By Gareth Vaughan

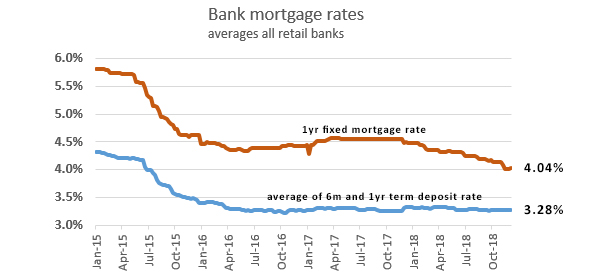

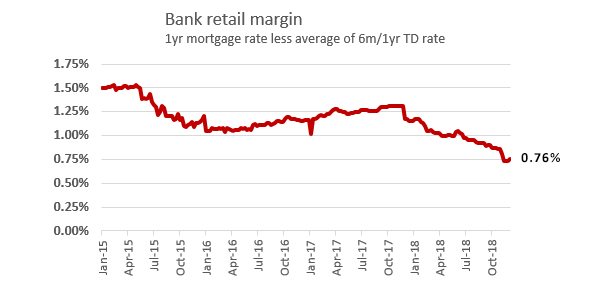

The recent sub-4% mortgage rates could be a generational low, says The Co-operative Bank's CEO David Cunningham, who argues they're not sustainable unless term deposit rates are cut significantly.

Speaking to interest.co.nz in a Double Shot interview, Cunningham said The Co-operative Bank had stood back and watched the recent home loan market competition between the big four banks believing it to be unsustainable.

"We've seen plenty of term deposit rates for six, 12 month terms around 3.50% even 3.60%, and when you're lending at 3.95% on one year or even two years, 35, 40 basis points is incredibly slim [for a margin]. Over time you tend to see that spread at about 1%," Cunningham said.

"So I've seen that competition and I've stood back and said 'it's unsustainable.' I think probably what we've just seen, sub-4% interest rates on mortgages is possibly the generational low...unless term deposit rates were to fall, say half a percent, in which case we'd see those [mortgage rates] back there."

"I think it was just this flurry of competition, maybe prompted by the [Financial Markets Authority and Reserve Bank] conduct and culture review, it was a way for banks to show that competition was alive and well. But I sort of stand back and go 'interesting but how many people have actually benefited from those really low rates?' Perhaps a few tens of thousands of people at the absolute most," said Cunningham.

All the big four banks - ANZ, ASB, BNZ and Westpac - have recently had their one or two year advertised fixed-term mortgage rate below 4%. However, they've now all ended these offers.

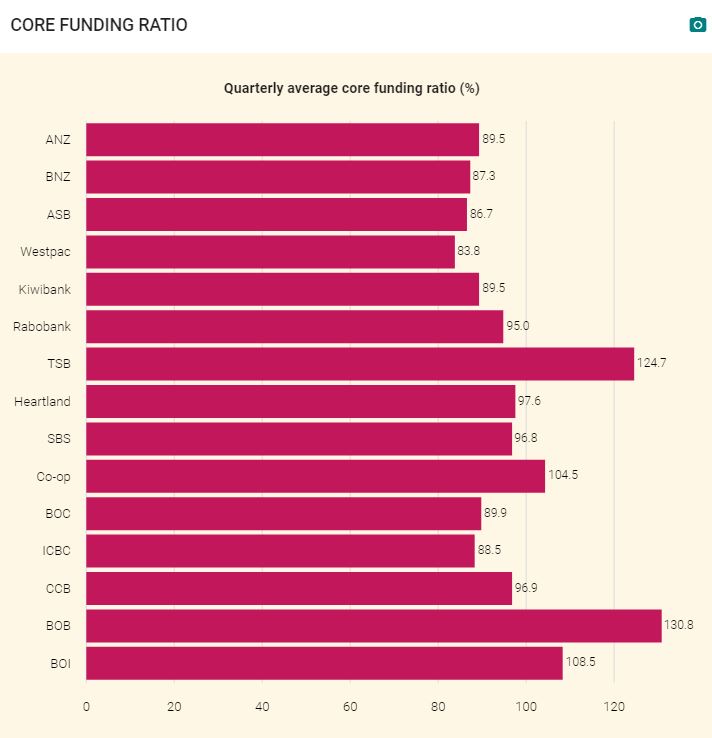

Unlike the big four The Co-operative Bank uses retail funding for all its funding requirements. However retail deposit funding is also important for the big banks. The Reserve Bank introduced the core funding ratio (CFR) in 2010 to reduce New Zealand banks' reliance on short-term offshore borrowing/funding. The CFR requires banks to meet a minimum share of their funding from retail deposits, long-term wholesale funding and/or capital. The minimum CFR for each bank - on a daily basis - is 75%.

The CFR is a comparison between an estimate of a bank's funding that's stable and can be assumed will stay in place for at least one year, and the core lending business of the bank that needs to be funded on a continuing basis. All banks comfortably met their CFR requirement as of September 30, as demonstrated in the Reserve Bank table below.

Meanwhile, Cunningham suggests one and two year mortgage rates will probably settle around 4.20% to 4.40% next year.

"It looks like the OCR [Official Cash Rate] is going to remain reasonably unchanged over the next year or two [as] we've certainly got a more dovish Reserve Bank Governor in Adrian Orr. So I don't think there's a lot of upside in the OCR. But what I do see is margins restoring to more sustainable levels in terms of that funding cost versus the lending rate. So I think probably mortgage rates settle, I'd say, round that 4.20% to 4.40% level for one and two year terms is what we're going to see over the year ahead."

Reserve Bank data shows $209.139 billion, or 81%, of $258.949 billion worth of residential mortgages is fixed with one and two year loan terms the most popular.

The charts below are interest.co.nz ones.

See all banks' carded, or advertised, home loan interest rates here.

All carded, or advertised, term deposit rates for all financial institutions for terms of less than one year are here, and for terms of one-to-five years are here.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

29 Comments

"The recent sub-4% mortgage rates could be a generational low"

Doubt it Harry!!!!

We are on the cusp of GFC 2.0 - if all hell breaks loose (which is more probable than not) what will the RBNZ do??? OCR could go to zero!!!

True, but a few considerations;

1) The OCR's practical lower bound is probably well above 0. An externally funded country like NZ would have a currency worth 30 cents at that level. $4 per litre petrol anyone? The RBA for example has said it sees a lower bound around 1% or slightly lower and I think NZ would be similar.

2) The banks won't necessarily pass on all cuts. Let's say the RBNZ cut 75bps, and the banks keep half, we might still only see 1 year rates around 4%.

If it is a global financial crisis, surely other countries would be easing at the same time which would keep our dollar up. Or have I missed something?

I think the answer is "it depends".

During the GFC the NZD dropped to 50cents while the OCR was at 2.5-3%, which was about 2% above the US Fed Funds rate of around 0.25-0.5%.

The OCR is now 1.75%, and below the US Fed Funds rate.

So if GFCII arrives and everyone cuts in unison, yeah maybe the NZD ends up in the 50's.

If emerging markets feel more pain before the US hits stall speed, that's where the downside risk is in my opinion (and I'd lump NZ and AU in with emerging markets as externally funded commodity producers). In that scenario, AU and NZ cut rates, while the US stimulates/rates plateau, that's a recipe for 30cents. Trump is the "economy is great" guy, he will recklessly stimulate long before he lets the US economy turn to crap.

The currency can easily trade 30c without the being at 0%

, the never ending credit growth and money creation has driven the price of money down.

so yes GFC 2 could be time to reset the whole system

RBA is looking at dropping official interest rate from the lower than expected growth rate, I don't think NZ is immune from this global slow down. Hold tight for a ride of your dream!

There seems to me to be widespread commentary on this site to help stabilise the market for the next 2 years.I don't see rates dropping but increasing next year. Those that sit on the fence could be right however, things could just as easily be the same as they are now, no change business as usual.

So RBNZ forces New Zealand banks to fund 75% from retail depositors. So the banks are forced to compete with each other for a share of that money. The New Zealanders who are lucky enough to have a share of the

170 billion dollars of term deposits in NZ banks get the benefit. Meanwhile, the poor old German dentist investing indirectly in the same NZ banks to fund the other 25% in Euros is lucky to get 1%. What sort of Term Deposit rates to Australian banks pay at the moment? What are the mortgage rates like in Australia?

ASB just paid 3.31% pa for 5 years, why would anyone take 1%???

Non residents also get 98% of their interest after tax.

Westie AJ. They aren't funding from retail deposits. It's a myth which was perpetuated in this interview. See below my question to Gareth. Deposits are purely loans made. Glorious double entry booking keeping.

You are quite wrong (and superficial). see below. And read the links in full. (yours and mine)

But do we want low lending interest rates for home loans?. All that seems to do is push up house prices, as people can afford to borrow more as they can afford to service a larger mortgage. Also NZ doesn't have a deposit guarantee for savers, unlike Oz, so savers end up taking a haircut if something goes wrong, and if savers are only getting a little bit above inflation, you can see why people are putting their money into houses or shares..

Gareth, did I hear that correctly? Your guest said 'The marginal dollar of lending comes from term deposits'....Why are we still perpetuating this myth and allowing banks to keep telling us this?. - Another missed opportunity to ask a penetrating question there Gareth. He even went to on talk about loans being made at 4% whilst paying depositors 3.6%. Perpetuation of a banking mistruth.

Loans made, are simply recorded as deposits on a banks balance sheet, bank deposits have very little to do with term deposits. See Bank of England release - Money creation in the modern economy, attached.

https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/20…

Nic. I am afraid you are perpetuating a silly urban myth of banks and money creation. If you read your link properly and better yet this one, you will find it is the banking system that creates money and not at any individual bank in the way you assume. But it does need some proper reading of the material. Most people who believe the myth do so without making any real attempt to understand the whole system.

As far as mangement in any one bank is concerned, they are limited by regulation to have at least 75% of all lending supporting their customer deposits (the Core Funding Ratio), and the rest supported by wholesale and other borrowing from wholesale investors and equity. Further, they are required to not mismatch significantly in the short term. Further, they are going to be under more restructions to increase their capital to support lending. Absolutely nowhere is there any license to just 'create-money-out-of-thin-air' and there never has been. You quite misunderstand the process and how it works.

It is never helpful to just jump on a systemic outcome of lending (when that happens, that is spent by the borrower and ends up as a deposit by another in the banking system) as some magical bookkeeping entry. Only the Government can do that (as in Zimbabwe, Venuzeula) and the outcomes are never good.) or central banks, as in QE (and that never happened in New Zealand).

Yes, I know political parties have been formed on the basis of this silly misunderstanding, but their logic only appeals to folks who won't think the intricate process through. The myth has been debated for years - and it never gains any traction in public policy because essentially it is a bankrupt idea.

I know you are a relatively new commenter here, but frankly we are over this pointless 'debate'. It was sorted 50 years ago.

I hope Withay reads this as well. Have bankers replaced the illuminati in CT circles?

Casts doubt on everything Nic writes really.

@Ex Expat. In an effort to extend an olive branch and show that we are all saying the same thing but in different language, I will quote David’s supporting article below. Important to note, the choice of language used I.e. “money created from nothing” depends on whether you view the banks actions as positive or negative.

Key sentences as per David’s article:

“In a modern economy, money can be created either by the central bank (the Reserve Bank, in New Zealand’s case) or by private sector institutions – in practice, mostly registered banks.”

“If, say, 10 percent of deposits are typically withdrawn for cash payments weekly, and this amount is re-deposited with the bank, then Bank A only needs to hold $100 in cash at hand to support likely withdrawals on its total deposits of $1,000.”

“Bank A can thus lend out $900 to its customers. They can then use this $900 as payment for goods and services. The $900 will likely be re-deposited. This is the first step in the process of money and credit creation by Bank A. So far, it has created $900 of money, and it has created credit to the same value.”

“Turning back to the money side, in our scenario, only $90 of the $900 in new money is likely to be withdrawn as cash, with other payments being possible through electronic transfers of account balances. Bank A thus has a further $810 to lend out. As this process continues, the ultimate outcome is that the initial $1,000 in deposits can be used to create new deposits (money) and credit (loans) to the value of $9,000. This new money is generally termed ‘inside’ money to reflect that it has been generated by the private bank ‘inside’ this economy. Bank A’s balance sheet has grown from $1,000 to $10,000.”

To quickly summarise the key point - $10,000 is now circulating in the economy when there was only $1,000 to begin with. The pro bankers will call it “inside money,” the anti bankers (for want of better terms) will call it “money created from nothing.” Either way most important thing is that if it looks like money, smells like money and ACTS like money then it IS money and this money didn’t exist before.

My bugbear is the effects of money creation. I hope both David and Ex Expat will admit that through the money creation process as outlined in David’s article that the created money/inside money/credit will and can never be paid back without some sort of write down or reset. It relies on further money creation to support the repayments on money that was created through this method further exacerbating the effects of money creation.

That is the issue. I hope I have expressed it well enough to get across my point and also to show that we are saying the same thing whether it’s Nic and I saying “money is created out of nothing” or whether it’s Davids article showing that $10,000 can be created from $1,000 - it’s the same thing! I would rather be talking about the consequences of money creation than the mechanism. More productive.

Thank you Withay.

My bug bear was how this was communicated in the interview without question. It just keeps people in the dark ages! and I would guess 99% of the population have no idea which is very undemocratic. Although the RBA have in the past referred to this process as the 'democratization of finance' - Another fallacy.

See that's where you're wrong David. When people sign up for a mortgage, when the bank prints off the loan documents they actually print off the required funds to liven up the loan as well. The core funding ratio is the ratio of denominations they print out, 75% is $5 notes. CET1 @ 4.5% minimum is the number of $100 notes. Tier 1 @ 6% is the number of $50 notes and the balance of no more than 14.5% is $20 notes.

Someone borrows $500k, the bank will print 75,000 x $5 notes, 225 x $100 notes, 600 x $50 notes & 3625 x $20 notes.

NzDan - no disrespect but what are you smoking???

He's a smoking some sarcasm.

nymad - thank you for explaining. It is sometimes difficult on this site to differentiate between wit and a genuine lack of comprehension of banking fundamentals. I will endeavour to be more discerning in the future.

I like breaking Poe’s Law.

My earlier response suggests you actually proved Poe's law.

From now on I will be more careful to consider each of your posts on whether your tongue is firmly in cheek or not.

Sorry David, the old text books don't apply anymore and haven't done for 20 or more years. I have made no assumption that it is individual banks doing this. Individual banks have different tolerances to how much risk they want to multiply up (but not in the conventional wisdom of the money multiplier effect, taught in schools by economists who have spent their careers in education). The digital age changed banking irrevocably and institutions are yet to catch up.

Yes, David seems to believe the "fractional reserve" story implicit within his referenced article. Even the RBA does not buy this tosh ( see here )

One final word on the creation of money is that as fun as it is to teach students about traditional money multipliers, I don't find them to be a very helpful way of thinking about the process. In Australia, simple regulatory regimes – which had earlier required banks to hold a minimum share of their deposits as reserves with the Reserve Bank – have been replaced with modern prudential regulation and market discipline. Again, the demand for and supply of credit is the real driver of money. That point can be reinforced by examining the behaviour of credit and money over time.

Good points Mr Chaston. In the comments section of the article you linked above, you say -

"Cryptocurrencies will turn out to have more practical use [than gold], completely replacing the 'money' functions gold used to have in the pre-industrial world."

You're still of this view today?

Gold as “money” is history, but as a store of value it is quite strong. In terms of “money”, I’m in two minds about crypto vs traditional fiat currency. There is a very interesting debate on the matter here, Peter for gold and Erik for crypto. https://www.youtube.com/watch?v=q8R71WGO3qU&t=63s

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.