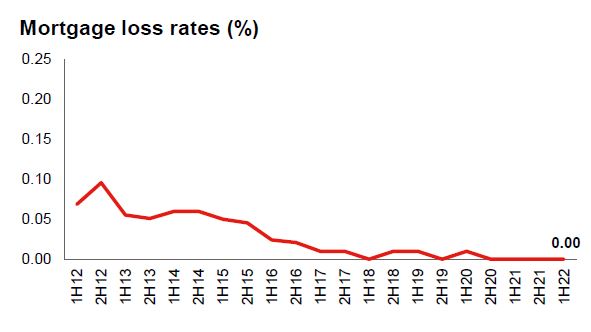

Westpac New Zealand has been making "really sensible" decisions about who to take on as home loan customers, which are flowing through to record low mortgagee sales rates, CEO Catherine McGrath says.

"Mortgagee sales are at historic lows. We've had four in the last six months as compared to 70 in financial year 2017," McGrath says.

"It's really showing that we've been making really sensible decisions about who we've been lending to. And yes, interest rates are rising and we may see them increasing again. But I've been pretty happy with the work the team have done in terms of how they look at how people can afford their debt, and what sort of interest rates we should assume so we don't just assume that servicing is based on the rates they are getting on the day that they take out the mortgages."

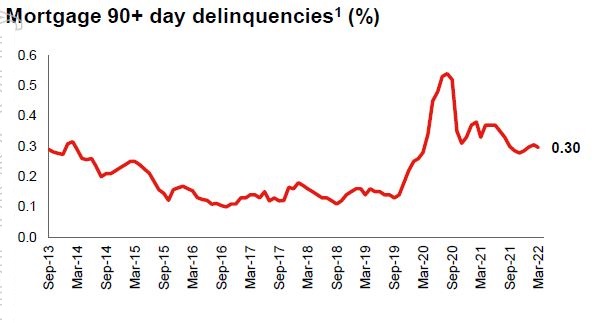

"The other thing we're seeing is that consumers are doing really well on their loan repayments [because] 68% of our home loan customers were ahead on their mortgage repayments at the end of 2021. So that's good to see that we are naturally preparing ourselves for some more challenging time ahead," McGrath says.

"And those customers were ahead of their scheduled mortgage payments by a median amount of $11.000 or about 10 months. So you can see that there's a reasonable amount of buffer that's been built up in there."

Westpac NZ's interim results, out on Monday, showed home lending grew 7% year-on-year to $62.2 billion at March 31. The bank's loan provision ratio dropped to 0.4% from 0.5%.

Supporting borrowers, the official unemployment rate is 3.2%, the lowest it has been since Statistics NZ's Household Labour Force Survey began in 1986. However inflation is at a 30-year high of 6.9%, and on Friday Westpac NZ's economists predicted house prices will fall 15% over 2022 and 2023.

Last week Westpac NZ's competitors ASB and ANZ both increased the interest rate they use to test whether mortgage applicants will be able to continue making loan repayments if interest rates rise significantly. ANZ's now at 7.15% and ASB's at 7.35%. BNZ's likely to increase its test rate from 6.75% this week.

Asked where Westpac NZ's test rate is at and whether it has been increased recently, McGrath says the bank uses a couple of measures when it looks at a home loan stress test servicing rates.

"The main relevant test right now is that we're adding 2.5% to retail rates, and making sure that customers can service that," she says.

Westpac NZ's current carded, or advertised, two-year rate - typically the most popular borrowing term - is 5.19% for those with at least 20% equity. Adding 2.5%, takes it to 7.69%. (See all mortgage rates here).

Charts below from the Westpac Group for Westpac NZ.

*This article was first published in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

10 Comments

Let's see how the mortgagee sales look in a year or two before being so smug.

It's not hard:

Banks extend around 60 % of their lending to one third of already wealthy households to speculate in the residential property market because the RBNZ offers them an RWA capital reduction incentive to do so.

{kind=link}

Furthermore, banks have migrated away from lending to productive business enterprises because the risk weights can be as high as 150%.

{kind=link}

And it's worse than that. The banks are even more encouraged to lend to residential housing because the government comes out and says that they will back stop mortgages at the first sign of trouble. Why the hell would they lend to anyone else when the government guarantees mortgages are virtually risk free?

They are saying this to restore confidence, due to the latent fear of mortgagee sales for overleveraged boomers. IMO the banks will simply ask over leveraged investors to sell without mortgagee sales to avoid crashing the prices too hard in a sea of mortgagee sales.

Do Westpac have any exposure on this? Second tier home loan lender.

Basecorp Finance has completed a successful issuance of an RMBS deal, its second capital markets RMBS transaction of 2021.Issuance size was $250 million and notes were rated AAA to BBB across six note classes by Fitch, with the transaction arranged and lead managed by Westpac New Zealand.

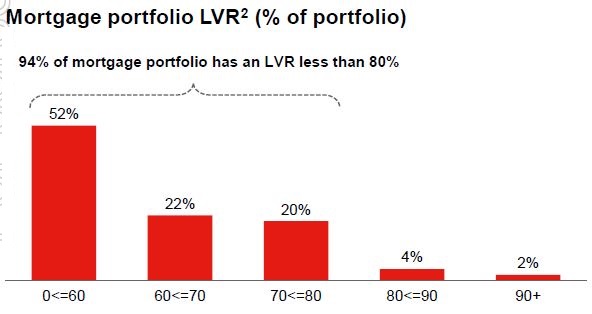

The mortgage portfolio LVR's above are probably done on some pretty high current valuations. If you take another 10% off these valuations that's probably going to be a reality at some point (this year?).

Exactly. The "V" is a fast moving number.

Already 26% of their lending book is at objectively risky LVRs. Their book is going to start looking very nasty/risky indeed now that Vs are falling fast.

If you purchased and fixed a rate in 2021 with an LVR of 80% what happens when you come up for rate renewal and the market is down 10%.

Your LVR is technically now over 80%. Does the bank hit you with the high LVR penalty rate on top of the already higher interest rate? Or do they just let it ride?

According to MisterB here -> https://www.interest.co.nz/property/115679/house-prices-declining-listi…

by MisterB | 7th May 22, 4:40pm

No it doesnt. The banks have gone on record to say they will not at a premium for existing loans.

Whereas BNZ State on their website (at the bottom): A low equity interest rate premium will apply to all loans with less than 20% equity.

https://www.bnz.co.nz/personal-banking/home-loans/compare-bnz-home-loan…

You are over thinking it Westie, look at it as you are already in the system. The rate will be what it is at that time. Same thing happened in the 80's but rates were north of 15%.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.