The mortgage money was still flowing right till we went into lockdown, according to new Reserve Bank residential mortgage lending by borrower type figures.

Over $6 billion was advanced by the banks in March and that was the highest tally for a March month since 2016 at the height of the boom.

And the first home buyers, who appeared to pause a little in February, were back in force, borrowing well over $1 billion.

Of this money borrowed by the FHBs about 38% was for high loan to value ratio (LVR) mortgages (above 80% of the value of the house borrowed). That's been fairly typical as a ratio, but the size of the mortgages has been going up.

For March, the latest figures show that FHBs took out $433 million in high LVR mortgages. That was divided among 854 mortgages, so, an average of an eye-watering $507,000 per mortgage.

In total the FHBs borrowed $1.137 billion, spread among 2472 mortgages, for an average-sized mortgage of nearly $460,000.

The amount borrowed by the FHBs was not a record high. That remains the over $1.2 billion borrowed in November. Nor was it a record high in terms of the percentage of the total mortgages advanced in the month.

In March the amount borrowed by the FHBs was 18.4%, which was below the high water mark of just under 19% in January. In February, however, there had been quite a sharp pullback, to under 17% of the total and less than $1 billion.

The amount borrowed by investors remained at similar levels to as in the recent past, with over $1.3 billion borrowed, making up 21.3% of the total.

The Reserve Bank has indicated it will very soon lift - for the next year - the restrictions on how much banks may lend for high LVR loans.

At the moment the banks can advance as much as 20% of their new mortgage lending on high LVR loans to FHBs and other owner-occupiers.

The latest figures outlining how much of the banks' money was advanced in high LVR loans were also released on Wednesday.

These showed that the banks had plenty of breathing space.

After exemptions we applied, just 12.3% of the banks' new mortgage money had been advanced for high LVR loans.

87 Comments

first home buyers had a pre-lockdown surge ? doubt it. just a lot of refinancing classed as new lending

First home buyers are a specific category - IE people who have not had a mortgage before. The $1 billion-plus referred to in the article will therefore be NEW money.

David, thanks for the reply. I messaged RBNZ a few months ago to get their breakout of remortgage vs genuine new lending. They weren't able to provide it.

So whilst the figures for FHB may be reported I just cant see how RBNZ can provide that level of detail even remotely accurately.

The C40 RBNZ data provides FHB data/ Auckland and New Zealand. , although not timely.

Oof

Glitzy, the fact that 'You cannot see something" doesn't mean it doesn't exist or that it's wrong

Each bank will be giving them a submission Glitzy. First Home Buyer is usually not that open to interpretation. It's pretty clear.

Now non FHB is different and will include top ups and refinances as well as new purchases, but not really sure what your point is. It's all new money to the bank that lent it. It's not loans rolling over into fixed or floating.

FYI David - technically these are not advances. The RBNZ data series is loan commitments. So the bank has entered a contract with the borrower but they may not be drawndown yet.

Thanks for the reply. Let me be more accurate. A first home buyer in the usual sense means a person who taking a step onto the property ladder.

However since a great deal of properties bought by investors are purchased using new trusts and these may or may not be classified as new buyers this means that we have a reporting problem.

Perhaps you should read the RBNZ definition, which is what bank data teams would follow....

https://www.rbnz.govt.nz/statistics/c31

First home buyer

A first home buyer is a borrower entering the home ownership market in New Zealand for the first time. In the case of more than one borrowing parties to a loan, borrowers are classified as first home buyers only if none of the borrowing parties have previously drawn down on housing finance for owner occupation. If the borrower, or at least one borrowing party, has previously drawn down on housing finance for owner occupation they are classified as "other Owner Occupier".

New debt right...as opposed to money. Some how the economy will need to be more productive in the future to be able to service that debt with actual money.

I guess you meant NEW debt.

I have three friends (late twenties/early thirties) who closed on houses after the pandemic had started. Yeah, I couldn't believe it either.

Its a massive amount of debt to be taking on. From a historical perspective (the full history of the NZ housing market), this could be the worst market timing (literally ever). Could be wrong of course, but the evidence certainly doesn't stack in its favour.

Literally insane. One (in Melbourne) bought on a 5% deposit. NAB has now come out saying they see potential for a 30% drop over two years - if that's what they're saying publicly already you have to assume their worst case is actually worse than that. 30% drop on a house bought with 5% deposit is a 600% loss on the equity. Just... why.

Yes I follow Martin North on DFA. He an ex-banker and just can't understand what has happened to the industry over there. Thinks its gone mad.

He hasn't understood the market for a very long time, he has also been wrong for a very, very long time. Do yourself a favour and stop following DFA, it's plenty of lovely graphs and analysis but it's predictions are just… well, wrong

This could be like the story of the boy who cried wolf. Martin might be boy crying wolf, but unfortunately for the property investors, they are the sheep.

If you were a smart sheep you'd still take a look to check the gate for the wolf, because the one time you don't, the wolf will be there and you're lunch.

Well done spruikers, more lives ruined.

FB

Sounding off again just like your wild 50% fall in house prices.

We wait and see.

by Foreign buyer | 23rd Mar 20, 4:09pm

If you have debt on property please tell me how you are able to sleep? I expect 50% reduction in NZ house prices when this is over. It is the greatest ever reset!

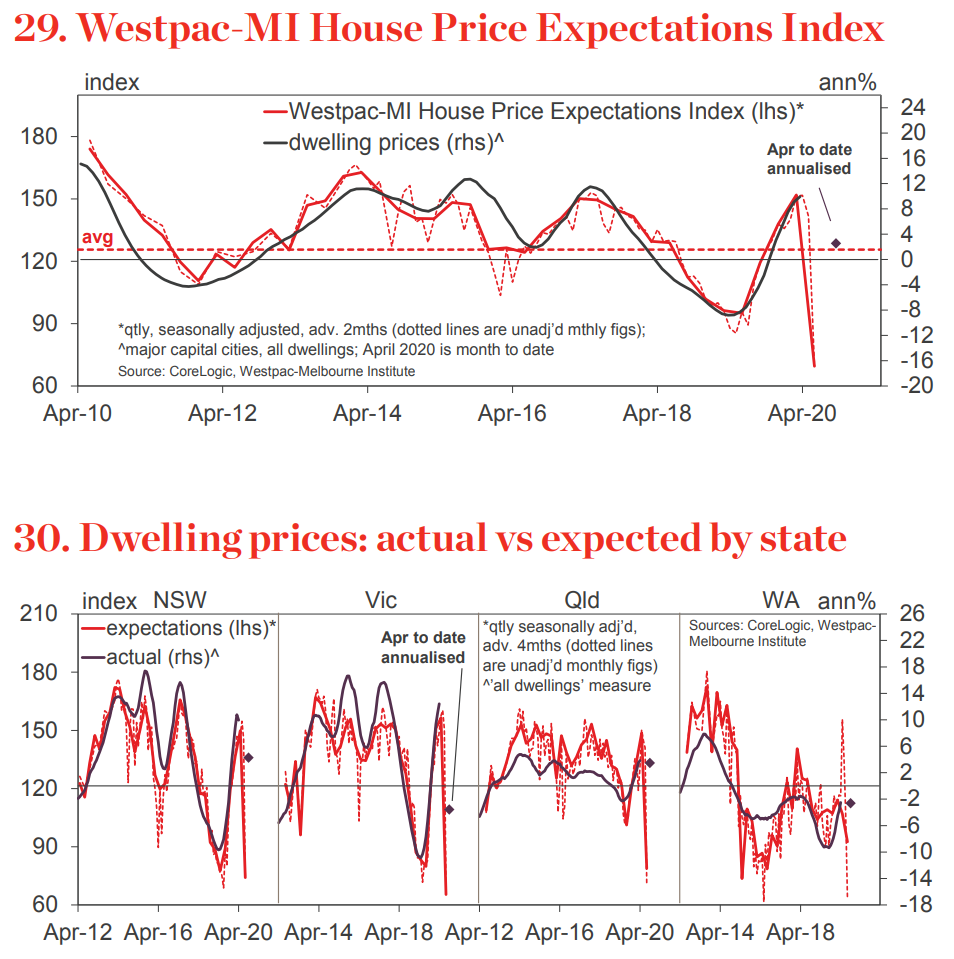

Is this graph a harbinger of things to come? (Keep in mind it's in Westpac's interest to 'talk the market up')

https://www.macrobusiness.com.au/wp-content/uploads/2020/04/rthw-2.png

{kind=link}

bw

Counters FB's 50% call by a long shot. :)

Might be like the WA chart - years of falling prices ahead of us.

Have you looked at the size of the bubble in Australian property when it is inflation adjusted? And realise we're in the same boat. I.e. our housing bubble is much bigger than what the US had in 2008. No chance of a 50% fall eh. And remember - its got far worse than what is depicted in these charts.

http://therealeconomy.weebly.com/uploads/1/1/2/0/11205553/729328626_ori…

{kind=link}

https://www.whocrashedtheeconomy.com/blog/2012/08/never-a-better-time-t…

Yeah, house price crashes don't work on the same time scale as share market crashes. Ireland took about 5 years to fall 50%.

But of course in your religion it's possible to have long stretches of double digit price growth but not long periods of double digit price contraction, because... magic? What is the voodoo explanation du jour, now that all the usual suspects have been zapped? Has Bindi got some sort of rain dance?

Have look at a graph of house prices in NZ fo the last 10 or 20 or 30 years, see if you can see a trend.

The recency and confirmation bias of the last 30 years for NZ property investors is so bad its getting embarrassing.

All I can say Yvil is think bigger - further back and see what you can spot.

Oh it's the stats illiterate one again.

Yes, bubbles show an uptrend when you are only looking at the uptrend part of the chart. You think you are looking at a meaningful timeframe from which you can extrapolate a trend to the moon, but you're not. So did everyone in Ireland, Japan, US, Spain, Bitcoin, Tech Bubble, etc etc etc. As it happens there is a comprehensive long term dataset for the US going back to 1890 (Case-Shiller index), which shows 0.2% long run real growth in house prices. But yeah, look at a 20 year time span in NZ and extrapolate that to forever as if it's a meaningful dataset, what could go wrong.

P8 - looks like its not just me who thinks house prices COULD fall 50%.

Yes IO.

We wait and see how accurate the flippant scaremongers are.

After all by your own admission you have been calling bubble burst for five years. Five years of scaremongering.

To me, forecasting a 10% gain in our property is just as scary as forecasting a 10% fall. Not sure why a trend down is deemed scaremongering from your paradigm?

If somebody said to me in 2012 that house price would go up by 50%, I'd say they were scaremongering. And we're now there - with all that associated debt, and not the ability to pay for it.

IO

Whats with this "COULD" now? A little unsure of your "mother of all bubble bursts" with a 50% fall.

I am just calling out the scaremongering.

You should perhaps modify your comments that this COULD BE scaremongering - as how do you know for sure that I won't be correct?

Unless of course you know for certain how the future is going to play out?

I'm not so arrogant to make that assumption - are you?

"Could" is the word used by people who have a grasp of probability.

Yep, on the 26th of July it could be sunny or it could be rainy or it could be cloudy. Really useful. Could is used by cowards.

A statement made 6 months in advance predicting house prices will (not could) reach all time high prices in March 2020 is much braver, you should try it and see how you go.

Yvil I'm not under financial stress right now because I thought a situation like this COULD happen. And had a plan for it. I didn't know when it would happen, but I knew it COULD.

So I'm now a coward in your books which is fine - simply because I was willing to address risk and because I know that I don't know for CERTAIN what is going to happen. And if its only coward who address risk by exploring the COULDs, then yes that is me.

In my opinion you're much better off exploring what you don't know, than what you do - its the things you're not aware of that will hurt you the most (like COVID 19). Exploring your own personal blind spots. I've been saying that we COULD have a 50% fall in property prices in NZ to help other peoples blind spots. I'm not saying its going to happen for certain but there's a reasonable chance it COULD happen. Now if you don't explore that as a possible outcome and don't have a plan for that possibility and you get burnt then its your own fault.

It seems to be the people on this site who 'know it all for certain' are under the most financial stress right now. One wonders why that might be.

If you're going to say that COULDs are used by COWARDS, I'll reply with DENIAL and CERTAINTY is used by FOOLS.

Yvil focuses on gathering evidence to reinforce why what he already thinks is correct, rather than carefully examining why what he already thinks might be wrong. This is the hallmark of an amateur investor/businessperson, as over the long run the probability of complete wipeout approaches 1. No difference in psychology from someone winning 5 in a row on the pokies and thinking they've 'figured it out.' Unfortunately NZ is riddled with Boomers who think they are geniuses because all they have had to do for 20 years is repeatedly double down on house price appreciation (and vote for pro-bubble policy). The idea that their own investing lifetime does not represent the full dataset is just a completely foreign concept, *even while they are literally in the middle of a once-in-multi-century event.*

The point is that anyone making statements about the future is working in probabilities weighing different potential outcomes, therefore it's always 'could' and never 'will.' You missed the point again because you are thoroughly stats illiterate. People who understand risk and uncertainty don't make 'will' predictions, they look at ranges of possible outcomes and then probability-weight them accordingly. Again though, you are a stats illiterate predicting a coin toss will be heads, getting heads, and concluding you're Warren Buffett.

Speechless, a truly magnificent burn.

Skyrocketing unemployment numbers, whispers of people trying to get as much cash out of ATM's as they can, tourism industry completely dead for the foreseeable future...

Landlords/Property Speculators - "It's just a flesh wound."

Dalio has put it that we've just been 'hit by a tsunami' - we don't know the level of the devastation yet but over the coming months it will become clearer.

Just on this; there is obvious reason for many to be very nervous whether it be employment, reduced income and meeting outgoings including mortgage payments, and especially so for SME business owners.

Unsubstantiated wild exaggerated comments and scaremongering especially by the likes of Foreign Buyer and Carlos67 is simply needlessly adding to the fears and worries that most people are now facing. I don’t suggest that one buries their head in the sand; everyone is already fully aware of the risks that exist and exaggerated claims inconsistent with respected commentators amounts to scaremongering and is neither necessary or appropriate.

So it would not be scaremongering to say house prices will rise by 50% but it is to say they will fall by 50%? There are people on both sides of these scenarios that have inverted opinions as to which is good and which is bad. Not everybody is fortunate to already own a home. Such people do exist...... you do know that I'm sure???

FB

I am not aware of anyone who has ever called a 50% short term rise in property prices - to do so deserves to be equally criticised.

I agree that not all own a home and I have often expressed the concern that homeownership for 25-35 y.o. has fallen from 65 to 35% over the past 30 years. That is a situation which you seemed to be in and I wish you and other young well in what is clearly a frustration. I do not suggest that this moment is the ideal or immediate time to buy.

However, your numerous posts show a lack of empathy for others. Next time you post over what is of concern to some, ensure that you do not display exuberant joy which you are prone to do. Your comment regarding a 50% fall was not only unsubstantiated and extreme, it had a smug sense of joy written all over it.

It must be quiet at your house when the AB's play the Ozzies.

I have been reading smug joyful comments from Boomer property speculators of the "avocado on toast" variety in these comment sections for YEARS. Your generation has actively voted to throw all following generations under the bus for your own gain and done irreparable damage to the social fabric of NZ as a result.

So yes, if you're a property speculator, I for one will be cheering while you hit the wall. If every property speculator in the country goes bankrupt that will be a great result. It's what you deserve. You reap what you sow.

Hear, Hear.

Correct

Telling FHBs that buying a house now could leave them *permanently unable to retire* is not scaremongering, it's responsible risk assessment. If you own geared property and you're getting nervous, you bloody well should be. What is wildly unsubstantiated is the idea that house prices will only drop 5-10% under a Great Depression 2 scenario.

Speechless, I see you are a new commenter here. Interest is littered with commenters predicting large falls of the housing market, they invariably disappear from the comments section 6-12 months later. Show a bit of respect for those that have been making correct predictions for years

You know if your still strutting about like a rooster talking about your March prediction in May, people will be feeling a bit embarrassed for you - "is he still going on about that?"

There are people that command respect, then there are people that demand respect. Guess which one actually get respect?

How many of them were calling it in the middle of a global pandemic and biggest economic contraction since the Great Depression?

The illusion of a pattern ALWAYS emerges from randomness. If you don't understand this fundamental concept and you gamble with borrowed money, you face a very high probability of getting cleaned out over the long run. Plenty of losers in the world who bet the farm because they thought they had figured out how to beat the roulette wheel. Spoiler alert: they didn't, and neither have you.

Under 'REPORT COMMENT' can we get an option for 'smarmy self promotion based on utter fluff'

So Yvil, for those so called been making correct precictions for years, did they predict there is this covid 19 pandemic happenning this year? If not, tell me why we should trust on predictions more than risk analysis.

I think what for you is observed as 'scaremongering' is simply an assessment of a possible outcome. I.e. rational assessment of outcomes vs an emotional response to a sub-optimal event (from your perspective).

Housing could fall 5% or unemployment and mortgage defaults could start snow balling and we see 50% falls or more - its happened before in other markets so no reason why it couldn't happen here. Does that trigger an emotional response for you? Neither outcome does for me.

IO

Good to see you re-evaluating your early call.

Cheers

"Of this money borrowed by the FHBs about 38% was for high loan to value ratio (LVR) mortgages (above 80% of the value of the house borrowed)."

And what's the bet they've drawn down their Kiwisaver balances to come up with their bit? Pretty good, I'd say.

So not only may they have ruined their present, they may have damaged their future as well.

to be fair, having it invested in stocks and bonds if the worst case rolls around is probably no better.

When the central banks have created bubbles in all asset markets and the safety of a bank deposit isn't necessarily that safe because of the debt associated to the financial bubbles....then the only option is speculating on gold or buying government bonds at negative real rates. Great way to save for an overvalued home.

Don't forget speculating on wildly volatile crypto!

Just watched this piece by Dalio. He talks about debt and deleveraging (its from 2012) but looks representative of where we are/where we could be heading. Debt growing faster than our ability to service that debt - even with interest rates near zero.

David, is there a regional breakout of the figures? I'm curious what the Auckland FHB figures are.

$507k average FHB mortgage, and we all know it's going to be higher in the expensive cites. I hope those FHB have decent solid incomes and haven't massively overextended.

When the PM and ministers are taking voluntary 20% pay cuts, and we could see 20% unemployment in the next few months, I don't think 'decent solid incomes' is a certainty by any means. Nobody knows yet how bad company earnings are going to be and the flow through to available funds for wages. Taking on debt right now is gambling for both the bank and the buyer (in my opinion...).

Exactly. Extrapolating current income/employment forward is nonsensical for almost everyone right now.

Indeed, taking on a FHB Auckland mortgage (likely to be $600k to $800k for many) right now looks fairly risky.. I wouldn't do it, i'd sit tight and wait, and look for cheaper rent in the meantime if renting.

Taking on debt at the moment is exactly what you should be doing if you are doing it for the right reason.

Buying anything that is going to return you over double the cost of borrowing is certainly what you should be doing.

This is the difference that makes successful people successful and the not so successful!!!!!

People that continue to wait for things to happen and those that don’t look for opportunities will always be an also ran!

This virus in NZ has been totally overplayed and has decimated many businesses as this Covid19 is not a dangerous virus whatsoever!!!

19 geriatrics from rest homes with underlying issues is no reason to close down the economy.

The trust is that we have been scammed and still are.

Why are we still in lockdown?????

Obviously many like being controlled.

Where is Phil Twyford our minister for economic development?????

They don't break it down. And yes, like you, I would make the assumption the city figures, particularly Auckland, would be higher.

C40 RBNZ data gives breakdown

ooof, just looked at the december 2019 numbers. Auckland FHBs with DTIs >6, on average borrowed $707k. So <$118k gross income (~$83k net after kiwisaver @3%), and ~$38k in mortgage payments (45% of income to service the mortgage). And thats at 6x DTI.. the category is >6x DTI, so there are worse numbers out there. And there were 181 mortgages in that category.

Edit: actually its not quite that bad if you assume its a couple, the tax take works out a bit less.. still not what i'd call comfortable, but a bit better than the above numbers.

She'll be right mate

All i can say is they have bigger cajones than me to take on that much debt on that little income. I thought 5 x DTI was uncomfortable, but >6, sheesh.

That's a death wish.

"After exemptions we applied, just 12.3% of the banks' new mortgage money had been advanced for high LVR loans."

At current house prices.

Everyone agreed that NZ and the rest of the world will be in a deep recession after this Covid-19 saga.

Now can anyone tell me; historically, has house price ever increased during a recession??

In a hyperinflationary environment - everything goes up.

Nothing 'goes up,' the currency goes down.

But the numbers on your payslip go up, and the numbers on your mortgage payment don't.. until the RBNZ raises rates to kill the inflation its been trying to generate for so long now. Inflation targeting is a curse.

Or the Government freezes wages to stop your payslip numbers from going up. How good did they have it in the 1970s/80s though? High interest rates keeping a lid on house prices, and a Government needing to step in because your wages were going up too fast.

Imagine taking out a mortgage today and effectively paying half the mortgage off in 5 - 10 years through inflation alone. Oh but colour tvs, cell phones and other "mod cons" not included.

Yes, certainly better to be a borrower than a saver if the scenario eventuates. I suspect there is a chasm of deflation between here and that particular danger. I don't really know.

Anybody that claims to know what is going to happen in the next couple of years beyond the bleeding obvious better be able to provide their time traveller credentials.

Mortage money up.......hope market does not fall badly for or all those FHB will be S@#$

Not a good time to be borrowing from anybody, hopefully they won't have to regret it.

Data only shows parts of truth. It won't tell you the whole story depends on which part of data you are looking at. Same as some data on convid-19, when it started, the motality rate was around 3%. People believed it and I am not saying the data is wrong. But now, see what happens in Italy? Was it still 3%? No. So I think it's just stupid that people saying that they can predict the future just based on the data. There are so many conditions are changing all the time could affect that predictions. So just wondering that, for those people who made prediction that for martch, housing price are going to reach a record high? Yes it did. Congratulations on that. But did you predict that we have a covid-19 situation now? What's the point to make a prediction just up to march and after that everything will fall apart? I think it's wiser to analyse the risks than making prediciton. Know the risks are involved with your decision. If it's manageable then go for it, if not, maybe not a good idea.

Virtually all of this will end up with the associated borrowers plunged into negative equity positions within the next 12 months. I feel for the fools who bought into this myth of ever-increasing house prices. Like in any Ponzi scheme, the latest to get onboard are the first to be shafted.

Buying now makes perfect senses if you re buying right!

3% interest rates just makes total sense if you are getting a 6% return if you are an investor, or if you are an owner occupier then if your repayments are less than the rent it would attract.

If you are looking to buy, it would pay not to listen to most on Interest.co who comment on property, as they are just doom and gloomers who haven’t been able to buy previously.

Get advice from people who are successful with property.

APPLY FOR A 3% LOAN!

Do you need an easy qualifying Business Loan, Home Loan, Personal Loan, Auto Loan, Debt Consolidation Loan....etc ranging from $1,000-$100,000 to business entities as well as secured and unsecured loans to individuals too. Good or Bad credit makes no difference with us with an interest rate as low as 3%. Applications are approved within 24 Hours. To apply, get in touch with us immediately via email: jameswunclerloanfirm@gmail.com

and be rest assured of getting your required loan amount fully granted to you.

Regards,

James Wuncler Loan Firm

Great exercise of irresponsibility during uncertain times at a large scale.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.