By David Hargreaves

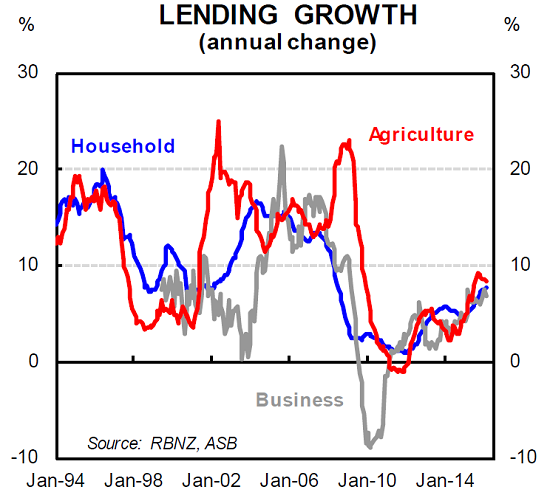

The New Zealand appetite for borrowing to buy houses is still sharp, with total household claims - mainly mortgage borrowing - again rising last month at their fastest annual rate since mid-2008.

The latest figures, collected by the Reserve Bank, show that for the fourth consecutive month total household claims increased by a seasonally adjusted 0.6% in February to a total of $229.875 billion, from $228.508 billion in January.

The annual rate of increase in the figure was 7.6%, up from 7.5% the previous month and the strongest rate of growth recorded since June 2008 at the tail end of the last housing boom.

In terms of just housing borrowing alone, it increased by 7.9% in the 12 months to February, compared with an annual rise of 7.8% in the 12 months to January, with last month's annual percentage rise being the biggest since July 2008.

At the end of January there was $214.207 billion of housing borrowing, up from $212.965 billion in January.

While the latest figures haven't shown any particular acceleration in the rate of borrowing that would unduly concern the Reserve Bank, our central bank would no doubt be continuing to watch the data closely. This is particularly the case given that separate figures released recently showed the household debt to income ratio hitting a new high of 162%.

Business borrowing, which has been really quite volatile in recent months, backed off in February after a big surge the previous month.

As of February total business borrowing stood at $89.990 billion, down from $90.116 billion in January.

The annual rate of growth in business lending was still 6.9%, but this represented a retreat from the 7.5% annual rate of growth recorded in the previous month, which had been the highest rate since early 2009.

Agricultural debt, being closely watched because of the global downturn in dairy prices, edged up by $29 million in the month to a new record high of $59.014 billion.

However the annual rate in growth eased to 8.4% from 8.6% the previous month and has been gradually retreating from the 9.2% rate seen in September 2015, which was the highest annual rate of increase since late 2009.

ASB economist Kim Mundy said while housing credit demand remained strong at the moment "we expect it to lose some momentum in the coming months".

"The Auckland housing market has cooled slightly in recent months, with prices dipping from recent highs. We will be watching March housing data to see if the recent lull is sustained. There also appears to be a marginal shift in mortgage duration preferences, with more borrowers choosing short-term fixed rates over floating rates."

On the pause in business credit growth in February, Mundy noted that this followed very strong growth in January, and said that on balance, business credit growth looked to be accelerating - which was consistent with "moderate economic growth".

Agricultural credit growth appeared to be peaking, albeit at high levels, she said.

"Working capital requirements to cover weak cashflows will continue to drive agricultural credit growth."

35 Comments

Why is this a surprise to anyone? It just makes financial sense to borrow as much as possible. Property in NZ only goes one way. And you better hop on the train before you miss out. Like myself, First Home Buyer...no chance at all.

I don't know if you are seriously deluded or just a troll. Your statement makes you come across as a creep who's only interested in them self - oh hang on you are. It makes financial sense to pay down as much debt as you can. If you borrow at a low interest rates and there is just a slight increase it can make the whole house of cards come tumbling down. Markets can change very quickly. Debt can magnify your gains but also magnify your losses very quickly.

No I'm not trolling and what I am suggesting is being reflected in reality. Leverage to the max and buy up as much Auckland property as you can. With this current government, you are practically guaranteed massive capital gains with no risk of losing anything. That's what happens when you welcome money from China, open the flood gates on immigration and have a tax system which provides incentives to borrow and buy property.

Try to prove anything I said wrong. You can't.

I know you don't like what I am saying, but this is what National voters voted for.

Guaranteeing capital gains and gearing markets are potentially risky as it is prone to externalities. That's why financial crisis occur regularly.

Asking others to prove that you're wrong is wrong-headed. You need to prove to yourself that you're wrong. That's a fundamental of assessing risk probability.

You say it better than me.

It's not a question of proving you wrong - it's being prudent.You call it reality - eventually the government will either change or the governments policy will change or more likely something will happen the forces a change on NZ. I don't know what that event will be but it's pure lunacy to believe that has has happened in the past will continue in the future. Dairy, oil and minerals industry's believed that the growth in China would continue for years to come - it didn't - it caught people out in the past and it will catch people out in the future. The economics of house ownership no longer make sense with the high ratio of income to price - at the moment it is the fear of missing out that is driving everything but timing to get out is very difficult.

Currently in CHCH there are 1747 houses for rent (according to TradeMe) - why would I want to buy with that number of rentals for rent. It has been like that for some months - there must be people who are haemorrhaging money each week they don't have a tenant. There are new subdivisions being created - supply is starting to outstrip demand. I've noticed that rentals are being put on the market - why - if they are such good value in terms of an investment.

Chch isn't getting another 40,000 people per year which is compounding an existing housing shortage. Nothing on the horizon points to any fundamental change. It's f'd. The difference between what you listed and housing is that housing is a need. And it's only going to get harder.

Yeah well, I don't want to miss out, can't risk it, I need to buy something, anything. This is the competitive world that John Key wants.

What actual property investors are doing is seeing the arbitrage between cost of mortgages (most never seen mortages as cheap as this in history of investing) and the yields available in secondary cities. Borrowing at 4% to earn at 7%. The 30% rule in auckland has also pushed auckland investors outside auckland

So why didn't you follow your own advice? You would have made a lot of money and would be jet setting around the world right now instead of writing on this forum?

Bad robot you had better get your sarcastic monitor chip looked at as it's malfunctioning.

While I agree, the thing is greed has taken over. Too many people think they can buy and sells tulips with one another to make themselves rich without actually doing any work ie making a good.

And it is working, they get rich by doing what the govt and council wants,

Ah the tulip argument. Thank you steven. It's all clear now. Houses are exactly the same as tulips. .. With respect, this argument is completely ridiculous and should not be brought into any rational discussion on housing. Its the flipside of the silly argument SpaceX is presenting.

There should be some law that disqualifies anyone who brings up the Tulip or Ponzi arguments when it comes to property. I propose we call it Zachary's Law.

Mr Smith, freedom of speech or there abouts on this site. You should take your "law" and move to China

You haven't heard of Godwin's Law or Poe's Law? These are laws of nature like Newton's First Law of Motion.

It is more a scientific discovery than an authoritarian edict. Today I have solved Global Warming and discovered a new law - I really am on a roll.

Moving Poe's Law violation. Step out of the car.

Don't mention 'tulips' or 'ponzi' to real estate agents like Zachary. It makes their prey jumpy.

The tulips are being sold to China.

Bad Robot needs a reboot.... no need for name calling on this forum.

If you look at history, you will see the highest debt/GDP ratio in the us was in 1935, 6yrs after the crash. Reason being, GDP fell off a cliff.

So at 162% how high could that go if same thing occurs again.

Interesting articles I saw on the net last night highlights real income in UK is 9% lower than 2008. That's a lost decade. And the us is similar.

China's debt has trebled since 2007. Zombie state firms.

As for Japan, well aren't they at QE23 or QE24?

Aussie - big deficits there. 47bill this financial year?

What does all this say about our major trading partners and our potential for an export led expansion which has so often saved us in the past.

Low yeilds worldwide is causing NZD overvaluation. And our OCR is one of the highest of advanced economies.

But wait buy buy buy! Lol...housing is a one way bet. Umm no it isn't.

I think today the ratio's are worse than 1935, despite the high gear, strong, robust, 9 year old recovery.

I agree with Bad robot and qual guy. You have to look at the big picture. When has the world economy been this bad? There are very big risks out there. Why has the Dow Jones bounced back so quickly this year? Any good reason other than Fed policy announcements? It's scary stuff. I don't think globalisation is here to stay, why is Trump so popular. The cracks are appearing in the big lie that is the world economy.

Yup, credit is growing 3x faster than GDP (ability to pay), good times!

Found this interesting article, about our BFF buying up large worldwide.

Govt Aided yaun exchange blips. May bug you...certainly bugs me.

Taint houses,(for a change)... but there are other machinations, going forward.

Read on.

Hundreds of dignitaries foreign and domestic have stayed at the storied Waldorf Astoria Hotel in New York. Herbert Hoover stayed there for three decades. Ike stayed there from 1967 to 1969, but he was afraid of heights and insisted to be housed on the seventh floor.

But in 2015, Barack Obama snubbed the Waldorf after it was purchased the year before for almost $2 billion by Chinese insurance giant Anbang. Obama feared the rooms would be bugged by the Chinese government.

It was probably a valid concern, but likely a little too late. The Soviets had probably bugged it a long time ago!

Last week, Anbang made an offer to U.S. hotelier Starwood for $14 billion - in cash - to buy the chain. Another suitor, Marriott, is vying to acquire Starwood as well, and made an offer consisting of shares and cash. Marriott's first bid was at the $65 level, an attractive prospect for shareholders. Yet Anbang's latest bid would force Marriott to pay more than $84 per share. At that level, the benefits of synergy from the acquisition will have all but evaporated for Marriott and its shareholders.

So, if Anbang wins, does that mean all of Starwood's hotels will be wired with listening devices? Check your future reservations now... before you suffer a cancellation penalty!

What should be more troubling - though not from a xenophobic point of view - is that the Chinese are buying up everything. And when I say Chinese, I mean the Chinese government.

Make no mistake: There are no "private" Chinese companies based in China.

It makes perfect sense for China to offload its currency through an acquisition such as this one, given the communist's country's effort to devalue the yuan. The yuan is pegged to the U.S. dollar and has been one of the strongest currencies during the recent global "currency war to the bottom."

That strength is hurting Chinese manufacturing and exports. Thus, it has no choice but to devalue to remain competitive on the global stage. And, while its economy is showing signs of organic growth, it's nothing compared to the trillion-dollar export industry which drives the Middle Kingdom's economy.

So, ask yourself this: If you were about to devalue your currency, wouldn't it make sense to go on a spending spree while your currency was still strong?

After all, the printing press is still working, and whether you pay a 1% or 10% premium to what others are willing to pay, the argument is moot if you're planning on a weaker currency in the months and years ahead.

It's a brilliant strategy with only one obstacle: The U.S. government is not fond of foreign governments buying up U.S. assets. Recall the 80s when the U.S. government was loathe to sell assets to private Japanese companies... but it did anyway.

China presents a different type of problem. It's a global superpower and that means something. And China's not exactly the most cooperative or progressive with its policies.

The U.S. may cave again - we need the cash, even if it is in yuan.

But it will be difficult for the Chinese to have their way. This year to date, the Chinese have made 102 deals globally, amounting to $81.6 billion. That's up from 72 deals worth a paltry $11 billion last year. Among the deals that are of note are ChemChina's $48 billion deal for seed and pesticides group Syngenta, Haier's bid for heavy equipment maker Terex Corp., HNA's $6 billion bid for Ingram Micro and - perhaps the most eye-opening - the yet-to-be-approved deal by Chongqing for the Chicago Stock Exchange.

The last time we saw this much foreign interest in such a short period of time was when the Japanese were buying up U.S. trophy assets in the 80s, culminating with the purchase of the Pebble Beach Golf Course, a buy that marked a top in real estate prices at the time just as the Nikkei was embarking on its massive downward spiral, the effects of which are still being felt in Japan today, some 25 years later...

China is not buying up U.S. assets because its economy or markets are at their headiest levels. Rather, it is buying up U.S. assets because its currency is at heady levels. Therefore the country is doing what any savvy investor would do - selling its most liquid asset, the yuan, while it's still high, knowing full well that it's heading lower in the coming months.

The antithesis being that in China the government owns the companies while in the US the companies own the government. So it's called soft power or something, the US does exactly this and is quite protective of it's position. How much of the world is owned or operated by US companies? It all bugs me, as much as our sychophantic government whores itself to any and all, lets seee a referendum on that!

What are you worried about? These are all signs of our "rockstar economy" that John Key loves so much that he sells NZ. Of course being a rockstar economy it needs to eat, drink and smoke too much. Our economy might as well shoot TVs and wreck hotel rooms.

If you invest in Auckland property there's never been a better time to borrow many to pay for addictive drugs, what could possibly go wrong.

Can someone shed some lights on the true meaning of "median multiples, house price-to-income multiple" as outlined in http://www.interest.co.nz/property/house-price-income-multiples ? E.g. currently in North Shore the multiple is 9.69, does it mean 9.69 of gross or net income?

Lower down on that page the term is defined. It's the median before tax income of one male aged 30-34 + 50% of a median before tax income of a female aged 30-34 + any working for families entitlement. I'm guessing the ultimate source is the Stats NZ household income surveys.

For sure - go crazy with the debt. Just make sure that you can either sell down whatever you buy when the time comes, or service the debt in the future when banks are no longer allowed to make up their own money out of thin air and hike the interest rates to attract cash deposits. Bear in mind that during that time, a lot of investors will be looking to do the same so depending on what you've invested in, over-supply may cause you to sell for less than you were hoping for. And remember what Uncle Warren said - "Be Fearful When Others Are Greedy and Greedy When Others Are Fearful".

No inflation or deflation it's a great time to reduce debt levels, and the low interest rates help with that. It seems strange when being level-headed with personal/family finances is contrarian.

Not just property, has anyone noticed the standard of cars driving about on our roads in Auckland these days ? The Toyota Corolla has been replaced by anything from Audi !!!! everything is now modern and people must be borrowing against their houses big time and getting new cars.

Older imported low end Audi's (A4's) and BMW (3 series) is not much more than a newer Corolla. Sometimes that Corolla will cost more.

Until you have to repair them that is....

I respect David Hargreaves opinion and have arranged for him to speak to our group in a small provincial city several times. However he is an intellectual not a practical hands on property investor. But then looking at the above comments I wonder how many full time investors actually think about these things. Having a political point of view does not put money in anyone's pocket. Sure I have borrowed plenty in recent months but I have not used that money to buy houses. But I have used houses as my security because for me that is the cheapest money. Over the last few weeks my and everyone else's share market investments have for the first time in 12 months been performing well. I have not borrowed to buy shares did think about selling down the portfolio to reduce the mortgages. However they are performing so well I think I will wait. So what I am saying is there is more to the story of mortgages than a simple buying and selling of properties. Unlike my property portfolio my infrequent (non trader) buying and selling is totally tax free and not subject to political comments by all and sundry. I and all the other share investors can pretty well do what ever we feel like. We take the risks and we take the losses on the chin and profits for our pleasure.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.