Talking ourselves into a funk?

The economy heading for 'stall speed'?

Falling expectations of inflation pointing to a need for further stimulus from the Reserve Bank?

Yep, there's plenty on the minds of the big bank economists this week as they view faltering global and domestic economic situations.

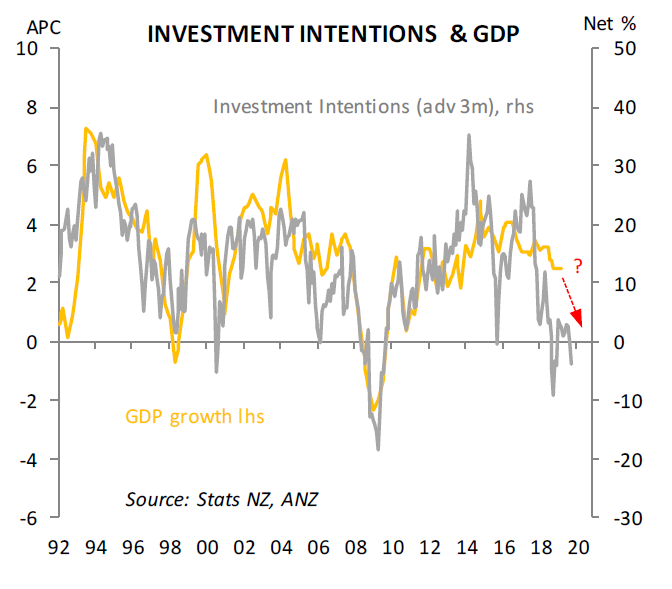

A powerful backdrop to the week ahead has been provided by the latest ANZ Business Outlook Survey, which was released late last week and showed business confidence levels and investment and employment intentions sagging to levels last seen at the height of the Global Financial Crisis.

The question of whether we are talking ourselves into a funk is directly raised by Kiwibank chief economist Jarrod Kerr and senior economist Jeremy Couchman.

"A lack of confidence among NZ firms has become a primary concern for the NZ economy," Kerr and Couchman said.

"Investment intentions are down, hiring intentions are down, and even firms' expected profitability was down [in the ANZ survey]."

The two economists also honed in on the ANZ survey's 1-year ahead inflation expectations measure, which fell to 1.7%, considerably adrift of the explicit 2% inflation target the Reserve Bank has.

"This is a worrying development for the RBNZ, with their own survey measure of inflation expectations falling sharply below the Bank's 2% target midpoint.

"If expectations become unanchored below the mid-point, the likelihood of further significant policy action by the RBNZ increases," Kerr and Couchman said.

They noted that financial market pricing had responded and there were now a little over 40bps of further interest rate cuts priced into market prices.

ASB senior economist Mike Jones noted, in relation to the ANZ survey, that NZ firms were "seeing an increasing risk the economy hits stall speed".

"We still think this outcome will be avoided given the support from a humming construction sector and the high terms of trade," Jones said.

"Still, the risks of a more protracted slowdown are rising."

It was hard to find "any cheer" in the ANZ survey, Jones said.

"Despite the encouragement from the RBNZ Governor [Adrian Orr], firms just don’t believe it’s a good time to invest.

"Who could blame them given the global gloom and signs of a turning in NZ’s economic cycle. As the chart [above] shows, the level of investment intentions suggests NZ economic activity is at risk of stalling.

"Our forecasts of a 2.5% [year-on-year] 2019 calendar year expansion look a tad lofty."

Westpac economists also felt the fall in businesses' inflation expectations was very important.

"Inflation expectations are a significant influence on how businesses adjust wages and prices, and as a result play a key role in determining actual inflation. The recent downshift in expectations means that the uphill battle the RBNZ has been fighting to generate a sustained lift in inflation has now gotten that much harder," they said

They noted that the next update on the RBNZ’s Survey of Expectations is due on 12 November.

"Although that’s just one day before the November [monetary] policy [and Official Cash Rate] decision, it’s important to remember that the RBNZ gets the results of this survey about a week before it’s released publicly.

"As a result, this survey could again have a big impact on the Monetary Policy Committees thinking, just as it did in August.

"This will certainly be a key event for markets to watch ahead of the November policy statement and could impact market pricing.

"We expect the RBNZ will cut the cash rate by 25bps in November, taking it to a fresh record low of 0.75%."

25 Comments

It's the job of bank economists to be 'optimistic' ( optimism being in the eye of the beholder, of course) and as a result, all of the above calls by the collective are still overly 'optimistic' no matter how cautious they appear. True optimism; optimism that the domestic economy is about to rebalance itself away from speculative hope towards productive endeavour is not far away. But the bank economists won't either write or like that, will they!

(NB: Perhaps the Aussies have beaten us to it again? "Brace for Aussie GDP wipe out")

There's still sufficient downside in the OCR for the RBNZ to play with.

And, of course, the current situation is exactly what a low OCR is designed to deal with.

The economy is being well-managed by a very capable and experienced RBNZ Governor - supported by a group of very talented professional staff - including economic, financial and legal brains.

TTP

It's funny how you only see the downside in OCR, but not the market that the OCR policy is failing to stimulate.

An economy is not “run” by any bank governor or government. It is after all Supposed to be a “free” market. Recession avoidance or attempting such by encouraging more debt is not a reflection of a proper capitalist business cycle. That cycle has to be curtailed precisely because world banks have been engaged in game called extend and pretend since 2008. That and avoiding marking to market in accounting maintains calm facade. Not much time now before the facade is again ripped away

"There's still sufficient downside in the OCR for the RBNZ to play with. And, of course, the current situation is exactly what a low OCR is designed to deal with."

Really!!!!!

And how are we going to deal with the next GFC ????

Therein lies where I think where the party will end for NZ and Aus.

The property market might just escape a crash this time, but it won't next time.

My pick is a crash sometime between 2022-2025.

Hi Fritz, can you please expand on 2022-2025 thoughts?

Exactly, with an OBR

The book by Akerlof and Shiller (Animal Spirits: How Human Psychology Drives the Economy) sums up well what we're seeing. But its not new.

Is it agreeable that our business owners are actually now the doom and gloom merchants within the new zealand economy - and not the left leaning hippies that have been labelled the DGM's for the last few years on this site?

The fact that 'doom and gloom merchants' is in the common vernacular is a perfect illustration of Shiller's work.

Yeah. It's a brilliant book.

The OneRoof supplement did a great job today to whip up more animal spirits frenzy. They cynically tried to give it a veneer of balance...

'Humming construction sector' the past few confidence surveys wouldn't support that.

Don't be fooled by all the cranes on the skyline. Those projects kicked off years ago.

Almost all of these bank economists have no idea.

It makes you question why bank economists are allowed to make public statements about expectations - because they are always good, regardless of how bad the outlook is. Snake oil salesman might be a more appropriate job description.

Yeah.

I do think the Kiwibank economist is quite good, however.

Yes. Those boys at kiwibank wrote a nice report back in February on the likelyhood of the NZ$ slipping into the "low fifties" against the US$ as a result of aggressive rate cutting here. In February we were 0.675 and higher and six months later we're trying hard to maintain buying power of 0.63. Adrian Orr looks like he's going to take the NZ$ - US$ right to Jarrod Kerr's target.

We move in unknown territory. All that economists didn't know, what negative interest rates were 5 years ago. Just like water running up a hill. They better sack the economist and pay the shareholders a bit more. Fasten your seatbelt and hold on. It's going to be a bumpy ride.

Generally, economists are dangerous. In our 21st century 'rationalist' view of the world, we put a lot of stock in science. Economists are granted quasi- scientific status, but the problem is that economics is pseudo-science.

At best, the work they do is educated guesswork. The problem is, the 'educated' bit is flawed....

Fritz, predicting any specific outcome in a system with so many known and unknown variables is extremely complex, and in all likelihoods extremely inaccurate. Weather forecast is a very good example. I would not call the science underpinning weather forecasting pseudo, because it does not get the outcome with any accuracy for anything more than 3 days ahead.

I guess the economists need to be a lot more humble about how they talk (as whatever they say is "assuming" so many things) but I would not call them pseudo because they do not get it right.

Now, if you are questioning credibility of predictions that favor an outcome for the person who pays the predictor, that is something completely different and can be true in any field, scientific or otherwise. And funny enough, to explain this phenomenon you will need economic theories

Good points, and I was probably being a bit harsh. There are also some good economists.

My comment was probably unduly influenced by the high prevalence of shoddy economic analysis, especially from those we typically hear the most from...

But I shouldn't taint the whole discipline with the shoddy majority.

"Quasi-science"- couldnt have put it better myself. No one can see the future

Falling expectations of inflation pointing to a need for further stimulus from the Reserve Bank?

Repeating the need for further "stimulus" wont resolve the fact that cutting interest rates and engaging in QE type assets swaps with banks doesn't make the latter's shareholders authorise their employess to extend copious credit beyond those with pristine credit scores and unencumbered collateral. In fact:

The reason the bond market isn’t pricing in a resulting burst of inflation is because the banks buying the balance sheet tools in the bond market (and maybe gold, too) know from experience and practice central banks are incapable of creating inflation. That much has been fully established by the last twelve years. The fact that central bankers don’t know it yet further strengthens the case; they’ll try and simply repeat the same failures even if they go full BoJ QQE shock and awe. Link

{kind=link}

Is this better than being overly optimistic and selling products with higher risks built in, as happened last time, triggering the GFC ?

Anyways, now that we have all agreed that recession/deflation is going to happen in the near future and monetary policy is not working, I say, time for the helicopter drop of money directly to consumers. Let the recovery start...

D-E-F-L-A-T-I-O-N .........I have been banging on about his for almost 2 years and I dont know when Mr Orr intends to state this in clear unequivocal terms , so everyone of us is clear as to the problem .

Its like the alcoholic who will not face reality .

We are in a delfationary cycle , and Ben Bernanke ( remember him ?) and the Federal Reserve are to blame for sowing the seeds of this poisonous plant .

QE money printing and zero interest rates was never going to end well .

These policies damaged one of the four factors of production , and things are out of balance

During the GFC Banks should have been allowed to fail , the debts of greedy banks everywhere from Ireland to Greece and Iceland should never have been passed on to the populace .

Now we have gone through over a decade of one of four the key factors of production having been reduced in value to almost zero , and if you need any evidence of what happens when you destroy the value of one of them look at this :-

4 FACTORS OF PRODUCTION

Damage or destroy the intrinsic value of any one of them and it will not end well .

LAND :- Ask Zimbabwe what happened when the value of farmland was reduced to zero by confiscation , it leads to horrors they are still grappling with 20 years on

ENTREPRENUERSHIP :- Ask Russia or Cuba or North Korea what happened when entreprenuership was destroyed .

CAPITAL : - Ask Japan what happened when the value of capital was reduced to zero through zero interest rates .

LABOUR :- Ask anyone in an unequal society what happens when you fail recognize the value of labour and fail to pay workers a fair wage It leads to crime , dysfunction and social disorder, among other ills .

We are dealing with the consequences of this QE - easing - printing - zero interest rate folly , and its time to call it out .

Well put. Although, what Bernanke, Paulson, Geithner all did at that time and afterwards rescued the USA, at a long lasting damage to the rest of the world. The USA has had a comfortable recovery, though the ordinary person has not benefited much. It is the Buffets who have gained the 99% of the meal, pun not intended. Trump is also a beneficiary of the more dominance the USA has got since then into the world economy. It is countries like Australia, New Zealand which are facing a delayed reaction and this time around the damage to us may turn out to me lot bigger and irreparable ?

The sag in confidence is unremarkable - it would have been truly heroic and Remarkable if all was said to be Sweetness and Light. Consider a small selection of headwinds:

- Urban environmental discontents projected outwards onto agriculture, ostensibly because of 'pollution' and other externalities but revealing much dissonance: urbanites 'pollute' their environment but there are more of them.... Ag is a large chunk of exports, Fonterra a large chunk of that, and while much of F's quandary is self-inflicted, the Ag sector as a whole is not gonna stick its head above the parapet and Invest, unless it's for its own survival.

- Oil and gas goneburger: and the Gubmint has shown that, with no warning and less analysis, it could happen to another sector overnight. Long-haul air travel is a likely target: another major export earner. Because reasons.

- Minimum and Living Wage movements: both directly increase input costs for the lower end of SME's, who are least well placed to absorb them nor to increase prices to compensate. No mention of a Living Wage for the hapless proprietors, they're Kulaks and deserve everything they get....

Unlike an exchange rate movement or a tariff, investment cannot be jawboned into existence. It's pushing on a string. But it does work the other way, only too well: strings do work in tension, so Investment is easy to destroy, displace or mute......

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.