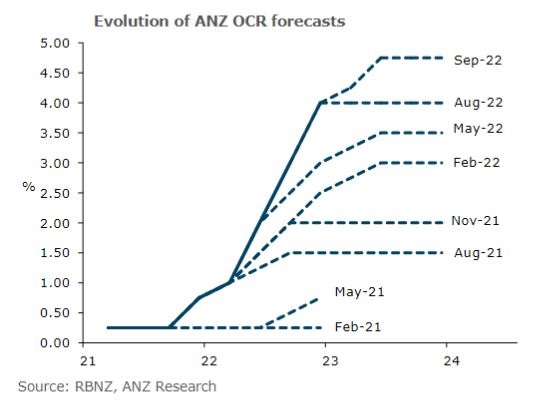

ANZ New Zealand's economists now expect the Official Cash Rate (OCR) to peak at 4.75% next year, up from their previous estimate of 4%, arguing that economic risks are firmly tilted towards inflation and inflation expectations.

The Reserve Bank currently has the OCR at 3%, having started increasing it from its record low of 0.25% last October. However changing her OCR call, ANZ NZ's Chief Economist Sharon Zollner says the economy isn't rolling over, with a tight labour market and strong wage growth partially offsetting the impact of higher interest rates. Additionally she says the low NZ dollar is also a meaningful offset to current monetary conditions.

With Consumers Price Index inflation hitting a 32-year high of 7.3%, and official unemployment at just 3.3%, Zollner says the Reserve Bank needs to see "a fair degree of slack in the economy," including unemployment rising to 5%.

On Thursday Statistics NZ reported Gross Domestic Product (GDP) rose 1.7% in the June quarter, well above the 0.4% increase forecast by ANZ's economists. Following the GDP release, ASB economists also revised their OCR forecast, now seeing a peak of 4.25% early next year, up from 4.0%. According to ANZ's economists, as of Friday financial markets were pricing in a peak OCR of around 4.34% in May/July next year, with cuts priced in after that.

"By hiking the OCR, the Reserve Bank is trying to cool demand to the extent that it drops below (constrained) supply, opening up a 'negative output gap'. That is, they need to see a fair degree of slack in the economy – including a 5% unemployment rate," Zollner says.

The Reserve Bank's Policy Targets Agreement with the Government requires it to target maximum sustainable employment alongside price stability - keeping inflation between 1% and 3% on average over the medium term - when setting monetary policy. However, just what maximum sustainable employment is, is somewhat vague. It's not a specific unemployment percentage.

The Reserve Bank is next due to review the OCR on October 5.

Wanted: Spare capacity

Zollner says recent economic data shows although the economic growth profile isn't strong, it’s not clear that beyond the housing market the rate hikes delivered to date are succeeding in opening up much spare capacity in the economy.

"That requires meaningfully lower household spending. In our consumer confidence survey, those with mortgages were more likely to report that it is not a good time to buy a major household item, but on the other hand, they were more likely to report a better personal financial situation. That likely reflects that those who have houses are typically higher income earners and therefore are being put under less pressure from the lift in the cost of living," says Zollner.

She says wage growth is at least the highest it has been since 2008 and is yet to peak.

"The share of jobs receiving a pay rise of greater than 5% has surged to the highest level since 2008. Median weekly earnings were up 8.8% year-on-year in the second quarter of 2022, the fastest increase since the data began in 1998. Firms’ wage expectations remain very high. The unemployment rate, at 3.3%, is highly inflationary and likely to remain so for at least another year."

Additionally Zollner says core inflation measures are all at least 4.8%, and it’s unclear they’ve peaked.

"While retail volumes are lower, ANZ card spending shows spending on discretionary items like restaurant spending holding up. Both business and consumer confidence are lifting from their lows. Firms’ four biggest problems are all inflationary: finding labour, costs, wages and regulation. Anecdote is consistent with demand holding up."

And while house prices continue to fall, with falls almost reaching double-digits, Zollner says they appear to have found a floor.

"In our updated forecasts, the OCR rises by another 175 basis points, from its current level of 3%, to 4.75% by the middle of next year, and we assume that goes into floating mortgage rates 1:1. But headline inflation does a lot more of the work of lifting real interest rates, dropping from 7.3% in the second quarter to 2% by mid-2024 – that’s 530 basis points of lift in real floating mortgage rates. That highlights that if inflation doesn’t fall as far or as fast as our forecast, for whatever reason, then there is still upside risk to our OCR forecast peak, even at 4.75%," says Zollner.

'Neutral OCR is rising'

She also suggests the neutral OCR, the level where it's deemed to be neither stimulating nor constraining economic activity, is higher than the Reserve Bank's latest estimate of 2%.

"Given how far inflation is above target, expectations that it’s going to remain that way for some time, and strong wage growth, it’s not unreasonable to think that the neutral OCR is rising. That is, on the street, people’s idea of what a 'good' mortgage rate looks like is likely lifting as the shock of the abrupt rise wears off and 7% wage growth takes some of the sting out of the increase in both debt-servicing burdens and borrowing capacity," says Zollner.

"While both uncertain and unobservable, the neutral OCR matters a lot. If it is indeed lifting, then the OCR is chasing a moving target. It needs to rise along with neutral 1:1 just to stand still in terms of the real contractionary impact it is having."

"We suspect the neutral nominal OCR is currently around 3%, or at least will be soon. That might sound high, but it’s worth noting that unemployment is currently lower, and inflation higher, than in the mid-2000s, when the Reserve Bank estimated neutral was around 5%."

"We are not anticipating that the Reserve Bank is going to make a sudden step change in their estimate of neutral. Rather, we are anticipating a slow-burn story of inflation pressures just not cooling as quickly as the Reserve Bank is forecasting. We therefore are predicting a series of 25 basis points [OCR] top-ups, rather than a continuation of aggressive double-sized moves," Zollner says.

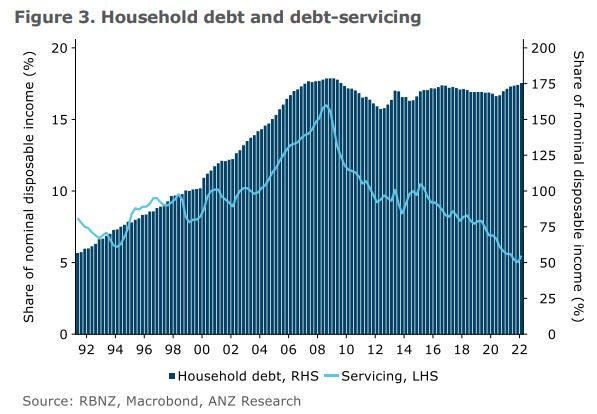

"The mythical median household is actually well-positioned to cope with the consequences for mortgage rates of an OCR rising to 4.75%. As figure 3 [below] shows, the debt-servicing burden is a fraction of what it was in 2008, when the OCR was 8.25%, and still will be at 4.75%. Household debt relative to incomes is actually about the same as it was then, though this statistic masks a large wealth transfer from a younger cohort to an older one."

ANZ is New Zealand's biggest residential mortgage lender with total housing loans of $102 billion at June 30.

191 Comments

They are not predicting, they are persuading - persuading commentators and the public that rates are going to get higher so that the banks can push mortgage rates up and / or get more customers fixed at high mortgage rates for longer. The banks want to feast on the diminishing disposable income of households whilst they can - they know inflation is cooling and time is short!

Um... have you checked in with the US Federal Reserve lately?

Noticed inflation rates in Europe?

Do you mean the US Fed that has just seen a 0.1% month on month rise in CPI and still seems insistent on creating a recession?

... Europe where gas prices are driving everything? Thankfully, we don't have the ability to export our gas so we are insulated from that madness.

Financial markets are now pricing in the possibility of a 100bp raise by the Federal Reserve soon.

It may not happen, but the markets are showing that it is a real possibility. Whatever comes out of the Fed next will not be gentle. They are on a path to raise rates in a big way, and fast.

Yes they are drunk on their power to kick people out of jobs and destroy businesses - it's a shameful and pointless p*ssing contest between central bankers.

Lol. No. They are just playing the game in the bounds of The tools available.

No one is. Setting out to personally destroy your life.

Instead of being pissy about it. Understand how they are working and plan how you can best benefit and protect yourself

I am very well protected, thanks. But, hundreds of thousands aren't.

What instead contributed to the “miss” to expectations for the core CPI, in particular, was how the index accounts for rent and shelter. Nearly a quarter of the whole consumer bucket consists of something called owners’ equivalent rent (OER).

This isn’t actual rents collected, charged, or even advertised; rather, it’s a placeholder the BLS uses to infer notoriously difficult to pin down shelter costs from housing prices. Without getting too far into them, OER tracks home values at a lag of 12 to 18 months.

Long story short, the summer acceleration of OER in the CPI and core CPI is last year’s housing bubble finally showing up in the mainstream “inflation” measure. Over the past three months, it “unexpectedly” offset the deceleration in other goods prices alluded to by the domestic retail sector that has been lately overwhelmed by inventory. Link

Banks are profit based entities, not public servants. At all times thier rightful mandate is to make as much profit as legally possible.

Solution to your anger = buy shares in the banks.

Also check where your kiwisaver is invested...

Perfect liberal Labour othodoxy, we need to create a mindset of renting in perpetuity and owning nothing. Push rates up to 10% and let's get the homes of the young reposessed so the State can look after them. Crush priviate landlords in favour of the state. Labour and Orr know what's best for you.

If they push rates to this level it will not be because they choose to; it will be because the alternative will destroy the value of the NZ $.

"Crush priviate landlords in favour of the state"

Good idea, lets start by removing the L̶a̶n̶d̶l̶o̶r̶d̶ ̶S̶M̶P̶'̶s̶ Accomodation Supplement

Hmm. An actual real Labour party instituted Land Value Tax in NZ, and broke up speculative land banks to get land into the hands of many average Kiwis, including owner-farmers. An actual left-leaning party wouldn't be subsidising property speculators as this lot have continued to do for years, and indeed have increased subsidies to in recent weeks by lifting FHB grant thresholds. A "labour" party wouldn't be over-taxing working Kiwis while subsidising property speculators.

It seems in NZ we have generous welfare for the older and wealthier and "rugged individualism" for the young, while we tax them and indebt them to fund that welfarism.

That's like saying, "real communism doesn't result in the starvation/death/murder of millions". A convenient line for sure.

I'd rather good governance that can situationally pivot, over ideological blinders.

No, it's just simply saying that if a party is behaving in a right-wing way, it's not a left-wing party.

I assume you don't think all countries with People's Democratic Republic in the name are actually democratic and govern for the hoi polloi?

They are seeing something coming therefore are trying to get people to fix now and fix for longer.….

That "evolution of forecasts charts" is very informative.

Might as well play in the tail on the donkey.

It comes from the ANZ report, so to me looks like a deliberate "read between the lines please" request from Zollner and her team. They seem to have been directionally correct in saying rates will move higher than RBNZ forecast across every forecast in the chart you refer to. My interpretation is they believe the reserve bank will have to push the official cash rate above 5% but can't say that out loud.

https://publications.anz.com/SingletrackCMS__DownloadDocument?uid=99702…

Yes. Going by the ANZ teams form of 7x upwards OCR track provisions - more upward revisions would be a dead giveaway.

5% pls in 2023 are very likely. 7-8.5% mortgages are coming.

If you listen to the "independant expert" likes of TA and AC "rates have peaked, buy now punters" - you are being sold a lemon and down a course to financial oblivion.

The FED will pull up their funds rate hard and it will be shocking to all (US stocks will shock and property will go flacid) ......US 30year mortgages are now skipping past 6%.

RBNZ must only watch the FED and can but only, go bigger.

The 3/4 hike priced into the FED meeting next week....a biggie!. If they go the full 1%... WOW....the RBNZ may have to do an out of schedule, emergency hike?? Maybe. Or the NZD goes well into sub 58c.....

NZ Gecko

what about the stress testing?

shouldn't the banks be taking into account their inability to forecast and therefore increase test rates as a percentage as well

Yeah agree. The RBNZ should lead this charge and it should require banks to be testing all housing borrowers at 8.5%. RBNZ have dropped many balls, lets stop crap performance it now.

This is all in keeping with the current knowledge that inflation will haunt us for years and energy scarcity will be here for another 10 years at least, maybe longer.

Oil drillers are all largely preferring to produce what they have already discovered (2 to 10x years ago) and not risk big on new rounds of risky exploratory drilling. This is due to the world govts saying in unison "we hate your guts" and may regulate you out of existence.

We need increasing oil/gas production for at a minimum of the next 10 years.......and will use its many, many products, for many, many decades.

Energy shortages are very likely to increase - inflation is the new norm.

Stress testing at 8.5% isn't enough.

If they forecast 4.75% OCR ...so 7-8% rates and know they are throwing darts so to speak then shouldn't they add a buffer....so they don't lend money to those who cant repay.

In these times testing at 10-12% seems more prudent.But that would mean tightening and we know where that leads.

What does the bank do.

Must be classic to be a fly in the wall in these organisations.All the hoopla of "profitable sustainable growth" meetings to now a few people being asked to join special meetings with legal to discuss "other scenarios".

And half the middle management must be hoping the game can be kept up because they bought a rental or two, and the other half hoping it falls in a great fucking heap because housing is the biggest pain in the arse they didn't think they would be dealing with when they started.

Sure, stress testing will be a moving feast past 8.5%, to who know where, as the OCR becomes a cat (RBNZ), chasing inflations tail....

how about all those who were stress tested at 6.5-7% ... this is going to get ugly

It is well to remember that in 1982, one could buy a 30-year US Treasury bond at 14% interest --like many investments, pretty spectacular in hindsight.

Rates can go much higher than they are currently; let's hope they don't approach those long-ago levels.

I was a teenager then, and my mother had a couple of rental properties. I remember her telling me that the rule of thumb for buying a rental was that the annual rent should = 10% of the property's purchase price.

Fitzgerald i bet she didn't have property managers either

did she visit the tenants on thursday evenings, every thursday evening, and collect the rent in cash?

good god...she probably paid tax on the earnings!

if we went back to that the price of housing would be a third to half from now...but the banks much smaller

i think thats where we are going...ouch for the couple of hundred thousand "landlords" who got into rentals

but we have been here before.....farmers know all about lean years, kiwifruit investment in the eighties ended up bloody hard going and vines were pulled out, manufacturers too...we used to have plenty of them.How many drawings were shredded and the machines sent to the tip.How many people with the ability to employ fifty staff and make something are still doing it twenty years later.How many lost their deer investment over the fence and into the bush....supposedly.oh....remember miami vice and the vbg...how many lost the lot.We will look back and tell stories of the auctions too one day.

some will find a way through.....roosters to dusters for others

but who really knows.....putin could capitulate before the upper hutt market does.governments will have to manage the banks knowing full well they have the populations heads on the block.maybe national will get in and commit to building the hundred thousand houses that we need.

and the not knowing part is the most f**king annoying part

and so many of the population are living in a state of complete uncertainty

no wonder we are dealing with mental health issues like never before...probably one hundred thousand kiwis don't know for sure where they will be living next week.probably half a million don't know about next year for sure. dinner,teeth,bills...no idea how

should someone buy a house or not buy a house...when did it become a life wrecking risk?

and becoming a society we aren't so proud of.....looting...really? don't mention the family violence...oops i did

living in new zealand is like living in the matrix.....how many kiwis are using the banks lending to fund a lifestyle and/or funding their lifestyle with a government payment.how many kiwis worry about a letter or a phonecall from the bank or government next week

we get told all these bloody numbers......ocr,pmi,balance of trade, twi,fixed rates...floating rates,gdp,gdp per capita

but we never get told how may are free of the banks and the government...it seems the two options mostly taken for "getting ahead" or "keeping your head above water" are the banks or the government.

how many don't give two hoots about what happens next week or next year? is it 6.8% of the population aren't in debt ,fed, housed and /or need a working for families payment to top them up on tuesday

is it 16%

is it 24%

any takers

how many don't rely on the banks,govt or a pay check?what's that number

how many kiwis are in control of their lives...let me guess

1%

I think it is gradualist delivery of higher expectations which they can't do abruptly or face losing their jobs (as the banks/RE industry pay their wages after all) or risk losing face if they are too far away from consensus/RBNZ views and are wrong. Hats off to Zollner though for leading the charge.

At least they intimate that given current inflation rates, real interest rates are still accommodative which appears to be lost on many commentators globally.

Moving up progressively from 3% to 3.5% to 4% to 4.25% and now 4.75%.....going forward definitely will be 5% .....plus.

Wait and watch.

Market need shock treatment so for a change instead of 0.5% should do 0.65% if not 0.75%....but will he....never

If the FED goes 1% the RBNZ may suddenly grow a pair.

I sincerely hope the Fed does not go 1 percent. If they do I expect a lower NZ US cross and that could be damaging to our little economy despite the spin off benefit to exporters.

Why doesn't anyone hold these bank economists to account? As a customer, could this not be taken as misleading information... the inconsistency and flip flopping in forcasts certaintly doesn't help one make good financial decisions. What purpose are they there for if they really have no idea...

Corrupt to the core but that is what you get when they can create money out of thin air and influence regulation. All power no accountability.

I don't believe it's corruption. They run a business and as such want/need to make money. Just like the car seller telling you their brand is the best for this or that reason.

When does it start to be misleading information or fake advertising? Ask a lawyer.

A bank is different to most businesses surely, in that one of their main functions is to look after their customers money. I just think it's a conflict of interest. If banks have no concern with their customers own financial wellbeing, that's a bad thing. I don't know, just my opinion.

I think it’s at least a form of corruption.

I think the picking of winners and losers and how the pie is shared (when the additional money is created) is where the problem falls in my opinion.

2008 - now, it has been decided that asset owners were going to be the beneficiaries of the money creation. Then we wonder why we have financial and social instability. How could that possibly happen! (um....)

And yet if you voice this opinion, you get ridiculed as a doom gloom merchant by the people who don't appear to care at all about financial and social stability - they only care about have more of the pie unevenly served on their plate for them (for no benefit for anyone else) and at the expense of the other members of society. It hasn't made society or the economy better, it has made it worse in many regards.

(and by no means am I a socialist, but what has happened 2008 has been ethically and morally wrong in so many ways that it should be prevented from happening again....well at least until the next long debt cycle is ready to come to an end 75 years from now....by which point nobody will be alive to remember the stupidity, just as nobody appears to remember the stupidity of the 1920's and 1930's).

Exactly IO.

Im not a socialist either but one reason I won't vote act or national is I wouldn't trust them dealing with the banks when if/when this goes tits up.

Will NZ get the best deal if Luxon is on the phone to Key?

Yip, as I've pointed out previously, if Luxon had any political smarts, he'd sell all his assets and put them in a blind trust.

If he did that, I'd consider voting for him.

Exactly what Key did.

In the interim, him owning 7 houses for his own financial benefit, during a 'housing affordability crisis' just comes across as being a hypocrite to those who are stuck in poverty (in my view).

Still going on about that even though it would be political suicide for him to do it now...

I guess Luxon might turn out to be a less politically intelligent/savy version of John Key. Perhaps good for the country (or perhaps not...if it means we swing too far left for to long), not so good for the National party.

im sure he wasn't using negative gearing and not paying tax

when's a journalist going to ask if he was paying any tax at air nz

they asked trump ...i hope they ask luxon

i would love to know

Well said!

Nifty, they do have an idea. It's way worse than they thought. It's a fast moving train wreck.

Hold someone to account for not correctly predicting the future in very unusual circumstances? Sounds like a good old fashioned witch hunt. 🧙♀️

They've been wrong for years...that's the only thing they're consistent doing.

I don’t think they have been that wrong really. The worst economists are the ones constantly predicting the Armageddon, the likes of Nouriel Roubini, everyone forgets the millions of times he’s wrong as long as he is right once a decade.

The broken clock is right twice a day sort of metaphor.

It's a chaotic system, where predictions and intentions feed back into the system. I don't think it's possible to accurately predict.

Correct. If economists could accurately predict then the market would react accordingly and the prediction would no longer come true.

What are they trying to achieve through these predictions though... are they trying to help their customers, are they deceiving their customers to increase profit, are they trying to put pressure on RBNZ and or political parties?

If they're consistently wrong they should atleast disclose that the probability of them being right is very slim. Yet they can't, because they're meant to be seen as the experts.

It's interesting though that it's the first time I've seen Zolner/ANZ acknowledge their incorrect predicitons... it's getting ridiculous now and even they're worried and/or embarrassed.

The met service get the weather wrong all the time and that is much easier to predict. Yet I still look at the weather forecast and don’t complain if it is a degree or two out, it is still useful information. As I said above I don’t think the banks have been that wrong, a few percent out here and there is expected, but they have vary rarely got it completely wrong. It’s up to you whether you listen to their predictions.

also it’s quite possible that their predictions influence the market thus causing them to be wrong. Imagine if they could accurately predict a 20% drop in stock prices, everyone would then sell hence there could be a 40% drop and they would be wrong. It’s a bit like back to the future, predicting the future can alter the future.

Think about the data and power banks hold. Also about much their senior executive is paid.

What a strange system that to function properly needs more of peoples’ money handed over to banks and for a certain percentage of the population to be unemployed.

Will the banks’ ‘predictions’ come true, highly likely.

Is it governance for the general population, or someone else?

Can I offer a different interpretation?

It's not that 'more of peoples' money handed over' is the answer, or the desired outcome. Rather, what has to happen is that the populace as a whole needs to stop making promises.

To explain further, 'money' is at the end of the day, just a promise that you will do something. Imagine an economy where it's just the two of us. You sell shoes, and I sell books. I need shoes, but you don't need any books right now. So, instead of me giving you books, I give you a promise that you can come and get some when you need them. Expand that out to a larger economy, and you get the concept of 'money' - lots of promises made to other people, that they can at some point in the future collect their books, or whatever else they desire.

When you introduce credit into a system, then you facilitate people making promises over and above what they can currently deliver. Perhaps I have 5 books in stock, but promise you 5 for the shoes, and another 5 to the butcher for some lamb chops. I'm confident that business is going well & I'll be able to deliver, so this isn't a problem. The problem comes when everyone gets enthusiastic, and starts making too many promises - the collective economy can't deliver on those.

So, what happens? Inflation, whereby my promise to give you 5 books becomes a promise to give you 3 books. At the same time, central banks seek to curb peoples ability to make promises, by increasing the cost of doing so. In the long run, Inflation + Higher Cost of Borrowing = a reduction in animal spirits. Which is arguably good & necessary, though somewhat uncomfortable in the short term, as people realize they've written a bunch of cheques that they can't cash.

Hey Medium, I like it, can you point to video or the like that illustrates this,?

That's very kind. Although given that I just made it up, I'm afraid not! Having said that, It's not original thought - more a distillation of other peoples insights, so am sure there's something out there if you're inclined to go down a google rabbit hole & see what you can find.

Ray Dalio cover this in how the money machine works, big debt crisis and the changing world order.

Zollner says the Reserve Bank needs to see "a fair degree of slack in the economy," including unemployment rising to 5%.

When you think about it that statement is nuts. The reserve bank wants to see people lose their jobs!

Sacrifice a few to preserve the most?

Hard to accept if you're amongst the few...

The aim is to preserve weath inequality - if labour gained any power we would have to share our resources more equally... like we did for decades after the second world war before the reckonomist ghouls took over.

I don't agree that's the aim. It might be a consequence.

Ok, the explicit aim is to weaken the power of workers to negotiate higher wages. The inevitable consequence of that is income inequality.

Yes, but of all workers. So depends on what you mean by inequality. Wage inequality? Not necessarily. Between capital and labour? Ok

Capital and labour - absolutely. But all workers are not impacted equally - some have more power in the labour market than others.

We are seeing this already in NZ - earnings for low earners have increased by 1% ($8 per week!!!) since the start of the year, whilst higher earners have seen earnings increase by 3.2% ($52 per week).

Adult min wage went up 6 percent on 1 april which then would dictate wage rises for the next level of staff. My son has increased 8 percent for same job at govt dept.

Adjust for inflation - global real wages in most instance are negative at present meaning the standard of living is being eroded to prevent debt defaults. But they may happen regardless.

Wage rises should follow higher productivity not for "thanks for coming". With low unemployment, competition for any staff means increased wages for all. It seems now is my chance to get a pay rise finally after all these years 🙏

What should rent and property rises be following instead of "thanks for needing a home"?

Maybe employee's should be treated as valuable members of the organisation rather than expendable resources and wage slaves. Maybe the pyramid should acknowledge that it's those at the bottom that are holding the structure up and the gains shared better. Employee's in a better position to invest in the business would have more reason to improve the business instead of shareholders who don't really contribute anything. Consider this; when the CEO leaves there's a lengthy replacement process but the business continues to operate. When a number of lower ranked workers leave there is no business to manage. Who's really more important to the functioning of the business? Imagine if the masses woke up to this. "Quiet quitting" just doesn't seem to be the most effective protest.

The pertinent question is: How much money does the CEO make for the company?

There's a reciprocal relationship involved with employment.

You forgo a higher wage in exchange for job security and benefits (paid holidays, KiwiSaver, etc).

Your employer finances your wage, paying you weekly/monthly, generates sales, handles the legal requirements of opening the doors, finances R&D and the growth of the company, and so on and so forth. They do that using the surplus between what you cost them and what marketable value your time generates them in the open market.

What's more important, earning a crust, or being showered in fake platitudes by your employer, as if you're a school kid getting handed another meaningless certificate?

The great thing absolutely anyone can go and start their own company. Go go independence!

The alternative is being like Turkey or Venezuela. Either way people lose jobs.

Do you mean Turkey where the economy is outperforming just about everywhere else?

GDP down about 30% in the last 10 years. Not very aspiring.

The theoretical alternative is falling wages for everyone, which doesn't really tend to happen.

Official unemployment definition is nonsense. There are a lot more than 3.3% of the population not working, in study or retired.

They also have to be actively seeking work. It is a measure of how well the economy is providing jobs for those who want it, not a measure of how many no hopers we have.

Since people are allowed to change their minds, and indeed ANZ have changed their minds many times this year, I am also changing my mind - but not massively.

rather than subsiding to circa 3% by May 2023, I now don’t think it will get there till September 2023.

I also think it will take longer to get to 5% unemployment.

And finally, with inflation persisting for longer, and the OCR going higher, I think the ultimate economic crash is going to be even nastier.

100 from the fed and 75 from rbnz not out of the question.

If the OCR goes to 4.75, then the prophet will be right.

And banks will be stress testing at over 9%.

At that point, the residential construction sector will be destroyed, unemployment will be rising above 7-8%.

anecdotal, but a friend says they are being stress tested at 8.8% currently

I have also changed my mind housemouse, I thought inflation would be coming under control by now but I’m starting to think this low unemployment rate is actually structural not just a hot economy. I thought 7% was the peak but it might not be or it might take a long time to cool to reasonable levels.

But I am fairly convinced the RBNZ will eventually overcook their response as they always do.

Agree with all that Jimbo, and most relevantly the overcooking that will occur. I think the economic carnage will be delayed, but will also be significantly worse.

If debt and asset bubbles, and values based on scarcity, status and wealth result in economic carnage there's something structurally flawed in the whole system.

Lots of new and unexpected data coming in, it makes sense to change our minds occasionally.

If the OCR goes to circa 4.75, term deposits will start looking OK.

And might be worth staying in KiwiSaver Cash funds for a while.

I switched into all cash funds late last year (and I know and really like shares!) making a certain 1-4% is preferable to possible losses of 20 to 50% in the moderate or high equity retirement funds.

With banks in the Western world all increasing rates at a pace, many of my favoured shares will plumment into 2023.

Disc- still holding energy/oil stocks....the only winner currently and going forwards imho.

Good call, still losing some money on cash though (after tax and inflation) with certainty.

Yep agree, I have been in Cash since february

No buying at the dip then huh?

As I have said before, I will at some point look to go back in to shares and a growth fund in KiwiSaver. However I think 2023 will be the time to do that. However if there is a stock market crash then I might buy in ‘the dip’

Did you miss it? The SP officially met the definition for a bear market this year (down 20% from peak). Are you picking a greater fall in 2023? Based on?

I respect people like Jeremy Grantham who think it’s far from over.

Inflation is far from over, rising interest rates are far from over and damage to company earnings is far from over.

Yip I agree with Grantham - I think we've just seen the end of the beginning.

Falling knives in every asset class, would mean very bloody hands. With all the company P/Es still way to high.....other than the oilers. Not buying much, staying in cash into 2023.

Exactly.

As I say, a massive and fast plunge in the stock market and I might reconsider.

Cash is worthless and its value is being eroded away by the day...

So what’s better old wise one?

Diversification...

Energy and some commodities maybe, everything else is about to crash, big time.

What do you actually mean? Diversification into what???

I'm not going to advise what you should invest in but it's common knowledge not to hold all your eggs in one basket.. especially cash in which is being made progressively worthless...

Yes we all know that. It's an investment truth / cliche.

But right now, I would say 'diversification' offers real limitations.

Everything is shite.

I would argue cash is less shite than everything else.

Yip agree...I'm about 20% equities at present and most of those are focused on energy, resources, metals etc so very defensive.

With share markets down 20% this year and inflation running at 7%, that 13% difference by holding cash is a gain...even if 'cash is trash'.

Even gold, the ultimate inflation hedge is down substantially, so cash is outperforming gold aka hard money right now.

And yet people constantly say fiat is shit. But it’s doing much better than any of its hedges. You can’t beat the value of money that everyday people use to trade with - unless of course your government are a corrupt bunch of numpties the likes of Zimbabwe / Venezuela / etc.

Debt is moving from being almost free to having a real cost. At that point bloated yield disconnected assets crash, and debt based leverage becomes poison.

Then...cash is king.

Great post.

'and debt based leverage becomes poison'

Watch out all you speculators!!!

Bingo! Now what would happen if we all believe that?

Rubbish cash is worthless

Its going up in value every day at the moment...it buys more of a house, more of commercial property and more shares than it did a month ago.

Exactly.

So are you saying inflation isn't eroding general purchasing power with cash? Have you been buying food, gas & general goods lately - finding you've been able to buy less? Seen the government giving cash away with the cost of living payment because peoples cash salaries aren't enough to cover basics? How's NZD looking with the likes of USD and AUD aswell - much purchasing power there?

There's this perception with some that holding cash is safe, the way the world's going it's actually pretty worrying. Ironically alot here that want the housing market to crash also hold their cash in banks... good luck with that.

You have got it all wrong Nifty1. The weekly outgoings for food and power etc is negligible compared to the price changes in the big ticket items. House prices in this country have gone up and down each week to the tune of $1500 or more over the years. Money is pouring into the USD, the liquidity crunch is coming and people are building their vulture fund to clean up when it all tanks.

Exactly what I was going to say.

The value of cash has been eroded for weekly cost of living stuff, but has more value for big purchases / investments.

Keep cash for either property and/or shares in 2023... (as I say above shares might be worth buying in 2022 if there's a steep fall)

So diversification is getting it all wrong? Inflation is not diminishing purchasing power?

The weekly outgoings for food and power etc is negligible compared to the price changes in the big ticket items

So rising costs and dimished purchasing power would have no influence on your cash holdings & potential investment purchases?

Some people here are so risk adverse that they'll never make moves... even if an opportunity is staring at them in the face... it'll always be too risky.

I'm sure many here didn't take advantage of the last couple of years, they're we probably sitting in TDs because it's 'safe'.

Holding cash long term is not a winner... it's a slow burning loser.

Who said it's a long term strategy? Not me.

1+ year in cash is pretty long term, especially if you're 100% in it. As they say, you snooze - you loose.

so what are you doing? It sounds like you are a property investor, add to the 'investment portfolio'?

Do you have shares? are you going to buy more shares?

Keen to hear more detail, as opposed to generic cliches.

No TDs longer than 6 months.

TDs less than 1/3 of total equity.

Recently bought a small business, independently managed, at less than 2* EBITDA (my workload 5-8 hours/wk, and that's in the start-up phase)

Looking for more

Why would I buy shares at 20, 30, 40 price earnings ratio?

Good. Agree

Yes, but shares are eroding at a faster rate than cash. And NZ residential property is eroding at a faster rate than cash, Even NZD cash cf. to USD cash. So, some of us are holding cash, because it's a less bad option than shares or property at the moment and biding our time for when shares or property are sufficiently deflated, that one can earn a sensible return on the income they generate.

Gold aka real/hard money is dropping so cash is outperforming nearly everything right now.

But when real interest rates are negative, its hard to know who is doing well and who is not.

Perhaps similar to my experience during the GFC, capital protection is the name of the game while you wait for the storm to pass.

It's buying less energy, less food, less shelter, less necessities than a year ago, 5 years ago, 10 years ago...

Cash isn't going up in value, those items are reducing in value.

TD's are already looking good, have been for a month or two. When just about everything else is tracking down, let alone making any gains, they look good to me. Still well on track for my 4.8% 12month TD rate prediction by Feb 23.

Still tracking down with a TD when taking into account tax, inflation & opportunity costs...

Not for me it isn't I'm actually living on mine and so I don't have to work, how do you actually put a "Value" on that ? That's right you cannot because its its priceless not having to work for some of the clowns that I had to put up with working in New Zealand. Currently on track for a 100% pay rise in Feb.

You need cash to take advantage of the opportunities that will be presenting themselves over the next 12 months.

Inflation makes property cheaper every day... don't wait more than 12 months to invest ..

Real wages are negative so everyone is getting poorer. If you're sitting on a pile of cash I agree, buying in 12 months time might be a good opportunity....but these things are complicated because you don't want to lose your fingers catching the falling knife.

And if affordability ratios/fundamentals count for anything (which history says they do), then it might be difficult to tell where the bottom is for this market.

The coming election won't have any effect on interest rates as the RBNZ is independent! Yeah right.

In which direction (if national win)?

He/she might be suggesting the OCR might start dropping before the election…

Ok yep I get it now. Still in which direction? The RBNZ have been comparatively aggressive to date.

So, have ANZ changed their house price forecasts?

Because if the OCR goes to 4.75, house prices will fall at least 25-30%, NOT 15-20%.

I expect we'll be reading about that updated forecast next week.

Yes although it could get to -30% real decrease without prices falling much at all if inflation is running at 7%. I wouldn’t be surprised if we get more of a stagnation than a massive fall.

We aren’t far off a real decrease of 30% already in Auckland and Wellington.

So are you saying 25-30% plus inflation, possibly more than 50% real? Sounds good to me but I think unlikely

25-30% nominal, so about 35-40% real ( as I think inflation is subsiding and will continue to do so, even if it takes a while to get under 4%)

And btw this is assuming ANZ are right and the OCR goes to 4.75

So only another 5-10% then if we are already 30% down.

I think the floor zollner found is in the world trade centre.

A 700k mortgage over 30 years stressed tested at 9% is $1300 per week in mortgage repayments. And that for a 2 bedroom shoebox.

Good luck to the residential property development and real estate sector sectors, let alone Architects, civil engineers, builders, contractors etc, if that’s where all this lands.

welcome to unemployment of over 7-8%.

HM

well a $300k mortgage will be $550(the national median rent) hundred a week instead of $1300

you can see where this is going

$700K-$400k=$300k

yeah about a sixty percent fall

Nah, it's the price of land that will take the major hit. That 700K mortgage is mostly land costs not construction costs. Plenty of scope for land to fall and construction to continue to make a margin.

Yep, there is still plenty of homelessness to be fixed.

Not on medium density development which is the majority of development in Auckland, at least.

Unless land values fall at least 40-50%.

If land values only fall 20-30% then it only makes a marginal difference when spread across a number of townhouses. Especially when construction costs have increased so much.

Land values falling 40-50% is not such a wild proposition anymore. You've been one of the most bullish on the house market (I'm excluding clowns like TTP as spruikers) and even you have moved your predictions from 5-10% to 20-30% over the last year or so.

WRONG.

I said 5-10% falls THIS YEAR, as my central prediction, with 10-20% falls as my next most likely. It looks like they might be around 10-15% for this calendar year.

I was always predicting 15-20% overall, from peak to trough.

If ANZ are right, and the OCR goes to 4.75, then I think 25-30% is quite likely.

If this case plays out, and you add in 24 months of 5% + inflation, then what you are suggesting is a far worse outcome than what the US experienced during the GFC.

So the price of a new build has gone up over the past few years due to input costs, rather than manufacturers and suppliers responding to price demand factors from loose credit conditions? I.e. Existing house prices rise 30% in a year, but that's not due to interest rates hitting rock bottom, but the cost of building a new house???? I suspect your cart is leading the horse.

I'm fairly close to the coalface. At the same time interest rates went down, due to an unexpected virus of unknown origin:

Labour up a significant amount (I want to say 20%, but it varies on trade)

Materials up a significant amount (or not available, pricier substitution used)

Time to complete jobs up 200-300%.

It's a great example of correlation not equalling causation, and how inflation since covid isn't just a story about low interest rates.

Fighting inflation is difficult when Reserve Banks will only use very small rate rises. The fact we expect inflation not to be put away for years should be some warning that Reserve Bank policy is widely seen as impotent.

Perhaps we are being chastened to an even higher terminal OCR? The last 15 years have been extraordinary in anyones' terms, and if 'getting back to normal' is what is now required, then may 'this' is it?.

It has not been that high since December 2008, when the rate was 5%, having dropped from a peak that cycle of 8.25%.

After all, look at where all this recent monetary madness has brought us to - right here. Is this 'as good as it gets'? If so, then no wonder the Central Banker's thoughts of 'more of the same, but even bigger' have been cosigned to the dustbin of experience.

What will happen is an over-reaction, and whammo we'll be in recession and unemployment will be up. We are now seeing net migration out of NZ as those folk who entered NZ during the time when things were bad overseas are now returning back to those countries from whence they came.

The net result will be fewer people working here in NZ, lower demand for everything, and house prices largely un-doing all the price gains of the last 3 years - especially in the big cities.

Any attempt to control inflation should have a light touch.

We've had over a year of light-touch increases hoping to tame inflation.

they will need to increase real interest rates...higher than inflation

this aint going to be pretty

That’s what I thought would previously happen but I don’t think it will now.

The RBNZ is going to overshoot in raising the OCR, just as it did in lowering it, and there will be economic carnage.

2023 is going to be a VERY rocky year.

Seems like you flip-flop as much as the economists HM...

I have hardly flip flopped at all.

But I have certainly made a few adjustments to my thinking.

And if you had it would be a very sensible thing to do when new data comes to light.

If you’d told me a few years ago that interest rates were going to more than double while house prices were in decline I would have said the economy would tank causing rampant unemployment. Yet somehow that hasn’t happened at all, we have low unemployment and decent GDP growth. It’s hard to see how anyone sensible could have predicted this.

Jimbo google" hysteresis" or read about it on wikipedia

there are delays in all systems...and our economy is one big system

Said the guy that called a 2.75% OCR maximum.

Yes I was very wrong on that.

However, like everyone, I wasn't expecting the Ukraine War, which has been highly inflationary and undoubtedly been a big influence on central banks hiking more aggressively.

Alas, economic carnage is what is required to bring inflation down - just look at any case study for any country that has successfully reduced inflation. If we end up with deflation then you will be able to claim an overshoot. We are no where near that.

Hurting much…

unfortunately, the only medicine for an over-reaction is another (That is in effect)

Finally banks starting to get realistic about where the OCR is heading. At least people are now going to start preparing themselves instead of burying their heads in the sand.

There once was a man named Taylor. His Rule stopped the 1970's/80s inflation monster.

https://www.investopedia.com/articles/economics/10/taylor-rule.asp

Tough medicine, but it worked. Interest rates above actual inflation or even 1.5x inflation.

So 25% fall is done thing and have to see how much more from here on

https://globalnews.ca/news/9134253/canada-housing-market-prices-rbc-spr…

... a generation has been addicted to house prices only going up ... to massive tax free capital gains ..... they're kidding themselves that the current price weakness is just a blip , an aberration ...

But , in the immortal words of that great property development group Bachman Turner Overdrive :

" You ain't seen nothin' yet

B-b-b-baby , you aint seen nothin' yet

Here's something that you're never gonna forget "

And start your slaving job to get your pay

If you ever get annoyed, look at me I'm self-employed

I love to work at nothing all day

And I'll be taking care of business (every day)

Taking care of business (every way)

I've been taking care of business (it's all mine)

Taking care of business and working overtime, work out

Randy Bachman - Legend!

Re Canada link, that's just in number of sales though, not prices. So not a done thing. Though some estimates suggesting 25% price falls by early next year.

So will ANZ announce another revised house price forecast (which would be their 4th or 5th revision in the past 12 months).

given that they now project the OCR to go to 4.75, anything less than a house price drop of at least 25% would be a joke.

An OCR peak around 4.75% is exactly what I did forecast very recently. Actually, if there are any risks, they are on the upwards side - an OCR peak of 5% is not an unlikely possibility at all. I would not be surprised at all if swap markets started pricing a 5% peak in the near future.

Moreover, rates will stay at or around this peak for a significant time, and only very slightly (50 to 75 bps max) decrease in 2 to 3 years' time; and such decrease will only happen if and only if the fight with inflation is won here and overseas, which is not a certainty at all. Even is such fight is won, central banks will not be keen on repeating the same mistakes of the past and reignite inflation with a return to ultra-loose policies.

The era of ultracheap money is finished - time to pay the piper - and time for the housing Ponzi to end once and for all, with a progressive return to sustainable house prices aligned with economic fundamentals.

Yes agreed, you've been quite clear for some time on here that the RBNZ needs to increase the OCR a lot quicker than it has.

If only we could have known earlier, oh wait....

Best subscription I have hands down

Banks keep lifting rates forecast. Central banks got as many people and businesses to load up on debt as possible now pulling rug out and anyone with mortgage, loans, credit cards, will end up paying some much more some who are over leveraged will just go insolvent many countries are already in this position you have to wonder if it was all planned.

As per Bernard Hickey, housing market in Auckland has bottomed out and is ready for the next move upward.........really.......is it lobbying or is it trying to influence or it is actually happening that market once again gearuping up to be in boom territory with high interest rates and still going up along with other factors.

- REINZ figures showing Auckland City and Wellington City house prices down 17-23% from the peak in October/November, but with signs the market is warming up again in Auckland in particular;

Bernard said the best thing is to buy residential land and make tax free capital gains.

I saw this listing you may be interested in: Church tells us "Sell away!" https://www.trademe.co.nz/3769910770

Who cares what BH thinks.

You gonna put an offer in for this one?

Rates up, assets down. Share markets have near instantaneous price discovery. Housing a bit slower as per the nature of its illiquidity when sellers are in denial.

As they are now.

Perhaps in other words, "You cannot run a Monetary System pricing risk at 0% forever".

The result would be/is the death of productive effort and the predominance of speculative behaviour. When the cost of Debt is 0% the borrower may never have to account for their actions; never have to pay off the loan if the cost of keeping it is 0%. Those days, 35 years in the making since we started all of this after '87, appear to have finally come to an end, and the cost of debt may be about to return to riskier levels.

Inflation, is perhaps not the reason, just the catalyst.

The best summing up of NZ in one sentence ever.

The result would be/is the death of productive effort and the predominance of speculative behaviour.

Word !

Also know as wisdom and gospel in the books of the Property Investor Association.

(how to enrich oneself at the expense of others for minimal effort/labour and benefit to society, while destroying the economy and society and community around you.....and anyone who thinks this is a bad idea must be ridiculed as a doom gloom merchant).

Was that the sound of Iceman sublimating into hot air?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.