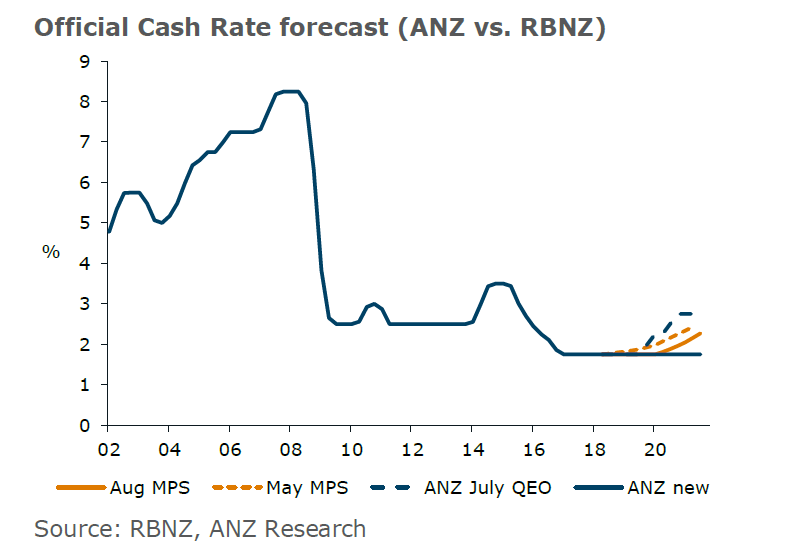

Economists at the country's largest bank have changed their call and are now no longer forecasting official interest rate rises in the foreseeable future.

And in their Weekly Focus publication, the ANZ economists say the next interest rate move by the Reserve Bank is more likely to be a cut than a hike.

Recent extremely 'dovish' statements from the RBNZ - along with it moving out its forecasts for rate hikes - have prompted the country's economists to all sharpen their pencils regarding their own forecasts.

Westpac economists said last week they now saw a one in three chance of an official rate cut within 12 months.

Previously the ANZ economists had forecast a rise in the Official Cash Rate from November next year.

"The Reserve Bank is reluctant to hike; they made that abundantly clear in the recent Monetary Policy Statement," the ANZ economists said.

"And we see growth averaging 2½% over the next couple of years; hardly a stall, but considerably softer than the Reserve Bank’s expectation. That combination is not consistent with forecasting rate hikes.

"We are now forecasting that the OCR will be flat for the foreseeable future.

"Of course it is not that we literally believe the OCR will never be moved ever again; rather, we no longer believe on balance that the next move will necessarily be upwards.

"Indeed, given how long it is until a hike could plausibly be on the cards, the balance of risks is, if anything, tilted towards the next move being a cut.

"But the economy is muddling through for now. We still expect core inflation to rise further in the near term, reflecting previous strength in the economy. But beyond that, the resilience of underlying inflation does not look assured."

The economists said their previous growth forecasts "were already less optimistic than the RBNZ and we’ve tweaked them lower". Additionally, the RBNZ made it crystal clear that the hurdle to hikes is extremely high.

"To our minds, that combination is sufficient to warrant removing hikes from our forecast entirely."

The economists said while they saw, if anything, the risks as skewed towards the OCR heading lower from here, they "will await further evidence before making that call".

"The key differences in our view versus the RBNZ’s expectations relate to the medium term. But of course there is much that can change the picture between now and then, and the near-term picture for both growth and inflation is decent. In light of that, we are comfortable biding our time."

The ANZ economists see the following developments as likely resulting in a hike:

A renewed lift in net migration or a marked fall in mortgage rates give the housing market another leg up.

Low surveyed activity indicators turn out to have very little impact.

Wage pressures broaden and impact on inflation in a cost-push fashion.

Inflation expectations lift on the back of higher CPI inflation.

"On the other hand, there are a number of risks that, should they come to fruition, could see an OCR cut eventuate, potentially in short order," they say:

Global/China growth slows more sharply than expected; the terms of trade take a tumble.

Bank funding costs increase due to a global risk aversion spike.

The housing market is weaker than expected, perhaps due to a faster fall in net migration.

Near-term consumption disappoints: the Families Package is trumped by higher petrol prices and a cooler housing market.

Businesses cut back on investment to the extent indicated in surveys.

Construction sector woes have negative flow-on impacts into the broader economy.

Drought.

The economists say the new committee OCR decision-making structure the RBNZ is moving to adds another level of uncertainty for RBNZ watchers.

"Perhaps a Committee will prove more likely to backstop growth. Or maybe it will have a degree of inertia that isn’t associated with a single decision maker. It is impossible to know, but it makes any forecast less certain. And making long-term forecasts of the OCR is a tricky business at the best of times."

47 Comments

There is only one reason why interest rates may be cut and that is a slowing economy. The banks will all go broke if people do not borrow from them, so interest rate cuts are there to tempt borrowers back. Not a good sign of things to come.

Two reasons, I suggest - to also stop the banks going broke from their current crop of debtors not being able to afford what they have already borrowed and spent. Lower interest rates will delay the day of reckoning for the banks, but only not avoid it. In a deflationary world (which it is!) debt is going to be a killer....and you're right - it is not a good sign of things to come.

Be interesting to see who in the zoo tenders their resignation 6 - 12 months after the OCR drop.

Very much "on point" BigDaddy in today's parlance ....

There is only one reason why interest rates may be cut and that is a slowing economy. The banks will all go broke if people do not borrow from them, so interest rate cuts are there to tempt borrowers back. Not a good sign of things to come.

Money comment. Totally agree.

The thing is it isn't sustainable long term. It doesn't encourage saving either. All it does is push the prices of houses up, as people can afford to borrow more, due to the interest repayments being lower.I think they would be better to keep it static, so at least there is some room to move if things really get bad. They can only take it down so low, and it will just make the NZ dollar weaker, and make petrol and other imports more expensive.

A fine balancing act required in clearly what is a transitioning NZ economy.

I have a lot of respect for Adrian Orr not only for his performance with the NZ Super Fund but he has slotted back into the RBNZ demonstrating a confidence and clear rational thinking and communication.

As such I feel all bodes well for management of the NZ economy but the potential external risks are a real threat which may be beyond mitigating.

We have one quarter of one trillion dollars in mortgage debt. It all bodes poorly for the New Zealand economy.

I have a lot of respect for Adrian Orr not only for his performance with the NZ Super Fund but he has slotted back into the RBNZ demonstrating a confidence and clear rational thinking and communication.

A monkey could have made money in these markets pre- and post-GFC.

Hi JC

Go and check figures before making flippant remarks.

Under his watch the Super Fund made 5 to 6% plus over and above the markets and other investment funds.

Adrian Orr was Deputy Goverorr Reserve Bank March 2003-2007, Head of the new Finance stability Dept. Mortgage debt rose at the fastest rate in New Zealand's history during his tenure.

Has the Super Fund out performed the Auckland housing market .

Easily.

Stay on rolling 1 Year fixed mortgages with intermittent floating.

Rates are on the way down to keep the system afloat (excuse the pun).

Petrol prices, local body rates, house insurance etc dampening down the consumer disposable income.

The question has to be asked, how on earth people are meant to be able to go on what economists say?

Most were stating that interest rates were going to be going up!

I am not a qualified economist but I can tell you that my predictions are a helluva lot more accurate than the trained economists!

Yeah i know right! Give your mate John Key a call and ask him if ANZ can make some room on the Economics Team just for you.

@ the kid 2 ........."I am not a qualified economist but I can tell you that my predictions are a helluva lot more accurate than the trained economists!"

If you were that good of an economist, coupled with your so called "supreme business acumen", you would be in the Bahamas by now, luxuriating on your private yacht....not dealing in residential properties, based on only one market.

Been to the Bahamas and it is not that flash.

A lot of cheap grog and that is about it unless you own an island.

Wouldn’t be enough for me to do over there either!

Don’t need to be a qualified economist to make accurate predictions!

I knew one qualified economist who gave a speech in the early 90s telling the room that property values were flatlining and not to buy, but stick with shares. I talked to him at the Xmas party and after he had had a few bevvies he told me that he was filling his boots with property investments and not shares. And how right he was to buy property then. How was your week TM2, did you buy that property you were looking at last week?

Housework’s, yes I did buy it, and I was the only bidder, and motivated vendor, which is what I like.

Extremely good buy and under true market value.You make money when you buy, but many on here will want to disagree with me, but that is why they are property bears, and do not get ahead financially.

Good work and good luck with it tm2. I hope you make a killing ;) we have had a hectic time doing up an old comm building which we bought for less than land value and have literally turned a sows ear into a silk purse. It's so awesome now. The property bears have a very myopic view unfortunately and so they will never agree with you and I, maybe one day they will get a taste for property.

Well done Housework’s.

The property bears just do not understand and so they probably won’t get into property investment.

We enjoy the buzz from buying a property under true market value, then improving it if it needs it.

When rented it is always positively geared so gives us an income as well, plus increasing capital gain.

Property gives us an ideal lifestyle that working for wages can’t.

Unless you have done this then people don’t know what can be done!

It's not really a question of being "correct" - at any point in time you have a one third chance of being correct - interest rates can go up, down or remain the same. Currently the country is facing headwinds - increasing rates , insurance premiums, petrol prices to name a few. Fontera , Fletchers (and other building company's) imply that the economy is perhaps not as robust as everyone thinks it is and this can not be blamed on the government - this didn't happen overnight -it has been building for some years. Currently it appears that the only way to keep the wheels from coming off the cart is by lowering interest rates. IMHO it;'s a question of the reason why interest rates are going up or down.

Brilliant interview about blowing bubbles and economics not understanding that concept... https://youtu.be/-PIm4dlw5qc

It’s funny, if you look around the economy you see evidence everywhere of inflation, it just doesn’t show up in the CPI. Housing costs are up, labour costs are rising in public sector - sure to hit private sector soon, exchange rate going down which will impact everything exported/imported, and the government is going to invest heavily in capital and services. But, forecasters think inflation is so benign that rates should be cut. I don’t see it. I’m not saying I’m right, i’m just pointing out that what could be over the hill is most likely inflation. What is the argument against this view? That confidence, growth and CPI are ‘down’. Well maybe, but they are measurements of what has happened. When we look at the drivers of inflation - labour market, stimulus, international dynamics, petrol, etc. it all screams INFLATION. So I say, interest rates are going up. If the next move is down then RBNZ will quickly reverse.

Check out BW's comment above: we are in a deflationary cycle with some false flag signs of inflation. The general trend is DOWN. Now those rate cuts may lure some credit junkies into borrowing more. I say nature will deal with those who have made themselves vulnerable when times are bad.

If we are in a deflationationary cycle why are house prices and rents going up? If we are in a deflationary cycle why are there labour shortages everywhere? If we are in a deflationary cycle why is petrol $2.29 in Wellington? Personally, I see more chance of stagflation than deflation.

Because you are only looking at the bipolar economic jitters of two tiny islands - zoom out and you will see deflation everywhere. And if there is one thing you do not want during deflation it is debt.

That’s odd - Jenee just informed me this morning that “Inflation is picking up around the world”.

I’ll coin a new term “Interest rate targeting”, The adjustment of CPI or inflation to justify sufficiently low interest rates such that the Auckland housing market doesn’t implode.

Weird huh. RBNZ been predicting inflation just around the corner for years now, and when it looks like they may finally be right, they change their mind and decide there isn't going to be any inflation. Minimum wage going up to $20/hr, public sector wage rises, surely this has to increase inflation? If not then they may as well keep raising them!

Now this is what I’m talking about. I forgot about the minimum wage. And don’t forget the recent pay equity deal for support workers has a relativity clause.

A good amount of macroeconomic data still suggests inflation is just around the corner:

- The business price index data from Stats NZ clearly states that cost pressures have been running at elevated levels for several quarters but haven't found their way into CPI.

- Our capacity utilization is also just 0.8pp below the record high level.

- Median wages have grown at 3.9% annualized rate since 2014 (unadjusted for inflation).

I think Orr's pessimism stems from reduced discretionary spending in the near future. Tightening across major money markets and a cooling NZ economy will put upward pressure on debt servicing costs and downward pressure on wages respectively.

https://www.stats.govt.nz/information-releases/business-price-indexes-j…

https://tradingeconomics.com/new-zealand/capacity-utilization

Hardly, I think you make a very valid point, Inflation in NZ could finally arrive. I have been going against the majority calls that the OCR is about to rise for the last 3 years, maybe it's time go against the new majority calls that the OCR could fall?

Also while I am asking questions. Why are floating interest rates so high? I’m no expert but I assumed fixed rates were set based on external factors ie cost of bringing in funding for a fixed terms and floating would reflect OCR and domestic costs. But OCR apparently trending down and already very low but floating rates are very high. Am I right in ensuring floating rates are explained solely by banks milking customers since they know we are choosing our bank based on fixed rates?

I think they want to lock you into a fixed rate. If you are floating it is much easier to change banks.

True, but wouldn’t there be a niche for charging a competitive floating rate? I mean if the the floating rate is almost 6% and the fixed rate for one year is 4% and the OCR is what? 1.75%? Surely any competitive market would have a lower floating rate?

Yes you are right, any competitive market would have a lower rate!

I guess there is also the risk factor. They probably get most of their funding on terms, if they lend it out floating then they are taking rate change risks.

ANZ Australia Interest rates offer currently.

Simplicity PLUS Home Loan (Principal and Interest) (LVR < 80%) (New Customer)

3.65% Variable

So their cash rate is 1.5% and they have floating rates at 3.65% and we have a cash rate of 1.75% and our floating rates are ~6%. What gives?

Stagflation is here. Hard to stop.

The issue for RBNZ is they have this mandate (obligation) to control CPI but only a very limited range of policy tools to do so. Government (both sides of the house) need to also take a lead here and help restructure New Zealand economy.

So the suggestion of a recovery in the NZ dollar to US 70 cents, made in an earlier article, would appear to be a very unlikely result if the banks are now chiming that they think rates will get cut.. But on the other hand they do desperately need more debt issued to fill the void left by the removal of foreign cash into the housing market. I wonder when the market will wake up to the reality that without that injection of capital and its subsequent flow through the housing market in every region that the 'real value' of property could be as much as 50% off?

The decade of low interest rates have pushed consumption out far enough. Like buying an over priced car with a "committed" 10 year lease. In other words, people are committed to high debt for a very long time and have very little left for additional expenditures or savings. Cutting rates won't help. Immediate effects could possibly come from tax cuts and wage inflation. Just look at the US....cutting rates did nothing but increase asset prices over the last decade. However, the "Trump" tax cuts pushed GDP to 4.% in the last quarter.

Any lower on the OCR and its a sign those dark clouds on the horizon are getting closer. Problem is there is nothing left to cut and the banks will not pass on the cuts to the same degree and it could get to the point pretty quickly where they ignore the cuts altogether. I have a bad feeling about whats coming and I'm not a DGM.

I fail to see why the mortgage rates can not be the same as in the UK at 2.5%. Thus said two days ago their central bank put interest rates up. I am paying off as much principle I can manage while the rates are low. When things move they move faster than anyone can catch them.

Housework’s, yes I did buy the property!

I was the only bidder on it.

Bid on a couple of others that I hadn’t seen, but didn’t get them, even though I was the only bidder on them, but owners wanted more.

I don’t pay anymore than I want or need to.

Let’s blow more air into the asset bubbles eh?, who cares about savers, thrift, and real economics.

When did we let central bankers have so much power? And where is the counterbalance? Politicians?, media?

Joe public who is not taught the basics about money in school?

Surely from time to time bad investment decisions just need to be cleared, house prices fall failing businesses end, we get back to sound money, sound policy. It called the “life cycle”. Let it cycle within limits of course.

I never found a 2% inflation target in my Finance textbooks? What’s that really all about “ I’m not going to buy

$1000 fridge because I’m waiting for that to be worth $980 next year if we have 2% deflation;Really?

Can someone explain why we accept all this stuff ?

Let interest rates revert to the mean, implement sound money policy , get real price discovery on assets, safety net for the real disadvantaged, get Government spending under control, reduce deficits, live within our means , Govt not higjacked by interest groups, Like Iceland let Bankers be imprisond for fraud, theft, let’s get back to before the world went mad

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.