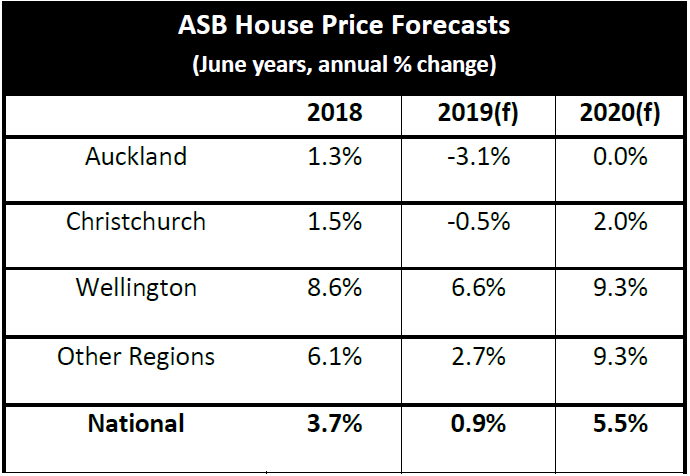

ASB economists expect nationwide house price inflation to pick up from the current annual pace of around 1.5%, to 5-6% by mid next year.

In ASB's new Home Economics publication, senior economist Mike Jones says while there are plenty of "cross-currents" at play in NZ’s housing market, it's ASB economists' view, that sharp falls in mortgage interest rates will combine with still-strong population and labour income growth to "jump-start the Auckland housing market and add a little more heat to simmering regional markets".

Even with the "jump start" though, the ASB's only forecasting flat, IE 0% growth for Auckland prices next year - after a more than 3% drop expected this year.

Talking nationwide, Jones says from late 2020, they expect the price cycle "to top out as new housing supply coming on-stream gradually reduces the housing shortage".

Westpac economists have been offering similar views of a pick-up in the housing market.

ASB's Jones, in comment on the Reserve Bank's 50 basis points cut to the Official Cash Rate on August 7, said the RBNZ’s determination to "slash rates until kiwis start borrowing and spending again" could well see a more enduring than expected house price inflation cycle take hold.

"Certainly, the closer term deposit rates get toward zero, the bigger the risk of a widespread asset-allocation into housing.

"However, the turning NZ economic cycle, policy-related handbrakes, and a ramp up in housing supply will all act to limit the extent of the upturn in our view."

Jones says that spring is shaping up as a key test of their view of the market.

"We find that declines in mortgage rates tend to take six months or so to impact house prices.

"So if we’re right that recent mortgage rate cuts (which began in earnest in March/April) will provide a boost to prices, we should start to see this show up in September/October housing data."

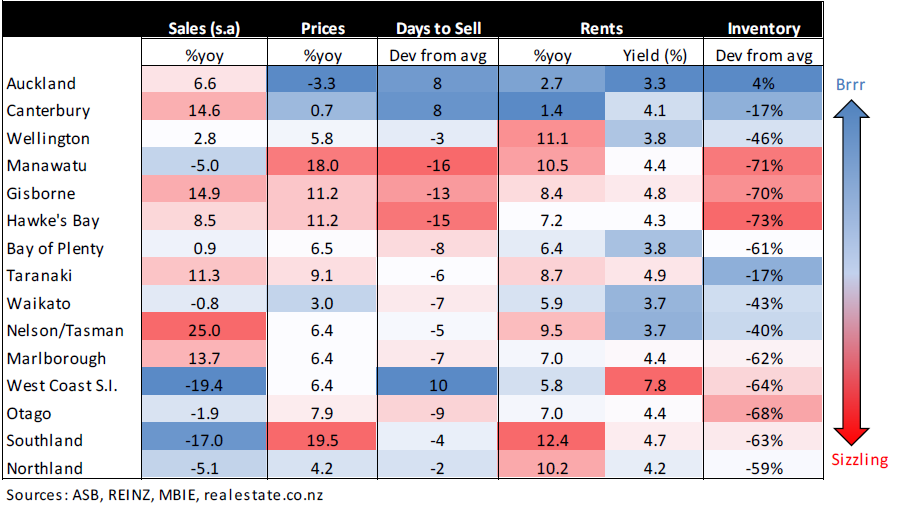

He notes that the picture remains very patchy around the country.

"Conditions in Auckland remain chilly. House price growth remains negative on an annual basis, albeit there’s been small gains posted for the past three months. Days to sell and inventory both remain above average levels suggesting we’ll have to see further thawing in activity before we can expect prices to lift.

"Canterbury is another notable underperformer... a ramp up in supply appears to be part of the story. This appears to be reflected in rents, which are running at just 1.4% yoy in Canterbury, the slowest growth rate in the country."

The report features a detailed Regional Heatmap, which shows the areas that are hot. And those that are not.

Jones says the Wellington market has cooled from the "giddy heights" of late 2018. Annual house price growth has slowed from double-digit rates to around 5.8%yoy. Days to sell and house sales are also consistent with the market shifting down a few gears.

"Still, inventory remains very tight with just 9 weeks’ worth of sales listed. As such, we could see a second wind for prices should low mortgage rates kick things off again."

Central and Eastern parts of the North Island are "cooking", Jones says.

"These markets are tight. Days to sell a house have fallen appreciably through the first part of the year, inventory is very low, and strong house price and rental growth has swiftly followed. More of the same looks likely, with supply slow to respond and low mortgage rates likely to further boost demand."

Housing market conditions remain fairly strong on the West Coast and South of the South Island.

"Notably, house price inflation in Southland remains the hottest in the country at 20%. Price growth in Otago and the West Coast has also been solid reflecting very low inventory levels. One possible fly in the ointment is the recent cooling in house activity in these regions, with July house sales data well behind year-ago levels. This data can be choppy though so we’ll keep an eye on what happens over coming months."

63 Comments

ASB economists clearly don't read Interest's comment section (why would they?)

Commenters not reading economists' statements either?

"Conditions in Auckland remain chilly. House price growth remains negative on an annual basis, albeit there’s been small gains posted for the past three months. Days to sell and inventory both remain above average levels suggesting we’ll have to see further thawing in activity before we can expect prices to lift.

Don't worry, TM2 will be along any second to tell them they don'y have a clue

"Canterbury is another notable underperformer... a ramp up in supply appears to be part of the story. This appears to be reflected in rents, which are running at just 1.4% yoy in Canterbury, the slowest growth rate in the country."

He means many are calling for a crash and ASB is predicting 0.00% in 2020.

Correct

"Price growth in Otago and the West Coast has also been solid reflecting very low inventory levels. "

"Housing market conditions remain fairly strong on the West Coast "

Yvil perhaps you can explain Interests ( REINZ ) median price chart for the West Coast to ASB , or perhaps the West Coast has moved to another location. .

Yvil

Too true.

I note RBNZ figures yesterday show over 27,000 FHB in past 12 months which is up on previous 12 months with 10% increase for FHB in July month compared to 2018.

So clearly - unlike the occasional DGM flippant poster who are increasingly in a minority - there are considerable numbers of FHB who not only think the market is fine (accepting that some fluctuation is possible) are committing with their wallets.

I do note that investor numbers are currently down but that is probably due to low yields, a likelihood of a lack of significant capital gain, and increasing compliance requirements. However, as the article points out, with falling interest rates for term deposits, property investment is likely to become more attractive. As previously posted, simply by default, my wife has recently purchased a rental again.

How is 0% growth reviving the Akld market???

Inflation adjusted that is still going backward. Never the less pretty optimistic at 0% growth.

I guess by revival they mean market remaining dead and not turning into a zombie!

Reviving a near dead patient doesn't imply hes fit for a marathon, hes just stopped bleeding out.

they have to keep the spruikers happy, hence the title

I chuckled at their 2020 estimates conveniently starting at the lowest of zero in Auckland. Couldn’t possibly be the slightest bit negative.

I never inflation adjust a house price, why you may ask ? because in reality your wages are not inflation adjusted. There is no way that wages have kept pace in this country with house price increases so the house inflation argument is null and void.To argue your going backwards owning a house is not supported by the numbers.

Never mind the current meltdown of the Global economy. Look over here guys, Auckland house prices are going upwards!

Sideways at best but sure.

.... the road runner is going " meep meep " as he smiles at the wiley coyote who's just run off the cliff and is now suspended in mid air ....

The coyote looks down at the thousand feet of clear air below him and the canyon floor .

... you know what happens next ... . Orc Land housing speculators : meep meep !

"senior economist Mike Jones says..."

Ah yes.

Would that be the same Mike Jones that spent 5 years at Fonterra telling them what the future held?! Mind you, he has spent 3 months at ASB now, so maybe he has seen the light!

Now there is the real news.

Sounds like a lot of properties in Auckland need a bulldozer, NOT a million dollar price tag.

"They never learn".

About as credible as a trump tweet. And done for the same purpose...to pump

Probably more likely to get in trouble with their employer if they forecast the 2020 outlook to be below zero and predict correctly, than if they predict it will be above zero but get it wrong.

The desperation is palpable!

“the RBNZ’s determination to "slash rates until kiwis start borrowing and spending again" could well see a more enduring than expected house price inflation cycle take hold.”

Just for a second imagine what our country would look like if certain entities didn’t interfere so much...

I'm looking in the market in the north shore as FHB. Recently just missed out on a property in a multi offer due to having more conditions in an agreement as you do as a FHB. Little bit frustrating when you've been saving to get that 170k 20% deposit but hopefully something nice will come up. It seems like the market is taking a turn on the shore in the lower quartile and I say that as being a massive skeptic.

It might be a risky move however because there still seems to be a lack of investors and the number of Asian people is way way down at open homes. But there is no denying that on the north shore at least in the lower quartile demand is going to be strong over the next couple of months as people still want to own and have their own place to live.

If you are buying for mid to long term capital gains with low LVR's I'd still be a bit worried.

You know your'e trying to buy in about the most expensive part of the country right?

Whats your price range RubberDuckey ? I know of a 2 bed stand alone property coming onto the market in October in Torbay.

This article is based on the myopic view that home owners need to borrow against their property to boost consumer spending [velocity of money].

With approximately half of Kiwi's living in rentals I'm not surprised the likes of Smith City are going down the tubes.

With more-or-less negative interest rates, people have to save MORE to build up capital to participate in capitalism - not spend more!

The idea that house price inflation is the NZ economies savior is like a heroin addict believing their best course of action to avoid a horrendous comedown is taking more heroin.

I guess all will be solved now that Jacinda is looking into petrol prices and Bridges wants to put the retirement age up - good times, such visionaries, lol.

Cutting the OCR to zero or even lower will probably save the Auckland market. At least as long as unemployment does not start rising significantly.

Our definition of 'saving the market' is different. Is it worth 'saving' the market at the expense of widening the gap between haves and have-nots? I'd say a 25-30% fall would save the market, from a human perspective.

I agree. I was using 'saving' in terms of the conventional wisdom, not in terms of what I think is desirable.

"save the Auckland market" - AT BEST, that is a misnomer.

A market is simply buying and selling. Regardless of the price on Auckland properties, there will be buying and selling.

The whole idea of a market is to offer a product (in this case property) to buyers .. after that you have 'price discovery' ..

ultimately the buyers decide the price.

Not sure why you think "the Auckland market" is in need of saving ?? Is buying and selling of property going to be outlawed ??

Many property owners think about 'the market' as their perpetual capital gains motion device. If 'the market' isn't generating any capital gains, it's clearly broken.

I am sure you can work out what I mean.

It's 'saving' in the sense of preventing a large correction or 'crash'

"preventing a large correction or 'crash'" AGAIN, another misnomer ..

The presupposition is something is In-Error - Why would you want to prevent "correction" ??

As for preventing a "'crash'" - capitalism clears out bad debt through bankruptcies, liquidation of unwanted businesses, etc. We don't shank price discovery in the shower.

I think you're being a bit ridiculous Fritz.

"We don't shank price discovery in the shower."

Gold.

Based on what Fritz wrote, I wouldn't infer that he necessarily wants to prevent a correction. He's just expressing what he believes will happen to the market if a particular monetary policy is followed. Nothing ridiculous about that.

I wouldn't read too much into the use of "save the market". It's just a phrase used to express an idea.

Exactly !!!!!!! :)

:)

Quote rewritten to reflect reality: "the RBNZ’s determination to "slash rates until [rich] kiwis [and new residents] start borrowing and s̶p̶e̶n̶d̶i̶n̶g̶ [extracting money from the poor] again" could well see a more enduring than expected house price inflation cycle take hold".

The RBNZ seems to be continuing its war on the young and poor...

Ready to do everything to keep that GDP growing. The purpose of existence is constant GDP growth, f*** the people, f*** the Earth, f*** everything else.

How does ABS's prediction of a completely flat Auckland market, match the article headline of' 'Jump Start for the Auckland house market"?

More like a handbrake.

..jump starting works when the battery is flat, but if the engine is rooted..........

... she'll still hit 100 mph.... you just need to find a high enough cliff edge to push her off ..

To be fair, you can also jump start a car with no wheels. It's just not gonna go anywhere.

bow to the master

Agreed, he headline "Jump Start for the Auckland house market" is misleading and wrong

ya reckon its more like in the movies when they put the paddles on the chest and give the poor sod a belt of Electrickery and the body jerks.. then minutes later they pull the sheet over the victim? :)

Supply up, economic growth down, confidence down, world growth down, Aussie market in deep shit.

China pulling in foreign exchange levers. great prospects. Self-interested bull based on usual tripe re pop an interest rate cuts. I have to repeat again: interest rates been falling for 7m, and sales have fallen anyway.

Also, buyer attitude is what counts. Buyer general attitude (except for some FHB who are not experienced enough to know better) is that prices will go lower and negative equity is an issue. Housing market sales in NZ as a whole is (last 3m) selling 15% fewer than in 2017, which itself was not a good year. If prices do go up, in each month we see the areas where that happens, sales go down. Market is over-supplied in Auckland especially and more is being added, despite sales dropping. Economists do not seem capable of distinguishing between housing need and housing demand. Need is indeed increasing but demand is not.

I think you need to take an economics course. Then get a job being an economist at a bank.

Then you will have enough knowledge to be absolutely sure that house prices go up, all the time.

And if they don't, you say they are, and get the RBNZ and the government to pull levers until they do.

Then you ask for a pay rise.

Some valid points there. But surely cutting the OCR to 0 and probably lower has a good chance of luring in a few more FHBs and investors to keep demand ticking along? Obviously a deposit will still be a barrier for many.

The NZ economy is looking a bit average, but it doesn't look too bad.

Assuming unemployment does not increase too much, I think it's quite a credible scenario to see Auckland prices flat-lining in 2020.

What I think is critical here is the employment rate. To what extent will work in the major engineering consultancies, architecture firms, building companies, and infrastructure contractors start to dry up? These are big employers of 'the middle class' in Auckland. Roading projects are drying up under the current government, and potential rail projects are stalling. Some of the big building projects will be completed in the next 3-6 months.

I've heard of one or two firms moving to 9 day fortnights. That's a drop of 10% in income.

So I think if unemployment stays below 6% then I don't think Auckland prices will fall much further. If it rises much above 6%, and whacks middle income jobs in particular, then it's a different story.

We need to keep in mind that prices are usually a bit stickier on the way down as compared to on the way up.

Agree about employment. But I would also be watching what the banks do re FHB LVR's as the banks will always make sure the ratio is enough to cover any expected fall in value +10%. And I mean a real FHB's LVR, not one that is cross securitised with the bank of Mum and Dad.

How the banks use the LVR should signal whether they expect the lowering of interest rates to make any difference up or down.

Mind you, since it is all about giving the market confidence, or in the case of FHB, overconfidence, then we should be wary of why banks, or bank economists send the signals they do.

I agree with employment being a huge factor.

Lots of companies trimming staff to boost profits as growth stalls

Of all the bank economists, Tuffley is the one I pay the most attention to. He tends to have a reasonable perspective in my experience that's worth feeding into one's own predictions.

I just cant see what the drivers are for such an optimistic call in the face of whats happening globally?

- The foreign money has evaporated

- Bank credit is much much harder to get no matter what the OCR is.....banks are still stress testing close to 7%

- Wage growth is poor

- GDP Per capita is poor

- Market sentiment "flat" at best as some friends in RE tell me... "its def a buyers market"

- Globally things are teetering... and the worlds 2 biggest economies in a trade war

The Auckland market has made a mug of me before but I really cant see this....it cant go up out of thin air?

You may have missed it but they have been cutting rates and relaxing LVR's, neither of those would constitute thin air.

@ Laminar..

As mentioned above the OCR is largely irrelevant when banks are stress testing mortgages at close to 7%....it is not easy to get money right now and I know of many who have had expired pre-approvals loan amounts markedly reduced when re-applying.

And the LVR reduction...well, where I live on the North Shore of Auckland the HPI is -4.4% in the last 12 months YOY so doesn't seem to be making any difference.

I'm always skeptical of banks making these calls......they are in the business of selling mortgages.

Wishful thinking to keep their shareholders interested. It would be really interesting to see the number of how much has been ASB spending in advertising their lending products during the last year compared to previous ones.

Enployment!

Forestry basically nonexistant now.

Tourism has to take a hit this year due to global conditions.

Wool taking a battering.

Fontura!

This effects everyone with less dollars in the system. People are struggling at present in the good times, take some big export earners out and it all starts to fall apart. 50 base point cut but nothing to see here, bussiness as usual. YEAH RIGHT!

The RBA chief's recent statements at Jackson Hole, that low interest rates will result in asset prices, is the best 'jump start' for Auckland housing...

Sponsored journalism?

0% for Auckland prediction could be an attempt to restore confidence to buyers in Auckland. If buyer expectations are for 0% growth implying that property prices have stopped falling, then the hope is that owner occupier buyers that are sitting in the sidelines will buy as property prices will not get any cheaper.

If tthe economists had forecast price falls in 2020 for Auckland, potential buyers might decide to wait on the sidelines for lower prices.

Typical banks spruiking market

Got to get those mortgages signed up $$$

Everything is beautiful A sun shining day in property

Yeah right lol

I came from China, not every Chinese got dirty money in his pocket.

I am not going to buy these crap with my own hard working money.

I am not going to take the last relay baton and run without shoes.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.