Economists at the country's biggest bank now see house price inflation hitting 8% by the middle of this year.

In the ANZ's latest Property Focus publication, ANZ chief economist Sharon Zollner and senior economist Liz Kendall say there is even is some upside risk to that 8% number.

"The market is tight and house price expectations have increased – but we think a number of headwinds will keep the market in check," they say.

"Given the current low interest rate environment, house prices could prove volatile."

ANZ is New Zealand's biggest residential mortgage lender with $85 billion of lending exposure as of September 30 last year.

The Reserve Bank will be watching financial stability risks closely when setting macro-prudential policy to ensure a growth-positive pick-up in housing "does not come with a risky speculative dynamic".

Previously the ANZ economists had forecast house price of about 5%-6% this year, but noted in their weekly newsletter last week that the housing market had the "bit between its teeth again" and said they would not rule out the possibility of the Reserve Bank actually clamping down on its loan to value ratio (LVR) limits again if necessary.

Westpac economists have for some time been forecasting that house price inflation will hit 7% and they were for quite sometime market outliers in their prediction, but as the housing market has perked up, so other forecasts have been rising.

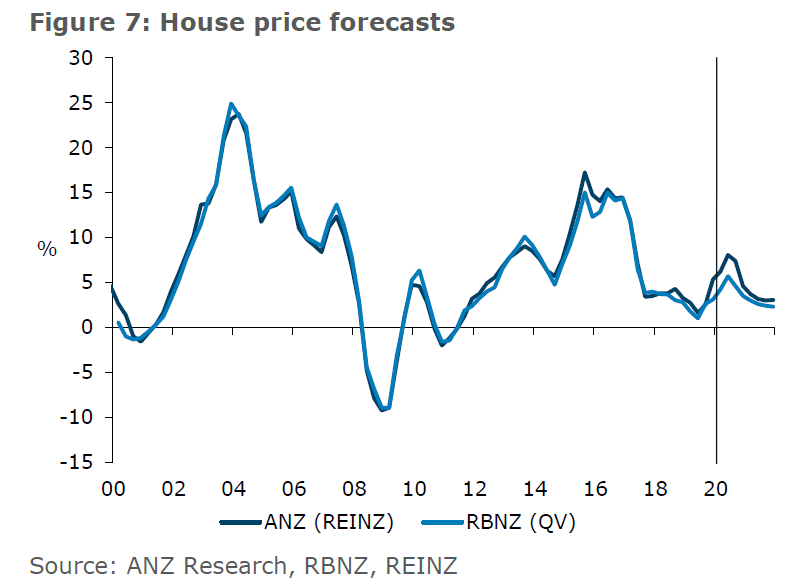

In the latest Property Focus, Zollner and Kendall say they expect house price inflation to reach 8% year on year before moderating, with affordability constraints, moderating population growth, and prudent bank and buyer behaviour keeping the market in check.

"But house price expectations have increased and the market is tight, posing further short-term upside risk to the outlook. And as always, longer-term downside risks should not be ignored."

They say while they expect that the RBNZ's LVR settings are in a holding pattern for now, a rapid increase in housing market strength combined with a risky speculative dynamic "would not be left unchecked".

In looking at recent trends, the economists say that the housing market went through a cooler period from the start of 2017 until the middle of 2019 particularly in Auckland, with house prices rising 7% over that 18 month period. A number of headwinds were at play: uncertainty, actual and proposed policy changes, affordability constraints and credit rationing.

"But conditions have turned a corner and house prices have recently rebounded, rising 6% over the second half of 2019."

They noted that over 2019, the Official Cash Rate dropped 75 basis points (to 1%) and expectations shifted to interest rates being lower for longer.

Mortgage rates fell and financial conditions eased.

"Consequently, the housing market tightened. Monetary policy is clearly 'working' (putting aside the question of whether rising house prices are in the long-term interests of the New Zealand economy or its inhabitants, which isn’t something monetary policy can do much about). But it wasn’t just interest rates driving the lift; this was against a backdrop of continued population growth (albeit easing), limited growth in housing supply, a tight labour market, and some easing in headwinds, particularly on the credit side," Zollner and Kendall say.

They say housing credit growth has picked up "a bit more than one might have expected" based on housing turnover.

"Banks appear to be competing more in the mortgage lending space. This may be partly related to the RBNZ bank capital changes that have the effect of making mortgages even more attractive versus other forms of lending."

They say they expect continued robust house price inflation through the first half of 2020.

"Annual house price inflation is currently sitting at 5.3% y/y (3mma), below its historical average of 6.8%. But we now expect this to reach 8% y/y in mid-2020, before moderating. This is above the RBNZ’s November MPS forecast for house price inflation to peak at 5.7%."

Zollner and Kendall say stronger house price inflation will support consumption, residential investment and GDP growth in coming years.

"This is one of the reasons why we no longer expect the RBNZ to cut the OCR any time soon."

They say It is possible that house price inflation could be even stronger if current tight conditions persist. However, at this stage they think that a number of factors will keep the market in check:

- Population growth is easing. Changes to net migration data make recent trends difficult to discern, but we expect population growth has abated somewhat.

- Financial conditions are easy and supporting the market, but further OCR cuts are looking less likely and the additional boost from lower mortgage rates will eventually run its course. Credit expansion is also likely to be tempered by bank caution in the current environment.

- Affordability constraints are expected to weigh. Australia provides a cautionary tale, proving that prices can reach considerably more eye-watering heights, but there are limits.

- Policy changes targeted at reducing investor demand are still playing out, which may be exacerbated by election uncertainty. And if lending gets silly, the RBNZ may step in with tighter macro-prudential policy.

78 Comments

Zollner and Kendall say stronger house price inflation will support consumption, residential investment and GDP growth in coming years.

The banks are not even smoke signalling anymore. They either fully believe in the power of the relationship of house price inflation and consumer spending or they're sending a veiled threat ("stymie our bubble and the consumer economy will fall through the floor").

Anyone that denies the relationship between house price inflation and consumer spending has a tenuous grasp on reality.

Correct. That is why the end of bubbles are typically disastrous for economies (negative impacts of the wealth effect) and why bubbles are tolerated by govts.

Bubbles? Champagne or soap bubbles?

Credit-driven asset bubbles. In the end, there is no cure for asset bubbles except for the bubble to unwind.

That intuitively feels correct but it hasn't been proven yet and there are options that could plausibly resolve it without an unwind.

That intuitively feels correct but it hasn't been proven yet

Given that all identified bubbles in the past have "unwound", it is proven that bubbles unwind. If you can identify an "unwindable bubble", go ahead. Let me know.

A better argument would be to say NZ residential house prices are not in a bubble. There is no "proof" that a bubble exists.

All swans I have seen historically, are white, therefore all swans are white?

All 'white swans' are white, yes. Some swans are black, but they're not white swans.

All swans I have seen historically, are white, therefore all swans are white?

All bubbles I have seen historically, unwound, therefore all bubbles unwind?

It's logically invalid.

No it's not. I'm alive, not dead. That doesn't refute the fact that all people eventually die.

Your statement was logically invalid because the premise can be true even if the conclusion is false. The structure of your argument is invalid on the face of itself.

You need to prove that all future bubbles will unwind, but all you are arguing as fact is that all historical bubbles unwound.

Your argument is also unsound, as you have not proven, nor has anyone, that all historical bubbles unwound.

Your argument is both technically invalid and technically unsound.

OK. Show me a perpetual bubble that hasn't unwound.

The New Zealand housing market.

All bubbles unwind. The very definition of a bubble is something that is unsustainable.

The definition of a label is not evidence, but even so, I think the definition of a bubble is simply an asset class racing up in value without underlying intrinsic value supporting it. No requirement in the definition for it to unwind.

You only know a bubble is unsustainable once it has popped. If it never pops, it was sustainable.

Round and round we go...

Correct. As per below bubbles are not sustainable.

And it is not usually known if a bubble existed until after the fact.

I still think the NZ housing market is a bubble. But we won't know that for sure until it unwinds.

Bubble is not a bad thing if you ride on it long enough. There is no bubble in NZ housing even there is don’t see it will unwind in years to come.

short/medium turn yes. Long term no. Spending more than you earn based on a paper value of a home is the greatest con of all. And most of NZ fell for it.

we had no choice

If the value of your house is increasing,... you can spend more. Doesn't take a rocket surgeon to figure that out.

Rising house prices, generally encourage consumer spending and lead to higher economic growth – due to the wealth effect. I've wondered for a while if the reasoning is correct. Because it could also be that rising house prices, if caused by a rising private debt:GDP ratio, will lead to increased aggregate demand in the macro economy because aggregate demand = GDP + the change in debt.

Well they just say it as it is, "stronger house price inflation will support consumption, residential investment and GDP growth in coming years" which is true

Correct in the near-term, but it's hard to imagine how expensive housing will make the country better or more productive in the long term.

Oh well, someone else's problem.

Only better health and safety and tougher regulations can make the economy more productive, when people are completely safe from any risk and totally secure in their job they will produce at maximum capacity.

From the generation that introduced participation medals and rubberised playgrounds for their children.

Doubling of land prices approximately every decade in NZ town/cities with populations in excess of 100K+ is both sustainable and very likely in our lifetimes.

How is it sustainable ?

I too am interested as to how something that sounds completely unsustainable is in fact sustainable by BHSL's reckoning..

What's BHSL?

Due Dilligence aka BuyHighSellLow

That guy was a terrible person, despite his accurate predictions. Glad he's gone.

I think you got that wrong, nobody would be silly enough to call themselves Buy High Sell Low

Selling is for fools. just buy.

I find ANZ's predictions on both, no OCR cut and higher house price in the first half of 2020, slow. Both of these have been obvious to me for several months.

But banks change their predictions like some change their underwear - daily.

The predictive record of bank economists is really poor.

One could suggest that the should stick to analysing rather than predicting.

In September 2017, Jacinda Ardern promised "houses for all". The median house price in NZ was $525,000.

One year later, it was $560,000 (+8.5%).

Another year later, it was $597,000 (+6.6%).

In the latest 3 months, it has risen to $629,000 (+5.5% in three months).

In context, 8% in the coming year is normal, if not a bit sad for those waiting the houses for all part.

RBNZ did not agree with Jacinda Ardern. RBNZ and Orr decided that what is needed is higher house prices.

So the Government of the day has no influence at all over house prices?

They certainly didn't legislate for higher house prices while the RBNZ cut rates and relaxed the LVR restrictions.

They appointed Orr and changed the RBNZ mandate, adding employment to the mix but I appreciate that it's election year and the default for the Left is going to be accentuate the positive and eliminate the negative so let's ignore those facts.

Adrian Orr was not appointed to boost house prices and employment targeting is also not targetting house prices.

The rise in house prices isn't a result of labour legislation, it was the result of the reserve banks response to a weakening inflationary outlook, both locally and globally.

My point is that Jacinda Ardern is either unable or unwilling to keep house prices down. She is in power, when she’s at work, so can do anything she has the political will to do. She could direct the Reserve Bank. She has changed some things and obviously chooses not to be effective.

She lacks many critical competencies and has failed to deliver on all major policy objectives, no argument from me on that.

I agree they seem to lack either the courage or commitment to act as is needed. The Foreign Buyer Ban and the honesty to confront the issue was good, however more is needed. They need to find their cojones (and perhaps take a leaf out of Prebble's book and get a bit hard with the ministries...demand action and face consequences if none is taken).

On the other hand, she should not direct the Reserve Bank. No politician should be directing the Reserve Bank.

I expect NZF is the handbrake. It will be an interesting election as I expect Lab/Greens really want to rule alone but such a prospect would alienate some of the swing voters they need to get there. Expect a lot of media spin over the next eight months. I will vote ACT unless it's close, where I could be tempted to vote NZF to keep them as king/queen maker. Lab/Green would be apocalyptic to a non woke non SJW, CIS pale male stale boomer.

Agree with all that. The level of disinformation is likely to be pretty high, I'd imagine. Brexit bus, Aussie-ute-tax high.

I feel like you need to weave in Intersectional and TERF into some of your references too :)

Well the median wage in New Zealand is $52,000, so a couple on the median wage who take home $84,000 after tax before any student loan payments only needs to save 8% of their collective pay to ensure their deposit merely tracks house price inflation.

They have to save 8% of the increase in house value for it to track house price inflation, and on a wage that is only going up 1 to 2% a year.

If it increases by 8% then the median house prices as at 31/12/20 will be be $679,000, a $50,000 increase. While the extra deposit only amounts to $10,000, the buyer would be adding $40,000 to their loan, an amount they will pay interest on over the following 25 years.

BTW: If it does reach $679,000, then the current government will have presided over a 29% increase in house prices since coming into power in October 2017. This exceeds the 25% increase from September 2014 to September 2017. Go figure.

So a 8 percent annual increase on the average value translates to a mere 100 Billion in additional housing wealth without factoring in additional stock , circa a third of ours nations GDP. With an extra 100 Billion we can buy more homes , so simple., once you know how.

"""""""""""""Wealth"""""""""""""

No matter whether you vote red or blue it seems that they are working directly against the interests of you and your family as a native born kiwi.

Ardern has forgotten what she was elected for and who even voted for Orr the unelected moron who thinks the medicine New Zealand needs is more rampant housing inflation.

As long as the underlying impediments to supply constraints (and excess demand via immigration) are not dealt with, then any extra disposable income will be capitalised in the value of the restricted asset.

And as the saving can be leveraged due to the magic of bank lending ratios, then the value of the restricted asset normally increase at a greater rate than the saving.

And it is raw land and development costs that are the biggest impediments.

Work out how to build houses cheaper - section prices go up.

Govt. subsidies to make it easier to buy a house - section prices go up.

Wage increases - section prices go up.

So for all the benefit any of the above savings made, within 3 to 6 months, they have more than been absorbed by housing price increase, the net effect is that most are worse off.

That's why the median multiple is a useful tool to determine whether the market as a whole is functioning alright as a steady/stable low median multiple signals that whatever wages and houses prices are going up by, they are stable relative to each other.

Global headwinds will keep OCR at its historical low for at least a year. NZ will embrace its coming golden decade. It will be soon synced with Melbourne and then Sydney (not only house price but so many other aspects). Smart people will start moving this way from the other side of the straight. Globalization 2.0 has so much to come.

House on beach at whanga goes for around $4 million...House at palm beach northern beaches in Sydney can be bought for $2 million.why is it so?so much opportunity to earn great money and have everything on your doorstep!!!!nd prices are crazy

I call BS, you forgot a "0" beachfront houses in Sydney go for min $20 Mill

Yvill Maaaate!!!!

Look on realestate.com.au.Type in Avalon or Palm beach.Look at the incredible views some of these 2 mill properties have.

Note that this is the furthest you can get to city centre ie the north.Think your looking in central city or Eastern suburbs.

Have a squiz Yvil i think you might be suprised!

Yvil.Google 17 cabarita rd avalon beach!!!!They are asking 1.9 mill.If that was whanga they'd be asking 4 mill.Either Sydney is way under priced or Whanga is way over priced.Only time will tell.

Yvil?

There are plenty of 3, 4, 5 million dollar houses at Avalon Beach as well though, right? Look at free standing houses in inner suburbs and it's pretty clear that Sydney is more expensive than Auckland on a nominal basis.

Yes that's true but I wasn't comparing Auckland to Sydney.I was comparing whangamata to Sydney!!!

Might be worthwhile to point out that the stamp duty is payble on top of that - so add another 100 K to the price of that proprety.

They have expensive stamps in Oz!

Bs ANZ.

Middle of the year is winter, in an election year.

This is not going to happen.

After the summer period, house trading will stagnate as always as people wait for the election to pass before making any moves. Where do they find these economists?

Maybe they are just hoping this prediction will come to pass so the reserve bank doesn't cut the ocr again.

More profit for the banks.

Good points. Although, we've got 5 months of the year before winter, so things could shoot up a fair bit before then. And winter might be flatter, but doesn't mean prices can't increase.

I have a suggestion. That economists and people in general (including me) should refrain from % predictions. It's a fools game.

I mean '8%' - how ridiculously precise is that, given all the potential influencing factors.

Rather, comment on the general direction and scale of price changes, and the reasons why. AND acknowledge the great limitations of prediction.

I think this 8% prediction is just a bat signal to all Chinese investors encouraging them to circumvent the FBB via Singapore.

Not going to happen. Xingmowang highlights that China is nigh on perfect, thus the idea that folk would flee the country with their wealth is absurd.

Both the Council of Mortgage Lenders (CML) and the Royal Institute of Chartered Surveyors (Rics) predict that house prices will rise by an average of 7 per cent across the country in 2007.

https://www.independent.co.uk/property/house-and-home/is-2007-the-year-…

Positive factors for the housing market include the continuing demand for property - from families, as well as immigrants and speculative investors. Interest rates low by historical standards also augur well for prices, as does relatively low unemployment.

It seems the down side reasons outweigh the upside reasons for a rise are highlighted more in the article and yet the the ANZ headline is the increase will be 8% this year. Imagine if the narrative was that prices would drop by 8%.because there is just enough reasons if not more for that to happen, but of course that would not suit their agenda of debt to you burst. Stoking the fire of fear of missing out is their best profit narrative which over rides the fundamentals every time.

All across Auckland there us a serious shortage of homes on the market but a massive volume of buyers - it has rapidly become a sellers market. Open homes last weekend were packed with buyers! So Auckland may actually see a 10% lift this year while other areas could be 15% plus or even over 20% like Gisborne, Palmerston North, Hawkes Bay etc.

Please could we have a forecast for Auckland v rest of NZ?

Auckland is 44% of sales.

Sales rise in Auckland is 13% last 4 months

Meteoric rise in Dec was mostly in brackets above $1.2 million.

It's the election year 2020 and all levers have been pulled to liquefy and boost the Auckland housing market. Average Auckland homeowner (and likely voter) will get at the least a 50k equity bump. That is just slightly less than the annual take-home pay of the average Auckland wage earner (likely to vote Labour or Green if they vote at all). Auckland decides elections now and the swinging Auckland voters are the most important of all.

How is it possible that house prices are rising again?

The Govt got rid of foreign buyers saying they were the problem.

"Speculators" were hit with CGT, loss of depreciation, high LVR's, ring fencing of losses, all of which were said would cool the housing market.

On top of that the Government was going to flood the market with a 100,000 new houses, causing competition plus making the RMA easier to work.

Then the Reserve Bank (no doubt under Government influence) dropped interest rates to close to zero so buyers can borrow as much as they want. Even immigration has slowed but still prices keep rising.

We will soon be in an impossible squeeze between ever rising rents due to discouraging rental investment, and ever increasing house prices.

It's going to all blow up sooner rather than later.

People are buying in the regions. Auckland can continue to stay moderately flat, with the regions going through a growth spurt there's less dragging of the averages down.

Agree. It dosent make sence. Perhaps cash printing is on track to make $100 bill's worthless. Money sure is. Heap though. RBNZ must be wondering it the big cuts last year were actually a mistake.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.