By David Hargreaves

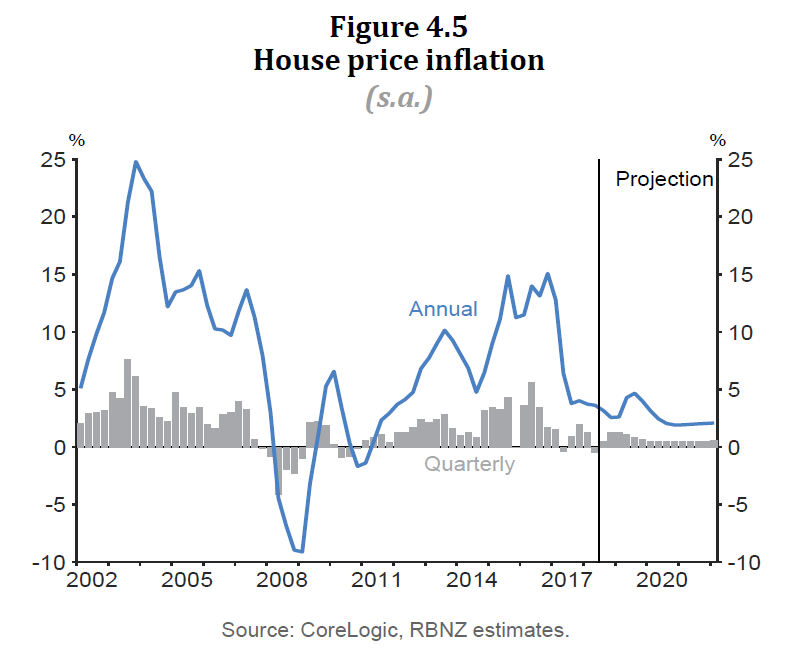

Reserve Bank Governor Adrian Orr says the central bank's latest forecasts for house prices over the next three years show a "historically low level of house price inflation growth" across the country, but with negative growth in Auckland.

"We have it as effectively zero in real terms throughout the [three year] projection horizon," he said on Wednesday at a media briefing after release of the bank's latest Monetary Policy Statement.

"That of course is for the country as a whole rather than just Auckland.

"Auckland is a big component of giving us confidence that it will be on average that type of low nominal growth across the country.

"Auckland – without doubt – negative, the rest of the country or many parts of the rest of the country still strongly positive on average. It’s a good outlook," he said.

Asked about how far prices might potentially go, Orr said: "We don’t project a particular Armageddon in house prices in New Zealand because there are so many factors that are supporting that asset class at the moment.

"But we would say that investor perceptions are being tested at the moment."

In the MPS document itself, the RBNZ says house price inflation is expected to increase slightly over 2019. The near-term pick-up in house price inflation is supported by lower fixed-term mortgage rates, and the recent easing of the central bank's loan-to-value ratio restrictions (from January 1).

Over the medium term, annual house price inflation is projected to fall to around 2%, which would put it somewhere in line with overall inflation.

Asked whether he was worried that consumers might stop spending in the face of a flat housing market, Orr said, no.

“What we have noticed over recent times is that the propensity of consumers to spend out of their increased perceived wealth from house prices has actually declined.

"A lot of what is driving our consumption growth going forward is the fact that people are employed, that real wages are rising, and our projection is for that to continue – both nominal wages rising as well as employment growth being very robust.”

In the MPS document the RBNZ states that annual consumption growth has slowed from around 6% two years ago to 3.3% in the September 2018 quarter.

"While household income is expected to be supported by the tightening labour market and a higher minimum wage, consumption growth is expected to moderate further. This is consistent with moderating population growth and low house price inflation over most of the projection.

"Growth in residential investment has also slowed, after several strong years. Activity in Canterbury has fallen. Elsewhere, constraints such as access to usable land, labour, and finance are holding back further growth.

The effect of KiwiBuild

"The KiwiBuild housing programme is expected to add to residential investment from the second half of 2019 as related policies, such as land for housing, start to alleviate constraints in the sector."

"The Bank has included $2.5 billion of additional (net) nominal construction spending generated by KiwiBuild in our projection," the note says.

"This is consistent with between 7,000 and 14,000 extra houses being built, assuming each costs between a half and the full value of an average new build.

"The net contribution of KiwiBuild to residential investment is what matters for monetary policy.

"As such, the Bank must make assumptions about how the capacity constraints discussed above will impact the effectiveness of KiwiBuild, and therefore what the programme’s impact on monetary policy will be.

"While KiwiBuild is assumed to contribute 100,000 affordable houses over 10 years, it is unlikely that this will be achieved without crowding out a significant amount of other residential construction activity, given the current and projected state of the construction sector.

'Crowding out'

"Taking capacity constraints and crowding out into account, the Bank’s point estimate is that KiwiBuild generates a net $2.5 billion of additional nominal residential investment activity by the end of fiscal year 2022.

"Over the next three years, the Bank assumes that half to three quarters of the houses built under the KiwiBuild programme will be offset by crowding out of private sector developments. The Bank’s forecast for KiwiBuild is equivalent to between 7,100 and 14,200 additional houses being built over 2019-2022, depending what you assume about the average consent value of these houses."

The RBNZ says it expects that the majority of KiwiBuild houses will be constructed outside its forecast horizon because of the constraints in the construction sector: it will take time to ease these constraints.

The Bank is expecting that the construction sector will continue to face robust demand and constrained supply. This means that the net contribution of KiwiBuild to residential investment is expected to be smaller than if there was spare capacity in the construction sector. However, if the housing market were to soften and residential construction slow or decline, then KiwiBuild may help to prop up demand in the sector, resulting in a larger net contribution.

"In the 2019 fiscal year, the Bank assumes that the net contribution of KiwiBuild to residential investment is almost zero, as the KiwiBuild programme is in its infancy and the construction sector is capacity constrained. Over the next few years, the net contribution of KiwiBuild is expected to increase as programmes within KiwiBuild, such as Land for Housing, start to ease capacity constraints."

77 Comments

Quite an interesting appraisal on the Auckland market going forward – imagine it may push a few investors/speculators to reach for the “sell” button.

Auckland TradeMe listings about to go through 13,000 – comparable this time last year was around 11,600.

Clearance rates are going need a bit of a giddy-up to avoid an increasing overhang.

Meantime all around I see build, build, build..

Something seems to be wacky with the TradeMe Auckland property count. Browse a 8 or 9 pages down into the listings and it says 14,060 listings, whereas for the first 4 or 5 pages of listings it says 12,997.

Hmmm - just did as you suggest and it seems the site is having something of a melt down.

The 31st January number was 12,285 - I'll take the 12,997 as being accurate as of now.

The 14,060 might suit my narrative - but I think it's a bit screwy.

I've been noticing the weird differential in the number of listings between page 5 and 9 for a couple of weeks now actually. So, no idea what their actual number is. Given realestate.co.nz usually has significantly more than TradeMe, maybe TradeMe's number is actually higher than the counter on the first page says?

It doesn't do the same thing when you filter for houses only etc, but the webpage renders very differently (on chrome).

I've been tracking both RE.co.nz and TM, and since 16th Jan listings on TM are up 1667, on RE.co.nz up 1345. Makes sense to me since you can sell privately on TM but not on RE. RE had 12198 on 16/1, TM had 11379.

Can’t say I disagree with him much regarding Auckland. I was saying it like a brocken record a while back - bottom of current cycle 2021/22, then will pick up. And the “bottom” will be within 5% of what it is now.

BLSH, it's interesting how you're finally factoring in the possibility of a -5% downward consideration in your own projections. That's a shift in your perception if ever I saw one....lol!

Adjusted for ave say 2%pa inflation, that makes it a possible -9% adjustment in the coming 24 months. While first home buyers will be pleased at the thought of more and more Spruikers predicting outright falls, I think like you, many are still shy to venture beyond your letterbox to reality land. There's a lot of potential and unavoidable downside risk yet to be sourced from overseas. Any moderate downside adjustments in the economies of our biggest trading partners are arguably healthy, not so healthy for the debt adicted speculator. Oh yes, you will no doubt talk on about the bottomless nature of the RBNZ's and other Central Banks tool boxes. Think again....

I guess we can expect more downward adjustments to BLSH perceptions as time ticks by??????

Poppy, you show me where I’ve said anything contrary to the above and I’ll stand accountable for any alleged backtracking.

BLSH, more to the point, where have you commented a percentage (-5%) ooops-sorry, an inflation adjusted -9% possibility before?

I’ve previously said I’d be shocked if drop exceeded 5% at bottom of the cycle. I’ve also said that if there is another global financial crisis I’d be surprised if the drop exceeded 10%. You’ve said that my comment is a “downward adjustment” - a downward adjustment from what prediction?

BLSH, if it's not a downward projection or (downside) projection you've made, then what the hell is it - lol?. There's no law against you adjusting perceptions depending on whats reported through the media. Before going into hiding, Agent TTP did it all the time.

What housing shortage? Its an affordable housing shortage, a glut of overpriced houses waiting for a reason (a shock) so as to find an as yet unknown but sustainable support base built on much healthier fundamentals.

I’m not adjusting my position one iota. Don’t you question my spruiker credentials. It is not a “downward adjustment” as this has always been my position. Prices fluctuating within a 5% band is basically flat.

...ah, just trolling ya :) Anyway, by you now slipping that percentage in there, it might now cause the RBNZ to dust off its unconventional tool box ;-)

Oh - okay, a -9% inflation adjusted fall is basically flat now is it?. Wasn't it you that referred to 1975 as the only time NZ houses truly crashed?

by BuyLowSellHigh | Mon, 10/12/2018 - 14:38 "The 2008 fall was less than 10%. Only really severe crash/downturn was 1975"

BLSH, NZ house prices underperformed the rampant inflation of the day.

Ok, good trolling then.

Don’t go telling me about inflation adjusted anything - we don’t even know what inflation will be. Yes, nominal price variation of up to 5% is flat. I think one of my properties went up by close to 5% in less than 2 months in 2015.

...are you referring to the one in Papamoa you paid 5% more than the asking price?

Brought your A-game today I see.

What a DGM

"We don’t project a particular Armageddon in house prices in New Zealand because there are so many factors that are supporting that asset class at the moment" makes him a spruiker in these here parts.

Freudian slip?

Who said anything about Armageddon?

If DFA has that term right, then Adrain's 'particular Armageddon' could be '30-45% down'

http://digitalfinanceanalytics.com/blog/updated-finance-and-property-sc…

Given his justification of why NZ won’t fall much, if at all outside Auckland, he must be surprised by what’s happening in Australia, which was in a similar situation in a lot of ways, before the market started tanking. He’s not showing that concern though, predictably.

Someone who believes NZ can't remain one of the most unaffordable housing markets in the world forever.

That's 'Doom' and 'Gloom' for some of the un-diversified, highly-leveraged 'investors' that hang around here.

Would you agree though that Auckland is cheaper than almost all other biggest cities in first world countries? I’m not talking price relative to income, just price. I’m more inclined to say that incomes in NZ are too low in comparison to other first world countries.

Auckland is also one of the most boring cities in the world where no overseas millenial would want to get stuck with a mortgage (the Kiwi millenials are on their way down south beyond Papakura).

That's a very disingenuous and slightly delusional way of trying to compare Auckland (1.7 million) with Sydney (5.1 million), London (14 million). I'll break it down even further for you - 17 is a much smaller number than 51 or 140.

NZ is much more comparable to an Australian state, and Auckland in particular is comparable to the cities of Perth and Brisbane - which are slightly larger, have much cheaper (and higher quality) houses, and much higher salaries.

Yes, London and Sydney are bigger than Auckland, but Auckland is cheaper.

Auckland is definitely nicer than Brisbane - it has no coast and a river that you can’t swim in unless you want to wrestle a shark. Brisbane is the Hamilton of NZ. The median price in Brisbane is $702,000NZD, Auckland is 862,000NZD. I’d say that price gap is fair given the difference in what you get.

....and Brisbane is about to hit the skids on the property front as well! I have rellies there who are trying to develop, and halfway through, the banks have said "That's it. No more funds for you". There's going to be a disaster in the Brisbane/Gold Coast market. So, yes, pretty much like Auckland and Hamilton then!

The median price in Brisbane is $702,000NZD, Auckland is 862,000NZD.

That's half the picture. I mean shall we trawl the real estate websites and compare what half a million gets you in Brisbane vs Auckland? Remember the kinds of houses people flip in NZ (mouldy weatherboard shitboxes) often get torn down in Australia.

And I disagree, Brisbane is definitely nicer than Auckland. Everyone earns more, food is much cheaper. People are friendlier and it's full of trees. Even compare the airports - last time I flew back to AKL from BNE it hit me in the face as soon as I got out the terminal. Auckland is just a step down, you're one-eyed not to see that.

Face it, you're just typing what you want to be true and what you desperately hope happens. I've surveyed the landscape and made my decision - you're stuck with yours with your finger in your ears. I'd respect you a lot more if you just said "I can handle a house crash because I'm in it for decades" - that's sensible. Your wishful thinking isn't.

It is close to the Gold Coast, I’ll give it that

And Auckland does have a departure lounge, to its credit.

In fairness you also just type what you want to be true.

How? I'm not buying in NZ. If anything it's in my best interest for house prices to continue to rise, because I have family members who own property.

Why would I *want* house prices to fall here?

EDIT: Full disclaimer, if the regions suffered a monumental price collapse, say 50%, in the next two years, I would buy. But even I'm not that bearish.

I dont know why as there are too many options but your assessments are not even handed, you display strong bias.

Auckland most definitely is not nicer than Brisbane. In Queensland, the suburbs are nicer, the quality of the houses is nicer, the weather is nicer, the food is nicer, the beer is nicer, the fuel is a nicer price, the wages are much nicer. Why are you telling blatant lies?

Comparing Auckland to other first world cities like New York, San Francisco, London or Paris is a bit of a stretch. They’re major global financial & business hubs. APAC as a region is insignificant on a global scale. Auckland isn’t even a financial or business hub for APAC.

Incomes are low because as a country we don't make any money. Or have a productive global industry outside of the primary sector. Depending on who you ask, we’re 28th - 34th in GDP per capita. Hence house prices need to be compared to income.

My view is, ours are out of wack because of capital inflows from elsewhere. (experienced the same thing living in Vancouver for a decade). Those capital inflows have dried up. Surprise, surprise, stagnant house price growth. As local money (apart from those who have made considerable money in housing), can afford to buy/trade up in Auckland. Same as Vancouver. Regions are booming because currently its the only place local money can afford.

I’m not saying they are similar to Auckland at all, I’m saying Auckland is cheaper.

Well, they are now that Auckland prices are falling. Those larger cities have people earning more money to support them.

Here are the median house prices in the top 100 US metro areas. Doesn't make Auckland look cheap at all:

https://www.kiplinger.com/tool/real-estate/T010-S003-home-prices-in-100…

You can’t ignore price to income like that, especially when there’s a foreign buyer ban. The median house price in Auckland is sky-high, and you just have to drive around and think to yourself, “are those very average houses intrinsically worth a million NZ dollars, really?” No, more like $700k or less.

But Auckland is unique among the world in that it has beaches. Or something.

House prices have risen because of the Auckland effect and they will go down in the regions for the exact same reason.

When exactly?

When the excess money from an inflated Auckland market is all tapped out, which looks like being around about now

Houseworks, who dares to utter the words "regions" and "correction" in the same sentence? Like it or lump it, both words do belong in the same sentence due to the overcooked valuations at play. The truth needs to be told.

"Auckland – without doubt – negative, the rest of the country or many parts of the rest of the country still strongly positive on average. It’s a good outlook. " - Governor Rbnz

People buying in to chase the higher capital gains in the regions will sell just as quickly when things turn. Australia is similar there too.

Many of these regional buyers are actually homeowners who have fled unaffordable Auckland are are there to stay. So they won’t be selling in a hurry.

So who will buy the next round of houses? Locals on their miserly incomes?

Well all the developers that have got signed contracts for Kiwibuild will be smiling at their agreed prices no doubt. So the govt may end up being the largest house buyer for 2019/2020

Kiwimm, a rather patronising comment dont you think and btw we dont necessarily chew grass and say moo

I would like to know where house price support is going to come from in the regions when cashed up Aucklanders stop being cashed up, given that local salaries are miserly in relation to house prices?

And what gives you the idea that people in the regions have meager incomes?? Many a horticulturalist would earn far more than you that is unless the police find their special herb, I jest haha. You may be referring to particular regions with high population of Maori like kaihohe 55 percent. But then those houses around there are especially low. There are many more parts of nz

I am (still) talking relative to house prices

You know that's what they said about auckland "overpriced relative to ..." but prices kept rising, confounding experts. The country as a whole has a lot of variables from region to region so what may be true for kaikohe is not necessarily true for thames and coromandel

Auckland was overpriced relative to local incomes. Now that non-local incomes have been removed, it is reverting. I suggest the same will happen in the regions once the migrating Aucklanders fizzle out.

What I want to know, when is it happening? The correspondents on here have been saying that and been wrong for the last two years. Kiwimm you are just another trying to keep the mantra alive.

............................ tick ...........................

... tock .....................

I can understand you are not brave to make a prediction...Or better still, valentines romancing

On a risk management basis, you should be short investment property right now. The likelihood and impact of a fall outweigh the potential upside risks.

Auckland prices are falling now. The regions will follow once the Auckland sellers can't get the price they need for their moves. I would give it 6-12 months.

I also reserve the right to update any forecasts as the information changes.

Short investment property which is not to say owner occupied provincial housing. And are you stil predicting a collapse? Timeframe 6 to 12 months, I would say that is a very short time frame, because the regional market has momentum. Momentum is what you would experience should you unwisely stand on a railroad track even if the driver applies the brakes in advance.

And momentum is a vector - so has magnitude and direction. Direction is changing.

"I also reserve the right to update any forecasts as the information changes"

So what you have is

- it will happen soon, 6 to 12 months

- I cant say how much by, a change of direction maybe

- I reserve the right to change my mind

It seems so tough when you have to try and be specific

I am not trying to make a specific prediction. Too much will change between now and any predicted date that for it to be right would come down to chance. Better to discuss and weigh up the risks. Unfortunately for the other readers, you have failed to offer up anything useful.

Keep the mantra alive rp. But while you have been harping on and generally missing out again and again we have bought more and more into the regions. The numbers stacked up and for some "unknown" reasons others also thought so.

Do they think house construction is supply constrained or demand constrained. If it’s supply constrained, then presumably the constrained will relax over time as resources are redeployed to housing construction. If it’s demand constrained then that implies a drop in prices.

more bad news for auckland property prices

I guess that's why tothepoint has gone into hibernation - I'm sure he's curled up in the fetal position having a little cry at the moment.

I have observed and now named the 4th_estate money wave. It originated in Auckland courtesy of direct foreign investment and q.e. derived liquidity which then spread to the regions. As the direct foreign investment and q.e. derived liquidity was crimped, Auckland stalled and proceeded to drop, as the money wave receedes around the country we will see similar declines in property values. It was all built on sand.

A house is a house is a house. They're just pieces of physical infrastructure, decaying from the moment they're built. Entropy waits for no structure.

But one species has decided to fool itself that attributing ever-greater numbers to that house, means something. Vis-a-vis others who don'd have a house, that may well be. As an overall game, it's a draw-down. Sooner or later macro society has more infrastructure balls in the air, than it can juggle. Looks like we are going to go to war over 'what's left', which may reduce the demand for housing......

Who would want a house! What a horrible life.

Much better to live in a certified organic tent woven from fine hemp consuming a healthy diet consisting of soy based meat-style certified vegan halal gluten-free dairy-free products which may or may not be cooked depending on the solar panels output. Since tiles and plastics are carbon intensive I'd use a cold outdoor shower instead.

Then I can look across the street and see the neighbours leaving their big house driving their 4 carbon-factories to school in a new Toyota Landcruiser SUV and think about how futile my efforts are.

You'd be doing your bit to offset their lifestyle.

When you have house prices falling in Vancouver, Sydney, Brisbane, Melbourne and Perth and Auckland you can ask yourself what they have in common if you like. There's a good list including; Pacific rim proximate to China, Anglosaxon property laws, Major national citys and transport hubs. I don't mean to imply anything and I suspect Adrean Orr didnt mean to mention the word Armageddon.

OH okay ... a central banker tells us it's going to be okay! Phew that's a relief! The central banks wrote a song about this... https://www.youtube.com/watch?v=1Vx8KpqTVCk

Bernanke 2007:

"Overall, the economy appears likely to continue to expand at a moderate pace over coming quarters," he said, adding that he doesn't see a recession coming this year.

Paulson 2007:

"I believe there is enough strength in our economy that we will continue to grow through this though housing is the weakest part of the economy."

Orr 2019:

"We don’t project a particular Armageddon in house prices in New Zealand because there are so many factors that are supporting that asset class at the moment...

the rest of the country or many parts of the rest of the country still strongly positive"

My thoughts exactly, not to mention Fed Chair Greenspan in 2005: “Although we certainly cannot rule out home price declines, especially in some local markets, these declines, were they to occur, likely would not have substantial macroeconomic implications.”

These guys just don’t see the bubbles, because they have their hands on the wheel and it couldn’t possibly happen under their watch, using their economic framework that led to it happening.

Well, they're hardly going to come out of nowhere and revise their forecasts to a massive and sudden price decline. They'd be bringing on armageddon themselves.

Out of Australia on the price feedback loop.

Now the price feedback loop has turned negative ...

"It's a snowball effect — when people see prices fall in a market, they're less inclined to buy,"

"People fear falling prices, and they move out of the way."

Banks remain cautious on lending, despite what may be their official line, he said, and the declining residential property market is putting would-be borrowers off buying.

"The net result is stagnation in terms of activity — more properties on listings, but not necessarily being sold, and deeper home price falls," he said.

"It becomes the feedback loop that drives prices significantly lower."

Source: https://www.abc.net.au/news/2019-02-13/lending-slump/10807478

At some point the banks will review and revalue the property portfolios of the business loan and commercial loan borrowers who have used the proceeds to purchase residential real estate portfolios. In most cases, the loans have a LVR covenant of 65%. If there are borrowers who are close to this covenant level, a downward property valuation may result in a covenant breach and the bank may request additional collateral. If there is limited cash available or limited unencumbered assets to pledge as collateral, this may result in properties being sold.

Remember that 8% of the borrowers owe 40% of the mortgage debt ...

I tend to agree with Kiwimm. It appears Auckland is running into an affordability issue. Auckland has the highest NZ household income at ~$100K/year but with average house prices at $800K an 8x ratio is way out of wack 4-5x is more typical. You can’t sell houses that people can’t afford.

Yes, it's always been an affordability issue, and I mean a definition of affordability that does not mean how much you can get a purchaser/renter to pay at the expense of their other basic needs like food, education, health etc.

As south_island_Simon said above one of the commonalities we have with other dysfunctional housing markets is UK based housing legislation.

This legislation particularly restricts the ability of land to be developed in sync with supply and demand signals which in turn causes supply shortages and thus houses prices are a lot more expensive than they need to be, irrespective of interest rates, immigration etc.

Any induced savings by lowering interest rates, saving in building costs etc, without the first solving land regulation(supply) only gets capitalized into the price of land, pushing up the price further.

With raw land price costing so much due to the artificial restrictions, then any reduction in demand either through house prices being too expensive for local buyers, and/or lower immigration leaves us with high houses prices and lower demand. And as future development land has already been purchased at inflated prices this underpins what the minimum any new sections can be sold for, which is still too high.

This only leaves housing to become cheaper by either equity losses by developers and home owners and/or Govt. subsidized interventions like Kiwibuild.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.