Bond market experts generally aren’t concerned about the fact the Reserve Bank (RBNZ) will likely continue buying New Zealand Government Bonds (government debt) for some years, if not decades.

The current and former bankers and economists interest.co.nz spoke to recognised the RBNZ was never going to suddenly pull out of the bond market, having become such an active player from the time it launched its Large-Scale Asset Purchase (LSAP) programme in March 2020.

While some had criticisms of the LSAP programme, they didn’t believe the RBNZ continuing to buy bonds once the programme officially ends in June 2022 will pose new problems.

Rather, they recognised continued bond-buying is part and parcel of quantitative easing.

The important things remain, the decisions the RBNZ makes around monetary policy and how these influence retail interest rates.

By the RBNZ owning so many bonds, it has another tool at its disposal to set monetary policy, consultant and former investment banker, Raf Manji, said.

How the RBNZ gets there is a technicality those involved with the New Zealand bond market will have to deal with, ANZ senior strategist, David Croy, said.

Traders have experience in this area, with the Federal Reserve, Bank of Japan and European Central Bank among those to have done quantitative easing for some years.

Senior associate at Victoria University of Wellington’s Institute of Governance and Policy Studies, Geoff Bertram, had a different view. He believed the continuation of a flawed quantitative easing programme would only end in a train wreck.

A gradual and managed retreat - all going to plan

Going back a step, the RBNZ has bought more than $50 billion of mostly New Zealand Government Bonds on the secondary market since March 2020 in a bid to put downward pressure on interest rates and support smooth market functioning.

It’s committed to stopping these regular bond purchases in June 2022. The RBNZ has been buying fewer and fewer bonds every week. Next week it plans to buy $250 million of bonds - $100 million less than recent weeks.

But because the level of activity the RBNZ has in the bond market affects interest rates, it’s pointed out it likely won’t be able to spend the next 20 years letting its balance sheet shrink at the same rate all the bonds it’s bought mature. This would see it take its hands off the monetary policy wheel.

Rather, the RBNZ has been clear it will need to continue being an active player in the New Zealand Government Bond market.

Each time a bond the RBNZ owns matures, it will have to decide whether to let it drop off, or reinvest some, or all, of the funds it receives.

A partial reinvestment would still see the RBNZ’s balance sheet shrink. In theory, this would see it be a less active player in the bond market, which would put upward pressure on bond yields and thus interest rates.

Conversely, if the RBNZ figuratively printed money to grow its bond portfolio, this would put downward pressure on interest rates and be stimulatory.

The RBNZ this week initiated a public discussion around the issue via an interview with interest.co.nz and speech thereafter.

The RBNZ noted that if markets get confused by all the levers it’s using to influence monetary policy, they might not respond the way it wants them to, thus potentially making its policy less effective.

What’s more, there are some risks associated with it holding bonds with long durations (some of the government bonds the RBNZ has bought will only mature in 2041).

Views from within the banking system

Manji said the RBNZ having additional monetary tools could help it control more of the yield curve.

The RBNZ’s head of financial markets, Vanessa Rayner, expanded on this point in a speech on Wednesday.

“All monetary policy tools have a common aim, but the transmission channels can differ,” she said.

“Balance sheet tools can work through different market channels as opposed to just reducing the risk-free short-term policy rate. For example: by reducing credit spreads and term premia (via LSAP); indirectly reducing the cost of other bank funding sources such as term deposits (via the Funding for Lending Programme); or clearing dealer inventories to improve market-making and supporting the market conditions necessary for monetary stimulus to transmit (via LSAP).”

Kiwibank chief economist Jarrod Kerr said ensuring smooth market functioning would be front of mind for the RBNZ when it eventually comes to making decisions around whether or not to reinvest the funds it receives when the bonds it owns mature.

ANZ’s Croy believed the RBNZ would be able to step back quite a bit. The Government will eventually be able to issue less debt, and because there is so much liquidity in financial markets looking for a home, there should be good demand for New Zealand Government Bonds.

Michael Reddell, who held a number of senior roles at the RBNZ, believed the management of its bond portfolio wouldn’t have a huge effect on retail interest rates. He said this was the experience in the US.

He questioned how the RBNZ would communicate how it intends to use its balance sheet as a monetary policy tool, in conjunction with other tools like the Official Cash Rate.

A view from outside of the banking system

Coming back to Bertram’s oppositional view, this stems from him being a proponent of money financing - the RBNZ printing money at the Government’s request and stimulating the economy more through fiscal policy.

Had the Government and RBNZ decided to take this less conventional route, the RBNZ could write off the debt and we could all move on, Bertram said.

He maintained this would be better than the current “charade”, through which the Government is effectively still financing itself.

This would prevent banks from clipping the ticket as the RBNZ buys the government bonds from them in a “money-go-round” that boosts asset prices rather than consumer inflation.

Bertram believed taxing wealth would be the best way of soaking up excess liquidity from the financial system. While he maintained this was fair and clean, he recognised it was “political poison”.

31 Comments

Sounds like Bertrum is saying full-fledged MMT is "political poison".

"Those from within banking world don't see problems with the RBNZ having to keep buying bonds on the back of its LSAP programme; But an academic worries NZ's headed for a train wreck"

Banking sector is supporting as have vested interest and enjoying the party but reality is that we are heading for a train wreck ...can delay the disaster but cannot avoid.

RBNZ has no exit plan and whenever it tries to exist is bound to derail so RBNZ measures which were announced in emergency situation are permanent for now and RBNZ instead of accepting and correcting will keep on adding more, just to prove and hide their mistake.

Reserve bank will face the biggest reset in near future.

Bertrum is right to question why we continue to support the charade of bond buying and selling. When you strip it back to the accounts it is obvious what is actually happening.

1. When Govt buys or pays for anything, it instructs RBNZ to create new money and this is paid into the relevant bank account. THIS is when the govt goes into 'debt' - when it spends the money (no bonds required).

2. Money accumulates in the 'reserve accounts' of commercial banks, which are held at RBNZ. RBNZ pays banks a tiny bit of interest on the cash in their reserve accounts. There is about $29bn in these accounts at the monent - and every dollar is counted as part of the Govt debt

3. Banks bid at auctions to swap some of the cash in their reserve accounts for bonds, which pay a bit more interest. Banks buy bonds and sell them onto investors for a profit (kerching)

4. When Govt sells bonds to commercial banks, cash in reserve accounts (Govt debt) is swapped for Govt bonds (also Govt debt). So the level of Govt debt does *not* change when bonds are sold. When people say that bond sales are 'issuing Govt debt' they are misinformed or being purposefully misleading.

5. Govts *chooses* to match the amount of bonds sold to the amount of Govt money spent - this policy choice could be changed.

6. When RBNZ offers to buy bonds from banks or investors (QE or LSAP) it creates cash (Govt debt) and swaps it for bonds (also Govt debt). So, again, the level of Govt debt does not really change (apart from the profit made by the bond holder - kerching).

What Bertrum is presumably pointing out is that Govt can spend money without selling bonds to profiteering commercial banks. The Govt money spent (aka 'debt') could just be left in reserve accounts earning next to no interest, or bonds could be sold at a fixed price and yield with RBNZ buying anything that is not sold. This won't happen of course - Govt love giving free money to the financial sector.

As Bill Mitchell says, bonds are just corporate welfare for the finance industry. They are also a neo-liberal charade to give the impression that the government is financially constrained just like any other currency user and dependent upon the private sector to finance it..

100%. Bond sales don’t fund a currency-issuing government. Nor do taxes. The government can set interest rates any time it so desires - it does not need to overwhelm the private sector in the bond market.

Reading that word-soup one can't help thinking about the $180 billion waters program and whether that's been taken into account. One third, or $60 billion for Auckland alone.

So $36k for every man, woman and child in NZ. Someone is taking the piss.

Civil engineering contractors?

100%. If I had my time again, I would have trained as a civil engineer. Whether or not I would be intelligent enough is questionable, however.

You still have time

And the health and safety industry. If I had the capital and the contacts I'd seriously look at buying/leasing some of those traffic control/impact attenuator trucks and hiring staff.

Watched two guys in one of those trucks charge out a good 4 hours for 20mins actual work, which was mostly unnecessary, there was a period of maybe 10mins while the watercare guys loaded/unloaded a small digger off a trailer where they were potentially in harms way, the rest of the time they were working on the footpath back off the road.

Given the chance to do things differently I'd have bought a quarry and concrete plant. Too late now though.

Strong Towns - Shopping Malls are killing the cities - The Shopping Malls are dying

A counterpoint to what Alison Brook doesn't see or talk about

The water infrastructure bill indicates we are repeating all the same mistakes American cities make as highlighted by the Conservative "Strong Towns" movement.

Watch a couple of theses short videos and then go back and read Alison Brook's article and what she says about planning

https://www.youtube.com/watch?v=y_SXXTBypIg

And a crack at Christchurch

How Christchurch, New Zealand became a lesson in how NOT to rebuild after a disaster

https://www.strongtowns.org/journal/2021/3/2/christchurch-rebuild

Walking round Wellington recently I was reminded what a nightmare of a city that will be to fully renew the pipework. $180B is a pipedream.

“Balance sheet tools can work through different market channels as opposed to just reducing the risk-free short-term policy rate. For example: by reducing credit spreads and term premia (via LSAP); indirectly reducing the cost of other bank funding sources such as term deposits (via the Funding for Lending Programme); or clearing dealer inventories to improve market-making and supporting the market conditions necessary for monetary stimulus to transmit (via LSAP).”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Real GDP in those charts and employment flatlining - you can’t hide from that for so long when asset prices are heading to the moon.

{kind=link}

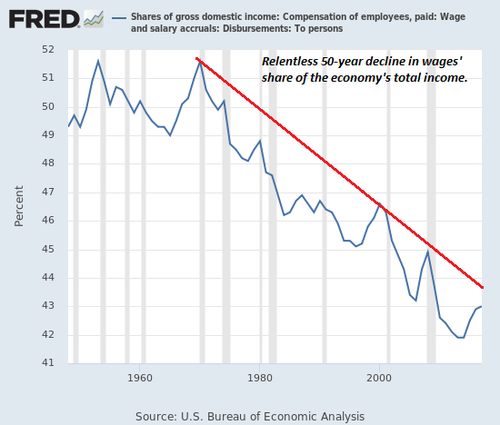

Goes to show just how blind to the reality the ptb have been given they've needed 50 years to decide someone other than wage earners needs to start paying tax.

...or clearing dealer inventories to improve market-making and supporting the market conditions necessary for monetary stimulus to transmit (via LSAP).”

History has shown US banks cannot get enough safe and liquid pristine US government debt securities on board. Occasional selling bottlenecks are mainly associated with repo funded not so liquid off the run government securities in times of severe general financial market stress. In this situation TBill demand goes through the roof.

{kind=link}

Living it up at the hotel Mogadishu

Too funny,

Damien Grant pants the RBNZ.

https://i.stuff.co.nz/opinion/300323958/the-reserve-banks-troubled-rela…

It wasn’t clear from the speech if the bank was going to embrace these values or if he was merely advocating them to his audience, the Institute of Directors, but if it is the bank’s intention to adopt them, well, our central bank has some hard mahi ahead of it.

May be its reflective of the political picture/mirage, but as same characters remain expect no change in performance or outcomes. Currency war remains.

That's up there with the best I've ever read from Damien Grant. I've always thought he was a little behind on the the shenanigans of the the RBNZ and its role in preserving the status quo. He decodes the whole charade brilliantly. And not without his wit in light of a very dangerous situation:

Adrian Orr has not been an effective guardian of the most valuable taonga under his control, our currency. It’s as if he has found a way of mass-producing pounamu and has been handing it out to his favoured constituency - banks and the Treasury.

And according to previous speeches from the RB they are consulting Tane, the tree god or some similar concept.

Actually I think inflation will pick up going forwards for structural reasons, essentially an aging society with more retirees will consume more and produces less. We are about to begin a demographic reversal in Western societies which has probably been accelerated by Covid-19.

At the same time as we have a millennial generation who are pro socialism so we may see increasing welfare (money), with lower incentives to be productive and work, meaning a lower output of goods and services, while we have more money competing for that smaller amount of goods and services.

...and compounding issues in industries like food production with a lot of land at threat of drought due to excessive use of water resources in many areas and draining aquifers at levels far in excess of the recharge rate.

RBNZ is devaluing your hard earned money in a grand scale. If that doesn't alarm you or cause a sense of urgency, nothing will.

M1 money supply- see how the printing press runs,

Buy a house today and secure your finances. They can print money but they can't print houses.

Be quick.

"They can print money but they can't print houses."

But we are printing houses now ;-p

It is possible to 3d print houses.

But you can't print bitcoin.

Better secure some crypto today.

Sounds like an addiction. Once you start you can't stop.

It's all a bit of a Rube Goldberg machine.. but will the marble be able to purchase anything by the time it gets to the end; that's the real question.

Are asset prices going up OR is purchasing power going down..

..

..

Dr Phil, Oprah.. somebody get me some indices~!!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.