ANZ economists say housing market activity is cooling because of the new LVR restrictions and they believe this slow down is different to ones seen after previous LVR moves.

In the bank's weekly Market Focus the economists say that history would suggest the current cooling will be temporary given a shortage of supply, and the market will "fire up again" in around six months.

"However, this time looks different as banks are actively attempting to lean against excesses, the interest rate cycle (both domestically and offshore) is maturing, valuations are even more stretched, additional macro-prudential measures are being worked on, and market forces (i.e. more intra-regional migration) will assist. This should temper the market from firing again until the supply side catches up," they say.

The economists say that banks are now "actively rationing credit" and "leaning against activity at the top of the cycle".

"In an environment where credit growth is still far outpacing deposits, the former needs to slow and the latter rise," the economists say.

"Lending criteria have been tightened beyond explicit prudential requirements. That’s a) responding to higher economic risks at the top of the cycle; b) trying to bring some balance back to the economy (i.e. stop the current account deficit blowing out); c) responding to shifting regulatory requirements (i.e. deposit and liquidity requirements); and d) common sense; excessive credit can be a key driver of booms and busts.

"The danger is that curtailed credit restrains housing supply though, so there is no free lunch."

The economists stress they are not saying they are expecting a correction "or anything like that".

"Valuations are certainly stretched and risks have increased, but outright weakness is hard to envisage when net migration flows sit at records, supply is responding only slowly, interest rates remain historically low and the underlying economy is still performing well (although there is a chicken and egg argument of course). 'Cooling' is quite different to 'cool'.

"But we do feel that it is now less likely that the market bursts away again in a few months’ time as it has done before."

As well as the 'credit rationing', the economists cite several other reasons for why things are different this time.

The interest rates cycle is maturing

"We no longer see any further OCR cuts after a “final” cut next month, and that cut is already effectively incorporated into current mortgage rates. But it is the international scene that is far more important to watch, where the realisation of higher headline inflation, a shifting focus to fiscal policy, and more hesitancy from some central banks to ease further are seeing yields increase. A spike higher in rates looks unlikely; the world is still far too fragile. But the boost that ongoing interest rate falls have provided the market looks to be behind us," the economists say

Valuations are even more stretched than they were

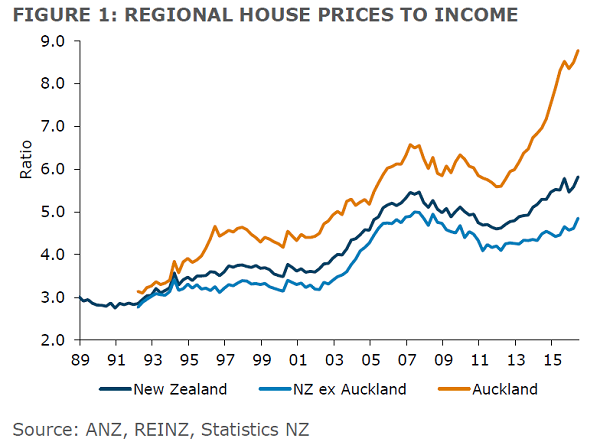

"In Auckland, we estimate that the ratio of house prices to income is close to 9 times. When the initial LVR restrictions were introduced, it was 6½ times. Nationwide, the ratio is now close to 6, when it was less than 5 in 2013. Over 50% of average disposable incomes are now needed to service the debt required to buy the median house in Auckland with a 20% deposit. Despite historically low interest rates, that is on par with 2007."

More macro-prudential measures are coming

"The RBNZ has made it clear that it wishes to introduce, or at least have the ability to introduce, debt-to-income restrictions. Discussions with the Government are ongoing, but we’d expect to get more information in the RBNZ’s Financial Stability Report next month."

Other policymakers are also stepping up their efforts

"Residency visa requirements have been tightened and increased funding for social housing has been mooted. From a political perspective, the pendulum is swinging more actively towards restraining demand and boosting supply. While there is still massive inflow potential for immigration given the global scene and political fracas, signs of improvement in the Australian economy could see departures pick up."

Market forces are assisting

"While there is a shortage in Auckland, there is a surfeit of houses in some regions. A migration “push” (Auckland is too expensive), and pull (the regions are cheaper) is playing out. Adjustment factors such as the average number of people per house is rising as valuations force changes. That means the kids staying longer at home too."

The economists say this combination is "no panacea" amidst a housing shortage in Auckland (and Wellington and the Bay of Plenty), "but these factors should temper the market’s natural push to keep rising, and effectively buy time for the supply side to adjust and respond – which it will, over time".

34 Comments

In an environment where credit growth is still far outpacing deposits, the former needs to slow and the latter rise," the economists say.

Which part of these official declarations do "the economists" not understand?

Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money.

The reality of how money is created today differs from the description found in some economics textbooks:

Rather than banks receiving deposits when households save and then lending them out, bank lending creates deposits. Read more

.....the banking system does not simply transfer real resources, more or less efficiently, from one sector to another; it generates (nominal) purchasing power. Deposits are not endowments that precede loan formation; it is loans that create deposits. Money is not a “friction” but a necessary ingredient that improves over barter. And while the generation of purchasing power acts as oil for the economic machine, it can, in the process, open the door to instability, when combined with some of the previous elements. Working with better representations of monetary economies should help cast further light on the aggregate and sectoral distortions that arise in the real economy when credit creation becomes unanchored, poorly pinned down by loose perceptions of value and risks. Borio Page 17 of 38

“In a barter economy, there can rarely be investment without prior saving. However, in a world where a private bank’s liabilities are widely accepted as a medium of exchange, banks can and do create both credit and money. They do this by making loans, or purchasing some other asset, and simply writing up both sides of their balance sheet.” Read more

After creating their liabilities banks are loathe to reward the owners (depositors) for the risks undertaken.

Westpac reduced its 1 month term deposit by -15 bps to 0.35%. SBS Bank reduced its headline 3.60% 18 month term deposit by -15 bps to 3.45%. Read More

There should be a law prohibiting such unethical wealth transfer, given there is no free market. It's truly a one way corporate discount to OCR undertaking ranged against the saving citizens charged with the responsibility of underwriting the whole structure.

Well said. No more dropping the OCR so that banks can increase interest yield

Unbelievable!, only now are the banks:

a) responding to economic risks ;

b) trying to bring some balance back to the economy;

c) ) responding to "shifting" regulatory requirements

d) applying common sense;

Only now are they recognising "excessive credit can be a key driver of booms and busts"!

It shows yet again we cannot trust the bank internal risk management, their risk models, and their director attestations. Firm lending regulation (DTI and LVR limits) must be put in place and maintained.

The economists stress they are not saying they are expecting a correction "or anything like that".......

Tightening of credit is the first sign. Banks love to keep their margins so when the interest rates keep going up you'll know the pressure is on while the RBNZ fumbles around pretending they have more control than what they really do. I believe the next year will get rather interesting.

Is it just me or is today the day of stating the obvious? First the finance minister finally admits immigration may be 'structurally higher' and now the banks are admitting the many things others have alluded to over the last twelve months. Wonders never cease.

Puff, puff , puff .......... the horrible reality is that all asset prices ( shares , property and other asset classes) have increased to the point there is no underlying value , no yield, and little return.

Commodities on the other hand , are almost all in a slump

Banks have sense enough to know that asset prices have reached a zenith , and lending into this market is dangerous

The asset price rises are likely a result of QE , but not exclusively , and there is a seriuos correction coming , which will start with stock markets , the collapse of a few banks ( who can guess maybe even a Chinese Bank?) followed by a serious house -price adjustment ( and NZ may be spared due to migrants keeping demand up ).

Properties have yield in excess of bank deposits currently. A serious correction would mean rich people will get 15%+ yields on their property - why should they get that? Or do you think average rent will drop to half its current price? Why should it?

"A serious correction would mean rich people will get 15%+ yields on their property"

I assume you mean people buying at the bottom of the next cycle? Where do you get 15% from?

If there was a housing correction do you think there would continue to be high immigration? Surely that tap would be turned off. Then rents would go through the floor.

FYI at today's prices yields are barely ahead and in some places behind bank deposits. Of course an individual investor’s yield will depend on the time and price that they bought at etc. etc.

Where does 15% come from? Even a 50% drop in Auckland house prices would see gross yields at present average rent levels of around 7-8%. Yes, that's gross not net. The bad news is that for house prices to drop that far we would likely be part of a serious global recession. As result rents would likely plummet resulting in a large drop in asset values without a significant increase in yield.

And before you mention immigration it doesn't matter how many people are chasing accommodation if they haven't got dollars in their pocket they won't be able to pay.

Thanks Tom,

You've outlined the paradox I and a lot of people are living with right now. I need a massive drop in house prices to be able to buy but such a drop will likely trash the economy. In a weak economic environment if I'm still lucky enough to have a job, who would lend me the money to buy a house???

A 15% yield would require a house price fall of about 70%. Unless investor loans are currently only at 30% LVR or so then the majority of investors will have negative equity if that happens

Some people have talked about such drops in value. I did grab it out of thin air though. Hyperbole? I would still think increased yields will favour those with wealth.

The wealthy in NZ are likely to have a large stake in the housing market, so the high yields would just be the silver lining of the cloud that is one of their main asset classes plummeting by 70%.

It'd be great for people not in the market but with cash elsewhere, but that's likely to be a small number of people. The main beneficiaries would be first house buyers, I'd have thought (once the dust had settled)

The next crisis will be a stock, bond and real estate crash. Global debt 30% higher than 2008. Holding real stuff as opposed to a promise is a no brainier. As always only a few see what's coming. The IMF and BIS have issued their warnings and the elites of the financial world are preparing by holding more cash and are now in gold. This time around however there isn't the money to bail out the banks so that is why we have 'bail in' legislation where depositors are seen as unsecured creditors and will take a haircut. The derivatives which have been described as 'weapons of mass destruction' held by banks ensure that they won't survive the next crisis. People need to educate themselves on the big picture as their future is dictated by global events.

And before the gold bashers come out in full force the financial elites now advocating a weighting to gold in portfolio's include Alan Greenspan ( former chairman Federal Reserve 87-06), Mervyn King ( former governor Bank of England), Ron Paul (3 times candidate USA presidency) and titans of finance Stanley Druckenmiller, David Einhorn, Paul Singer, George Soros, John Paulson, Marc Faber, Jim Rogers etc, etc, etc.

Hedge funds have proven to be the worst investments over the past decade, averaging just 0.7% per year and underperforming every benchmark. The only thing they have excelled in is extracting fees from clients.

http://www.etf.com/Swedroe%3A%20Hedge%20Funds%20Miss%20Mark?nopaging=1

Nothing wrong with gold, but lots wrong with people that don't really understand the nature of money. Your enthusiasm is commendable, but is simply proving to be the ranting of the freshly converted. There are some very smart people on this site so parroting dogma that can be read elsewhere won't win you any friends among them. But I warned you of this already& you misread it as gold bashing. Slow down& take a breather eh! The flaws in the system are well known here, all you are doing is preaching to the converted. Don't clog the forum with posts of little substance, bring some original thought& analysis.

Ooooo - aren't you so clever and important. If I comment, I'll bloody comment what I want and when I want, Mr Self-Appointed Moderator

And of course the central banks have been net buyers of gold since 2010, with China, Russia, India and many others dramatically increasing gold purchases since 2008. The present stagflationary environment mirrors the 70's when gold 'went up' many many times in all currencies. Year to date for example gold is up 46% in sterling. It is protection against depreciating currencies. Does anyone dispute that since 2010 we have been in a currency war with currencies being forced to devalue against each other. I could go on but do the study and it becomes obvious that the financial world is changing at an accelerating rate and gold as a part of your portfolio is your financial insurance.

Preaching to the converted - I don't ever see gold mentioned as an alternative investment on this site. I doubt one in a hundred knows anything about it!

Firstly, it's difficult to class a lump of metal that doesn't pay you anything an 'investment'. It's just buying a commodity and hoping it appreciates.

Secondly, I know more people buying gold than shares, because even people without much financial knowledge see it as something tangible, whereas investing in shares is terrifying to most people because of all the scare stories. People are aware gold is worth more than it used to be, and struggle to disentangle this from background inflation.

5000 years of history tells us gold is money and not just a lump of metal. It has been forced out of our currency system by the 'new' fractional reserve system based purely on paper money. No paper money system has lasted and paper money can't store wealth. Otherwise buried money would be treasure as opposed to gold. Keep printing the paper money and it becomes worth less. Quite simple really. The central banks see it as money and hold it as a reserve assett. Why can't you see it I wonder.

5000 years of propaganda and ignorance tells us gold is money.

There, fixed it for ya. It is just a lump of metal. Nothing can store "wealth", when our concept of wealth is an illusion.

To "Real Money": Fact: all money has been "fiat", i.e. including paper, for thousands of years. If you invested fully in gold back in the 60s/70s then you'd be looking silly right now compared with property and stock market investors. You can ramble on about leverage and debt, but the fact is that those who rode the inflationary/debt cycle were winners, not those who held on to gold for 30yrs and went backwards. This cycle will turn and debt will be shunned in future again...it's all part of the cycle.

Ok, agreed, we're only talking about 40-50yrs of a person's life, no big deal, but it's a long time to wait for another cycle. Gold is just another asset class and it will have its day just like any other asset class. If you become emotionally invested in it like some rabid Hillary or Trump supporter then you need to take a breather and get back to reality.

To all of our economists and genius forecasters, the IMF chart in this link should give you pause for thought...

http://www.icis.com/blogs/chemicals-and-the-economy/2016/10/budgeting-g…

"Fertility rates. These have been below the replacement level of 2.1 babies/woman for the past 45 years". So much for the infinite growth on a finite planet meme.

1) That's not world fertility rate.

2) We have a massive immigration (so don't worry, we can still work towards overpopulating NZ).

Where is the infinite growth coming from? Take me from "barely higher" to infinite with your greenie magic. "The global average fertility rate is 2.5. This means that global fertility is barely higher than the global replacement fertility. The replacement fertility is the total fertility rate at which the population size stays constant. If there were no mortality in the female population until the end of the childbearing years, the replacement fertility would be exactly 2. With the current level of mortality the global replace fertility is 2.3 – the narrow gap between the current global fertility and the global replacement rate means that theincrease of the world population is due to the increasing length of life and population momentum.1"

Projections of population growth

By 2050, the bulk of the world's population growth will take place in Africa: of the additional 2.4 billion people projected between 2015 and 2050, 1.3 billion will be added in Africa, 0.9 billion in Asia and only 0.2 billion in the rest of the world. Africa's share of global population is projected to grow from 16% in 2015 to 25% in 2050 and 39% by 2100, while the share of Asia will fall from 60% in 2015 to 54% in 2050 and 44% in 2100.[3]:3 The strong growth of the African population will happen regardless of the rate of decrease of fertility, because of the exceptional proportion of young people already living today. For example, the UN projects that the population of Nigeria will surpass that of the United States by 2050.[3]:4 The population of the more developed regions is slated to remain mostly unchanged, at 1.2 billion, as international migrations from high-growth regions compensate the fertility deficit of richer countries.

World population August 2016 , it was estimated at 7.4 billion. The United Nations estimates it will further increase to 11.2 billion in the year 2100.

Just remember the household debt to income ratios are calculated for all households.

When calculated for just those with debt ie excluding the roughly 30% without debt,

then the ratios are roughly 50% greater.

Try and make that work with interest rates back to normal, whatever that maybe, but as a guide US 30 year rates long run are very close to 7% meaning our mortgage rates would be maybe 8%.

Nice of the banks to now start restraining credit when the horse has bolted and mortgage growth still in excess of 9%.

Hard to see this ending well I fear.

Yes it would be very interesting indeed to see DTI ratio in action. Depending on the ratio introduced, I wonder how much mortgage growth will slow as a result? Could be quite significant. And a decent hit to GDP and irate bank shareholders.

Interest rates will not go over 5.5 per cent for fixed rates for a long time if at all.

People that continually hope that interest rates are going to shoot up are delusional.

If the do go above this it means that inflation is out of control.

It is a different world and priced accordingly.

The U.S. Rates for 30 years fixed has been early 3s for awhile now so mid 4s is about right here.

Some countries you can borrow on mortgages at 0.5 per cent.

No one in NZ will borrow if rates were 7. Per cent or so as they wouldn't be able to service the mortgage.

NZ can't afford to,have their financial system collapse

A few years ago when the economists were tipping rates to go up including Bernard Hickey etc. I felt that they should be dropping, and yes that is what they they did.

Get used to the current rates as status quo.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.