ANZ economists say consumer spending hasn't been as strong as it was during previous economic growth cycles - and they point to high house prices and associated high debt levels as key reasons.

In their weekly Market Focus publication the economists say since 2014, consumption growth has been more subdued than could have been the case.

"...And we think this will continue to be a theme going forward. We expect households will strengthen their savings buffers and that consumption growth will moderate from here. Income growth is expected to remain solid, with conditions in place for a pick-up in real wage growth."

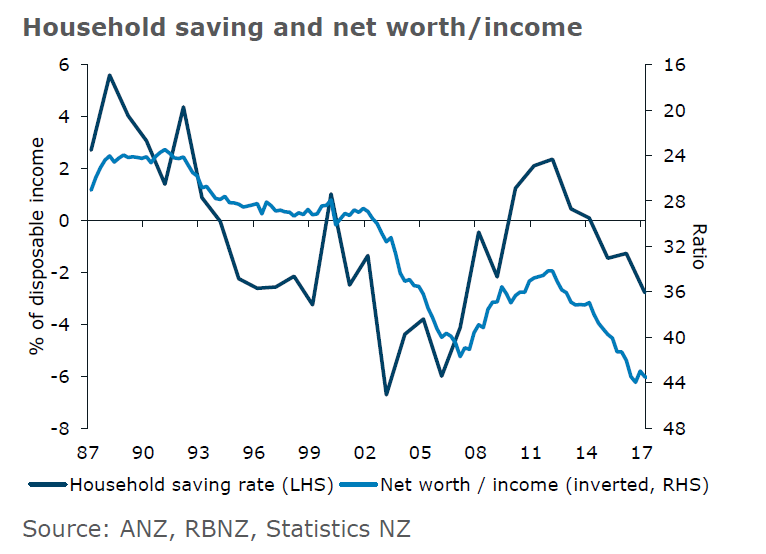

The economists say that over the current cycle, net worth has increased relative to incomes (inverted in the chart below), driven by strength in the housing market. But the saving rate has not deteriorated as much as capital gains suggest it could have.

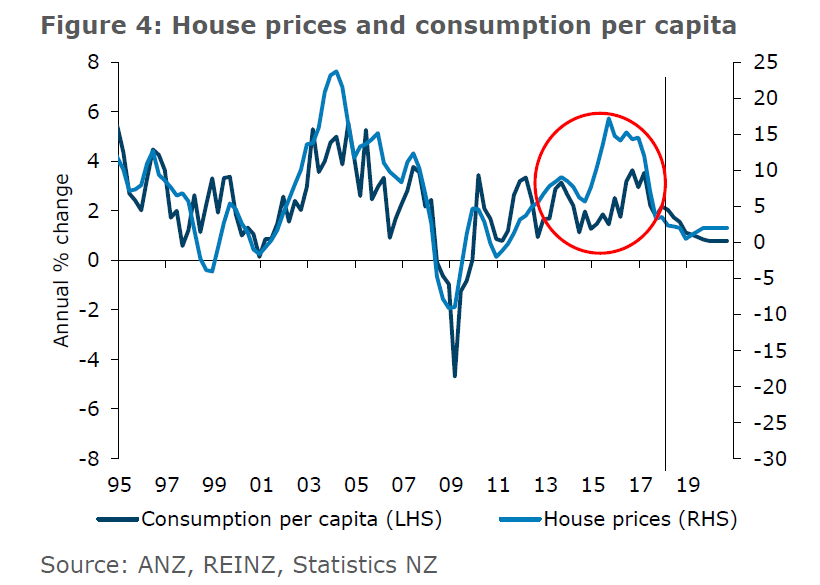

The economists say that a simple chart of house price inflation versus consumption per capita (see below) tells the same story. "Consumption did pick up when the housing market strengthened, but not to the extent it might have. All up, it’s a picture of a more cautious household sector than the housing market cycle would have normally implied," they say.

"The fact is: households have good reason to be saving more.

"House prices and household debt levels are already very high.

"For those who already own houses, average debt burdens are significant – household debt is currently 92% of annual GDP and 167% of household disposable incomes."

The economists say the recent cooling in the housing market will have made that debt feel a lot more “real” for a number of households.

"...And we expect consumption will be dampened as a result – for all that debt serviceability remains around historically average levels.

"For the median-priced house bought with a 20% deposit, mortgage repayments are 33% of average household income. And this would rise quickly if interest rates increased.

"While we don’t think that will happen any time soon, it is likely to be on the cards eventually – and households will be mindful of that."

The economists point out that would-be home buyers need to save a lot.

"Houses are unaffordable for many, at six times the average national income, and closer to nine times in Auckland.

"This means that to purchase the median house with an 80% loan-to-value ratio one would need $110,000 in savings – 120% of the average annual household income.

"In Auckland, one would be looking at 170% of annual household income – no small sum."

Credit availability has also been a constraint on some would-be home buyers’ ability to take on debt, they say.

"Again, this reflects high levels of house prices and existing debt levels, with restrictions on high loan-to-value ratio mortgages playing a role and the Reserve Bank treading carefully when it comes to loosening these restrictions.

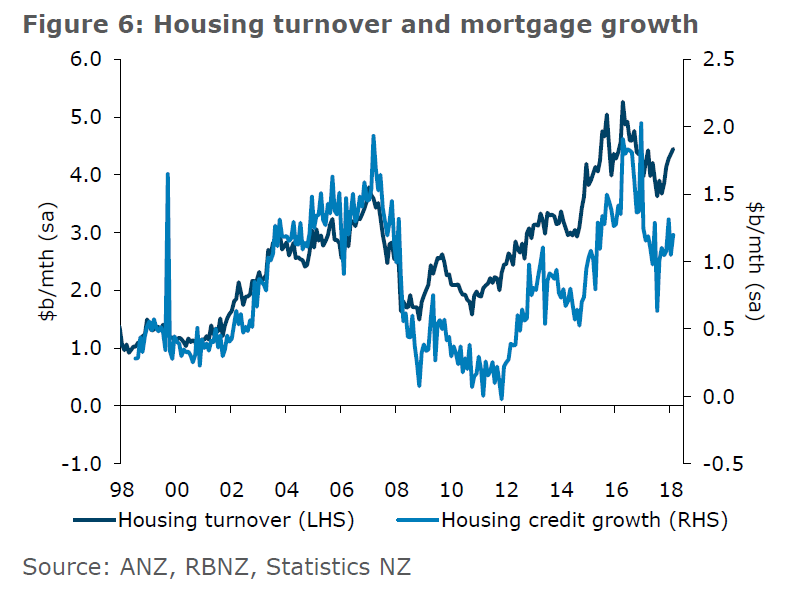

"Indeed, as a consequence of these constraints, new debt associated with housing market turnover has been lower this cycle.

"More recently, banks have also worked hard to close their funding gap, with reduced credit availability contributing to recent cooling in the housing market.

"While we think this dampening influence has stabilised, credit availability will remain a constraint for some."

So, in light of these constraints and a cooling housing market, the ANZ economists believe that households will need to improve their savings buffers.

"We expect both house price inflation and consumption growth will moderate from here. In fact, we are already hearing from our discussions around the country that retailers and businesses in discretionary services are experiencing softer demand. But while consumption looks set to slow, we think income growth will remain solid – implying the household saving rate will increase.

"Incomes are expected to continue growing around their current, moderate pace – supported by robust, but slowing, GDP growth and a pick-up in real wages. Conditions are in place for real wage growth to improve. The labour market is tight and expected to tighten further. Firms say it is difficult to find skilled labour and these capacity pressures should eventually lead to higher wage inflation."

49 Comments

"The economists say the recent cooling in the housing market will have made that debt feel a lot more “real” for a number of households."

Now that homeowners can see that their house values could also drop, suddenly they are not as keen to borrow against the mortgage and use their houses as ATMs. Less consumer spending means less money coming into local businesses. A shift in sentiment is all it takes and we'll see house prices go back down to normal levels.

note: I'm not describing a crash, but rather a more healthy 3 to 5 times income (or say even 5 to 7) rather than the current 9 to 12 in Auckland

Now that homeowners can see that their house values could also drop, suddenly they are not as keen to borrow against the mortgage and use their houses as ATMs. Less consumer spending means less money coming into local businesses. A shift in sentiment is all it takes and we'll see house prices go back down to normal levels.

This is actually a different phenomenon than what is being talked about here (but relevant in its own scope). What they're basically trying to 'softly, softly' suggest here is that the people are tapped out.

What they don't refer to is how bubbles, particularly housing, become a self-generating organism that feeds off itself. They actually have the potential to become the be-all-and-end-all of the economy.

Dont blink ........... Kiwis are far too quick to embark on spending sprees , I suspect that the real cause is because Banks are actually making it harder to borrow against inflated property values .

The ability to expand property portfolios is much harder now that speculators equity is no longer expanding like it once was. People are spending less as there are soaring rates, insurance and maintenance costs to contend with. It's more about paying of the actual debt through principle and interest payments rather than through disposal. Also, now that present Government policy is no longer conducive for amatuer landlording, this speculative ponzi is no longer self sustaining. The wealth factor is slowly subsiding, making way for the worry factor. This massive amount of equity was accumulated in a dangerously short time. I cannot see how it could be easily banked if there is a rush for the exits. If there were a trigger, "poof", it could easily disappear as fast as it came. Then that exposes the true value and consequences of excessive debt.......

Only now, when it is too late, do we understand - high house prices make you paper wealthy but they reduce disposable income. Now that we have a few hundred billion in debt, there is no money left over to buy the things we need and so we all have to live like paupers. Our future growth will reflect this as we squirrel away every penny to pay for that meth house Tony Alexander suggested we buy in order to start at the bottom of the property ladder.

But at least the banks made record profits right?

They did. Someone always makes money from other people’s misery. Banks are like camp followers trailing an army trading for sex and looting corpses.

That was a joke by the way. Banks perform an essential function. The problem is they face systemic incentives to destroy the system. Hence the need for regulation and monitoring which they fight. That is why comments from ANZ CEO a while back were interesting.

I am afraid that the property price will stay at this level.

The pillars that support NZ's high property price:

1. Baby boomers' wealth

2. Migrants and migrants' deep pocket

3. AKL city council's urban restriction

4. Fletcher buildings monopoly position on building materiel

5. Shortage on builders

No party in NZ can chop off these pillars at one go.

Baby boomers die/need to spend their finite wealth in their retirement which will be significantly more expensive than they expect.

Migrants don’t have as deep pockets as is made out in the media.

Auckland city looks like it making big expansions in both green fields and brow fields - look for another big kiwibuild site.

Fletcher - pretty sure that will continue although if they are smart kiwibuild will support other suppliers

The shortage on builders will be addressed by factory building of homes.

Over a period of how long?

Slowly. But baby boomers are dying and downsizing every day. Many of them are still working but as they leave the workforce they will need to tap their housing asset and there are only two ways to do that - debt and sale - and guess what? Debt leads to sale. It might take 20 years, so not a crash, but at some point their impact will no longer be felt and the market will settle at a lower level.

Please check Stats NZ's long term population projection in the next 20 yrs.

Check year 2038 and the projected population ranges from 5.1 million to 6.4 million.

http://nzdotstat.stats.govt.nz/wbos/Index.aspx?DataSetCode=TABLECODE754…

I’m talking about specific baby boomers dying. The baby boomer generation is finite, god isn’t making any more of them.

The biggest driver of property prices is economic sentiments which you have not factored into your argument. Cyclical economic slowdown, similar to the one we saw in 2008, causes businesses to rein back hiring and investment. As a result of household income uncertainty or job insecurity, home owners lose their ability to service debt and list their properties on the market for a quick escape.

Moreover, low savings rate hinders the ability of the household to settle a few mortgage payments while waiting for a good market price. There aren't enough deep-pocketed migrants, construction companies and baby boomers out there who would want to get into the housing market in bad economic times.

"Immigrants will keep the demand high" is the new rationale behind the endless price rise assumption. Remember the pre-GFC "who defaults on their mortgage" rationale?

NZ is indeed a lucky country.

The business cycle used to play a big role when NZ's tie with US (and AUS) was much stronger and NZ's tie with China was much weaker.

Things changed, folks.

A downward business cycle in US/AUS may coincide with a up business cycle from China. And pure physics tells that these two waves cancel each other out.

And now in China, the only biz cycle is up because it still has a huge rooms for developments.

In sum, an unprecedented and ever growing economic tie with China makes economic cycles effective-less in NZ economy.

Why assume the US and Chinese economic cycles may move in opposite directions?

The only reason China could decouple itself from the previous global downturn was the excessive debt their banks and regional governments pumped into its monetary system. Most of this money was diverted towards industries that built up spare capacity which remains unutilised till date. Contrary to your view, many economists believe that the Chinese financial market could be the epicentre of the next global financial crisis (remember 2015 where this almost happened).

U still believe in these many economists who can suddenly forecast a collapse of China when they all failed to see the GFC.

These many economists will never forecast right because they use western economic theory to forecast an unique oriental Middle Kingdom.

The Western power brokers and leaders (across politics, business and academia) fawned all over Japan during its epic bubble. Only a handful could see not all was well. Arguably, China is in a more dire situation than Japan ever was in terms of debt, fiscal management, and transparency.

I presume that you thought USA forcing Japan to appreciate Yen got nothing to do with the lost 10 yrs of Japanese economy.

It's truly a magical kingdom if basic economics do not apply to it (but apparently physics...of finance...do).

The world now has a gold backed currency for trade, The Chinese yuan.

This will erode USA's military backed currency.

I want NZ to ditch US dollar for trade just out of pure morality. And lets bring our troops home and stop supporting their evil!

Some of your pillars are referring to building supply challenges, however there is no shortage of properties for sale in Auckland. Currently over 12500 listings on Trade Me and over 13700 on realestate.co.nz.

When there aren't many buyers around willing to pay the over inflated prices, then there is only one way to sell your property.

As interest rates keep rising in the US, offshore funding costs for the banks will increase causing interest rates to rise here as well regardless of what the OCR is. Also we will see alot of owners come to the end of their interest only loans and get put on to P&I loans creating a little more pressure.

When the squeeze comes on some will suffocate and be forced to exit. If youre one of the 12500 that have had your property on the market for months, what are you gunna do?

The net savings rate being negative looks bad to me especially when combined with declining consumption. Should consumption be dropping off this much when the servicing costs of household debt is still quite low. How concentrated is the consumption and debt?

Interest rates may well not rise....but when you end up paying 6%(or whatever) interest on a laon of $600k on your house now worth $450k...then effectively they will have.

I blame millennials. First they spend all their money on avocados, now they won't spend anything because they want to buy a meth house as their first home... luxury

Avocados are healthier than meth houses

Not according to baby boomers or Tony Alexander.

An interesting perspective is how many high end cellphones or flights to London it costs to buy a house. For example, if it was 200 high end cellphones 20 years ago and now it’s 800, is it any wonder people prioritise cellphones? The cellphone is 1/4 the price relative to houses and offers significantly better functionality. Overseas holidays are similar. By inflating house prices we encourage people not to save and then we complain about the profligacy.

Big Macs is running at about 180,000 macs for a central suburb Auckland house today vs 80,000 macs in 1990. That is a lot of Macs to forgo to buy a house like your parents did.

The deposit requirements alone these days are almost as much as a house cost in 1990. People are expected to save for their deposit today, why couldn’t people in 1990 save for their house? Probably terrible with money.

The deposit requirements alone these days are almost as much as a house cost in 1990. People are expected to save for their deposit today, why couldn’t people in 1990 save for their house? Probably terrible with money.

Back in "dem times", I would have thought that a 20% deposit was a starting point. Correct me if I'm wrong.

In the early 1990's I saved 15% of the house price but it was an affordable new house and paid $87,000 for it. I was still short by 5% of the deposit, therefore it was a sub-prime loan and LMI was required until I had built up the equity enough to put me within the 80% threshold. The loan was also stretched out from the usual 20 year term to 25 years. I did it on a single income and damn near paid it off within the first 10 years. Now it is almost impossible for a single person to buy a house on their own, even if they can manage to sae the deposit and the loan term is 30 years. Crazy!

Wait a sec I thought large amounts of avocado stock were taken out by the weather events and the booming black market in them? Millennials would probably waste their money trying to go organic & grow their own (the cycle has come full circle, except with much higher costs in vege gardening & worse growing conditions due to land ownership & recent weather). Met quite a few millennials trying to bring about another grow your own tea fashion. Pretty common to see them with more than just the green under the lights of the sustainable gardener.

I've read interest forums for a while now and I'm always amazed no one discusses money creation by banks in relation to our housing market. As per the article, consumers are tapped out due to another credit bubble thanks to the banks having the ability to create money through fractional reserve lending. I think we are doomed to go from bubble to bubble all the while feeding inequality in a very negative and unfair way while this is in place.

Am I on my own thinking this is the single biggest factor in our house prices?

I think you're right. Without a never-ending series of bubbles, the global economy seems to be stunted. Regarding the banks role, the crux of the issue is what is the extent of indebtedness that h'holds and businesses can hold before the whole economic system is destabilized. Interesting to note that Japan's h'hold debt was never as great as it is in NZ or Australia, even at the peak of their bubble.

"Without a never-ending series of bubbles, the global economy seems to be stunted." Scary thing that we consider adding to the money in circulation as growth when all it does is devalue the money that currently exists and certain sectors get artificially inflated i.e. housing.

With what you said about the crux of the issue, I think different bubbles can pop at different levels. It just takes a "black swan" event which tips things over the edge.

While black swans can pop a bubble they are by no means the only manner and gradual mechanisms do exist (especially more ideal when an entire generation has it's retirement savings tied into said bubble). However for a living necessity such as secure housing should it be beyond the local residents ability to access it? Unfortunately for many it is but the Government solution to pay private operators more at inflated rates (above even standard pricing in hospitality), seems not only more likely to exacerbate a dependency of both parties on those mechanisms, it also allows the continual inflation of the bubble at the rapid rates. Other mechanisms to slow bubble growth and increase access should be prioritised. When then considering another bubble whose influence that can be extremely detrimental to the locals the growing need for good food production land causing a reduction in food production, and reduction in food for local markets at affordable values. There is a certain point where artificial generated black swans, or bubble pops would be useful, but the measures for controlling such are fickle. Previous examples can go either way, and even current examples are poorly researched on wider effects. Plus NZ really does not like it's citizens that much so I cannot see any effective changes for another generation. But as a bonus this generation gets... not sure, a kiwi over the rest of the world? (Because the health system is nothing to brag about, especially now when most of it is just as inaccessible). What would a generated black swan look like? (e.g. the unexpected and large change such as a full restriction on foreigners buying & owning residential stock as an example would be terrible by itself; sure housing would be available but many would be neck deep in mortgage debt already or expecting large gains as the only feather in the retirement nest.)

loan acceleration is the most negative it's been since the GFC, look see here...

Thanks for the link fat pat. Any idea why the RBNZ discontinued C5 data? The GFC comparison is interesting as well, I would think that the negative growth was due to subprime etc then but what is causing such a similar downtrend now? The million dollar question is how much longer until this causes real issues as we are reliant on new and expanding credit to pay for our current loans (seriously though, I have a deposit and I'm itching to buy a property but holding off)

If I were you I’d wait a couple of years. If people are tapped out without disposable income then how will they cope with rising interest rates and the govts new “rebuilding budget” (ie. higher taxes)? The mortgage stress will grow exponentially and today’s million dollar house will be way cheaper by 2020/2021.

Hey Withay, I think the best time to buy a house was 2009. That probably doesn't help does it. The C5 data hasn't been discontinued. Its all available at the RBNZ stats page https://www.rbnz.govt.nz/statistics/c5 Anyone can download the raw excel data and play with it. Those graphs are just some amateur analytics that I did. Here's the R code with some thoughts in PDF form. It seems to me that if the government does not counter private sector loan deceleration with deficit spending (as cs says below) then a recession could result. Unfortunately they seem hell-bent on running a surplus. Overseas capital flows and immigration rates are wild cards. Time will tell..

I wonder what the banks have in mind to arrest the falling loan growth.

Interesting that consumer loans aren't particularly volatile. It must be a boring industry.

Some wise banker once said that the best money he made was from the business he didn’t do. Why aim for loan growth if the borrowers can’t pay you back in future? Chasing loan growth is a fools game

Wow, thanks for the analysis, very interesting. I think the government will jump in when houses get too negative for their liking, as bad as high house prices are a recession is politically worse. And yes plenty of wild cards as well, I note that immigration hasn’t been turned off yet so that will be interesting. If there is a major drop, my money is on a very large problem overseas (which seems very possible). Locally, I think we will be fine otherwise.

As Steve Keen always says, when private credit growth just stops accelerating (even if it keeps growing), at high levels of pre-existing private debt, it can cause a recession. His Minsky software is very interesting and well worth watching - complex systems modelling, rather than dsge modelling, or whatever the whiz kids call it.

Hi Ludwig, CS. I agree with both of you, frustrating wait though as everything not just housing seems to be in a bubble so really just have to sit on my hands and do nothing for a while. Also, I have the impression the government will try support current prices (LVR's were relaxed slightly start of the year for example) so will be interesting to see how long they can play that game or how aggressively they pursue "stability."

.

The ANZ do a fair job of reading the tea leaves, but the likelihood of a major default event somewhere or other must be pretty high and rising by now. When times are good then the inability to repay loans can be kept hidden, and the default amount rises steadily. As money gets tighter they burst out of the shadows with high profile defaults. Carillion in the UK could be the first of many.

Not sure who might go bust in NZ, but there has to be defaults before too long. Last time it was the finance companies in NZ, the merchant bankers and mortgage bankers in the US and the UK.

Check this out and expand to see the history, it shows wholesale world USD bank rates:

https://fred.stlouisfed.org/series/USD3MTD156N

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.