Inflation has rocketed to its highest level in over 10 years, with the annual figure reaching 4.9% at the end of the September quarter.

That's far higher than economists were picking - even though they expected the figure to be a big one.

And it's more than the Reserve Bank (RBNZ) was expecting. It forecast 4.1%.

Wholesale interest rates rose sharply, with the two-year swap rate rising by 10 basis points, while the Kiwi dollar climbed to nearly US71c.

While the latest annual inflation figure is officially the highest in 10 years the figures back in 2011 were affected by the last GST increase.

Before that you have to go back to 2008 for the last time inflation was 'naturally' at this sort of level - exactly 13 years. (Inflation spiked to 5.1% in September 2008 before dropping rapidly as the worst of the Global Financial Crisis hit.)

The annual inflation figure in the quarter ended June 2021 was 3.3%, which was itself a fast rise from the previous quarter figure.

The RBNZ targets inflation between 1% and 3% with a specific focus on achieving 2%.

Having delayed raising the Official Cash Rate in August due to the oubreak of Covid Delta, the RBNZ earlier this month made its move and increased the OCR to 0.5% from 0.25%.

Even though the country - and particularly Auckland - remains hamstrung by the Delta outbreak, the latest inflation figures would appear to make it certain that the RBNZ will be forced to hike rates again - probably to 0.75% when it next reviews them on November 24.

Ben Udy, Australia & New Zealand economist with Capital Economics said the strength in inflation over the last six months means it is unlikely to fall back into the RBNZ’s 1-3% target until the end of next year.

"We had already expected the RBNZ to continue hiking rates despite the Auckland lockdown. But the strength in consumer prices in Q3 will surely nudge the Bank towards an even more aggressive hiking cycle," he said.

ASB senior economist Mark Smith said the widespread nature of price increases was "not a comforting sign".

"If it were not for the Delta variant outbreak, the pace of OCR hikes being implemented by the RBNZ would potentially be quicker than 25bp increments," Smith said.

"As it is we still expect ‘considered steps’ from the RBNZ, with 25bp hikes in November and February 2022, with the OCR hitting 1.50% by the end of next year.

"The speed and magnitude of subsequent OCR moves remains conditional on a range of factors, including the degree of economic scarring caused by restrictions to contain the Delta outbreak and whether inflation expectations and other inflation anchors are consistent with the 1-3% medium-term target - or become unstuck."

Statistics New Zealand said the consumers price index rose 2.2% in the September 2021 quarter, the biggest quarterly movement since a 2.3% rise in the December 2010 quarter.

Excluding quarters impacted by increases to GST rates, the September quarter movement was the highest since the June 1987 quarter, which saw a 3.3% rise.

Annual inflation was 4.9% in the September 2021 quarter when compared with the September 2020 quarter. This was the biggest annual movement since inflation reached 5.3% between the June 2010 and June 2011 quarters.

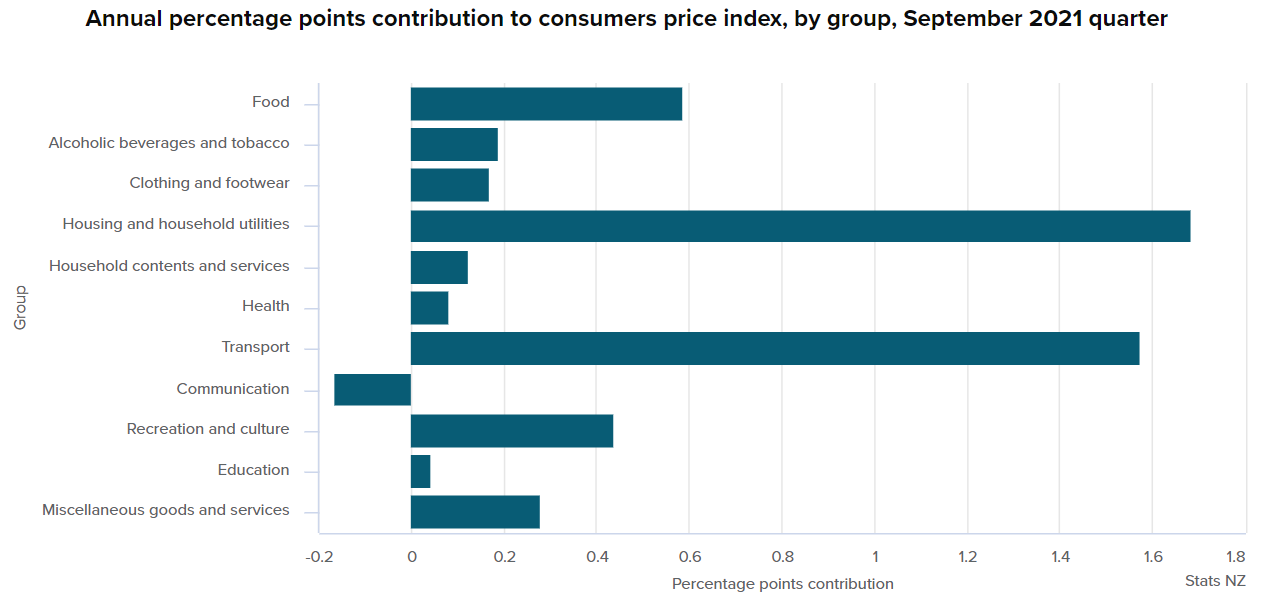

The quarterly price rises were widespread, with 10 of the 11 main groups in the CPI basket (such as food and transport) increasing in the September 2021 quarter compared with the June 2021 quarter.

The main drivers were housing-related costs, such as construction of new houses and local authority rates.

Prices for construction of new houses were up 4.5% for the quarter, and 12% for the year.

“Both supply-chain challenges and high demand are pushing up the cost of building houses,” Stats NZ's consumer prices manager Aaron Beck said.

“Construction firms reported that it is hard to get many materials needed to build a house, and that there are higher labour and administration costs.”

Local authority rates and payments rose 7.1% in the September 2021 quarter. This was higher than the 3.1% rise in the September 2020 quarter.

“Many councils set smaller than usual rate increases in 2020 to alleviate cost pressures on rate payers due to COVID-19,” Beck said.

“In 2021, councils faced increasing revenue and cost pressures.”

Rates are captured once a year in the September quarter, as this is when ratepayers see price changes set by councils.

Vegetable prices rose 19%, making it the second largest upwards contributor to inflation. This was influenced by higher prices for tomatoes, lettuce, and broccoli.

Transport prices rose 4.2% in the September 2021 quarter, due to higher prices for petrol, as well as international and domestic airfares.

Petrol prices rose 6.5% in the quarter and 22% for the year. The annual increase is the highest since the September 2007 quarter to 2008 quarter.

Global fuel prices fell over early 2020 as the COVID-19 pandemic took hold. Overall, global fuel prices have risen steadily since then.

The weighted average price of a litre of 91 octane petrol was $2.27 over the quarter, up from $2.13 in the June 2021 quarter, and $1.86 in the September 2020 quarter.

Consumer prices index

Select chart tabs

190 Comments

Annual inflation was 4.9% in the September 2021 quarter when compared with the September 2020 quarter. This was the biggest annual movement since inflation reached 5.3% between the June 2010 and June 2011 quarters.

If I'm not mistaken, the spike in inflation between June 2010-11 was due to the GST hike, so was in a sense Government-mandated inflation.

It would be good to check prior to this time as to when inflation was last over 4.9%, I wonder how far back one has to look?

Check the PTA. All inflation is government-mandated inflation. We require RBNZ to shrink the purchasing power of our earnings but the government does not increase their tax brackets by inflation. It is a con.

FYI for anyone who's interested, the CPI was at an annual rate of 5.1% in Sept 2008. One year later (Sept 2009) it was at an annual rate of 1.7%. Does anyone thing we'll have a similar dramatic drop in the annual rate this time?!

You just never know!

What caused that drop?

"The 2008 stock market crash took place on Sept. 29, 2008. Easy credit and raising home prices resulted in a speculative real estate bubble. While the market crashed in 2008, the problem started years earlier. The stock market crash of 2008 was the biggest single-day points drop in history up to that point. "

Can we out-do 2008? Time (and most probably what happens in China) will tell....

Indeed !

And according to one local outlet :

"Cost of living soars: Biggest inflation surge since 1987"

October 19th 1987.... Now, let me think...

Indeed again (see me post below at 11:28)

>"The stock market crash of 2008 was the biggest single-day points drop in history up to that point. "

Yawn, biggest nominal value fall in an index which(almost) constantly increases. 29Sept2008 doesn't even make the top 10 in % falls on the S&P now, nor did it make the top 5 when it happened.

Interesting. Wonder how that magic trick was pulled-off?

We know house prices, which went down a bit, do not form part of the CPI calculation. So what in partucular caused this huge reversal?

(See above) People who've gone broke or lost what their spreadsheet told them their net worth was, stop spending.

Perhaps deflation when banks stop creating credit.

The June 1987 quarter, which saw a 3.3% rise.

I was asking about the annual increase, not quarterly.

Time for the RBNZ to be courageous and lift rates by 2-3% to reduce inflation in accordance with their mandate?

Orr is this inflation just transitory?

https://i.stuff.co.nz/business/opinion-analysis/300098412/adrian-orr-ba…

I agree. The RBNZ should aggressively and urgently raise rates, NOW.

I think that it must, at the very least, increase the OCR by 75 bps next months, and also raise the OCR to 4% at least, by mid next year at the very latest. An OCR that is not over-stimulatory should not be far from the inflation rate - so the current level of the OCR should be already at 3%, at least.

CPI was under target for a long time so why not let it run high for a while to balance out over the long term?

Unfortunately Orr cannot change OCR in isolation. Has to watch what's happening overseas. Probable outcome of raising too quickly and too high compared with overseas cash rates is massive carry trade pushing NZD above 0.75cUSD/NZD. Some would say that's not a bad thing.

Big increase in OCR would lead to economic carnage - think of what it will do to mortgage rates and all those first home buyers trying to make ends meet with the huge mortgages they've been forced to take out just to get onto the housing ladder to support their family. Firstly to their mortgage payments once their term rolls over and secondly to the value of their home.

And these people are more important than those who chose not to borrow and bid recklessly because?

Well, having shelter is a necessity, so I would say yes, it is just as important to consider than those that opted not to, or have already been able to pay down their mortgage significantly.

Brock, I'm of an age where a lot of people I know have bought houses recently (in the last year or so). Most of us have quite large mortgages. You might think it was reckless, but the problem is for people barrelling towards their forties watching house prices increase rapidly their entire adult lives, experiencing the instability of renting with a young family, and experiencing eye-watering rent increases year on year, it was reckless NOT to buy a home if you could possibly manage it.

Whether that will turn out to be the case remains to be seen. But I don't see why we should focus on trading off between recent first home buyers and the currently assent-less. Both groups have been massively screwed by decades of government policies that put them in an impossible position. Why the hell should either of them carry the can for rampant property speculation, nimbyism, and monetary policy that was largely in favour of older generations?

I'm of that age too.

FHBs pitted against their peers is one of the political tragedies of this situation. You're angry about the stupidity of house prices, and then feel forced to buy anyway, and then you're incentivised to keep the same system going and the people who should be your allies are your enemies.

It's always been obvious that it has to end though. At some point it becomes too, too ludicrous, and there always has to be a wave of FHBs who take the hit. Unless you think the trajectory we're on is sustainable, and the median house price should be $2m in 2026. Trying to stop that 'wealth' destruction from happening will destroy our society. Utterly annihilate any semblance of egalitarianism and turn our economy into a third-world joke. Is that worth it to save one wave of luckless investors, who could have done otherwise?

But why are the only two options that FHBs take a hit, or the assetless take the hit? Why, just for once, can't it be the people who both caused and massively benefited from asset inflation who take the hit? Tax the hell out of those who have made a fortune from property speculation and use that as a fund to subsidize first home buyers to keep their original equity position, or something. I just dont believe that there's no way to fix the problem except for kicking a significant subset of millennials in the face yet again.

You know, I would be all in favour of that. I'd be in favour of punitive taxation of third, fourth etc. properties. I think the situation is bad enough to merit blunt-force redistributive policies.

The country is still run by and for property owners though. Realistically that isn't going to happen unless under-40s start showing some political cojones that have never yet been in evidence.

Have a read of 'The 4th Turning' (or watch a few youtube videos)

If the theory plays out as the authors expect, we're now midway through that turning where millennials begin the rise to power within society with the 'grey champion' boomers on the decline. Gen X are the passive observers, unsure which side they should be following. They back the boomers for now as that is best for them in the immediate future, but as boomers leave the workforce and die off Gen X realise the power falls to the millennials so over the coming years a shift will be away from boomer centric policy (which is about self interested entitlement at the expense of social stability and the good of a civil society) and more towards millennial views that will be about social cooperation and building institutions that once again work for the good of the people and not the good of the few.

The turning started around 2008/09 and is likely to finish by the end of this decade. This type of cycle last occured in the 1930's and 1940's and culminated with Bretton Woods and the rise of the Greatest generation. The outcome was 'the high' which occured from 1946 through to the point where Kennedy was shot, and then we saw the boomers rise with their period of woke enlightment through the sixties and seventies. So boomers have essentially been the dominant force in society for the past 50 years or so, but their chickens are coming home to roost. How will they react?

You are correct. If the less that 40s dont show up and vote they will continue to be ignored. To focused on their phone and instaface etc...

Yeah so let's go hard on DTI rather than OCR.

So they get screwed on mortgage payment increases.

Or, they AND everyone else get screwed on the cost of... everything else.

THIS is why a housing bubble is so stupid. It's a Chinese finger trap. We'll have families (well, more of them) unable to afford food, and all the media tears will be about middle-class FHBs who've bought property at ridiculous prices and investors crying because they can't possibly be expected to ever *sell* a property, it's supposed to be an endless upward ladder...

This.

All thanks to a couple of generations of self interested kiwis and their political representatives.

Well, it will all come back to bite.

I'll say it again...OCR is way too low....should be about 5-6%. Crazy stuff.

The RBNZ must start aggressively and urgently raise rates, now. Not doing so would be reckless negligence.

Exactly. There mandate is to keep CPI in the 1-3%. They need to raise now or they are not doing there job.

Will we see Orr with egg on his face?

By their own admission, changes to the OCR take 9-18 months to be transmitted to the economy. The reckless negligence has already happened while they sat on their backsides did nothing for the entire past year.

Their clown chief economist has been giving very bad advice.

You are right, unfortunately.

Now the RBNZ will have to be very aggressive in tightening, and play a painful game of catch-up in trying to avoid the start of a wage-price spiral. It is also very important that they clearly communicate a new very hawkish attitude to monetary conditions, so to start influencing all medium and longer swap rates as soon as possible. Maybe, if the RBNZ start acting very aggressively now, there is the hope that things might not spiral completely out of control.

test

The incompetence of those we entrust with our future is outstanding.The whole of NZ just took a 4.9% pay cut while the reserve gives money to the banks at .25%.

Every NZr who bothers to do a household budget could have expressed this ever burgeoning outcome, over the last 18 months at least. Raising the OCR was a political black eye in the making. Now it’s too late. The cat was out of the bag and the horse out of the stable far too long ago.

Stagnation!

Here we come.

Do you mean stagflation?

Probably both!

Anyone trying to recruit currently will confirm that salaries to get the right candidates are rising sharply.

A real kick in the guts for wage earners and the asset less classes.

But will Labour acknowledge this?

Nah.

It's a kick in the guts for most home owners too - unless you're in a position to downsize or move to the regions, there's a high chance your next house is about to get more expensive faster than the value of your current one increases at.

Not only that, Councils will then jack up rates, which have now established a pattern of being ahead of inflation.

We are witnessing the final shots on the war on the disposable income of what is left of the middle class.

s a home and property owner I am happy to have a kick in the guts - we have not shared the same burden as the asset less class by a long shot.

My point is more that there is an increasingly smaller and smaller pool of actual winners out of the status quo.

"Move to the regions": I think that the window of opportunity for this strategy has now past or close to being past.

Looking at how much house prices have increased in the regions, I wonder at whether they are actually worth those dollars now.

And I a suspect that many people will find it quite hard to sell these places at a later date for what they paid for them if they decide to move again.

Thats if they want to move again. Some will not. They will stay where they have bought. They will be fine. But there are all sorts of reasons why people may want to move again. eg Get closer to a hospital, family, friends, warm temperatures etc.

Come on. Borders open. Loose immigration. Any drop in property value will be quickly tempered by the incoming horde!

Exactly. Labour is too preoccupied with meeting it's other target.

As I said before it gives a feeling as if we are living on moon & have to pay hefty amount for basic amenities..

Sad govt. failed to acknowledge it and take any action and always categorize it as transitory, but don't know how long they keep shifting the goal posts.

Yup, but don't expect the government to realise it any time soon - it would mean accepting that not adjusting PAYE rates for decades and increasing fuel excises and levies is actually causing economic harm to the people they supposedly care about.

Time to adjust tax thresholds?

Could be a double edged sword - give people more cash to compensate for rising cost of living, but then of itself could be inflationary...

The proposed English adjustments that were legislated prior to the 2017 election did exactly that. Labour reversed them.

..um no. That's just another way of taking more out of our pockets. Time to stop robbing us all via inflation.

Inflation is TAX. It's just easier for the leadership to place the blame elsewhere.

Inflation is not a tax..its theft pure and simple

I thought Sharon Zollner made a pertinent comment back in March (emphasis mine):

While there was a view that economics needed to change, there were “some basic facts”, she said.

They included that debt made people vulnerable, a problem deferred was not a problem solved, and “if something is unsustainable, it will end”.

“It is not just houses in New Zealand, this is a global issue,” she said.

“If you misprice something for a long time, people will demand the wrong amount of it. And I would say ‘risk’ has been mispriced deliberately for a very long time.”

The message for 20 years had been “central banks have got your back”, Zollner said.

“People say to me ‘the Fed won’t let equities fall’ or ‘the Reserve Bank won’t let house prices fall’, as if central banks are omnipotent, and that fails the ‘too good to be true’ test.

“One thing that could demonstrate that is the rise of inflation.”

Indeed. Everything is priced as if there is no possible risk in any investment. Thus we get a huge 'bezzle' -- the gap between what assets are valued at and the actual returns they can generate in the long-run.

A crash in both housing and equities is the best-case scenario right now. Look at the dilemma China is in now to see why keeping the bubble afloat only ever makes the final reckoning worse. That said, I wouldn't be surprised if the Gov't and Reserve Bank choose endless landlord/corporate welfare and continually declining real living standards over letting asset prices fall.

Excess of demand over supply - in a buoyant economy with a tight labour market.

A blow to those with funds held in bank term deposits.....

TTP

That's a fallacy. If excess demand pushes up the price of item A, the consumer goes to item B.

If the money supply was not increased then there is no extra cash to cause inflation - just a transfer of choice - or even go without.

Money creation causes inflation. Inflation measures the full basket of goods. No more cash, then no overall change.

Hi Rastus,

We live in a market economy.

When there's a shortage of a commodity, rationing occurs. The price mechanism is the rationing mechanism - and prices increase.

Go down to your local supermarket, hardware store or petrol station - and you'll see everyday examples of the price mechanism in action.

Cheers for your wallet, my friend!

TTP

Of course price increases. But when they do on product A, the market makes you make choose B.

If you don't increase the money supply the same cash circulates. The entire basket as a whole can ONLY rise if you increase the amount of cash circulating i.e if there is more cash in the same basket.

Like most you have been hoodwinked.

Increasing the money supply causes inflation. End of story

"Of course price increases. But when they do on product A, the market makes you make choose B."

You can't assume that at all, Rastus. It depends on the cross-elasticity of demand coefficients. (Go read up on basic microeconomics.)

TTP

The fact the RBNZ and "professional" economists are surprised shows how irrelevant their predictions or opinions are.

Would love to know how people think that raising interest rates will:

- tackle funding shortages in local government

- stop the Saudis manipulating the price of oil

- reduce the costs of building materials affected by global shipping

- increase the number of people that can build or support the building of houses

Seriously - someone help me out.

-won't

-will preserve relative value of the NZD, very pertinent to fuel prices here

-ditto

-will reduce incentives to keep housing empty while cap gains accrue, and as above.

The real question is what will happen if we don't raise interest rates. Namely, the staggering malinvestment will continue, and we'll see progressively worse inflation as other countries' rates start to drift higher. Asset prices preserved while purchasing power declines = ever-increasing inequality.

Surely if DTI was introduced it could reduce the extent to which OCR rises do the heavy lifting?

Oil prices have increased by 30% in the last few months, shipping prices are still sky high. Increasing the OCR by 100 points or so will increase the value of NZD by, what, one or two percent? It's irrelevant.

I completely agree with the need to reduce malinvestment and particularly the credit fueled housing boom. I just don't see how changes to monetary policy will have anything more than a placebo effect. Govt needs to get a grip and tackle the issue directly.

I agree that more direct and targeted measures would be preferable. Property investment is politically sacrosanct though, economic policy is held hostage for now. And I'd argue that much as raising rates wouldn't do a lot to help the problem, lowering them unnecessarily sure as hell helped caused it.

"lowering them unnecessarily sure as hell helped caused it"

100%

Reply to Jfoe

The raising will not help the items on your list. Just like 5+ years of low interest rates was not able to increase inflation, until the RBNZ flooded the market with liquidity.

The liquidity (QE) was used as a lever to hold bond yields down (and therefore market interest rates). QE is simply the central bank bidding up the price of bonds to keep the yield low. My view is that cheap credit / low interest rates is one of the factors driving house price increases (not increased liquidity), and the increasing price of goods and services we are seeing now is due to spikes in demand, supply chain issues, restricted energy supply, etc.

Brain:

Don't say it

Don't say it

Don't say it

Don't say it

Don't say it

Mouth:

BUY BITCOIN!

According to Richard Werner, we're supposed to believe the gold price, at 0% YoY, is not manipulated. Werner thinks the good news is that the manipulators have created a golden investment opportunity, as gold is underpriced. He goes on the say once the cap is lifted, gold is going to do a lot of catching up in a short time.

The central bankers can't print more bitcoin.

The astute investor should be holding some.

October 2020 the avg house cost 35 Bitcoins.

October 2021 the avg house cost 10 Bitcoins.

Home prices are down 75% over the past year. Anybody know why the housing market crashed over the past year?

Because the value of the dollar has been destroyed by low interest rates

So say 10,000 other crypto's.

Futile debate.

Time will tell.

HFSP

The US makes a decision on BTC ETF's tomorrow, if approved, the price will skyrocket.

Be Quick!

What happens in the dark of night on Nov 5th is revealed on the morning walk on November 6th.. The burned out corpses of things that go skywards with a hiss and a roar are found littering the ground.

Transitory

who could have forecast such a thing?

er

What is the point of having an "independent" central bank if they are going to pick and choose when to follow their mandate to control inflation?

35% house price inflation and 5% consumer price inflation and they still have interest rates at effectively zero?

Is it incompetence orr criminality?

It is reckless negligence compounded with disingenuous incompetence.

The RBNZ has been wrecking the country and its financial system with its moronic, ultra-loose and destructive monetary policy. Now we will all have to pay the price, with stagflation and with the RBNZ being forced to raise rates to levels much higher than otherwise would have been necessary, had they acted with competence.

and with the RBNZ being forced to raise rates to levels much higher than otherwise would have been necessary,

Really? The RBNZ's words and actions are saying nothing to suggest that their hand is being forced to raise rates.

Exactly, we had a hint of pending deflation last year and it was emergency interest rate cuts and extroadinary levels of market intervention.

Now we have evidence of actual high inflation and its a wait and watch approach.

You get the feeling that central banks are more about protecting asset prices than controlling inflation and when you see the insider type trading activities of Fed members, then you consider that our central bankers will primarily be asset owners, you can't help but think they may have independence issues given the inconsistency in their actions when dealing with the data in front of their noses.

If we saw a downside miss of this magnitude from normal interest rate settings, the RBNZ wouldn't hesitate to cut by 100bps with zero notice given.

Asymmetric mandate.

Yes the inconsistency in their behaviour when presented with data has certainly got me questioning the legitimacy of their independence.

The paradigm that they appear to see the world through is something like:

'what possible actions could we take in the present circumstances to ensure that those with assets retain their capital or become better off in the short term'

As opposed to:

'what possible actions could we take in the present circumstances to ensure financial stability over the longer term'

- Consumer price inflation has only just got out of their mandate

- They have foreseen inflation that didn't exist a number of times in the past 10 years so are right to be careful

- There is a pandemic which is a bad time to raise rates.

- While obviously not all of the inflation is transitory, some of it probably is.

You will see rates rises from here, they will definitely follow their mandate and control inflation, no incompetence "orr" criminality involved, but a nice rant all the same.

The pandemic is just part of life's volatility. To excuse use covid to exceptionalise everything is rediculous.

But damn convenient.

So missing their target once (or is it twice now) is "incompetence orr criminality"? Seems a bit over the top to me. Auckland's weather forecast was fairly wrong yesterday, I am not claiming incompetence or criminality over that one event.

but, but, but... transitory.

The only thing more hopless than a generic economist, is an economist working for the RBNZ.

By looking at how the RBNZ has managed its monetary policies in the last couple of years, I must say that I'd rather trust a used cars dealer or a real estate agent than Orr.

"you have to go back to 2008 for the last time inflation was 'naturally' this high"

"the September quarter movement was the highest since the June 1987 quarter"

Both 1987 & 2008 were followed by recessions, a bad omen?

Not a bad omen at all.

Merely a reality that as sure as night follows day, bust follows boom (not necessarily in real estate, that's a rare outlier)

Look at every building boom, it's always been followed by a bust or at least a major drop away.

It's history repeating itself:

- Strong demand

- rising house prices

- increased building

- costs rise as resources are put under pressure

- OCR rises

- demand decreases and developers costs further increase

Then something has to give....

Indeed ! I was merely making the point that the last two times inflation was higher, recessions followed

I am sure as an architect you have seen plenty of construction busts too.

With its ultra-loose monetary policy, Orr has engineered one of the biggest housing bubbles of recent memory, and he is responsible for the unavoidable carnage that will result once the bubble pops.

Love the comment the 4.9% was higher than what the RBNZ predicted - which was 4.1%

I'm learning this year whatever the RBNZ predicts - whether it be unemployment GDP, add somewhere between .5-1% of their prediction and you will be closer to the actual number.

The RBNZ's predictors are having a shocking run with their forecasting this year.

Not surprising at all. Central banks and govts always underestimate what is seen as negative (inflation) and overestimate what is seen as positive (income growth).

Wow, if the CPI is reporting such large increases imagine what the situation is actually like out there.

On an anecdotal basis re the huge jump for vegetables - our local supermarket was completely out of broccoli last week with a note up citing an unusually warm September followed by unusual cold and wet weather creating a total gap in supply. I imagine prices were way up when they were in stock.

Wait until the current fuel figures make it in.

100%. I seen a pump price for diesel at $1.75/lt in Taupo last week. Outrageous

Let's see what the inflation numbers look like when another 2-5% of the labour force are removed due to vaccine mandates.

This won't be pretty.

Why don't these people just get their vaccine or get a medical certificate if they have a condition that prevents them from getting vaccinated.

In July, I made comment below on RBNZ OCR decision. I hope they still don't regret that they failed to raise OCR when they had chance back then. They will need to do bigger hikes now.

by company of heroes | 14th Jul 21, 2:35pm

Soon enough the fear of uncertainty that RBNZ is holding will cost us big time... The strength of domestic NZ economic data is undeniable so far and the inflation is out there already. I hope they don't regret when they see this Friday's CPI data.

The average Aucklander would probably still go backwards very soon in disposable income. Even if they got a 10k pay rise tomorrow. Tax man will take 33%. Bank will take 75% of whats left when they raise your 500k mortgage interest rate by 1%. You will be left with $33 a week to cover CPI inflation. When oil goes to US$100 then petrol increase alone will probably take care of that.

Like your reckoning Westie. To be honest, I think you'll find many are already living paycheck to paycheck, from beneficiaries right up to the top end of town. Most of society is not prepared for the current economic climate because the idea of a rainy day never really occured to them.

Or they just never had the headroom to bother with worrying about it.

Ouch that's sobering.

I had our banking advisor ring me last week, we have nearly finished paying the mortgage off, asking if we want to borrow a million or so and get into housing investments. I said we will wait and see what happens over next few months as no panic, she said well house prices will keep going up 10-15% again, especially when they open the borders. So banks obviously been told put the FOMO up existing clients to borrow borrow borrow. The OCR needs to go up so people stop and think about the debt they taking on with inflation is going up up up as well.

. So banks obviously been told put the FOMO up existing clients to borrow borrow borrow.

They have to meet their sales targets, which are incremental. Most of the banks' foot soldiers don't think about the bigger picture. They listen to what their superiors tell them

That is illegal isn't it? Were they qualified to give you financial advice?

That's how they keep the "system" running. The reason we didn't have the inflation problem going on was the "system" worked. They created fake inflated assets to soak excessive printed money to keep the inflation down by talking property price up. Even if you finish paying off your mortgage, they will try to get you on another one,otherwise you will just spend those gains to let the excessive money flowing into market. However, things are different now with supply shortage. People are not easily buying into those schemes anymore. You wonder why we have soaring inflation now....

Does anyone know to what extent the RBNZ's mandate formally considers exporters?

I would imagine it's not an explicit consideration, but it's an implicit one in terms of the RBNZ's employment mandate.

Does anyone have any thoughts as to where the NZD dollar might stand if the OCR was raised 1% over the next 3-4 months?

RBNZ's mandate is really simple - keep employment as full as possible ie between 4-4.5% and keep inflation between 2-3%. Outside that and the new government mandate on housing affordability (which nobody is too sure what they can actually do about this) - the bank has no other obligations.

In regards to the NZD - if the OCR rises - leading to increases in bank interest rates- which is what the RBNZ will need to do to pull inflation down to the 2-3% band - then typically the NZD will rise making exports dearer from NZ. However it also depends on what the rest of the world is also doing with their interest rates, if all the countries lift their rates then it could end up with the NZD falling.

Last week there was talk of a OCR hike in Britain in Nov which has an inflation problem, US is definitely tapering their bond purchasing and I wouldn't be surprised in the RBA in Australia lifts their OCR in 1st half of 2022 - especially if they get a strong post lockdown rebound.

That said interest rates arent the only thing that drives the NZD- demand for our exports such as milk or overseas investment in NZ - ie buying commercial property or multinationals like Costco setting up business here can also result in a high dollar. Anything that drive foreign currencies into NZ will lift the dollar, anything that detracts foreigners investing in NZ will lower the NZD.

Small correction, it supposed to be 1% - 3%.

There is no mandate on housing "affordability", instead the weasel word "sustainable" was used instead.

As of this morning I'd suspect it would already be priced into NZD rates.

According to asb 60c by February is priced in.

I think people have a tendency to oversimplify on the OCR decision.

Raising the OCR can actually generate some inflationary impacts as well as deflationary.

For example, increasing the cost of borrowing for developers may be inflationary in terms of new housing.

Increasing mortgages may be inflationary for the rental market, by increasing landlords' outgoings.

No doubt the deflationary outcomes are greater than the inflationary ones, but it's not totally clear cut.

I would rather see mild raises of the OCR and use of things like DTI to help cool housing.

Yes I think that we could see rising inflation as the OCR goes up. And it could mean that we have to lift rates much higher than expected to contain inflation rate rises.

The trouble is that the central banks also risk slipping into deflation if these rises cause asset prices to fall and credit lending conditions to deteriorate.

All I can say it what a cluster the central banks have made - and its by their own doing so don't feel at all sorry for them.

Asset prices have to fall. Current prices are not sustainable for the wages being paid to the employees. Most people have just stretched themselves to make money on speculation that they will sell their house in 2-3 years and make money. Then they will move to Australia when world is normal again. Lots of stupid thinking.

Or incomes have to increase.. Guess which one is already happening, although not distributed evenly by any means.

Not Quite

1. Borrowing for new developments - these are short term borrowings guaranteed by pre development sales (most development loans are between 1-3 years for developers) - so the OCR going up usually has minimal effect on the price of a new development - it would add only about 1% to the price of a new build. Material and labour would be having a bigger impact on housing developments - which is adding now somewhere between 5-10% onto a new build.

What people can afford is the biggest factor for the price of a new development. The OCR rising makes it less affordable for people to buy as they cant borrow as much- so the developer will either not build if he cant get enough demand (as people cant afford his development) or will need to build a cheaper property that meets what people can afford.

2. Rents dont have a big effect on inflation - Stats have only had rent included for the last 2 years in the CPI figures and they use an averaging effect - which accounts for what people are really paying - not the headline or advertised rent amount.

Good points, perhaps minimal effects for development projects well underway.

But surely an inflationary factor for prospective development projects, where loans have not yet been secured?

There are a large number of off-the-plan purchasers, most of which cannot lock in finance until approx. 3 months from settlement and many settlements are 6 to 18 months away.

I already know of developers letting purchasers 'walk' on unconditional contracts (minus costs) because the purchaser's funding has been declined due to increased purchaser build costs.

The only reason the developer allows the purchaser to walk from an unconditional contract is when they can sell at a higher price.

Once they can not do that, everyone will be held to their contract with those they cannot meet their obligation voluntarily, being sued for specific performance.

Once we get to that stage, it can collapse like a house of cards.

I reckon that stafe is fairly close.

What a joke, anyone who does the supermarket shopping and pays the bills knows inflation is 10%. Honestly what are we paying these people for.

Yes a lot of people I talk to who have been doing online grocery shopping say its a 10% rise for them in the last year - buying the same stuff....

Could it possibly be that the products online are dearer than those in store perchance?

Also online shopping is expensive for supermarkets to run.

Something tells me the instruction was - "HOW MUCH! Ok, just make sure it reads as south of 5%"

We need it higher. At least 25. The more the better. Just to keep RBNZ happy. They are always complaining that not enough inflation. So they will stop to print money like no tomorrow. Tourism is dead, many other businesses almost same. We just keep buying houses from each other for higher price. Soon you will need 5 houses to buy bread and milk.

Can we get some predictions out there, what's going happen end of this year/early next year....?

shit, meet fan.

Same as it was before. When NZ used pounds and switch to dollars. Maybe NZ dollar will collapse and we start to RMB or Bitcoin.

I think they will increase by 25 BPs in November, and then again at the first meeting in the new year. Then possibly a pause to see how things go.

RBNZ quickly cut the OCR by 1% when covid came. Now inflation has come, why not raise it back by 1%? Or is just doing things what suits the current government, RBNZ's invisible handler.

Interesting thought...

What will a change in interest rates actually achieve?

So much debt now, that an increase would surely be counter intuitive,

- For businesses it will increase the cost to service debt and likely lead to even higher prices.

- For consumers, they will need to forgo purchases to pay the mortgage.

I believe the technical term is "snookered"

Snookered is a great word to describe it.

'Damned if you do, Damned if you don't' is a phrase that springs to mind too.

Or(r) 'Between a Rock and a Hard Place'

Or(r) more crudely 'Screwed'.

Exactly, but this is why having interest too low in the first place is a bad idea. People load up on cheap debt and then you can't raise rates without causing pain.

If inflation - which is rising globally - forces other countries to raise rates, we'll have to as well. We have zero influence over global prices. But because of our stupid, stupid mortgage bubble, it will hurt us more than almost anyone else.

Like it was during the 'crisis' last April when we appeared to be steering down the path of a deflationary hell hole - the question becomes, who is going to end up holding the bad debt. It becomes a game of hot potato.

(until the Fed starts buying junk bonds again...and you realise there is no longer market risk)

At what point do heads need to roll at the RBNZ? They have consistently grossly failed to understand the impacts of their policies and have completely failed in two of the primary mandates: Control inflation, and ensure financial stability.

Not that labour shouldn't share a huge portion of the blame. Giving the RBNZ the mandate to ensure "maximum sustainable employment" is so flawed and is in direct contradiction to an independent body controlling inflation through monetary policy

Geoff Bascand is jumping ship, who's going to be next?

Who on Earth would (re)employ one of these people, after they've transitioned through their 'I'm quitting to re-evaluate my life's objectives' period?!

Of course! The OECD or IMF as reward for a 'job well done'.

These central bankers aren't elected and they aren't accountable. What is the penalty for not meeting their policy targets? Who is going to fire them?

Not Ardern, who is qualified in economics no further than the family fish and chip shop business.

Not Robertson, who is qualified in economics no further than the family creative accounting business.

This government is the most incapable of doing any thing good for the country. They is a control freak government. Everything is controlled and more like a dictator. All their promises have fallen short. House prices gone through the roof. Cost of living haa gone beyond reach. No pay rises. They stopped them. Doing charity with tax payer money. This is no longer a Liveable country for middle class employee who doesn't have rich parents to help them buy a house

Their failure is profound.

Don't bank on any other party being much different. Perhaps they could do less worse. Can't think of the proper phrase.

Looking at the National front bench, they're conceivably more incompetent than Labour's. Which is quite something.

Typical meddling by Labour, thinking they know more than everyone else, and then finding out down the track, they were completely wrong.

Presumably this will put additional pressure on the government to open up Auckland sooner. I'd really like to see them commit to an actual date!

I'm going for the 1st November, its a Monday so that will be the last weekend to get the vax. Simply has to open up before December or failure to do that will cripple the retail sector due to no Christmas shopping. Time is fast running out, there are no other options now but to give us a fixed date. Remember this will have a high fear factor as the government are no longer locking down to protect you, it will drive the remaining percentage to get the vax.

I doubt they would give less than 4 weeks notice as this point, because that would give unvaccinated time to get 2 shots.

The worse thing about this whole thing is people thinking that RBNZ increasing interest rates will make any difference to price increases driven by actions taken in China, Saudi Arabia, Russia etc. It's madness.

Except that the inflation isn't just about oil, is it? Though that is a big part.

I think people know - and this article demonstrates - that housing/housing-related inflation is a big part of our inflation increase, and that is very definitely tied to the RB's interest rate settings.

It is tied to RB's interest rate settings, but a reduced interest rate should only lead to a one-time shift as prices adjust to the reduced cost of borrowing. The fact that prices have continued to rise points to other drivers being just as significant - e.g. consumer confidence buoyed by Govt announcements, compounding equity gains amongst the house swapping older middle classes, favourable tax and policy settings for home owners and landlords, accommodation supplements and other subsidies, shortage of affordable housing, highly desirable housing in the 'right' school zone etc.

I don't think interest rates are 'just another factor' in the housing bubble though, I think they've been most of the cause. I think they've been especially potent here in NZ, where property has become a way for risk-averse investors to park money for really quite limited yields because TD rates have been so low. If TDs go up by even 1-2%, property at current yields starts to look like a really crap investment. Even more so when the same rate rises have cut FHB borrowing capacity by 25% so they can't even afford to buy it off you for what you paid. That's the day we thought would never come -- because we thought inflation was dead as the dodo.

Madness is letting.... encouraging, people to get ridiculously indebted to provide shelter for their family within feasible commuting distance of their place of employment. Madness is to brain wash the population into thinking a down turn is a bad thing and must be avoided at all costs. Madness is a bank whom lends money on a non-productive asset that increases in value 30 plus percent in a year.

What a surprise RBNZ asleep at the wheel, and the government guilty of meddling with the RBNZ's mandate, with very negative results.

Can someone please hold Adrian Orr to account. The RBNZ forecast a 20% fall in property and were so heavy handed in their response we saw a 30% increase. We now see 5% inflation way above the 2% mandate. His response has literally raided the savings and the salaries of all NZers to prop up the property ponzi.

Enough already... what does he have to do to be seen as incompetent.

He's doing a stellar job for his employers. And that.....isn't you and me. We just get to pay his wages.

Orr is a complete failure.

Up to 1/2 of NZs housing unaffordable inflated cost is tied up in the non-value added costs associated with the cost of land and bringing it to a developed stage.

Non-value added costs being those costs that only exist because of restrictive Govt. policies and if weren't there would not reduce any amenity value of the property.

So prices have the ability to fall considerably in value. The reason they never fall to their full publicly recorded potential is many homeowners will feed the loss from other sources, like savings, delayed health, and educational costs, etc. And of course, the Govt. will try to political subsidize any fall.

With Covid, we already have had nearly two years of practicing this.

The straw that broke the camels comes to mind.

So prices have the ability to fall considerably in value.

Consider yourself in the minority if you firmly believe that. I'm a contrarian at heart and think that it's possible. Not sure what the catalyst would be though. Cost of credit is only 1 factor at play.

{kind=link}

Yes.

This is how the future is going to be unless we change the culture of take and take and take unless nothing is left to take.

We all want more and more. We want it easy but how long the easy last? More gain means there has to be more pain somewhere. Nothing comes for free and same stands for low interest rates.

Looks like the property market had priced in the inflation event last year and will continue to do so.

USD 100/bbl, bring it on!

2 winners to blow everyone else out of the water.

Looks like I'll be buying more flat whites this Christmas.

Well that pretty much guarantees a 50pt minimum OCR increase in Nov and still the OCR will be -4% in real terms

I got so sick of any fiat currency I held in the banks being quietly whittled away by inflation, I got into Cryptocurrencies end of 2020 ...and haven't looked back. The gains I have made have left inflation it's tracks and much, much more !

Play the bankers at their own game ! and for once "turn the tables" on the greedy *&^*(^(^ !!!

Sure, it was a risk, but out of 12 coins I bought only 1 has not made a profit.

Been out of property investment in NZ since March 2016 and my only regret is that I didn't get into Crypto then !

So for all you "property bull" commentators out there who have referred to me and others on here of being a DGM with property investment, always remember there is more than one way to skin a cat :)

Crypto is fine if your living in your mortgage free house and just playing with Bitcoin. You cannot live in your Bitcoin so its pointless if your still renting.

Not true. You can put your savings (aka house deposit money) into crypto and keep paying rent. A big risk for sure, but so is borrowing a million dollars.

So if the bank would lend you a million dollars to buy Bitcoin or a million to buy a house, which do you think most people would spend it on ? Pretty obvious really beside the fact the bank will not lend you a million to buy Bitcoin in the first place. The risks are not even comparable, in fact they are at opposite ends of the scale.

Carlos67 I understand what you are saying and you need a roof over your head - but at the moment Cryptocurrencies are the best performing asset class - period. So what I would be doing is DCA (dollar cost averaging) the amount you are saving for a deposit and put it into Crypto ....and just watch and wait :) .... there is still so much more to come in this space.

Then when the SHTF in NZ residential property (which no doubt there will be some sort of "correction") you are in ! Take that deposit which should of at least doubled and with the correction in house prices, you'll be sweet ......plus you'll have a smaller mortgage ! ......NFA DYOR

Annual inflation soars to 4.9% - a 10-year high

No worries...Uncle Orr will protect your backside as is just transitory......and transitory could be from few years to a decade......LoL

Do not be surprised if next data too is higher as RBNZ will repeat...........

Inflation at UNSUSTAINABLE™ levels - just like house prices, right Jacinda?

I just bought a coffee in Dunedin. Nothing special - just a large latte.

The price for the coffee was $7.20

I don’t need a press release to tell me that inflation is already here.

It is time to reduce your bank debt if you can. Get rid of your worst performing rentals and hold on tight. Interest rates are going to rise quicker and further than many thought. As they rise asset values will drop. People will be only able to borrow less than they can now if hey can borrow at all. The party is over.

To be fair, many people were giving the same advice a year and a half ago, at the start of the first lockdown. People (including me) keep underestimating the power of money printers.

To be fair, there were more people on here that were saying that interest rates can not possibly rise, in fact many stated that rates were going to go negative. Sure the pending rates rises have not really hit us yet but its not looking good for no rises is it ?

Yep, can you can hear the buzzer from the cockpit yet. As much as Orr has muffled it, the message is now clear.

"Pull up pull up hazard warning...pull up".

The Pilot even looks like Orr

Feijoa,

Last year October 2020 I bought an iPhone 12 pro which cost me $2099.

This year October 2021 I bought an iPhone 13 pro which cost me $1999. A better iPhone at a lower price.

I drink a lot of coffee but I guess you could say that I spend more on iPhones than on coffee. Looking at those two items in isolation I could conclude that we have deflation.

Actually a single coffee a day keeps the iPhones away. Swap coffee for a single drink of choice and the price for that drink shoots through the roof with increases (even bottled water) compared to consumer electronics which are known to have a huge markup esp when compared to the rapidly lowering production costs and the waste. At this point they may as well be giving iPhones away just to save the dumping costs to landfill but that might ruin the brand image having some poor people get end of line ones instead of the trash trucks.

Wouldn't know, iPhones are junk I have a decent Samsung for half that price. The last Apple product I used that was any good was an Apple 2E in about 1984. I only need to replace it every 5 years and I'm still using the last one just to run just a single App with no SIM card in it. Your spending more on phones than I spend on cars.

Dude ! was in Dunedin in April .....where did you buy it ?

Certainly not the night and day because they don't serve anything fit for consumption. Nor for that matter what is served at service stations (although the inflation on coffee prices there are far above 5%).

The music is stopping and we are wondering if we have a chair or not. The decision the Govt is now facing is to protect the interests of NZ citizens who actually voted them by pushing an immediate OCR upwards jump, or continue to protect Bankers bonuses and speculative lending by doing nothing. Doing nothing is further crushing the value of retired savings and what little equality is left in the fabric of society.

"Lets Do it" has become "Lets do Nothing".

I think 2022 is going to be a very 'interesting' year...

A few people on here have predicted that 2022 or 2023 is the year it all hits the fan. I'm beginning to see the light and I think they could be right on the money.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.