By Roger J Kerr*

The headline for last week’s commentary piece was that the Kiwi dollar had stopped depreciating at 0.6500, however a positive was needed to turn the sentiment around and start a recovery against the USD.

The NZ GDP growth numbers for the June quarter (not the Government financial accounts Jacinda!) provided that turnaround catalyst, with a stellar 1.00% expansion and the Kiwi rocketed up over one cent to 0.6700 as a consequence.

There will always be a significant reaction in the currency markets to economic performance numbers that are so far above prior expectations (consensus forecasts beforehand were around +0.70%).

What was particularly encouraging from the detail of the GDP figures was that the growth was across the board of nearly all industry sectors, services being a standout lift.

There were no major one-off variables or inventory increases that could reverse out next quarter.

The continuation of the strong GDP growth performance in 2018 does not necessarily make a mockery of the very pessimistic business confidence surveys. The uncertainties that business folk are reflecting in answering the survey questions on the general economy and their own business outlook is all about Government-signalled changes to taxation and collective workplace wage/conditions agreements in the future.

The reality is that low business confidence results mostly influence business investment decisions and if investment/output eventually reduces, GDP growth will slow up.

However, these changes do not happen overnight and it may take until 2019 for the economy to slow if the business sentiment remains so negative. The ball is in the Labour Coalition Government’s court to restore the relationship with and confidence of the business sector by watering down some of these signposted and extreme economic policy shifts.

The ball is also firmly in the court of the RBNZ to re-examine rather closely their economic forecasting model as their GDP growth forecast for the June quarter (+0.50%) was precisely half the actual outcome!

A continuing positive for the Kiwi dollar from the stronger than expected GDP growth result will be a revision upwards in the RBNZ’s inflation forecasts for the next 18 months.

It will be interesting to see if Governor Adrian Orr changes his wording or inferences in this week’s OCR review statement. It is positive for the Kiwi dollar if the RBNZ are forced by the stronger economic data to increase their inflation forecasts and bring forward the timing of the first OCR increase (having just pushed it out further a month ago).

The Reserve Bank of Australia are stating that their next OCR move will be upwards. In contrast, the RBNZ appears to be giving equal waiting to a move up and a move down.

Given the the positive momentum in the rural economy right now (forestry, fishing, dairy, beef, sheepmeat, horticulture, wine and Aucklanders selling up their houses and shifting south), there is a real risk that the RBNZ have made a misjudgement on the economy and inflation. Therefore, sometime before the end of 2018 they will be forced to change their tune.

It is not unreasonable to expect to see the Kiwi dollar appreciating another two cents just on the back of this potential RBNZ flip-flop alone.

CPI inflation numbers for the September and December quarters, released in mid-October and mid-January respectively, will be key indicators as to how the lower currency value, higher wage settlements, higher fuel prices and less imported deflation are transferring through into general inflation.

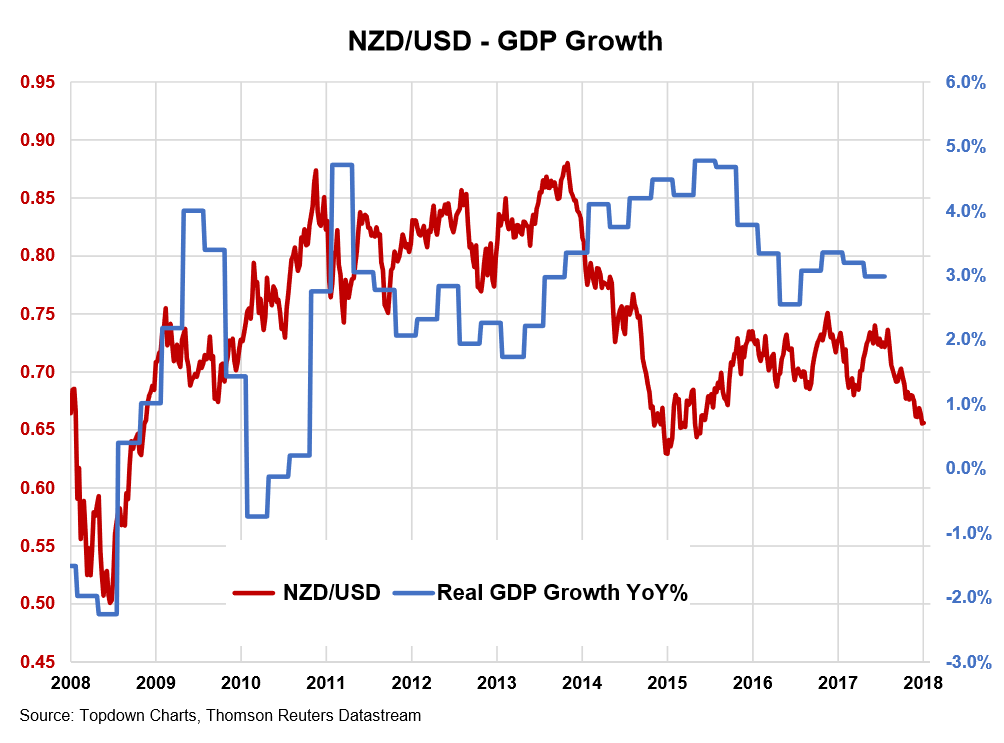

Whilst not a perfect correlation between NZ GDP growth and the NZD/USD exchange rate, the chart below does support the view that the Kiwi dollar at 0.6700 against the USD would still have to be considered undervalued on economic fundamental grounds.

The loose correlation broke down in 2014/2015 when dairy prices collapsed and the Kiwi dollar went down as GDP growth increased due to other industry sectors going gangbusters and compensated out the dairy downturn.

The outstanding GDP growth number will also act as a catalyst to prompt the offshore speculators to reverse their weighty “short-sold NZD” positions and take their profits before the Kiwi rises any further and those profits are eroded away. The speculators will be the Kiwi dollar buyers that send it higher over coming weeks.

Adding to the NZ dollar’s turn-around in sentiment and direction is how the global financial and investment markets are now interpreting the escalating trade war between China and the US.

Up until last week, the FX markets reaction to an increase in tariffs and tensions was to buy the USD against the Euro. However, a change has occurred with the USD weakening over this last week to nearly $1.1800 against the Euro, even though President Trump upped the ante on the Chinese with more tariffs and the Chinese cancelled planned trade talks.

My reading of this change in treatment by the FX markets is that they have now realised that a full-out trade war is not good for the US economy and thus not a USD positive.

Any slowdown in US economic growth in 2019 as a result of Trump’s tariffs will make his Government’s budget deficit even larger than what it is already going to balloon out to (6% to 7% of GDP). Thus a very large negative for the US dollar’s value. Potential political risk for Trump surrounding the November mid-term elections in the US is also a US dollar negative factor coming up.

The forward looking scenario I expect for the NZD/USD over the next 12 months is a stronger Kiwi to 0.7000/0.7200 on a weaker USD, RBNZ stance shift and re-alignment with the higher commodity prices over the next six to nine months. After that, there is a risk of a pull-back to marginally below 0.7000 on a major global share market correction downwards and the “risk-off” investor sentiment is always something that pushes the Kiwi dollar down.

USD importers should continue to hold-off on any new hedging and allow hedged positions to reduce to policy minimums. USD exporters should now be forward hedged to the hilt of their policy maximums.

Daily exchange rates

Select chart tabs

*Roger J Kerr is an independent treasury Management advisor. He has written commentaries on the NZ Dollar since 1981.

28 Comments

Always think its worth offering an alternative position. There has and will be a short lived NZ rally on 3 month old GDP numbers last week. Reserve bank may talk of raising rates on Thursday, but can't as their 0.5% prediction is a quarter early in assumption. Raise rates now, dollar will strengthen a touch but bury the economy because of impact on housing so there are bigger falls down the line as Fed and other banks tighten between now and the end of the year. Lowering rate option is now pretty much off the table so there is no point in him mentioning that this week. Rate rises will be before the end of next year (Q3) and will be stepper and faster. Debt junkies have 6-9 months to get their houses and finances in order.

Relief rally to 68.5C-69C before final quarter correction below 62 (which will be magnified by September quarter GDP at the end of the year taking NZ dollar below 60C by January 1st).

More inflation for many until middle of next year.

The 6-7% NZD fall we had during the June quarter gave a boost to exporter (farming) incomes. But the hangover is coming... Inflation lags currency moves by about 2-3months so september quarter inflation will be sharply up and GDP result will be hammered by that high inflation. As a nation that imports far more than we export, and with little ability to increase agricultural capacity, we will be hurt more than we benefit by the currency falling.

And I know next to nothing about farming, but I'm guessing that farming input costs are at the lowest point in the wet part of the year. Ground too wet to do much, so fertiliser, fuel and other input costs are low, hiking back up as the ground dries out and you can do work about the farm. Unless buying supplementary feed is a big winter expense?

@Foyle That is a very short sighted view of exchange rates. You dont want to import more than you export and a declining currency will support a better balance of trade.

Re trade imbalance: Thank you captain obvious.

As for NZD falling helping our economy: About 70% of NZ exports are Primary products which in these Green-dominated times we have little capacity to increase, and for which we take a price set by international competition. Dropping NZD doesn't help that. Non food and beverage manufactured exports (not reliant on and limited by primary production) account for about $10billion or 15% of our exports. That is the one tiny sector that might get a boost, though will soon be nobbled by the large rises in min wage (and flow on through economy)

Most of our primary products are sold in US $, so a declining NZ$ increases returns in NZ dollar terms, which is helpful.

Simply the result of Labour's increased welfare handouts. Its not productive growth, just beneficiaries spending up large thanks to Jacinda's largesse.

Over 60% of NZ's beneficiary budget goes on the pension, regardless of need. National were not going to do anything about that non-needs-based handout. And they were electioneering on increasing Working for Families and the Accommodation Supplement too.

Facts, schmacts.

60% to the pension? I wonder why that is necessary? Lack of provision during their working life perhaps - or too many with an overhang of debt?

https://www.stuff.co.nz/business/money/72598973/A-third-of-Kiwis-will-h…

Kind of explains the gambling addiction of the past few years if there are too many approaching retirement with inadequate provision, that lure of untold capital gains must have been a big temptation to top up funds.

Standing on one's own two feet is a model for others to follow, not oneself?

Aversion to socialism, a preference for libertarianism etc...very loosely held values, too often.

Very dangerous when you place a nations financial future in the hands of a generation who won't be around to see the wreckage.

reminds me a little of John from Bricks and Slaughter Part 2. Short termism by the banks and the boomers!

The best bit is at 2 minutes 56 where it pans across what looks like a letter to ANZ disputing the change to P & I.

Dear ANZ

The above Loan Accounts have been interest only, which on 17th November reverted to Principal and Interest.

This is a significant increase of our loan repayments from $5700/mth to (illegible) .

If he was paying $5700 per month interest only he's borrowed $1.5 - $1.8 million in mortgages at age 60 - 70. I like how he's calling it an increase to his "loan repayments". Buddy, you aint repaying anything on interest only!

This is a significant increase of our loan repayments from $5700/mth to (illegible) .

I reckon its $8985/month. 57% increase. Ouchies, that'll leave pucker marks on the office chair.

He was probably the sort of landlord who looked down his nose at his serf tenants. Guess they’ll be having the last laugh as they put in a cheeky lowball bid on the property they’re renting.

Heh, and doing everything they can to keep the place looking shitty for the open homes before the mortagee sale to keep the price down. Broken holden on the lawn with grass growing thru the open bonnet always helps.

It’s always interesting to examine what the main contributors to GDP in NZ are.

For the June 2018 quarter the largest contributor to GDP was “Rental, hiring, and real estate services” at 12.8% of GDP. Second largest was “Prof, scientific, technical, admin, and support” at 10.4% of GDP, with “Manufacturing” third largest at 9.7%. “Agriculture, forestry, and fishing” was a distant ninth at 5.3% of GDP.

Clearly shows that our economy runs on us renting out property to each other, with a few farmers producing a bit of milk on the sideline.

Well done Oscar.

Now, for everyone else, consider that 1/3 of all business lending in NZ is actually to the property sector then our debt allocation is producing an absolutely abysmal rate of return. Add the $260 billion of actual debt to households and you have an economy built with no foundations. Unless resources are re-allocated into the productive sector then housing (and it's debt) will collapse the economy.

Why? Like at what level does that occur and how long does it take to happen?

KW,

I often disagree with Roger Kerr, but he is correct in saying that the growth was across nearly all industries,giving the lie to you absurd and highly biased comment.

Of course,if you have any evidence to support your view,I would love to see it.

Spending by households (about 60 percent of GDE) rose 1.0 percent this quarter.

Investment in fixed assets fell 0.1 percent

Exports of goods and services was up 2.4 percent. Imports of goods and services rose 1.5 percent. (note: this can be accounted for by the fall in the NZ$ not increased production)

So household spending drove growth - and since wages didnt go up, where do you think the money came from?

A rising interest rates and high inflation environment forces a replacement of speculative investing with value-seeking as traders exit long positions in over-levered and underperforming businesses, in search for businesses capable of doing more with less. As asset price appreciation tends to fade out, markets actively seek safer investments in growth assets such as infrastructure, healthcare and technology etc. for income returns.

https://www.marketwatch.com/story/value-stocks-may-break-out-helped-by-…

Why so much focus on the Kiwi $ fundamentals side of the exchange rate rather than the USD? Every dollar of QT is a dollar destroyed, while most other central banks are still in QE. Every reduction in US trade deficit is a dollar removed from Eurodollar supply. The Fed rate and the NZ OCR are on par for the first time in maybe 30 years and could soon have a differential in favour of the US. There is a strong case for a strengthening of the USD in the short term, it's the only game in town. We are still a banana republic with a commie at the helm.

I'm thinking most of the GDP leap came from the internal economy, maybe driven by high prices for avocados and flat whites and removal companies frantically shuttling tenants to their next fixed tenacy? I can't see the export sector being responsible for much as it tends to ship everything out at the lowest cost with little or no value added. If its a wet spring avo's will be pricey so I pick GDP to stay high into the new year!

4th time lucky?

His articles tend to be at interesting changes in the short-term movement. His last article was at the recent low, and we did bounce upwards a little bit. I noted at the time that I was expecting to see a bit of a climb, followed by yet another lower high that will be followed by yet another lower low. The NZD has lost almost 1% since the lower high of a few days ago. We shall see whether his July prediction of a return to 0.7 - 0.72 will eventuate before my expectations of 0.60. To date, the trend is still downward. His articles tend to mark short term lows with a few days of rebound following before the declining trend resumes. Eventually he will call the turn correctly. Reviewing his predictions as shown in his articles on interest.co.nz, he hasn't been correct on the currency change for quite a few months (other than very short term variations).

Yeah but the thing he and everyone else except the reserve bank are missing, is that GDP is so uniformly up across all industries, because the NZD is down 11%. Falling currencies support nominal GDP. Sorry to say but the economy is “growing” because the currency it’s priced in is devaluing.

NZ still has a substantive current account deficit and typically GDP growth boosts imports, which worsens the the current account deficit, which should put downwards pressure on the NZ$, other things being equal.

Yeah but the thing he and everyone else except the reserve bank are missing, is that GDP is so uniformly up across all industries, because the NZD is down 11%. Falling currencies support nominal GDP. Sorry to say but the economy is “growing” because the currency it’s priced in is devaluing.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.