By Zoe Wallis & Jeremy Couchman*

Key points:

- The New Zealand housing market has cooled convincingly over the past year.

- In our view, this slowdown has been caused by a confluence of factors including LVR restrictions, pre (and post) election uncertainty, affordability constraints and tighter credit conditions.

- However, there remains a gap between supply and demand that is unlikely to be corrected in the near-term.

- The outlook for the housing market over the year ahead remains uncertain. We still expect to see a small rebound in activity over the next six months, but price gains are likely to be much more limited.

The New Zealand housing market has undoubtedly cooled over the past year. House sales are 26% lower across the country compared with a year ago and house price appreciation has stalled to essentially flat over the last year.

So is the housing boom turning to a bust or is this just a temporary bump in the road? In this note we take a look at some of the key drivers of NZ’s housing market and the implications for the outlook.

Why have things slowed down?

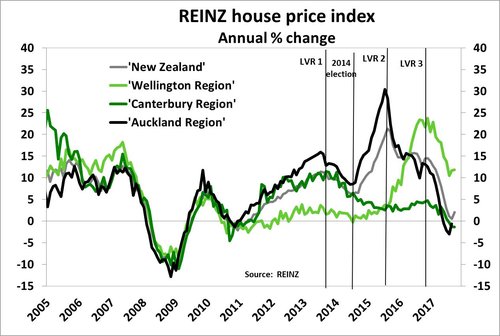

T here are many forces currently at play in the NZ housing market that we believe are driving the current slowdown. First of all, the RBNZ tightened loan-to-value ratio (LVR) restrictions for property investment toward the end of 2016 (see ‘LVR 3’ on chart) which appears to have had a significant impact on property investment.

here are many forces currently at play in the NZ housing market that we believe are driving the current slowdown. First of all, the RBNZ tightened loan-to-value ratio (LVR) restrictions for property investment toward the end of 2016 (see ‘LVR 3’ on chart) which appears to have had a significant impact on property investment.

The new rules require essentially a 40% deposit when buying a residential property that isn’t owner-occupied. For most owner-occupier purchases, a 20% deposit requirement has been in place since late 2013 (‘LVR 1’ on chart).

Second, uncertainty ahead of the 2017 general election has seen a more cautious approach from property buyers – particularly the investor segment.

This was especially evident when there was still significant talk of introducing a capital gains tax, but the general policy uncertainty also caused people to hold off major buying decisions – similar to the pattern we saw prior to the 2014 election.

Labour has proposed increasing the bright-line test from two to five years – meaning that those who buy and sell an investment property within five years will have to pay tax on the capital gains over that time. In addition, Labour and NZ First both want to ban foreigners from purchasing NZ land and property.

More significantly in our view, is the prospect of the new government scrapping the ability for investors to offset losses on their rental properties against income tax - which has been an attractive feature for many investors. Now that we have a new government, we are watching closely for the specifics around implementation of proposed housing policies. If implemented in full, these policies are likely to reduce demand from property investors further in the year ahead but on the flip-side may provide opportunities for more owner-occupiers/first-home buyers to get into the market.

Third, affordability constraints – particularly in Auckland where the median house price to income ratio is running at over 9x – means that saving a deposit and paying the mortgage are a higher hurdle for the average household. New Zealand’s overall price-to-income ratio is around 6x, but that masks a wide range of variability - from a ratio of 12.7x in Queenstown, down to a much more affordable 2.6x in Whanganui.

Measures of affordability are now just starting to improve as house price growth has moderated and wholesale interest rates have shifted marginally lower in recent months. But rising mortgage rates in coming years could put additional pressure on affordability, particularly if house prices continue to rise – increasing the dollar value of debt taken on by the average buyer.

Finally, in response to a more restrictive funding environment, we have seen housing credit growth reined in over the last year. Mostly, these changes have been tweaks around the edges, but there is an increased degree of caution present around residential property-secured lending in the market at present. The growth in housing-related lending has pulled back from a cycle-peak of 9.1% year-on-year (yoy) in August 2016, down to a pace of 6.9% yoy in August 2017. This is the slowest growth rate seen since late 2015, although it remains above the post-GFC average growth rate of around 5% yoy.

Underlying demand remains while supply lags behind

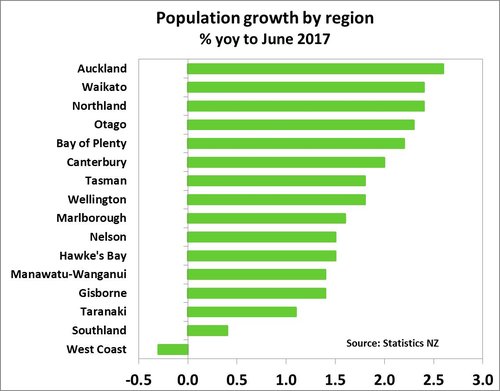

The latest figures from Statistics NZ show that New Zealand’s population increased by 2.1% over the year to June 2017. In Auckland the growth rate was higher at 2.6% yoy - or equivalent to an additional 42,700 people.

The latest figures from Statistics NZ show that New Zealand’s population increased by 2.1% over the year to June 2017. In Auckland the growth rate was higher at 2.6% yoy - or equivalent to an additional 42,700 people.

Assuming an average of 2.7 people per household (the average household size measured in the 2013 consensus) implies that around 15,800 additional houses needed to have been built in Auckland over the past year to keep pace with population growth.

In reality, just over 10,000 dwellings were consented with an estimated 7,000-8,000 of those actually getting completed. So in Auckland alone there was a shortfall in residential dwellings of about 8,000 houses last year.

Additionally, new building consents have been lagging behind population growth in our largest city for quite some time. Estimates suggest that there is a pre-existing shortage of somewhere between 30,000-40,000 dwellings in Auckland.

Across the rest of the country we have seen strong population growth in areas such as the upper North Island and Otago (see chart), but almost every region has seen its population expand over the past year.

Across the rest of the country we have seen strong population growth in areas such as the upper North Island and Otago (see chart), but almost every region has seen its population expand over the past year.

The newly formed Labour-NZ First coalition government is looking to both increase the supply of housing and also cut net migration numbers – which theoretically should help bring supply and demand in the market back into balance.

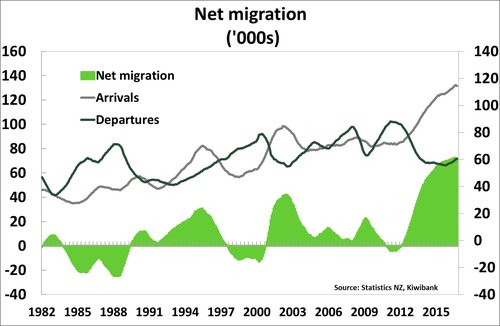

Population growth has in large part been driven by record-high net migration levels in the past few years. Net migration has contributed over 2/3rds of the increase in population – with the other 1/3rd due to natural population increase (more births than deaths).

Under the new government, the Labour party’s policy of cutting net migration by 20,000-30,000 per year (from the current annual rate of 71,000) appears to be the preferred policy – rather than NZ First’s much more restrictive stance of cutting net migration to an annual rate of 10,000.

The reduction in numbers is expected to largely be achieved through tightening up student visas and the number of unskilled workers coming in.

However, our view is that net migration will still remain solid and still elevated by historical standards. Other major governments have tightened up migration policy in the past year, including:

However, our view is that net migration will still remain solid and still elevated by historical standards. Other major governments have tightened up migration policy in the past year, including:

Australia has increased the stringency of English language tests and citizenship test. Migrants who become permanent residents will now have to wait four years before applying for citizenship – versus one year previously.

In addition, New Zealanders in Australia are facing tighter rules around applying for citizenship and access to student loan assistance.

- In the UK, immigration changes have tightened up salary requirements for Tier 2 visas and levied an Immigration Skills Charge for skilled migrants on employers.

These are two of the most common destinations for New Zealanders to move to and hence, with tighter international migration rules and reduced rights while overseas, we expect many New Zealanders to continue to stay put – lowering departure levels.

At the same time, for those who can still obtain a visa, New Zealand remains an attractive place to live and work – especially given some of the geo-political tensions in other parts of the globe.

Hence, despite the anticipated changes in migration policy from the NZ government, we expect net migration to remain solid at a pace of 40,000 to 50,000 in the next couple of years. Net migration gains of this magnitude would still require an additional 15,000+ homes to be built in NZ each year just to compensate for population growth.

Building sector operating at full steam

However, we don’t expect to see any sort of quick resolution on supply within the next few years. The new Labour-led government has pledged to build 10,000 new houses a year on average across NZ, with 5,000 of them in Auckland. But the construction industry already appears to be operating at full capacity, with most construction firms reporting a lack of skilled labour as the biggest constraint to increasing production.

The NZ Building and Construction Industry Training Organisation (BCITO) estimates that New Zealand “needs 65,000 new people over the next five years to meet new growth and replace people who leave” in the construction industry.

The NZ Building and Construction Industry Training Organisation (BCITO) estimates that New Zealand “needs 65,000 new people over the next five years to meet new growth and replace people who leave” in the construction industry.

At present, it is estimated that there are about 11,000 apprentices in training – a record number but still not enough to fill the gap. At the same time, a rough estimate of skilled work visas issued in the 2016/17 June year, show that approximately 6,000 migrants entered NZ on a construction-industry related skilled work visa.

Labour’s ‘Dole for Apprenticeships’ programme is estimated to increase the number of people in training by 4,000 – although not necessarily entirely in construction and building.

In addition, Labour is allowing building firms to hire a skilled tradesperson on a three-year work visa (without having to meet labour market tests) if they take on a local apprentice for each overseas worker they hire – although this will be limited to between 1,000-1,500 at any one time.

Adding these pieces of data together points toward clear skill shortages in the industry, but reports suggest that there is also a distinct lack of unskilled workers, which is likely to also be a limiting factor in ramping up building work.

Hence, if the government really wants to increase the overall amount of houses getting built each year, they will need to figure out a way to meet these skill shortages. Already the cost of building work has increased significantly in the last few years, with the cost of building new housing up 5.4% yoy, due to the rising cost of labour and materials.

If we are to increase supply without a significant increase in the number of available construction workers, we will need to get savvier about how we build. For example, a significant shift toward more prefabricated and denser housing could help speed up the building process, reduce the amount of workers required, and in some instances lower the cost of building materials. However, until New Zealanders give up their dream of an individually built house on a quarter-acre section, we expect that the increase in housing supply will continue to lag behind population growth for at least another couple of years.

Affordability issues here to stay

With the housing supply and demand imbalance likely to persist, we don’t expect to see a significant correction in house prices in the near future. However, as mentioned above, affordability constraints are also having an impact on New Zealanders’ ability to get a foot on the property ladder. While this has been a noteworthy constraint in Auckland in recent years, it is increasingly becoming an issue around the rest of the country as well.

Unless prices actually start to decline, it will take some time for affordability constraints to ease as incomes rise. We expect to see wage growth pick up from its lacklustre pace of 1.6% yoy in coming years as the labour market continues to tighten.

However, the RBNZ’s tightening of LVR restrictions at the end of 2016 has seen the share of mortgage lending to property investors decline from almost 40% of all lending, down to about 23% currently (see chart).

However, the RBNZ’s tightening of LVR restrictions at the end of 2016 has seen the share of mortgage lending to property investors decline from almost 40% of all lending, down to about 23% currently (see chart).

While credit growth has also shrunk over this time, this has allowed more first home buyers and other households who are trading up, to purchase property.

The other factor that is important to consider is the outlook for mortgage rates in coming years. The Official Cash Rate (OCR) is currently at a record low and that has kept mortgage interest rates near historically low levels. But in the past year, mortgage rates have started to slowly creep higher.

We expect to see the RBNZ hike the OCR from the end of 2018 which will put upward pressure on mortgage rates as well. In addition, global central banks are also moving toward tighter monetary policy settings, which put further upward pressure on local rates here.

LVR restrictions a permanent feature?

The RBNZ’s LVR rule changes over the last four years have had a varying impact on the housing market. However, these rules were always supposed to be ‘temporary’ with the idea that LVR restrictions can be used to smooth the peaks and the troughs of a housing market cycle.

So this begs the question, at what point will the RBNZ feel comfortable removing LVR restrictions? We don’t expect to see the outright removal of this policy, but if prices decline significantly then we suspect the RBNZ will look at loosening LVR settings.

For example, the Bank could increase the percentage of mortgage lending to those with less than a 20% deposit up from currently allowing 10% of all lending, to 15% and then 20% over time. This would still keep the amount of leverage in the housing market lower than that seen prior to the introduction of the rules - when about 30% of some banks’ lending was to those with less than a 20% deposit. A similar approach could be taken for the investor segment of the market.

What does this mean for the economy as a whole?

While house prices have been rising since the GFC, so too have household debt levels as people have leveraged up at low interest rates in order to get into the market. As a result the household debt-to-income ratio in NZ has increased to 169% - a record high.

While house prices have been rising since the GFC, so too have household debt levels as people have leveraged up at low interest rates in order to get into the market. As a result the household debt-to-income ratio in NZ has increased to 169% - a record high.

With household debt so elevated, increasing mortgage rates will quickly have an impact on household consumption.

Overall this feeds into our view that interest rates hikes in New Zealand will be gradual and we don’t expect to see mortgage rates get anywhere near back to the levels we saw pre-GFC - partly because of elevated debt levels in the economy.

Studies show that, in the short-term, a rise in household debt tends to boost economic growth at the time – as we have experienced in the last few years.

However, over the subsequent three to five years, growth is slower than it otherwise would have been.

In addition, if the housing market were to experience a sharp correction, then this would have a negative flow-on effect to the broader economy as people rein in spending.

While our central view is for house prices to experience a small rebound in the near term and then flat line for a few years, there remains significant policy uncertainty in the wake of a new government.

--------------------------------

*Zoe Wallis is Kiwibank's chief economist and Jeremy Couchman is Kiwibank's senior economist. This article first ran here.

52 Comments

I suspect that a very large number of ma and pa investors who bought on interest only and no yield have all been looking to use this to convert their taxable income into equity for their retirement. I could accept it if it was limited to new builds only (thus not transferable) as it would force the pace on increasing density, and would eliminate speculation from domestic money on existing housing stock.

Has the policy for stopping tax loss offset on personal income been announced yet...?

Noooo, you cant do that!!! then PAYE earners wont get 50% off their tax rate due to the income loss but still be able to cash out capital gain tax free!!!

where have all the Chinese gone ?

I mean all the spruikers made all these excuses and now all silent

Of course sentiment about Auckland property market has changed Anyone with cash is waiting and watching

The lower $NZ will play quite nicely when comes time to buy

trouble is with all the migrants who wants to anymore except those trapped in NZ

Hi, yes, it was stated on the labor policy website but was short on detail. Little had stated it would be phased out over 5 years and in the labor budget that appears to be costed in as a 5 year process.

Averageman, yes, phasing out of this has been announced/confirmed to occur over 5 years. The phasing out will allow 80% of the amount to be deducted in year one, followed by 60% etc. Clear details about this were quite hidden in labour policy announcements always couched in terms of 'removing tax loopholes for speculators'.

However if the same 'loophole' is not closed for companies (common ownership companies can write of losses from one company against another) it's just going to hurt PAYE earners - the middle class not the rich.

The only positive thing anyone can still point to for the housing market is tired argument of supply and demand. But if it was down to supply and demand, why have prices declined for much of the past 9-12 months?

Looking ahead, those supply and demand constraints are also going to be addressed by the new government. Lower immigrating, no foreign buyers, and 100k affordable new homes.

I would suggest the likely path of price of house prices continues to be to the downside. In Auckland we could easily see another 20-30% decline, on top of the roughly 10% we have seen already from the peak.

Hi user123,

You ask, "....why have prices declined for much of the past 9-12 months?"

In fact, they haven't. Relative to the gain in prices through 2014-16, the decline in the last 9-12 months has been very small.

Further, in areas such as inner city Auckland and Wellington, prices have actually held firm or continued to rise - albeit at a slower pace. If you want a good 3/4 brm house in these areas, you will likely have to pay more than in November 2016.

Well located (central) property in Wellington and Auckland is likely to remain a very good investment. There is huge pent up demand for it. People are prepared to pay a sizeable premium for convenience and avoid transport/travel hassles.

There is' huge pent up demand', yet sales are at historical lows. Trade me listings up. Can toothypointy, describe what 'huge pent up demand ' actually is.

Hello Cowpat (my bovine friend),

The situation with the inner city suburbs of both Auckland and Wellington is that there have been very few houses coming on the market for much of the last 12 months. House owners in these areas are reluctant to sell. (Ask anyone trying to buy a house in those areas. They'll tell you it's slim pickings.)

There are plenty of people who yearn to live in the inner city suburbs, so the demand there remains strong. People like living close to the Wellington/Auckland CBD's for convenience, lifestyle etc etc - and many more people/families would do so if they had the ways and means.

So, despite a softer housing market generally, prices in these areas have not weakened and in many cases have continued to rise.

With Auckland's population increasing by more than 800 people each week, it's hard to see the pressure coming off inner city houses. No doubt they will become increasingly sought-after.

Tothepoint, would it be reasonable to suggest , (and going on current Trade me listings alone ), that it is the Wellington region/city, that is better placed than Auckland when looking purely at housing stock for sale/ per capita.

Cowpat is my neighbour. We're both going down in Remuera.

Double -G has 3 years passed. I have just walked past my first Bentayga, unsure if someone has recently sold or arrived. On a further note although we have a PO box , letter box becoming fair game for agent advertising. Have advised elderly mother that her home should now be placed on market, as she walked back from same PO box without car. Which agent should we choose, and how low can be get the commission to go. Welcome back , it seems just like yesterday.

I just love chartist/ statisticians!

Get ready to polish off the old comparative chestnut, "Compared to 5 years ago, in 2012.....". No wait! Compared to 2007, 10 years ago...... etc....If in doubt, change the parameters....(My overly used 'train going over a hill' analogy.)

Looks like your cherry picking here. ie saying no average regional price drops are happening because some few "krack" areas show no drops.

On the other hand with fewer "low income/quality" immigrants coming in the areas they would occupy will see the biggest drops...so the Q is what is the NET change? still looks flat or negative overall...

Due to artificial market intervention. Removing it now will most likely cause the house prices to accelerate even harder than before. Just imagining it is making me feel like I'm having a good time bareback with someone very unsanitary (meaning not good). If you weren't able to purchase a house within the last 2~3 years and if the house prices decline 20~30% I think picking up a bargain will be the least of your worries.

I think lower immigration is a good idea. Most students come from 3rd world countries with no money and most of them aren't in a position to buy outright (there are exceptions) so I'm thinking culling student immigration numbers aren't going to have massive effect.

Here you go user123; This article explains very accurately why there's been a huge drop off in property sales since January this year. The short answer is China pulled the plug on capital outflows and all that lovely overseas money is long gone, never to return.

Better Dwelling: China’s Massive International Real Estate Buying Spree Is Officially Dead

https://betterdwelling.com/chinas-massive-international-real-estate-buy…

CJ099, can you please point out precisely where, I quote you:

"This article explains very accurately why there's been a huge drop off in property sales since January this year. The short answer is China pulled the plug on capital outflows"

My eyesight must be quite bad cause I can't find it. Thanks, I know you wouldn't just make this up

@Yvil, It's quite clearly states in this article that sales have declined -26% across NZ. The reason for posting the other link is to show what prompted such a big decline, It's not just LVR rate increases.

@user123 supply and demand is a term that refers to a price response curve. It does not refer to specifically to the amount of immediate buying demand but rather a distribution of demand based on the variable 'price'. As price falls demand rises, that's the general rule, a downward sopping demand curve. In this particular case 'demand' refers in large part to a population of willing but unable buyers. As price falls more of them will be able to buy and it would follow that this acts as a cushion to falling prices.

The article address your points:

It says claiming youl build 100K homes does not by itself get them built and notes skilled labor shortages and then looks at labors specific policies to address it and concludes that the stated policies are insufficient. It notes that immigration, though lowered, will remain high, concluding that the supply/demand imbalance will not be solved any time soon.

user123, you say; "the new government ..will supply 100k new homes". Sounds great, truly...

The problem I have with the analysis is that the assumption that the ratio of people per household will stay at 2.7 even when rentals/prices increase. This is what is used to point to the supply/demand imbalance. What I believe has happened is that with small rental increases we have seen a change in the patterns of occupation, and some groups such as student immigrants are probably opting for a lot of people per unit (elastic demand in economic terminology). A shift from 2.7 people per household to 2.9 would reduce the demand for houses by about 40,000 houses. However, the continual discussion of supply demand imbalance has fueled price increases based on a speculative bubble - where prices have leapt far beyond rental increases. I think you take the prospect of capital gains out of the mix and the interest in property plummets.

Using the 2.7 ratio is somewhat misleading ,to state a shortage or underbuild, as at the last census regionally Auckland was 2.98., a number which in itself required an increase in the number per household, from the previous census because of dynamics of flow. Bottom line , there could always be a housing shortage if one desires. I believe Samoa is wonderful at this time of year.

Auckland received 50% of the population and 30% of the consents its pretty simple, The climbing number of people per household in Auckland is a response to a shortage of housing.

Seeing as no one seems to actually know why prices have stopped rising in Auckland, it might be worth thinking about other possible paths.

What if NZ booms?

1 We have full employment, apparently.

2 We have very low interest rates by historic standards.

3 We have a construction boom (all available hands employed).

4 The currency is going down.

5 World growth is high, at least on the basis of PMI data, as far as I can tell.

6 We have just elected a spend-more government.

7 We have just elected a "gut the RBNZ" government (okay I might be exagerating here, but that's my take on it)

What if, unexpectedly, the export sector starts making good profits? They will then try to poach workers by offering higher wages. Hey, ho, wage inflation. Public sector strikes. Cries of "No-one saw it coming". 1970s redux.

Meanwhile, over in Aussie, they are starting to have a field day as the worldwide stockpile of mineral resources is used up. They have a gas shortage of all things. Hey,ho, raw materials inflation. Eventually petrol prices double (or treble...). Cries of outrage and "No-one saw it coming". 1970s redux.

Indeed the $NZ is declining nicely to the level JohnKey was hoping for maybe

I would not worry because a lower $NZ will be good for exports & foreign investment

NZ is a nice safe haven and will remain

Someday Auckland might even advance to constructing a rapid transit system like long deceased Mayor Robbie always wanted

What a treat that would be

@ex socialist Supply and demand did not drive the majority of the price change. The lions share of the gain has been a result of interest rate changes and expectations around future interest rates. Supply and demand imbalances added a bit of froth.

As to increasing the number of people per household that is simply a demand spring been coiled, it does not remove demand. Long term the fundamental trend for number of people per household is ever lower. The main cause is increasing relative wealth and increasing average age of the population.

Your compassion of price change to rent change is flawed, it is change is cost vs change in rent that drives investment.

Well firstly do we agree that increased immigration did not cause the 'lions share' of the price growth?

I think the issue of low interest rates is overstated - people were only prepared to borrow because they saw extensive capital gains. A 4.5% mortgage doesn't make sense if you are only getting 2-3% return (after expenses) on the investment. What we established was a ponzi scheme that was based on an expectation of further capital gains which has run it course.

The number of people per household is a function of price. You are right that it will uncoil as prices decline - but the evidence from rentals is that it will take a lot of decline before people opt to change living options.

You are right that the long term average people per household will drop - and the demand for houses in a static population is commonly an increase of 1% per year. However, that demand is for a different type of house (apartments town houses) which are in a lower proportion of the building stock than other cities. Auckland with its relatively large number of stand-alone houses can absorb more people than (say) Sydney.

Immigration and the housing shortage are one in the same problem and it adds froth but is not the main driver of the price change.

The issue of low interest rates is simply mathematics. There are two forces of particular note: the first is if you halve the interest rate you double the relative return and this will cause prices to double over 'some period of time', independently of any natural growth etc. The second is that home owners actually need to repay the principle which dampens the effect.

So the investor market and the home owner market have different sensitivities to interest rate changes. The weighting of the impact is relative to the proportion of the various types of property owner.

If you take Aucklands last peak in 2007 median prices were about $465,000. Assuming 65% of homes are owner occupied, taking mort rates in 2007 of about 9%, and rates today of about 5% you get a weighted interest rate implied change in prices of 1.6x. Then add inflation as a wage proxy and it spits out 21.4%. These factors combined give you an implied housing peak of $903,000 in 2017 which is why affordability today is approx equal to affordability in 2007 and why median prices peaked at $905,000.

The implication is that scarcity is causing the market to bounce along the upper limit of affordability.

So Rasputin Peters has already had an effect on the market ?

His anti-immigration stance will spook both local and foreign investors , and this should have a dampening effect on asset prices , hopefully

Peters dislikes immigrants in general and Asians in particular .......... remember his outburst when he said :

"Two Wongs dont make a white "?

The Asian community will not be so willing to just throw money around if they think they are not welcome

"Two Wongs don't make a white "...come on, that was kind of funny!

Jeeepers - five years ago David Chaston would have sand-boxed you for that

Didn't they reply "Aotearoa - The land of the wrong white crowd"?

Funny if you're white... not so funny if you're "Wong"

Not funny to me.

I would describe it as racist and highy offensive.

Simply not acceptable.

What a beautiful week people. How the tides have turned :)

GZ homes selling at RV? https://www.trademe.co.nz/Browse/Listing.aspx?id=1426414413

Will this be the new norm?

Wow sold in 2015 for 1.736 so they are taking a hit already. https://www.trademe.co.nz/property/insights/address/Auckland/Remuera/Or…

Capital gain has vanished for the last 2 years...

Don't look down as you might lose your lunch.

So many dreamers. have a look at this https://www.trademe.co.nz/property/residential-property-for-sale/auctio…

Sold in march 2016 for 760k and asking for 960k now.

They will be lucky to get what they paid last year seeing that capital gain has now gone negative yoy

The reality

Two economists say "the construction industry already appears to be operating at full capacity, with most construction firms reporting a lack of skilled labour as the biggest constraint to increasing production"

How and what do you have to do to acquire labouring skills - like, you are working under the direction of a supervisor - what do they want - someone who you don't have to supervise - get off the grass - there is enough trouble with cowboy-builders now without getting into unsupervised builders labourers

Their could be a large number of ex Fletchers "shovel leaners" come available in the labouring sector shortly

I think they're forgetting to mention that the two big main facts that continue to contribute to the strong decline in Auckland property sales are. 1) Chinese top end buyers are gone. 2) The Ozzy banks stopped lending to overseas speculative Investors that includes Kiwi investors due to the absents of top end foreign buyers to drive speculative price increases. Basically the party is over.

Any sensible Investor would wait at least a year for the market to bottom out to more affordable levels, which it will since China will be keeping a tight reign on capital flight.

CJ099, Hold on, just a few comments above you said:

"This article explains very accurately why there's been a huge drop off in property sales since January this year. The short answer is China pulled the plug on capital outflows"

and now:

"I think they're forgetting to mention that the two big main facts that continue to contribute to the strong decline in Auckland property sales are. 1) Chinese top end buyers are gone"

So does the article "explain accurately" or "forget to mention" ?

I think you're just trying to confuse matters Yvil. We all know that Speculative Investors massively contribute to distorted the property market particularly for Auckland along with foreign Buyers. Hence why Auckland's property prices are 9 x over income ratios which is not sustainable.

If you walk in to any Australian owned bank and ask for an mortgage for a property investment you will need a huge deposit and you can't just use your property portfolio.

Hardly any difference in price reduction so far, however would not be expecting the market to take off anytime soon. The market is at still and it will stay that way for awhile.

Sellers expectations. Just have to look at the Auction Clearance rates at the moment.

Building sector operating at full steam.

Yeah, nah. The building sector is at full capacity building the low density, sprawling far and wide, McMansion houses that Phil Goff forces down Auckland's collective throat by his policy of over pricing land supply. But those McMansions are labour intensive and the industry could easily produce 50% more homes with higher density production, all that needs to happen is for Phil Goff to stop jacking up land costs.

If Jacinda can convince Phil Goff to stop being utterly useless. If Jacinda can open up land supply to Auckland, then yes we can build more very quickly.

Absolutely right. A 19th century carpenter would have no trouble fitting into todays construction methods: they would be utterly familiar even though tools and materials had come along some.

My previous rant applies: copied in full to save y'all from clicking a link: http://waymad.blogspot.co.nz/2017/09/prefab-impediments.html

Just imagine the reaction of the current playaz to an announcement like This (thought experiment alert!)

"We are prefabricating a Hoosing Factory offshore. It will be highly automated, needing only a few top-flight technicians to keep it running. It will arrive onshore in December and will commence operations in February. The houses produced from this factory:

- will use materials proven overseas but new to NZ,

- will be manufactured to sub-millimetre tolerances,

- will be built under cover,

- will be assembled in 2-3 days on site by an experienced crew using battery-operated tools.

The factory is expected to have a throughput of 20 houses per day, and will operate 20 hours per day for 360 days of the year.

- Maintenance crews will be flown in for a 5-day upgrade and maintenance window.

- Unit costs for the houses thus produced are expected to be in the region of $800/square.

- All houses will be serial-numbered and will come with a 20-year guarantee of weathertightness."

The litmus test? That 19th century builder should be utterly confounded.......and that's why we don't need 'Builders' to build houses.

Affordability issues here to stay

Maybe.

Nope, houses could become affordable in Auckland within 3-5 years if Jacinda opens up land supply to Auckland.

Yep, Phil "the A-hole" Goff plans to sprawl out Auckland over every corner of the region to make housing continually unaffordable.

We stand at the cusp. Which policy setting will triumph? Will it be the Labour Party policy or the Labour Party policy? What is the Labour Party policy?

my guess is overseas buyers who won't be able to buy existing homes in NZ will now go to Melbourne (may be Sydney) for new properties. On average, 2-3br apartments in Melbourne is cheaper than Auckland.. more opportunities and higher ranking universities

Regarding housing supply: Given the Labour parties commitment to affordable housing, and will probably be the policy they are judged by most frequently, it looks like they will need to find an incentive system that makes it economically advantageous for councils to permit new dwellings at a very high rate and a way to attract major players to housing development to build estates.

However this will not be easy, there is a very good reason the previous government spent a decade trying to ignore this issue or kicking it down the road. Genuine progress and change are difficult and create net winner and loser situations.

...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.