Kiwis increased their household borrowing at the fastest rate in some seven and a half years last month, new figures show.

The figures, collected by the Reserve Bank, will be of great concern to the RBNZ, which has been monitoring the increasing rate of growth of household debt.

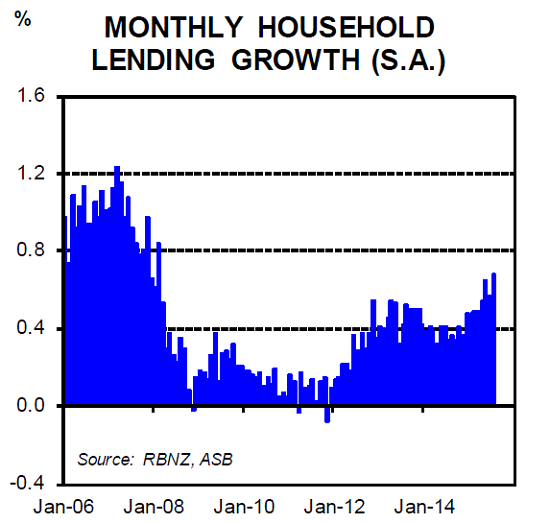

According to the RBNZ's 'sector credit' statistics for July, total household claims - which is mainly mortgage borrowing - increased by a seasonally adjusted 0.7%.

That's the fastest rate of growth since February 2008 at the tail end of the last housing boom. As at the end of the month total household claims stood at $219.813 billion, up from 218.726 billion in June. The latest figure is some 6% higher than it was a year ago, which is the fastest rate of annual growth recorded since September 2008

And, in a figure that will likely also cause the RBNZ concern in the light of its worries about a depressed and indebted dairy sector, agricultural borrowing has climbed by over half a billion dollars in the past month, to total $57.515 billion, which is some 7.9% higher than the figure a year ago. That's the fastest rate of annual growth in agricultural debt recorded since November 2009.

Business borrowing was more subdued, edging up to $85.827 billion in July from $85.815 billion the previous month, though the latest figure is up 6.7% on that recorded in the same month a year ago.

ASB chief economist Nick Tuffley said the RBNZ would see the lifts in housing and agriculture lending "as a financial stability focus, rather than an inflationary issue".

"The lift in housing-related credit is a further symptom of the recent re-acceleration in the housing market, while agriculture credit growth will in part reflect dairy sector cash-flow pressures."

Tuffley said, however, that the ASB did not think that the strength of credit growth would stopping the RBNZ from cutting the OCR to 2.5% from the current 3% (as ASB predicts), "given the housing market is not contributing to consumer inflation pressures".

On the agricultural borrowing figures, Tuffley said a number of farmers would be relying on overdraft facilities to cover operating costs, contributing to the recent growth in net debt (as opposed to borrowing for capital expenses).

Back on the household borrowing and on separate detailed mortgage figures also released by the RBNZ, Kiwis are still very much favouring fixed over floating mortgages, with the proportion of fixed rate mortgages now making up 74.8% of the total, up from 74.6% a month earlier.

But within the fixed figures there appears to be an interesting shift occurring, with more people going on to shorter fixed terms - possibly indicating a broadening belief that interest rates generally are going to be lower for longer, and hence no need to fix for very long terms.

The amount of money borrowed at floating rates, which had been dropping month by month, was fairly static at just over $52 billion in July.

The amount fixed for under a year rose to $61.526 billion from just $59.525 billion a month earlier, while the amount fixed for between three and four years dropped to $19.219 billion from $20.584 billion.

11 Comments

It looks like the biggest increase across all categories -- attributed to low mortgage rate?

Good for P2P lending?

Too expensive to float at 6.2%, even if short term fixed rates drop to 4.0% next year.

The margin (savings) between 6.2 and 4.6 from now til Christmas will outweigh the potential margin between (5.9 floating Nov) and 3.99 (1 yr fix) next year (maybe).

So we have not arrived at a brighter future? This government might need to borrow some more to dole out tax cuts to keep the wheels turning.

.

.

.

.

.

.

Doesn't the law of sectoral balances suggest that the more debt the private sector holds, the less debt the public sector needs?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.