inequity.

They like the way the RBNZ telegraphs rises early (and they jump in and raise rates way before the OCR is raised) and they love the fact that once people are locked into 1, 2 or longer year fixed rates they can cream it in knowing their inequitably calculated break fees will keep the revenue flowing.

Must be grand to be be a bank in NZ.

And then ..."Lowering inflation needs to be a team effort, he says."

Say what! Isn't that woefully inconsistent with what he just said?

We just need some good economic policy to promote productivity improvements. Our population is consuming more but we have fewer workers, we need to get into a higher gear just to stand still.

The ASB report contains this bit (my emphasis added):

"The hit to the household sector is being masked by strong NZ population growth with net immigration to NZ around record highs. Our research on the impacts of net immigration suggests that the current composition of migrants is not adding as much grunt to domestic spending that historically has been the case. However, it also suggests high net immigration could still add significantly to medium-term inflationary pressures, consistent with the tougher line the RBNZ took in the November MPS."

The research mentioned is here: https://www.asb.co.nz/content/dam/asb/documents/reports/economic-note/a…

Those people who hold the view that "migration = inflation (especially in house prices)" ... please read.

While the research paper suggests there was a change sometime before covid, and immigration was previously more inflationary, I question this view given that inflation was largely within acceptable limits before this. My interpretation is that low, sustained interest rates after the GFC, slowly but surely resulted in house price inflation as buyers recovered from the shock of the GFC.

I remain staunchly of the view that the effects of immigration are significantly overstated.

(Just an aside, more/better proof reading is required, e.g. "The medium-term impacts from higher net immigration point to upward pressures on core inflation and tighter labour market capacity."

It’s an interesting topic.

I think the wealth composition of immigrants has some sort of impact on inflation, and house prices. But how much is the big question.

Back in 2003-2005 NZ had high levels of net migration. Compared to now, the composition of that immigration was much more orientated towards British immigrants, with I assume a higher wealth profile compared to recent immigrants.

Inflation went to quite high levels around 2005-2006. Did that high net migration, with quite a high wealth profile, contribute to that quite high inflation? I would suggest it did, but again by how much?

A range of other factors no doubt contributed, including broader demographics and things like WFF (putting more money into people’s pockets )

Would that be because they are paying increased rent (vs prior) to cover landlord's mortgage costs, and thus any extra money they may bring adds nothing to domestic expenditure - but sure helps the banks' profit exports?

More likely that considering most immigrants are now from third world countries, a lot of the money they earn is being sent back home to support their families and to pay their immigration agent/employer the cost of their visa. If local workers were employed all their wages would stay in NZ and support the economy, but if you employ an immigrant a significant portion of that wage now goes straight overseas..

Speculation?

Or have you seen the remittance figures? (Go on - I dare you. And while you're about it - compare them to other developed countries.)

Weird, most employers I know are pulling back. Any income rises means fewer jobs.

Yeah I dont see much inflation or pay rises next year. I think the fuel excise comes off in the next CPI figures?, but otherwise I wouldn’t be surprised if we had deflation this quarter, fruit and veg down, fuel down.

Yeah our company are saying to not expect any healthy pay rises next year.

When they say "households will need to do their part", could that also look like rent freezes from all the landlords who just got a bunch of money back in their pocket? Particularly for all the single people who need to earn two peoples' minimum wages worth just to stay afloat? Asking for a bunch of friends.

Most went from paying $10,000 in extra tax and making large losses, to only paying 60% of that, before insurance costs went up 50% and their rates bill doubled. To break even under Labour's rules I would need to charge $1200 per week for a 3-bed house in a small town.

Anywho, many landlords I know don't bother to increase rents year on year. They have recently to try and offset tax and insurance increases. If that settles down, the rent increases will too.

What will take longer to slow down is the exodus of rentals as people sell up. The quickest way to do that is to pull back on social housing budgets and limit AirBNB nights per year.

"To break even under Labour's rules I would need to charge $1200 per week for a 3-bed house in a small town" - did you buy the house recently? If the house costed $200k to buy, would you make a profit at current rent?

Up until recently I was also a landlord in a small town, but I bought years ago when prices were cheaper. I was paying $250 a week then for two houses, but eventually the rent evened out even allowing for interest deductability.

Having to pay $1200 a week to keep a 3br house in a small town is a much higher risk than I'd be comfortable taking.

Is that what it was when you bought it, or after interest deductability stopped kicking in? I don't know how many people made the numbers stack up in the first place in the last few years.

What those single people need to realize, is the landlord has gone out and borrowed a ton of money to buy a house that already existed and needs help to repay the loan. The sooner that's done, the sooner their landlord can leverage equity to outbid another young aspiring FHB couple and "provide" much needed rental stock.

And the main reason he "invested" in existing property is because it is tax free.

I assure you that once you tax landlords more, tenants will pay more rent. The lag time will be maybe 6 to 12 months. Taxing accommodation is a universal tax.

The interest deductibility changes are not universal, they punish those with more leverage and have no effect on investors with no mortgage.

Which is good, we want to discourage leveraged speculation in property, those risking their own money don't contribute to us needing to bail out banks when finance goes tits up.

Would love to see a process where - investors can buy/build new builds tax free and sell after 5 years with no tax.

While bringing in a tax for any seconadry home purchase, of existing stock, which would attract a 50% or higher capital gains tax.

Sure. Tell your friends:

- Increasing one by $40/wk due to tenant changeover. Four adults going in, 3 adults leaving, so the per-person rent is dropping. Currently organising double glazing for this property, which is already (over)loaded with insulation, heat pump plus extra heating, fans, ventilation system, and so on.

- No changes elsewhere. Insurance and rates well up but my problem to deal with, not the tenants'. I have the cashflow to cover them, and since they're claimable they're a zero-sum game, lost savings interest notwithstanding.

Also, not a Boomer.

Why do you consider what is now the basics in a new build, as overloaded?

I don't, I'm saying the insulation in the house is well above spec. For example, Zone 2 ceiling insulation standard is currently R2.9, but the house has a dual layer of R3.6, and has had that for at least 5 years. R2.9 makes me shiver just thinking about it. The house in question was our first family home, and my wife feels the cold, so the house will likely be well ahead of Healthy Homes (or equivalent) standards for many years to come. We've never rented out a house we wouldn't be happy living in ourselves. We consider tenants to be our customers, and therefore it is worthwhile investing in their happiness.

FWIW every upgrade was put in well in advance of HH requirements, and we're not retro-fitting double glazed panes, we're completely replacing the windows to minimise air gaps as well as reduce future maintenance requirements.

Thanks, I couldn't understand from your original comment how it was any different from a normal new-build or house that met HH standards. I put the R3.6 in my houses about 5 years ago too, it's worth doing. Yes - I also consider the tenants I've had to be my customers. Particularly important in a small town because your reputation is at stake.

@ General Comment

"Insurance and rates ..... since they're claimable they're a zero-sum game"

Make sure you get an accountant to help with your tax return, to prevent any issues with the IRD, because you might be confusing "Claimable" with something that's potentially "reimbursable".

Yes I have an accountant to handle the bookwork, I wouldn't be surprised if I'm using the incorrect term. "I am not very smart but I can lift heavy things." - a t-shirt slogan, maybe.

good on you.

But, It's not just the 'term'. It's an important concept to keep in mind when doing your numbers on an investment property (not just the end of year tax return).

Consider these two scenarios as an example:

1) your income is $100k, your insurance/rates are $0,

= your taxable income is100k and therefore your tax to pay is around $23,920

2) your income is $100k, your 100% claimable/deductible insurance/rates are $10,000,

= your taxable income is 90k (100k income minus what you've claimed/deducted) and therefore your tax to pay is now around $20,620.

Your 10k that you've paid away in insurance/council rates will not save you 10k somewhere down the track (so it's not a zero sum game), it will only save you $3,300, as per the examples above. Keep that in mind when doing your numbers.

Correct. The number of people that don’t realise that is astounding.

I'd be very rich if I got $1 for every time I've people people get that math wrong. (And don't get me started on how depreciation works!)

Landlords havent gotten any extra money back in their pockets. All that has happened is that they wont be put into a mortgagee sale next year when the deductibility would have dropped to 25%. You see, deducting 100% of a 3% mortgage in 2021 is the exact same amount as deducting 50% of a 6% mortgage in 2023. So landlords up to now havent had to pay any extra tax, other than those suckers who bought an investment property after 2021 who have zero deductibility. The real poo would have hit the fan in 2024 when deducting 25% of a 7% rate mortgage would have become totally unmanageable and all the tenants would have been evicted so the landlords could sell up. Tell your friends to enjoy still having a roof over their heads.

What you haven't factored in such an apocalyptic scenario, is that until the mass of landlords manage to sell, the bank is probably going to want them to keep the tenants in place to continue servicing the mortgage. The houses won't disappear.

If they do manage to sell, who are they selling to? If it's another landlord, then the tenants may stay. If it's a First Home Buyer, then chances are they are vacating a rental property (not everyone is a "flat mate").

Yes. The houses don't vanish into thin air, and the bank isn't going to want them to remove the income while they still have it coming in. And right now, there aren't many people except those at the top who have the capital to buy/service a loan, even with prices very low compared to a few years ago.

I don't understand why the (not even subtle) disdain/hate for people like my friends renting, when we all know the structural issues that are underpinning the reasons many can't own (and if you don't know, a cursory Google search of this site will help you find out). I rent AND own a rental because these are the best financial decisions for me right now to meet my long term goals. Neither of these facts says anything about my personality or worth as a human being, or that of my friends who rent (or own). It's just a house.

It does however say volumes about our tax system and how NZ Inc misallocates capital into relative unproductive assets.

(I too am a LL. I don't get the tax rules I want - only the tax rules that everyone else votes for.)

re ... "So landlords up to now havent had to pay any extra tax..."

Your understanding of how the removal of interest deductibility affects how much tax must be paid is absolutely hilarious. (And wrong!)

".....ASB economists see household living costs rising again next year - but at a slower rate....."

Translation: prices going up.

Translation: prices going up at a slower rate.

(Even when inflation is back within the RBNZ's target range ... Geez. Guess what? ... prices will still be going up.)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.