Big. But not quite as big as expected.

Inflation has hit its highest level in this country since 1990, but the 6.9% figure as at the March quarter is somewhat below market expectations, which were for a figure of 7.1%.

The latest 6.9% figure is up from 5.9% as of December 2021. It is around what the Reserve Bank (RBNZ) was expecting. It has suggested that inflation will peak at about 7% in the first half of this year.

The key 'non-tradeables' (IE domestically-generated) inflation figure came in at 6.0%, up from 5.3% in December, showing that there is a great deal to do in terms of controlling rising prices within the country. Statistics New Zealand says the domestic/non-tradeable figure is the highest since that particular series began in June 2000.

'Tradeable' (imported) inflation was a searing 8.5% in the year to March, which was also a series-high figure dating back to June 2000.

In terms of the quarterly overall figure, inflation rose 1.8% in the March quarter.

Bear in mind that the RBNZ is charged with keeping inflation in a 1% to 3% range, explicitly targeting a 2% level. Governor Adrian Orr has conceded the central bank is "not in a great place now" with inflation. The RBNZ's main weapon against inflation is the Official Cash Rate (OCR), which it raised by 50 basis points to 1.5% last week. Much more hiking is expected yet.

Ben Udy, Australia & New Zealand economist for independent economic researchers Capital Economics said the first quarter inflation figure was broadly in line with the RBNZ’s expectations, "which reduces the likelihood of another 50 basis point hike in May". The 1.8% q/q rise in inflation was below the analyst consensus of a 2.0% q/q rise, but was enough to take annual inflation to a 30-year high of 6.9%.

"Looking ahead we think inflation is now around its peak. The government’s reduction in excise taxes should reduce fuel costs in Q2. What’s more, as house prices are now falling we think homebuilding inflation will ease before long. And base effects mean the pace of quarterly price growth would need to ramp up further to lift headline inflation again in the quarters ahead.

"The RBNZ noted at its April meeting that it expected inflation to peak at around 7% in the first half of this year. As today’s data are broadly in line with that forecast the chance that the Bank hikes rates by another 50 basis points in May has now diminished. Still, we expect inflation to remain well above the RBNZ’s target throughout 2022. So we still suspect that the Bank will hike rates to 3.0% by the end of this year," Udy said.

The main driver for the 6.9% annual inflation to the March 2022 quarter was the housing and household utilities group, influenced by rising prices for construction and rentals for housing.

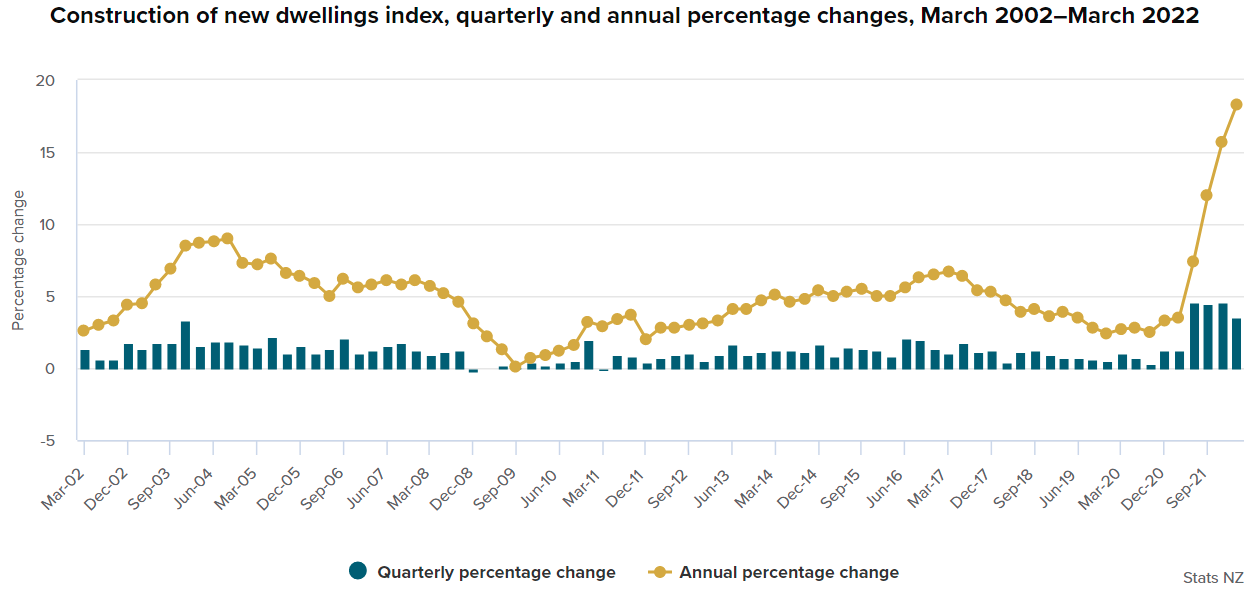

Prices for the construction of new dwellings increased 18% in the March 2022 quarter compared with the March 2021 quarter, the largest increase recorded since the series began in 1985.

“Construction firms have been experiencing many supply-chain issues, higher labour costs, and also higher demand, which have pushed up the cost of building a new house,” Stats NZ consumers prices senior manager Aaron Beck said.

Transport was the second most significant contributor to annual inflation, up 14%. The largest driver of this was a 32% increase in petrol.

The increase in cost of food also contributed to the annual movement, with food prices up 6.7% annually. The largest contributors to this were vegetables (up 24%) and ready-to-eat food, up 5.6%.

Annual inflation main contributors:

- Housing and household utilities increased 8.6%, influenced by home ownership (up 18%) and actual rentals for housing (up 4.0%).

- Transport increased 14%, influenced by private transport supplies and services (up 23%) and purchase of vehicles (up 5.6%).

- Food prices increased 6.7%, influenced by fruit and vegetables (up 17%) and grocery food (up 5.5%).

- Miscellaneous goods and services increased 5.6%, influenced by other miscellaneous services (up 11%) and personal care (up 6.4%).

Consumer prices index

Select chart tabs

144 Comments

Just the start of the bad news for this inept Govt.

Is that your only take..no wonder the system is stuffed?

The system is only stuffed because of wayward power seeking politicians the general calibre of which has hit rock bottom.

What specifically did the politicians do that has stuffed the system?

To be fair, it is more along the line of what they do not do. This is not the most open honest transparent govt ever, that's just a buy line that was peddled.

A gross over reaction to Covid.

Borrowing ridiculous amounts of money and spending it into the economy on folly.

So are you going to return the tax payer (your terms - government money) handout you were given then? Thought so...

What proportion of the total is that then?

Everyone is doing it right now via stealth....its called financial repression and it happens when the real interest rate is held in a deeply negative position.

Bit of a rubbish comment this. It's like suggesting someone should volunteer to pay additional tax each year because they dislike the govts performance. You know, out of principal.

Completely over baked the cv19 fiscal response. Oversaw the biggest surge in house inflation (after promising to fix it) and in general delivered sweet FA of what the promote aside from the promise of new taxes and a new public holiday.

I like the pooled water analogy. They walked away from property and taxation reform, and then acted surprised when billions of printed $$$ ended up in property and prices spiked. So I think the failure of the first term to enact structural change like what they campaigned on was the problem, otherwise we would have seen a far more muted effect from the money printed.

Oh look, a Strawman!

what handout? didn't receive a thing.

Your local Coffee Shop did

So I'm supposed to give back their money? You're an odd one.

And them being at less than 66% of normal operating revenue...that caused rampant inflation? How's that happen?

... yes , but we only got 6.9 % inflation ... we were tipped to hit something starting with a " 7 " ... feeling very chipper ... 6.9 .... yessssireeee , no problems here , then ...

Might head down to the cafe & order up a coffee and smashed cauliflower on toast ...

Well that's some kind of parallel universe that we have no idea what the outcome would have been.

We kind of forget that 2 years ago New York was setting up emergency hospitals in Central Park and we had no protections against the virus.

Every business was drawing up plans for redundancy and scrambling for protective supplies. England locked down for a year while we got to enjoy a golden summer - twice.

Withdrawing the loans to value was stupid, the rest was understandable. The opposition were a shambles.

We're not unique, it's everywhere. Making out that the government is solely responsible, rather than human nature, financial illiteracy and greed placing us here, is whitewashing to fit a political opinion.

Yep, cue the blame game - part of human nature and the unwillingness to look at one's own beliefs and conditioning.

Funny fact - human nature is not fixed but we don't teach this in our schools. Greed is simply fear. Financial literacy is an oxymoron. If we were to truly understand we wouldn't allow financial institutions in their current form, and nor would we continue with the current setup.

Well said DDH

What folly?

Be specific.

Are you suggesting that short-term allowances to keep people eating and businesses' above water - even if most decried them as insufficient allowances and people and businesses had less to spend than usual - was the causal factor in inflation? How is it you think people having less income to spend than usual caused inflation?

https://www.nzherald.co.nz/nz/politics/inflation-nation-the-question-no…

excerpt;

National called on Labour to fund its $1.7 billion tax cut from this same $6b allowance, leaving the remainder for public services. It's a clever way for National to have its cuts and eat them too, but it does weaken its position on inflation.

Until the party dares to say that it would trim back operating spending from what Robertson proposes, it cannot argue that it would deliver anything other than the same level of inflation as the Government.

They could just spend more efficiently to reduce inflation achieving the same or better outcomes with less funding but likely such optimisations and efficiencies would not become apparent until they were in government with access to all the data that brings with it.

If they can't name the optimizations they would enact how are we sure they exist.

How the government is spending its money is public, you don't need to be in power to give concrete figures on how you would do it better.

While the government has a significant influence, keeping inflation under control is the Reserve Bank's job. RBNZ has failed miserably.

Amending the RBNZ Act to include maximising employment, against expert advice, has largely led us into this mess.

The central bank was reluctant to fight hard against inflation until recent announcements from the government on resuming international tourism and people import to levels never seen before.

Inflation control is not the job of the government, it's the job of the RB. The reason why we have a (relatively) independent RB is so it isn't distracted by political considerations from its mandate of controlling inflation. The target is 2% +/- 1. Not 7. The buck stops there. Yes, of course in the best of worlds the fiscal policy would not be madly adding to inflation and the two would work in a coordinated fashion. Right now, the real rates are so negative that G't and RB indeed are co-ordinating: they're both raising inflation by their actions. Job well done!

But the government screwed the RBNZ over to a certain extent with the change to its mandate to include employment.

I have little doubt that, whoever was in power when Covid hit, would have reacted in the exact same way, following the lead of other larger nations..

It's laughable how National is attempting to brand this as "Labours' Cost of Living Crisis"..

Well but this is not true. First, look at the % change in NZ fiscal stimulus vs other OECD countries (https://www.imf.org/en/Topics/imf-and-covid19/Fiscal-Policies-Database-…) NZ is #2 in the world, after the US. But second, look at where the spending went (redistribution vs capacity-building initiatives). You'd ideally want to spend in areas that deliver future growth, rather than chiefly providing a safety net. So a different government may have made different choices - like the rest of the world shows. But again, inflation control is the job of the RB, not the job of the government.

Pandemic comes > Government locks the people down > prints money to pay for lost earnings > Government changes RBNZ focus > RBNZ keeps money cost low to help Government. No, nothing to do with Labour /s

I hope people own their votes. It’s going to be a long hard poor time for the young. Mine flew out of NZ last month. Smart.

Very astute. ✈️ ✅

Was NZ the only country to do this?

Don't forget Labour will have added 100k+ newly eligible voters by the end of this year through its 2021 Residence visa programme.

Comparing the qualification criteria to the usual residence pathway, it appears that most of the eligible applicants wouldn't have gained permanency without aunty Cindy's generosity.

I would be taking this voter grab a lot more seriously, were I in Luxon or Seymour's position, but surprisingly not a peep from either of them.

Yes, smart! Both my children in Aus. Early twenties, doing really well! Would be mad to come back here anytime soon! There is going to be a massive exodus of young over the next couple of years because their prospects here are bleak to say the least!! If the current muppets get another term then NZ is toast! It pains me greatly to say this as I love this country!

Overseas exodus happens every time we have a labour lead Govt. Then those Kiwis high tail it back to NZ to take advantage of our generous welfare system that they never contributed

It's a pain too that even if we change to National, there's no incentive for them to return. What have young people to return to if we elect a party of property spruikers whose great policy plan is to take taxes off fellow property spruikers and leave working Kiwis paying for the bulk of society? Bleak indeed.

Next one 7.9%, and then 8.9%, and then 9.9%.

4.93, 5.95, 6.93. Does raise some eyebrows, doesn't it.

Mirrored by The Mortgage Rates.

Inflation rate of 6.9%. Standard KiwiBank 5 year is 6.79% "Next one 7.9%, and then 8.9%, and then 9.9%."

7% Interest Rates this Year, Guaranteed. Very Soon. Maybe Next Month.

exactly .9 again ............

It's amazing how steep that graph is.

And the scary part is pricing intention surveys, that have been the most accurate predictor or inflation over the past 18 months, project it’s going to keep this trajectory.

The RBNZ like to talk about inflation “peaking” but their track record to date on predicting inflation has been pathetic

I suspect that is keeping interest rates from going as high as they need to. When the market works out the RBNZ has got it wrong again, they will continue upwards

interesting times.

More ominous than amazing I suggest.

Reminds me of the "if we do nothing" covid forecast graph.

Atleast it's not 7%, thank goodness.

Hahaha

Same old spin isn’t it. Oh it’s not as bad as some thought it would be therefore it must be good. Have a tot & go back to sleep good little sheepies.

I wonder if it was 6.99999998, still not 7 I guess, well done to the person on the excel sheet.

6.92884% March 2021 index number 1068 vs March 2022 index number 1142

=if("total">6.9,6.9,"total")

White font on white background and hide the cell, nobody will know Minister. Good man.

Nah what you do is code it into VBA and then lock the project. That way even moderate excel geeks cant see the formula.

Just imagine how you know who would have been…

So if you have locked in a price for a new build, are we going to see a large number of building companies fold as presume they going to have to absorb the rising costs. Or if you have not locked in the price is the new owner going to find they have lost equity before they have even moved in as well as sky high mortgage rates. Going to be interesting to watch that industry.

Yes. And I have been calling this looming crisis for a year…

Different kind of Leaky Home Syndrome this. Shall we call it Inflate Cost Syndrome. How many will be affected, both Builders and Buyers ?

Answer - LOTS! There will be carnage for both.

And economists have been totally asleep at the wheel, about their lack of analysis on what's coming in this space. Which just shows how useless they are. OK at describing and explaining what has happened, generally very poor at forecasting what is coming. Far too reliant on models that have fundamental limitations.

I don't like or agree with everything he says, but at least Tony Alexander has been hinting at this looming crisis for a few months. I suspect he's more concerned than he lets on, too, given how much he is indebted to the RE / property ponzi for his support.

By the way, it will be far wider than builders and buyers in terms of impact. It will also whack architects, engineers, planners, surveyors, tradies, building supplies people, RE agents etc etc. Also less direct impacts on vehicle sales etc

Answer - LOTS! There will be carnage for both

Is DGM the new black?

Black is a great colour for DGMs.

Despite being a DGM, I don't wear black at all.

The fixed price sell off the plan model is effectively dead unless you can really whack up the margin to cover the risk of future price increases. Better off to either land bank for a while and wait it out, or if you can fund without presales you may get a better price selling on completion. Or you may not of course. Build to rent is another option, if the rent will cover your costs.

The fixed price sell off the plan model is effectively dead unless you can really whack up the margin to cover the risk of future price increases.

Exactly, and as it's been such a big part of the construction boom over the past 3 years, its 'death' is going to have huge impact. It's a real double whammy, that is atypical- soaring input costs, and falling prices...

Do you agree with my long stated view WD that there's going to be carnage later this year in all the construction-related sectors I mention? Like me, you will have an informed industry perspective.

Developments in train will keep things going OK, for a little while longer, but once many of those developments are completed (of course some won't be completed), then that's when we will see real issues.

Most trades seem to have a good 12 months plus of backlog to get through however it will be interesting to see how many people start to put off those smaller renovations as interest rates start to bite. It's also not great timing for all those apprentices that are starting to come through either as companies will be having a second thought about increasing their staff costs.

One useful tack would be to have a moratorium on covenants that effectively serve to prevent finishing the less important parts later. There'd be nothing wrong with folk having a gravel driveway for the first few years - as used to be common - or finishing fencing and landscaping later. Some costs could be reduced there.

Food up 30% but 85" flatscreen TVs down 0.5%?

Easy. Flatscreen TV sandwiches. Substitution sorted.

Ouch, that construction inflation.

Huge headwinds for that sector.

Funny on the .9 thing!!!

The most amazing thing about the construction inflation, to me, is how stupendously expensive it was even before that increase. Must be mind-boggling now.

A standard sheet of plasterboard at home depot in the states is $10.53 ($15.60 NZD)

I can't find Gib at Bunnings online, but elephant board standard sheet is $34.51 NZD

Plenty of "gib" available on TardMe if you're willing to pay the scalper prices.

https://www.trademe.co.nz/a/marketplace/building-renovation/building-su…

I notice in the Australian building code they seem to just use plywood for bracing instead of a specific monopolized brand of plasterboard. Dumb aussies, Noo Zuland is way smarter.

Yes when had work done on our place the architect used the Gib website to calculate the bracing. The result is that you have to use the Gib brand in the build to pass inspections (even though they are all just gypsom with some paper each side). All very dodgy.

Along with the Gib screws, Gib jointing compound, Gib finishing compound, Gib rondo ceiling battens, Gib trim tape, Gib cove etc.

yes and the elephant board doesn't have the 'paperwork' autocratic councils demand...the biggest issue is still housing which ties up everyone's spending power and housing has been the victim of bureaucratic over-indulgence...so rather than building a cheaper house that doesn't have a cavity or double glazing lets just let them sleep in cars...

The often trotted "back in my day we had basic starter homes with no floor coverings, single glazing, no insulation, no driveway, no heating, why can't the younger generations do the same".

I'm sure if the option was there most if not all aspiring FHB would leap for one of those homes if it meant they could become home owners.

Councils are autocratic now to avoid ratepayers being stuck with the cost of another building industry foul-up of "just trust us" Leaky Buildings Crisis proportions. It turned out that the industry could not manage its own standards if it was at the same time allowed to dodge responsibility.

The answer would be mandatory industry insurance instead of council regulation. But the problem is the industry is uninsurable. No one will underwrite an industry insurance scheme.

However, why we can't have pre-approved cookie-cutter homes in bulk is another matter.

Yeah, businesses always do that, they put 9s in the end to make the price looks good. ;)

Interesting that it was in an upward trajectory before COVID.

the headline should read - Raruraru Pikinga Nui Robertson-Orr - both Dads have a problem

Reality would be somewhat higher than 6.9%. Instruction would have been just make sure it is <7%.

It was widely predicted to be 7% or higher so with the convenient figure of 6.9% the media can now use their favourite saying “Lower than predicted”.

Yes I'm sure Robertson is going to risk his career (and potentially a criminal case?) and instruct stats NZ what the number should be.

Now that we have seen Clarke in Singapore with the PM,the conspiracy crew have moved onto Stats NZ ...

This could be one of their ways to curb the inflation expectations. Can't blame them! Haha!

It'll get blamed on COVID-19 and Vladimir Putin. Craig Renney assures us that government spending doesn't contribute to high inflation, so Robbo, if you're listening, start pumping up that May budget!

"Experts say..."

The last three inflation figures: 4.9%. 5.9%, 6.9%....?!?

Is the probability of getting 3 x 0.9's in a row 1/1000?

The odds of getting the same last number 3 times in a row is 1/100 I think. The fact that the number is a 9 is no more relevant than if it was a 6 is it?

If you assume that the digits are equally likely, odds of any digit 3 times would be 1/100 as you say. But we wouldn't be talking about it if it was 4.6, 5.6, 6.6, would we?

But it's even worse than that. The digits aren't equally likely:

https://en.wikipedia.org/wiki/Benford%27s_law

" But we wouldn't be talking about it if it was 4.6, 5.6, 6.6, would we?" - exactly.

It's fudged. It's been tweaked under 7%.

Hmmm mortgage interest rates in 1990 were circa 10%?

The lesson that we can all take away from this is that government issued fiat currency should only be used as a medium of exchange and should NEVER be trusted as a store of value.

The value of money is a bit like a packet of Raro. These numbers reveal that Roberston and Orr have been taking turns whizzing in the jug.

Inflation is theft...but all seem to think its great until it gets over 2%?

Inflation is tax. But they will never admit that.

No it's not .I have no problem paying tax ..inflation I have no choice, it's taken automatically every day.

Your have been sucked in like most of the sheeples. When the government prints more money, prices eventually increase.

The extra money will just result in higher prices and no additional output. And increased prices mean that existing money becomes less valuable.

If the price level increases by 10 percent, existing dollars are worth 10 percent less than they were; they will buy (roughly) 10 percent less in terms of goods and services.

i.e Inflation is exactly like a tax on the money that people currently hold in their wallets and pocketbooks.

Warren Buffet thinks so to -

NEW DELHI: One of the world's richest investors, Warren Buffett, today termed inflation as "a cruel tax on people" and said that improving one's earnings is the best protection against price rise.

Inflation a cruel tax on people, says Buffett - The Economic Times (indiatimes.com)

Doh..as if any on this site was unaware of that..but inflation is still theft no mater how you want to dress it up.

The government doesn't print money. Banks create debt and we buy it. Buying and selling overpriced homes for unearned gains, demanding your "money" grows in equities and assets allows the banks to create more debt.

The demand for monetary wealth is the driver. The hoarding of monetary wealth whether it be "real" assets or shares prevents money flowing through the economy, furthering the need for more debt creation.

False economic beliefs and fear are the primary cause.

So the real question is who's doing the stealing? Who we think it is and whom it actually is may be worlds apart.

A medium of exchange is all it should've ever been. Instead it's been used for power and control.

The belief in storing value is the delusion.

The fear of not having enough now or in the future is the cause of our financial woes.

The demand for more is an addiction in each and every one of us and it's been used to perpetuate economic servitude.

Economic theory will not and cannot solve this issue.

We all have to question "what are we demanding?"

The divide and conquer game is being used to full effect.

Ignorance is bliss!

Fudged

4.9%. 5.9%, 6.9%

Coincidence or keeping the number low intentionally?

The data speaks load and clear.

If they are going to fudge it, why not 2%, exactly at the RBNZ mandate?

Or maybe 6.8% to not make it so obvious?

Does anyone believe this number when it is a basis of the manipulation to remove and replace anything that goes up too much in price.. A bit like removing companies and trusts from the definition of foreign buyers.

So you can be absolutely sure we will get the wrong policy response based on fudged numbers, OCR should be at least 6% already but the property lobby is driving the agenda... Slow motion train running down hill at the moment being held back by these fudged numbers but will surely accelerate and leave the tracks resulting in the inevitable disaster.

Beware NZ,our politicos and bureaucrats, who have been enriched by the state for ever while doing nothing, are now having to work for their money and showing their incompetence. Anyone can drive down a straight road. To get top dollar fom thE public purse, you need to be able to negotiate a few bends.

Brilliant. Construction costs and rents are the big domestic (non-tradeable) drivers of inflation. Please explain to me how increasing the cost of borrowing (a key input cost to construction and rent) is going to help.

The desire to capitalise falling discounted present values of future cash flows associated with residential property is diminished when interest rates start rising.

I understand that higher rates could discourage housing developers in the future - but the pipeline of building and construction work is huge with hundreds of publicly-funded projects. I just can't see costs coming down. Although I guess they might stabilise.

If prices stabilise for 12 months then there is no inflation.

Potentially by destroying credit confidence/lending and as a result significantly dropping inflated prices that we currently have (and destroying non-viable businesses and projects in the process). Yes it will be messy...but its already a train wreck now so why try to keep an old sick dog alive? (isn't it viewed as humane to put it out of its misery?)

I think you assume that prices can only ever go up - which appears to be the bias you view the world from where raising the OCR isn't the solution to imported inflation....yet the solution to imported deflation up to now has been dropping the OCR (to zero) which has resulted in creating this mess in the first place. You can't have it both ways/have your cake and eat it too - all that does/will do is create very distorted markets (which appears to be where we find ourselves).

Price is now more than ever a factor of what you can afford to spend. Interest rates determine the value of money. Low interest rates and money is everywhere and spent freely. Higher interest rates and money is saved. With higher interest rates and the inevitable housing crash, houses will flood the market and prices and rent will come down. Builders who cannot build new and compete with existing homes will stop building and the competition suckling up supply will fall away, and construction costs will fall too.

That is what is going to happen... transition from valueless money to valued money,,, very bad if you have debt, very good if you don't and are a saver. Governments should avoid these ups and downs... BUT that requires competence in both the government and the reserve bank.

Bank loan rates are still marginally below inflation for the shorter terms.

And they can only do that because the FFLp is giving banks money at a discount. That stops in June and that is when the pain will peak.

How much would the fuel excise cut (which is temporary) play into this as well?

Yes I would like to know the impact of that too - is it a ‘but for that’ cut it would be over 7?

I assume this quarter's numbers factor in the 25c drop in fuel tax, as that was effective before March 31.

Who's looking forward to the June numbers?

It does factor it in. So the real number would be considerably higher than it is currently.

And we’ve essentially banked the 25 c/L increase to be reapplied in q2/3 when the subsidy is removed.

Which may not be any time soon:

https://www.stuff.co.nz/business/128412382/minister-indicates-fuel-tax-…

Prices for the construction of new dwellings increased 18% in the March 2022 quarter compared with the March 2021 quarter, the largest increase recorded since the series began in 1985.

This part of the inflation problem will be fixed by Q4 2022. Because there wont be any new dwellings under construction. Except maybe by Kianga Ora. Unfortunately all of the employment associated with that construction will be gone to. Many of those workers are immigrants who will move to greener pastures. Putting more downward pressure on rents.

Maybe something like Kiwibuild could actually work well in that environment.

Strange how the results are 4.9% then 5.9% then 6.9%. I get the feeling there has been 'rounding down' going on.

Stats NZ always rounds down. We probably have double digit inflation after you account for all the arbitrary hedonic adjustments and unreasonable substitution of goods. The NZD is dog poop in terms of a store of value. They have butchered our currency in 10 years.

If you calculate the overall figure from the published weighting and index numbers you actually get to 7.02%!!

A rounding error I'm sure...

Probably changed the weighting last minute to get it under 7%. Didn't have time to update the published weighting.

Seems i am one of the last Bears left. If you look back at inflation, generally when there is a large run up in inflation there is always a cliff it falls off pretty soon afterwards.

I expect we are at peak or very near before we head into disinflation possibly into deflation at the end of next year.

US yields have inverted, high energy prices normally proceed recession.

Very interesting times we live in.

Good to have some inflation mixing things up, it got a little boring watching inflation dropping away for so many years. We needed some spice.

After years of quantitative easing and now a supply shortage overseas, keeping the inflation rate below 3% has become unrealistic. Attempts to achieve this via hiking interest rates pose a serious risk of causing havoc in the economy via a liquidity crisis.

The mandate of the Reserve Bank of 3% is no longer achievable. Money created ex nihilo has initially led to asset price inflation. It is now hitting consumer prices, fast and hard. This wave of inflation cannot be retained via raising the official cash rate. The supply shortage side of inflation is completely immune to interest rates anyway.

It is now crucial to protect the economy from a beginning recession that could lead to a crash, as indicated by property price moves.

The Australian central bank has left their official cash rate at 0.1%, as opposed to our rate that has been aggressively raised to 1.5%. Both approaches appear a bit extreme, but our approach poses a serious risk of initiating a waive of insolvencies.

Lol - perhaps we shouldn't have pushed to OCR to zero to solve the issue we had by importing deflation via globalisation?

And yet that is exactly what we have done....and have created massive debt/asset bubbles in the process (1980's through now).

You can't have it one way and then not the other. If you want to drop interest/mortgages rates to zero while we import deflation, then we need to raise interest/mortgages rates when we import inflation. Doing anything else will completely distort markets with prices that never reflect fundamentals and local incomes.

Ahh the good old privatise the gains and socialise the losses.

Stop copying and pasting this.

Mods can you delete Markus's account he has been spamming the above for days now. He isn't engaging in constructive discussion.

"He isn't engaging in constructive discussion." your in the wrong site mate?

donny11 - Are you the Chief of the Vested Interest Brigade ?

To be fair he did engage in a few earlier posts, although I think he equated house price falls with the fall of civilisation in NZ and a Mad Max style future within a couple of months. So not sure whether that falls within your definition of "constructive".

So..... we have to come up with a new way of distributing money, and living with less material stuff, whilst somehow ensuring our human needs and wellbeing are fulfilled.

The people and physical infrastructure will still exist, so this story of an economic crash is part of the problem.

Yes, there needs to be a cleaning out of inequities. Holding on to the status quo, busyness as usual, a return to "normal", and economic recovery doesn't solve any of it.

It's time to change our ways. We're being slapped upside the head in so many ways and still not learning.

'Permission to speak Mr Orr'.........

'Don't panic'........https://www.youtube.com/watch?v=nR0lOtdvqyg

We can all call bullshit on that number now as it always ends with a 9. How long are the people going to put up with this BS CPI index ? What happens when the fuel tax exemption ends ?

More interest rate rises. Houses will continue to soften in price. More listings as that happens as some of the fools who bought recently using debt will panic. One can not put a figure on it but house values in general will ease. Less buyers, more listings and day to day living costs getting higher and higher. As a country we are in a bit of a pickle really.

A lot of terraced housing popping up all over Auckland. I think some of these things will fall over.....

"soften" "ease" that real estate vernacular is hard to stop using, isn't it? Although I still have "prices will go sideways" to cross off on my RE lingo bingo card...

Inflation to the moon!

Still heading upwards. All we need now is the Chinese to lose control of Covid-19 and a poor northern hemisphere grain harvest.

Emergency lift to the OCR of another .5% out of cycle...?

After reading all the comments claiming the numbers are fudged I think i've identified the reason the price of tin and aluminium is at/near decade highs.

Demand from headwear suppliers!

There is fudged, and there is fudged.

Say we have four numbers (Calculated to 11 dp)

6.99999999998

6.98888888888

6.89999999999

6.88888888888

The average to 11dp is 6.944444444443

The average to 1dp is 6.9

Round the numbers (up or down to nearest 0.1) before averaging and you can end up with an average of 6.85 - 6.95.

Round the numbers (up or down to nearest 0.1) before and after averaging and all of a sudden you go from 6.8 - 7.0

Want to be really cheeky. Round down to the nearest whole number and the average is 6.0.

With a large enough data set you can get any number you want as an outcome. It all depends on a few small assumptions and a little bit of rounding.

"With a large enough data set you can get any number you want as an outcome. It all depends on a few small assumptions and a little bit of rounding."

Nice, I hope NZ stat have mathematicians who knows it very well and tweaked data to achieve desired result 4.9, 5.9, and 6.9 in the past few CPI results.

"Inflation hits 30-year high of 6.9%, but was lower than expected"

This comfort is similar to : Was expecting to lose eye sight on both eye but extremely lucky that have lost total vision in one eye and ONLY 60% in another eye so can can still know if it is night or day.

Be positive.

Is this some kind of conspiracy theory going on? First we find headlines in every paper in NZ that first home buyers are in for a rude shock because of inflation and increasing mortgage rates. Then we have headlines that we are touching 7%?

Now inflation numbers are 6.9%.. Is this kind of a balm on public, a feel good factor?

I see next month a 0.25% increase which would calm the nerves. But this is all artificial and I see inflation rising to 8-9% by October.

Someone is playing an inflation war in the world. See more aggressive stands by strong nations by July- August and rising inflation.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.