ANZ economists are seeing a "heightened chance" of an economic growth wobble and have lowered their near-term GDP forecasts. They see continuing softness in the housing market and possible impacts from that through slower consumer spending patterns.

In their weekly Market Focus publication the economists say that while they retain a broadly constructive view of the medium-term growth picture, "we have turned more circumspect near term".

This has been reflected by the economists cutting their forecasts of growth in the already completed (but the official figures have not yet been released) September quarter from 0.7% to just 0.3%, while they now see growth of 0.5% in the December quarter, down from a previous 0.7% forecast. However, the economists have raised their forecasts for the second and third quarters of next year to 0.9% from 0.8% previously.

The economists stress that the "wobble" they see for growth is not expected to turn into something longer-lasting, "but it certainly marks us out as less upbeat than the likes of the Treasury and RBNZ".

"Above-trend growth is hard to achieve when the most cyclical part of the economy (housing) looks set to remain soft. That has obvious implications for both the outlook for tax revenue and monetary policy, although the picture is complicated by inflation risks that are shifting higher."

Last week the Reserve Bank of New Zealand released its latest Monetary Policy Statement containing updated economic forecasts. The RBNZ's forecasting GDP growth of 0.7% for the September 2017 quarter and a bumper 0.9% for December - both forecasts now much higher than the ANZ is predicting.

The ANZ economists say there appear to be two main areas where their view differs from that of the RBNZ and Treasury:

"1. We see the soft housing market as likely to have more of a negative influence on consumption. Even if the relationship between house prices and consumption growth is not as strong as it once was, we still expect there to be some negative seepage – we are arguably seeing that already in softer spending data. We acknowledge that the outlook for household income growth still looks reasonable. That is important. However, we can envisage a scenario where at a time when the asset side of the balance sheet is looking a little shaky, that households will look to lift precautionary savings (i.e. not spend the full income windfall). Additionally, history has taught us that at the very least, it is difficult for the economy to grow above trend when the most cyclical part of the economy is soft.

"2. We see a higher chance of private sector activity being crowded out by the public sector boost, particularly in the construction sector. Simply adding new public spending to growth forecasts is too simple by half, especially at a time when a number of sectors are already dealing with capacity pressures (and migration restrictions have the potential to accentuate that). Yes the likes of the KiwiBuild program aims to circumvent one constraint that the sector has been grappling with – access to capital – given that it puts the Government’s balance sheet to work. However, the key issues surrounding capacity and labour resourcing remain."

The ANZ economists say a "number of indicators for Q3 activity" have looked "soggy".

"The heavy traffic component of our Truckometer contracted 1.4% q/q in Q3 – the weakest quarterly growth since Q3 2012, though weather may have played a part.

"Both milk production and livestock slaughtering fell over the quarter. Compared with Q2, visitor arrivals are down 3% as the impact of key sporting events unwinds. While total paid hours rose 0.8% q/q in Q3, growth was softer for some of the services sectors where we use paid hours as an indicator. And core electronic card spending saw its weakest quarterly growth over a September quarter since 2012 (with October figures pretty mediocre too), providing a serious hint that housing market weakness is spilling over."

The economists say there are "broader risks" too.

'Taken a hit'

"Business sentiment has obviously taken a hit and anecdotes on the housing market have remained weak post-election.

"The latter is hardly surprising given some of the more interventionist measures being proposed. We are certainly keeping a close watch on market listings.

"They are low across the country right now, but if they start to increase, perhaps as investors look to exit, then the risk profile for prices would be skewed lower. Net migrant inflows have already started to soften and indicators on construction have been a little ho-hum as the sector struggles with capacity, costs and capital pressures.

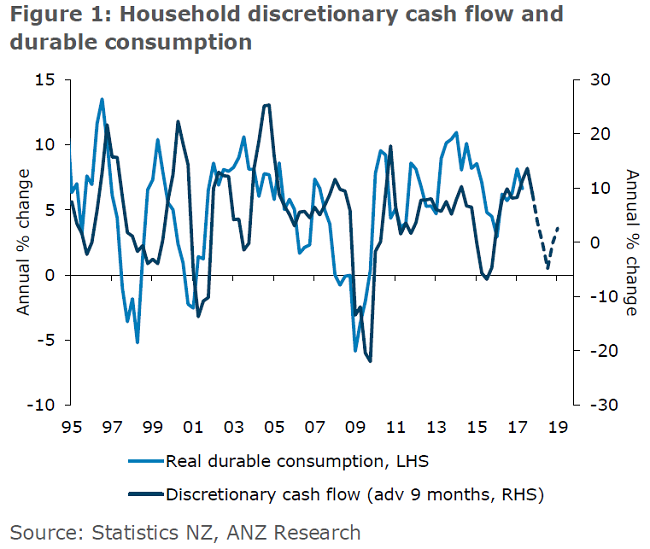

"Additionally, we are also picking up that bigger-ticket spending (car sales especially) have been sharply weaker of late, which again hints at housing market spill-overs. Weaker spending growth would certainly not be inconsistent with the signal provided by the likes of our estimate of household discretionary cash flow."

The economists believe housing market weakness is set to persist, and hence so too the risks of broader spill-overs to the rest of the economy.

"For all that though, we are not forecasting large outright falls in house prices (that would require a lift in forced sales in our view, which we don’t expect)."

Positives for the economy

The economists do point to a number of upcoming positives for the economy, however.

One thing they outline is their expectation that the "biggest headwinds" from the credit cycle are arguably behind us.

"Over the past 12 months or so, banks have restrained credit and competed more aggressively for domestic deposits as they have attempted to close a funding gap.

"Looking at the quarterly change in household lending and deposits as a proxy, that ‘gap’ has closed a great deal. While we are not expecting the credit flood-gates to open by any means (things like the RBNZ’s review of bank capital are still lingering in the background), as a cyclical driver, credit dynamics should turn more neutral."

In other likelly positives for the economy, they see "alternative growth drivers" emerging domestically.

"Fiscal stimulus is the obvious #1 candidate, and some of the numbers at face value look large. In 2018/19 alone, the new Government is proposing spending an additional $3.5bn (which doesn’t include new capital spending or additional initiatives from the coalition agreements).

Spending impact

"All else equal, things like the proposed families package will arguably have a bigger spending impact given that it will put additional money in the pockets of those with a higher propensity to consume.

"So for now we are happy to retain a broadly positive medium-term expectation, with growth returning to more-or-less trend rates.

"Notwithstanding the near-term risks, we forecast annual growth up towards 3% by the end of 2018, and averaging 2½-3% over the next couple of years."

18 Comments

ANZ are one of the better, if not the best, economic commentators out there. A few points:

- I agree with ANZ that RBNZ's growth forecasts are too bullish

- I also agree housing market weakness will flow into wider economic weakness

- I disagree the families package will have a significant effect. Extra assistance is going to middle income families, however I would respectfully suggest that it won't result in much extra spending, given how much many middle income families are struggling pay package to pay package. It will provide a bit of relief, but I doubt a large consumer impact.

- I also think we'll need 2 years before Labour's house building programme kicks in properly, too

People who struggle pay check to pay check provide the biggest bang for buck when you give them a benefit.

Hmmm maybe, maybe not.

Depends

A lot of people will try and pay down loans etc a bit quicker

Or just be in a situation where the money doesn't run out 2 days before pay day

Sure there will some consumer spending benefit, but minor and on food basics much more than anything else I suspect

At least they're communicating that asset "price" appreciation is associated to consumer spending. Their biggest information gap is the quantitative impact. In the case of Australia, asset prices and h'hold budget pressures have contributed to businesses such as Aldi take market share across higher income demographic profiles outside their target shopper. Of course, I'm pretty sure that there is something behind the positive correlation between volume of new car sales and house price appreciation in NZ.

Bloody rate of growth is utterly unsustainable, long may this last so we have to find another way to prosper.

Cheap money has been the driver of asset price explosion, and has facilitated borrowing against the revalued assets .

The Banks of course have loaded onto the bandwagon with reckless abandon

At best its dangerous to borrow against an unrealized gains, which could reverse at any time .

At worst it could lead to a insolvency if the debt becomes unsustainable

Way cool!

I see excitement coming from some economists! :)

It does beg the question of what "over the moon" means for the economists come next year...

Don't mention economists and excitement in the same breath. Caused a big stoush in the comments here last time it was done.

My god, what have I done?

Rich Dad Poor Dad, Robert Kiyosaki talks about the imminent market crash.

https://www.youtube.com/watch?v=PNjtNSzdOBY&t=327s

It's not hard to imagine the deflationary aspect of the next slump. More jobs (service related) are dependant on ever increasing house prices and attached ATM's. Take that away and we are left to export our way back to health - scary thought. After the 2008 GFC, some foreign banks charged interest on cash deposits in an effort to get them to spend it - a risky move given that people could have stashed it under the floorboards. Each global crisis since the 80s has ushered in even cheaper and easier access to money. On a global scale, what new tools and solutions are in place to support recovery after the next bust?

Yes the deflationary aspects are a huge issue. The world economy will struggle to get back off the canvas - Debt has been masking the true cost of production for all commodities , so wiping debt will bring an ugly reality. What comes next is anyone's guess but the old rules will be off the table.

This spells it out

https://medium.com/@End_of_More/our-culture-cannot-evolve-a621d6a4aa96

"As long as hydrocarbon fuels were available in cheap excess, everyone was prosperous, A gallon of gasoline delivers the same work output as 50 men working a 10 hour day; that meant we all had an army of personal slaves so we could enjoy our democracy.

Now energy resources are no longer cheap or so abundant, and as a result, living standards are falling, and everyone can see they are falling without knowing why. We can no longer afford our ‘gasoline slaves’, despite promises of hundreds of years worth of coal and oil being available.

This is the big lie. Without hydrocarbons, we have no future prosperity. There are no “alternatives”. Cultural evolution is impossible without the leisure to carry it out. Technology is not going to deliver an amazing new energy resource. Without abundant energy availability, the nations of the American landmass cannot hold together as a single entity. Nor can any of the other ‘economic systems’ of the world. They too are destined to break apart."

ham n eggs,

I enjoy your posts. You describe our future in apocalyptic terms-no hydrocarbons,mass poverty and presumably,social unrest on a global scale. With 4 young grandchildren, that's a pretty scary scenario to contemplate,but how accurate is it?

I have a book written in 2004, The End of Oil,by Paul Roberts. It was highly persuasive,but predated the growth of the fracking industry. Of course,the time will come when oil and gas are clearly and irreversibly in decline,but that point keeps getting put back and neither you nor I know when that tipping-point will come. Meanwhile,solar power and wind generation,EVs are rapidly emerging to help reduce the pressure on hydrocarbons.

glad you enjoy them! Yes i also have kids so its not a nice scenario to ponder ... solar and wind (and EV's if you like) are just an add on to existing electricity generation /infrastructure.. they are only a small piece of the total energy puzzle (which underwrites ALL debt). Re timing / reality this is worth a read.

https://surplusenergyeconomics.wordpress.com/2017/11/13/112-will-things…

"What we’ve been witnessing since the turn of the century, though, has been an increase in the energy cost of energy (ECoE), combined with emerging constraints on the quantity of accessible energy. This process makes the continued growth in aggregate money and credit dangerous, because we are creating claims that the real economy will not be able to meet."

and as to the conclusion, analysts are now picking Oil prices to head up sooner than expected...

http://www.artberman.com/u-s-supply-oil-ending/

http://www.nzherald.co.nz/world/news/article.cfm?c_id=2&objectid=119437…

I well remember the 1992 warning letter which was pushed to the back pages of the MSM because everyone was facinated by the OJ Simpson trial.

pfffft ... scientists. What would they know.

... now back to those economist tea leaves...

John,

You may not have noticed,but that book-though I would call it pulp fiction-was written 20 years ago.

"the "biggest headwinds" from the credit cycle are arguably behind us."

LOL. Only an economist could think that.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.