The performance of the housing market is "not consistent with an economy in the midst of the worst recession in 100 years" and a 'circuit breaker' is needed, Kiwibank economists say.

Commenting on the latest super-hot housing figures from the Real Estate Institute of New Zealand, Kiwibank senior economist Jeremy Couchman said double-digit price gains during the worst recession in 100 years, "just don’t pass the sniff test".

He said the Kiwibank economists were now no longer picking a correction in New Zealand's house prices for either this year or next.

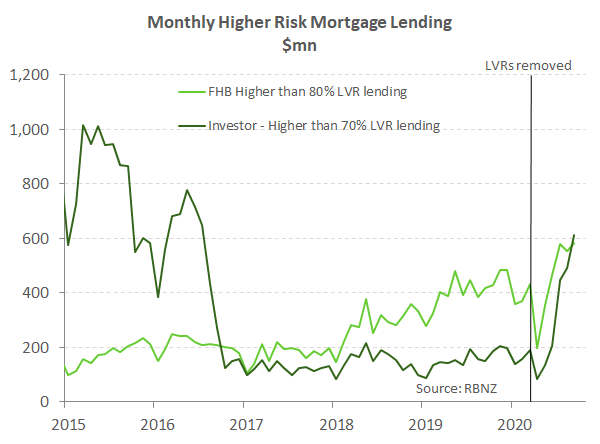

He noted that credit growth among higher risk borrowers is accelerating.

"A circuit breaker is needed, and the [Reserve Bank] has delivered with the likely reinstatement of LVR restrictions. Although to be clear, the RBNZ is not focused on house prices, but heading off a surge in high-risk lending."

Couchman says the strength of the housing market, and the rate of credit growth, out of lockdown has "surprised everyone".

Numerous factors are behind the phenomenal rebound in the housing market post lockdown, he says, including record low mortgage rates, the removal of LVR restrictions, and the distinct lack of listed property.

"An earlier return of the macro-prudential speed limits [through the LVRs] is warranted."

The 'speed limits' will "come back into play" from March 1, Couchman says, but given how banks’ speed limits are measured, "the handbrake on new high LVR lending approvals and lending will start to be pulled much earlier than March".

"Banks generally give pre-approval for loans for 90 days. Knowing the restrictions are coming in March, banks may start tightening up in December/January. Tightening of LVRs will most likely fall hardest on investor-related lending. Since April lending growth to investors has shot up. Particularly to higher risk investors, defined as those with equity of less than 30%."

Couchman says while the RBNZ looks to have "turned the heat of the housing market down a notch or two with LVRs", he notes that the RBNZ has also added more monetary policy stimulus this week.

"At the November MPS the RBNZ made good on a promise to provide banks with cheaper funding with its Funding for Lending Programme (FLP). From December, the FLP will provide banks with a cheaper source of funding and enable banks to pass on lower lending rates to households and businesses.

"Lower lending rates will continue to underpin the housing market next year. Just less of the cheaper FLP funding will be directed to higher risk mortgage lending."

78 Comments

So it seems all claims about banks not lending risky mortgages to their clients including those from the RBNZ yesterday trusting banks criteria were completely unfunded, who would have wondered?

The graph is a bit misleading. It's using 30% LVR for investors and 20% for FHB.

ANZ said that they were sticking to the 20% LVR for FHB, but have relaxed their threshold from 30% to 20% for investors. Ideally the graph would have 2 stacked lines for investors, showing borrowing under 20% and borrowing between 20 and 30%. We can expect the 20-30% range has increased a lot, and the under 20% range may only have increased a moderate amount.

Yes, noticed that too, that doesn't change the fact Kiwibank is lending more risky than it should.

But it wouldn't show what other cross security they may require on purchasers or guarantors other assets. So in effect, they will have more security than what the LVR shows.

My soon going to be ex tenants are buying a house with a 10% deposit from ANZ, just told me that their finance has gone through.

Though the rent they pay is quiet nominal for their earnings, they decided to get a place of their own thanks to the uber low rates.

Both husband and wife are working and getting around over 180k per annum.

If the Government were genuine about high house prices in NZ they would fire Orr. He is the property investors/speculators best friend. Uncontrolled high house prices will create massive social problems in the future.

It is a ticking time bomb! created by Orr.

Being Orr is a bit like becoming the captain of the Titanic after its hit the iceberg - then being blamed for the sinking.

He is pushing out positive messages to keep everyone calm, while pandering to the rich elite and telling the poor there are plenty of liferafts and everyone will be fine.

We always like to blame others for our mistakes. Blame no one, but just yourself.

How many of us have voted for National or Labour? :)

Interesting how Couchman says there needs to be a circuit breaker event but then goes on to tell us the FLP will "enable banks to pass on lower lending rates to households" - in other words more cheap loans will be provided.

Couchman has just showed us how hypocritical banks are and how insatiable and "profit at all costs" driven they are.

Like a glutton blaming the chef for causing his ever expanding waistline.

Especially if the collateral offered and accepted by the RBNZ for FLP is Residential Backed Mortgage Securities (RMBS).

Banks will pump up the RBMS pools by extending cheap mortgages underpinned by the RBNZ's FLP interest rate cost concessions.

And yet the RBNZ made this claim yesterday:

"Low interest rates are a global phenomenon, and reflect the fact that the level of interest rates needed to match savings and investment in the economy has declined over time. These developments have been largely outside the control of central banks."

Surely the RB wouldn't be that stupid as to accept RMBS' - didn't the bundling and trading of those kick off the GFC when the defaults started happening??

Surely… ???

Haha.. yeah maybe I answered my own question

Exactly: Residential Mortgage Backed Securities (RMBS) - are eligible for RBNZ repo funding operations.

https://www.rbnz.govt.nz/news/2019/08/submissions-received-on-new-mortg…

August 2019

The Reserve Bank has today published a summary of submissions on its consultation proposing a new mortgage bond standard aimed at supporting confidence and liquidity in New Zealand’s financial markets.

Submissions on the new proposed mortgage bond standard are broadly supportive of the introduction of a high grade residential mortgage backed securities framework for New Zealand – known as Residential Mortgage Obligations (RMO).

a new mortgage bond standard aimed at supporting confidence and liquidity in New Zealand’s financial markets.

LOL - no mention of a stability factor.

Wow.. now I'm convinced the RB is out to lunch. This is a BAD idea.

Wow. The RBNZ are just out of control. I just can't believe that they can get away with it.

Agree. Kiwibank is essentially saying: "Oh please RBNZ make me stop writing risky loans". Next up: "Please RNBZ loosen the restrictions on the amount of capital reserves I have to keep on hand" Followed by "Please RNBZ give me a bail out".

Ahh the blame game continues. Who's going to step up and be circuit breaker though? Clearly banks won't, RBNZ doesn't care & Govt spinning PR bull.

It's just a sign of our success, right guys?

Nothing like being rich on paper

"Its a good problem to have" (unless your 30 and have to dedicate every penny that lands in your bank acc for the next 20 years of earning)

30*

Actually Clemente, when I took my first mortgage out 30yrs ago every spare penny went to paying it back then.. nothing has changed really. 20 and 30 yr mortgages were the norm. If you're 30 now and think you should be able to pay a mortgage down in less than 10-15yrs then you're gonna be disappointed. Home ownership has always been about sacrifice - if you don't want to make it, don't buy - but don't complain either

Ah yes, 'it was just as hard in my day'. That old lie again.

Also, why in the hell shouldn't people complain? I have been saving. I have been sacrificing. Prices this year have gone up by twice my yearly take home pay. How exactly am I supposed to 'sacrifice' my way out of that?

Firstly -it's not a lie. Secondly if you insist one purchasing in on of the worlds most expensive cities then that's your call. If you can't afford to buy then that's just life - suck it up or move but stop whining

Home ownership is not a "right" but a privilege - the sooner some people accept that the happier they'll be

Firstly, yes it is. Secondly, did I say I live in Auckland? No.

Unless you actually experienced it you have no idea nor have any right to disparage what I said. If you live outside of Auckland then you should have no problems purchasing unless you're aiming to high. Cut your cloth to suit your budget

I didn't 'disparage' what you said. I pointed out tou were factually mistaken. Also, it's a bit rich stating in one sentence that 'unless you've experienced it you have no idea' and in the very next sentence completely dismissing my experience. Try taking your own advice.

Don't conflate the two. You called me a liar - something you have absolutely no idea about. As for your personal experience - seems there are plenty of people able to purchase in todays environment so obviously it can be done - perhaps you don't want home ownership badly enough

No. Look, there is a difference between the claim 'it was hard for me' and the claim 'it was just as hard in my day'. One is about a personal experience, the other is a general claim. That's the claim you were making, and that claim is a lie. Its simply not true that it was just as hard for people in general to buy a first home 30 years ago as it is now.

I'm not going to comment on the personal dig, other than to say please stop making unfounded assumptions about my personal circumstances.

Perhaps you should take your own advice. You're the one that said, quote"that old lie again". The "general claim" I made is far from a lie - it's a fact. You also were the one that brought your personal circumstances into the conversation not me. As I said previously home ownership has never been easy but if you want it badly enough it's achievable as is manifestly demonstrated by 1000's of families and individuals around the country currently.

Are you both missing the point? House prices are almost unaffordable in NZ for the average family. The earnings to house price ratio in NZ and Australia are INSANE. If you are saving for a deposit on an average income (or two) you will still struggle with main centre prices. People with money, investors and Banks do well, the average Joe struggles, especially if only one income. I do know, I had freehold rental and a freehold home in Auckland. I paid $180K for my house 25 years ago, built a minor dwelling on my section for $120K 15 years ago, now they are worth over a million dollars. AND the quality of the main house is awful (built 1961, no insulation in the walls, kitchen needs doing again) My 24 year old son will be living at home forever. The quality of houses in NZ are dreadful for the money. Are we protecting our future, or destroying it? Big business rules.

Yes, the system is badly broken.

The fact that some do well in a broken system but do not see that they do so on the back of this is disappointing.

Some even think they are doing well because this is the way it should be.

Al123 you are completely correct. Hook, you are completely wrong. It's obvious, Hook clearly is a boomer that just thinks millennials complain without good cause. The level of competition from overseas investors, immigrants, this crazy love of buying houses for investments and incompetent building legislation is at the heart of this bubble, something that was around but not to the same degree 30yrs ago.

It is time to tax heavily all forms of speculative housing. This will go a good way towards paying the hole created by Covid, stop the housing Ponzi from inflating even further, and redirect resources away from parasitic speculation and into productive activities, thus balancing the economy.

This is something the Government can easily do, bypassing and overwhelming the shortsighted and damaging policies of the RBNZ.

Not that I expect this Government to have the balls to do it (and neither would National have the balls to do it, mind you).

They don't have balls to do this. If they have balls, our PM wouldn't rule out CGT. At this stage, increasing the supply to meet the demand is not going to work, trust me, no one want to sell at a loss. All the new houses will just keep pushing the prices up until there is a break point.

And you just demonstrated a higher IQ than our prime minister.

The PM ruled out a CGT for two reasons - 1: It's political suicide, and 2: It'd be repealed by her replacement in a blink. The fact that it's been tried and rejected elsewhere in the world tells a story - it doesn't work.

Are you saying that other countries don't tax capital gains in this asset class (housing)?

BTW, this is not true.

Cheers.

I'm saying that countries who have tried a broad CGT have dispensed with it. NZ already technically has a CGT on Housing encapsulated in the Brightline marginal Tax imposition. I'm not aware of any jurisdictions that employ a system that taxes the owner of RE regardless of whether they sell it or not

Rentier capitalism has been stewing in the oven for decades... The parasites have their house portfolios now ... the damage is done

You would HUGE gonads to fix this mess

like

- outlawing the ownership (by any entity/person 18+) of more than 2 houses/titles ... give them 6 months to comply

- outlaw non-resident ownership

Hahaha.. you forgot to add making flying the sickle and hammer mandatory. That first suggestion has so many holes in it it makes a sieve look waterproof. As for the second - we already have a FBB or are you saying a NZ citizen/PR temporarily domiciled overseas for work commitments is banned from owning RE?

Just so you know - this isnt law yet ... the final draft might be somewhat more detailed

We are already knee/thigh/neck deep in hammer & sickle territory ... we may as well admit defeat and start socializing some of the wins as well ...

Just to clarify - what law are you actually referring to?

dont worry - its all just idle imaginings in case youre concerned

That would be like telling people that can't be kiwis anymore. What do you mean I can't be a selfish twat who speculates on housing making the future worse for other people (and a result for myself but I don't realise that yet)? Its what I do and how I 'get ahead' over my fellow citizens....it makes me feel superior...

It will go down like a cup of cold sick...

fortunr, unless you've been living under a rock for the last 5 years you'll be aware there is a "Brightline Test" specifically designed to deter rapid speculation. You need to understand that not everyone (in fact probably the majority) don't intend or are not equipped to start "productive" businesses (what the word "productive" actually entails I'd like to hear). It's easy to yell from the sidelines when you have no skin in the game.

and hows that Brightline test working out for us then?

It is still a tax obligation on rapid speculation. It was never designed or intended to stop price appreciation - even you must understand that

no holes in that sieve then?

sweet - i can sleep easy

LOL and buying a rental and selling it 5 years and 1 day later is not speculation ? Give me a break.

There had to be a cut off at some point. If you had a clue you'd realise most serious landlords hold properties longterm. Every asset class is subject to speculation regardless of how long it's held. I said the BL test was to deter short term speculation - not end it completely

the circuit breaker is coming ... in the form of no incomes

Renters - get organised and get a rent strike underway. Let the govt know you have all had a guts full.

I wonder if this may happen

If it does I'm buying THL and KMD - gonna be a run on campervans, tents and outdoor clothing. Maybe TRA could be good too - all those secondhand vans

Kiwi econonist saying.... Everyone is saying any sane person can see what is happening except our verh own Mr Orr who maybe has some personal agenda to settle with average Kiwi and FHB and is supported bu our very own JA and his team

JA gifts to national supporters / speculators for voting her and screw tradional Labour voted, who are been taken for granted as now who cares for next 3 years.

Cannot sack elected PM (side affect of democracy) but get rid of egoistic Mr ErrOrr.

When exactly should we expect manifestation of this 100 year recession?

No sign whatever at present or on horizon.

Economists have stuffed it up again.

Maybe you should look at GDP figs, hiring intentions and UE rate. Are you in some sort of parallel universe??

If you're employed outside of hospitality and tourism it certainly doesn't feel like we're in one.

There's plenty of other sectors suffering - ECE, education, health workers, Ag workers, farmers and horticulture, fishing, forestry, manufacturing, construction.... Not everyone works in the service and admin world.

Next January in will be 50 years since I bought my first house in Oxford, UK with my soon to be wife. I was just 21 and my wife to be was 19. I had just completed a 5 year apprenticeship but had saved enough for a deposit.

I was a post war kid from Cardiff who was from a extremely poor family. My mum was at the time the youngest tenant of a council house in Wales and my Dad was off work for 2 years with TB.

At the age of 5 we moved to Oxford and my parents had a small loan to use as a deposit on their first house. My dad had to cycle to the other end of Oxford to start work at 7.00am finishing at 5.00pm. He cycled home had his dinner and went out in the evening to do another job. The working week included Saturday morning then. My mum took us to school for 8.00am and then caught the bus to the City to work in a shop until she had to leave to pick us up from school. We had chickens in the garden and two allotments to keep us fed. Nobody was fat in those days.

We got our discipline from our parents and never bought a coffee or had a meal out while courting. Fish n chips was as good as it got. My working life at that time (I started work at 16) was 7.15am to 4.15pm Monday to Friday with 1 hour overtime Monday to Thursday, 7.15am to 12.15pm on a Saturday and 7.15am to 4.15pm on a Sunday. My wife worked shorter hours than me because I went home for dinner at Lunchtime. When I got home from work I Had a sandwich and then worked on the house until bedtime to make improvements. My only time off was Saturday afternoons when I played soccer.

We bought and sold 3 houses over the next 12 years with the same work schedule for me. We had 2 children in the 70’s so instead of working my wife took in international or local students to keep us moving forward. I kept building extra rooms so we could have more students. By 1983 we lived in the best part of Oxford, we were now having six students and our two kids were at private schools. We left the UK in 1988 and had not at that time ever bought new furniture or TV. When you were really poor you never forget and you never waste anything. My kids are now in their forties and own houses and have good jobs but the waste I see from them just amazes me.

I am now 70 and have just sold up in the Far North and moved to Wellington to help with our two Grandsons. We wanted to put our surplus cash into a bank to give us extra income but at 1% it is not viable so we have just bought a brand new house as a rental that will give us a 4.5% return. You will find a lot of us Boomers doing the same.

I worked hard all my life to get what I have and I’m not ready to give it to James Shaw and his lot. We have a Trust that owns everything and we plan for it to be a inter generational trust for my Grandsons and their Children. We remember the stories from our Grandparents, parents and our own experiences and don’t intent for our future family to have the same experience. All this has nothing to do with speculation but everything to do with hard work.

My advice to you youngsters is to get on the housing ladder somewhere and the more work it needs doing on it the better as it will be cheaper. Then all you have to do is work on it and time will take care of the rest. Don’t listen to the Bernard Hickeys of the world as they have no idea what they are talking about, they are just a bunch of Hacks.

The past simply aint the future sorry

Boomers had it sweet

they rode the biggest resource consumption boom ever

Never to be repeated

https://ourfiniteworld.com/2020/11/09/energy-is-the-economy-shrinkage-i…

You have no idea what it was like, and neither do the Hacks who write about it. You guys have no idea how cushy you have it. It was our post war generations hard work that gave you what you have. You can choose how to use it but it seems really hard work, two Jobs and working every night to improve property is not one of them.

perhaps this explanation might assist...

"money is a token of energy exchange.

if you artificiallly expand the money supply by creating ‘infinite debt’, what you are doing is borrowing against the collateral of the future. (your children’s future to be exact)

politicians have done this to keep voters happy and themselves in office. This passes the buck to the next generation.

This worked as long as (cheap surplus) fossil fuels powered the system and created ‘infinite jobs’.

We are now the generation where the energy input has slowed, and seems likely to stop.

‘cash’ (the call on energy exchange), is accruing in the hands of fewer and fewer people, while more and more people are getting less and less. These are the haves and have nots.

Cash mountains cannot be re-invested in factories producing widgets, because fewer people want to buy them, or can afford them. Bezos must keep his game of ‘pass the parcel’ going faster and faster, otherwise Amazon will collapse. He does not create wealth, only pass stuff we don’t need, hand to hand.

People are finding themselves priced out of living itself, hence the millions of homeless, and proliferation of foodbanks."

I don’t know what you are on but it is not good for you. The future is amazing, I wish I was going to be around to see it. But at least I know my Grandsons will have a great and interesting future as science picks up pace to gives you things you can’t even imagine now.

Debt

You may have heard something about it?

How there is somewhat more of it around these days?

Honestly you boomers are clueless

Its not a matter of how "cushy" you think the kids have it

Its a matter of future prospects

THAT was why the boomers fluked it

Because the resource base and the requirement for a mountain of Debt says all those promises about the future are about to implode

and no science isnt winning the war .... otherwise the Debt mountain would be necessary

Oh that is nothing we were so poor we used both sides of the toilet paper and also wore my underpants inside out to reduce laundry detergent expenses.

Actually we never had toilet paper. Old newspapers with pictures of useless future generations was the order of the day.

Laundry detergent? You have to be kidding. It was a hard bar of soup in a tub in a old outhouse next to the outside loo.

Just read this on newsroom

IDEASROOM

A difficult year … but life has never been better

It has been one of the most difficult years in recent memory, but research shows life is actually getting better, and we are the most privileged human beings to have ever lived on this planet, writes Andrew Taberner

2020 has been quite a difficult year for us all – perhaps the most difficult that many of us have experienced. As the year draws near to a close, our fears about climate change and the post-pandemic economic forecast may have left us feeling gloomy about our lives, and about our prospects for the future.

Now seems like a good time to take stock, and to remind ourselves, that in fact, life for most of us, around the globe, continues to get better, year upon year.

I’m not saying this in a ‘chin-up’ or ‘Pollyanna’ sort of way, but as an evidence-based statement. I have a professional background in physics, and have spent much of my professional life measuring things, particularly the way the human heart works and how it responds to stimuli, stressors and disease. As Lord Kelvin, perhaps the most important physicist of the 19th century said, “To measure is to know”.

Understanding and appreciating our lived lives is a complex and ultimately subjective experience, but it is still possible to measure the quality of life. Numerous researchers around the world have done so, and their data are largely indisputable: life is getting better, and we are the most privileged human beings to have lived on this planet.

The Historical Index of Human Development is one objective index of human development, which allows us to measure how life quality changes over time. This index includes measures of life expectancy, access to information, literacy, education and so on. And according to these measures, life, for most of us, keeps improving.

Just because something is bad today doesn’t mean it was better in the past. We have reason be sceptical, but many more reasons to be optimistic.

This evidence may not align with our subjective assessments: in 2018, 18,000 adults across around the world were asked the question “is life getting better or worse?” Just over 40 percent of people in China thought life was getting better, and it turns out they were the most optimistic – few residents of western liberal democracies, in which life is demonstrably and measurably better, think life is improving. Perhaps it’s time to better appreciate what is good in our lives?

How we assess the quality of our lives is a personal matter, but there is value in obtaining a broader perspective, by comparing our lives, for instance, to those of our ancestors. When we do so, the evidence of progress is striking.

Two hundred years ago, most human beings could be expected to live for little more than 30-40 years. That’s if you survived childhood; 40 percent died before age five, even in wealthy ‘Western’ countries. Today, Kiwis have nearly the highest life expectancy in the world, at ~81 years. Much of this advance has been as a result of knowledge discovery and technology development in nutrition, food supply, sanitation and medical treatments.

Education is another important indicator of human development. In 1800, almost 90 percent of the world’s population could neither read nor write. My great grandfather, Thomas Taberner, according to our grandfather, could barely write his name and at the age of eleven began working in a coal mine. His first two wives died in their 20s; his third spouse, also illiterate, was my great-grandmother. My great grandfather on my mother’s side was sent to work in a flax mill at Raglan when he was nine. He never completed any more schooling.

In 1820, 90 percent of the world’s population, including many in ‘the West’, lived in extreme poverty and struggled every day just to survive. Now, fewer than 10 per cent are extremely poor. This millennium alone, 170,000 people been lifted out of extreme poverty every day. Although many remain poor, those numbers are still staggering.

And for those of us in wealthy societies, think of the impact of the development of household appliances, which have cut the number of hours that we as families spend on household chores from 60 hours a week in 1900 to less than 19 hours a week today. So much hassle has been removed from our lives by the invention of the washing machine, the vacuum cleaner and also the refrigerator – the latter being perhaps the appliance most difficult to imagine life without.

These advances we’ve made have come at the expense of enormous amounts of energy and resources from the earth, and whether that’s sustainable, long-term, is another story. I hope that we will be able to raise the quality of all human lives, at lower energy cost and in a way that will be better for the planet. But it’s important that we don’t romanticise the lifestyles of our ancestors. If we want to go back to ‘the good old days’ we’ve got to be prepared for 44 percent of children dying before they’re five years old as a result of untreatable life-threatening diseases, so say nothing of near-continuous warfare and conflict.

Covid-19 has been referred to “unprecedented” and in many ways it is – including our ability to control its spread. In the six weeks that the so-called Spanish flu hit New Zealand in 1918, 8,500 people died. Samoa lost 22 percent of its population in that pandemic and in Aotearoa around 2500 Māori perished.

In terms of the number of deaths, and lives ruined, Covid-19 doesn’t compare to the Spanish flu. That’s because of the advances made by learning institutes and industries here and around the world, which means we have better information, better communication and better understanding of viruses and how to contain them. New Zealand has done well in the Covid-19 pandemic because it has listened to its scientists.

Yes, there are myriad reasons to be optimistic, and statistics that can help us take stock of how much better our lives have become. New Zealand has one of the best healthcare systems in the world, rates of violence are at historical lows, and we are living in a historically peaceful era that has been referred to as ‘the long peace’. In addition, leisure time, travel, information, freedoms and human rights are all increasing.

When considering whether life is getting better or worse, we need to remember to do the maths. The numbers show it’s not all bad news, and most of it is good news. Just because something is bad today doesn’t mean it was better in the past. We have reason be sceptical, but many more reasons to be optimistic, and especially to be grateful.

Remember that when the Nicotine & Alcohol industries uttering that we're not a nanny state, we're all responsible adult. Regulation, circuit breaker is the last thing the industry need. Not much different to the Banks. Magically they're prudent enough, so please. This is a century life time opportunity to own multiple houses, mortgage to the tilt, LVR gone, ASB started their own? - move away from them, change to the Banks which fundamentally sounds and understood that 'this is the way' - Banks must lobby the current govt. to completely remove the bright line test. This is the way to quickly support the booming economy.

"This is a century life time opportunity to own multiple houses ..."

when you see comments like this it makes you proud to be a kiwi

Phew. Lucky I got my pre-approval for $700k in now then, with a $110k deposit. Sure. I'd be paying a low equity fee, and I can't get the special rate, but my repayments for a 20 year mortgage would still be less than my rent and what I was putting into savings for the deposit, and I'd bump those up for the first year anyway to get under 80% lending ASAP.

What the hell is a circuit breaker if not a recession? Recessions are brutal on those who lose their jobs and a worry for everyone else that they may lose theirs.

The housing crisis is purely government created:

1 Too many new people

2 Too many regulations

3 Too little productive activity

4 Too much wasteful activity

The governments response has been to pretend it wasn't them, they didn't do it and get the RBNZ to put interest rates down to hide the evidence.

How do we reverse the downward spiral of the last 30 years?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.