By Gareth Vaughan

ANZ New Zealand has not sought any form of government guarantee for loans in response to the economic impact of the coronavirus outbreak, but CEO Antonia Watson says she is keen to hear details of a working capital partnership between banks and the Government floated by Finance Minister Grant Robertson.

Speaking to interest.co.nz in a Double Shot interview, Watson said there was no specific message from major bank CEOs for Robertson as to what banks want from the Government at a meeting on Monday.

"The Minister mentioned that they are looking at some sort of working capital partnership. We will be hearing the details over the next couple of days so will be really interested in what that looks like. Because one concern that we have is that overlay of responsible lending and at what stage is a small business far enough down that track that it's not going to help. And having some government support with that might be useful," said Watson.

Asked whether this meant some form of government guarantee Watson said; "I think we'll find out over the next couple of days."

"We haven't asked for anything like that. That's something the Minister suggested and we're really open to hearing what he's thinking."

Cabinet agreed on Monday to the development of a “business continuity package” in response to the coronavirus outbreak. Included in this is a targeted wage subsidy scheme, training and redeployment options for employees affected by coronavirus, and options around how the Government could work with banks to support companies that face temporary credit constraints. Details are still being worked through. Robertson said it was important to get the timing and criteria right. He wouldn’t comment on the size of the package, saying this would depend on the criteria.

Watson said the bank bosses had assured Robertson they are "really concerned" to work with customers to get them through this period of market dislocation. She said banks are united around the message Robertson has helped emphasise being; "Contact us soon and early if you're feeling any stresses and strains because of the impact on your business of the virus."

"We're really willing to work with our customers to help them and there's a range of things that we can do like we do with a drought or anything else around loan restructuring and term deposits and those sorts of things," said Watson.

In terms of what ANZ NZ's hearing from customers, Watson said it's reasonably early days so it still feels very anecdotal. ANZ NZ is NZ's biggest bank with $170 billion of total assets as of December 31.

"Individual customers are coming to us. They are tending to be in the expected sectors, maybe forestry, retail, tourism. There's certainly no systemic themes that are coming through to us. I think that's the thing with this particular issue, with the virus, [is] that it will be horses for courses, there won't be one overall response. And I think that the Minister was very clear on that as well. That they're looking at very targeted responses because it depends on who you are and where you are what the impacts might be," said Watson.

'We're in a very good position from a liquidity and funding sense'

In terms of the strength of ANZ NZ against the backdrop of the international coronavirus outbreak and turmoil in financial markets, Watson said it's in a good position from a liquidity sense, which was one of the big issues for banks when the Global Financial Crisis (GFC) hit in 2008. Liquidity risk is the risk that an entity can't meet its financial obligations as they fall due. Banks can be vulnerable to liquidity risk as a result of what the Reserve Bank terms the maturity transformation role they play in the financial system. Retail banks borrow shorter-term or on-call deposits, while the major part of their lending is via long-term residential mortgages.

"Certainly from our bank's perspective we're in a good position from a liquidity sense, and that was one of the big issues in 2008. The availability of credit I guess there's two things. One is that you still want to lend responsibly. And the second one is we've had an interesting scenario this year appearing again where we've seen more confidence in borrowing. And I guess in the low interest rate environment we've seen lower deposit growth. So that could have an impact on credit ultimately [see more on this here]," Watson said.

She said there could also potentially be "a flight to the perceived security or the actual security of bank deposits."

"So we'll just watch that play out. But at the moment we're in a very good position from a liquidity and funding sense, which is great going into something like this when you are seeing market dislocation," said Watson.

Asked whether the strong liquidity position could hold up over several months if the economic situation worsens, she said we'll have to watch how it plays out but banks are much better prepared than they were pre-GFC.

"We are very well prepared for liquidity issues now. The new rules that came in after the GFC have put us in a really strong position. We've got enough liquidity to cover all of our offshore borrowings and/or all of our [funding] maturities for I think it's something like 18 months," Watson said.

"So I think that's something that people should take a lot of confidence in."

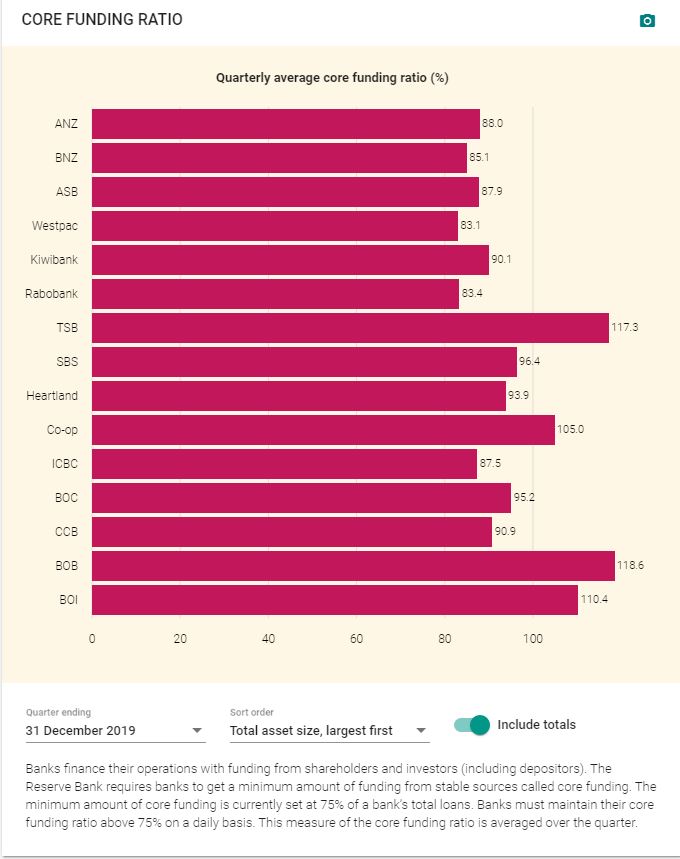

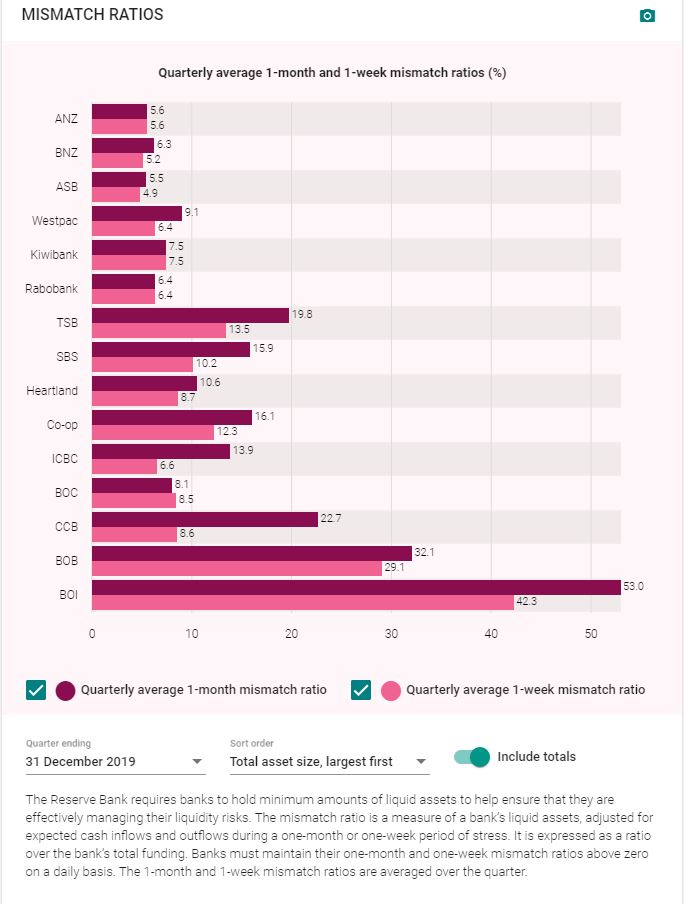

In 2010, in response to the GFC, the Reserve Bank imposed minimum prudential standards on banks aimed at addressing the degree of liquidity risk they take on, and their approach to managing that risk. These include minimum ratio requirements calculated from banks' financial data, rules and guidance on the risk management processes that banks should have in place to manage liquidity risk, and requirements for regular reporting to the Reserve Bank of data on their liquidity positions.

These include minimum one-week and one-month mismatch ratios, and the core funding ratio (CFR). The CFR is a comparison between an estimate of a bank's funding that is stable and can be assumed to stay in place for at least one year, and the core lending business of the bank that needs to be funded on a continuing basis. The minimum CFR has been set at 75% for banks.

"Our liquidity group meets regularly and they look at a range of things and decide how we are placed against them... And the value of those ratios is really playing out," Watson said.

"From a capital sense, a funding sense, a liquidity sense we learnt a lot from the Global Financial Crisis and we're in a very, very strong position on all of those now."

'New Zealand has got options'

In terms of NZ, she said the country is in a good position compared to many other countries because it has got options. These are due to relatively low net government debt, a little Official Cash Rate capacity with it currently at 1%, economic stimulus from a government infrastructure programme, being an exporter of food when people will still need to eat, and being a long way away from other countries and having control over our borders.

Asked whether she thinks New Zealand can avoid recession Watson said; "I think there's a wide range of parties that are very interested in doing that and they're working really well together and that's probably all we could ask for."

*The charts below come from the Reserve Bank.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

19 Comments

"So we'll just watch that play out. But at the moment we're in a very good position from a liquidity and funding sense, which is great going into something like this when you are seeing market dislocation," said Watson.

Given sticky bank deposits are unsecured bank IOUs created from purchasing a borrower's IOU there is obviously no funding issue because funds are not part of the equation. And these must match each other over the life of the unpaid borrower's IOU while the depositors spend the debtors' interest and principal payments over time. Which in reality are a fresh set of counterparty IOUs.

And some people have the temerity to suggest its all some sort of giant shell game trading promises to pay....

Gareth has a measured, respectful interview style. And Antonia Watson's poker face is iron-clad and I could sense the defense was tight. So no meaningful insights there (for me anyway).

As an aside, the ANZ share price looking rock solid on the ASX today. Mind you, is there anywhere in the world that backs and trusts its banks like NZ and Australia. They're an integral part of the fabric of society.

Working Cap Pship with banks. Spin it another way! The bwanksters who have been creaming ridiculous sized bonuses and bulging annual pay cheques now want to tap me for some of my tax payments.

The very people who got us into this asset bubble monster.

B-off and stand on your own two feet - like ma and pa struggle business is expected to do.

Yes, Captain Watson was deliberately oblique on what that actually means. But it's pretty damn obvious. The banking industry's charmed existence courtesy of the nation's serfs is clear to me.

Its election year, so hard to imagine taxpayers money going to the banks. Well overtly anyway.

Its election year, so hard to imagine taxpayers money going to the banks. Well overtly anyway.

All depends. Over the ditch, Scomo is donning his samaritan robes (hopefully without the Hillsong brand logo) and gearing up to divvy out public funds to the downtrodden (not that I personally disagree with that as it's better than rorting the system as the ruling elite have been doing for their own interests over there). Indirectly, the banks get a piece of the action.

That might be a vote winner. Its not seen as propping up the banks.

Note she says: "The new rules after the GFC have now put us in a really strong position to deal with things like these"

We have to make sure if National want to take an ax to regulations then we need to make sure they don't succumb to include financial regulations. Its always very tempting for a government to ax financial regulations as it will give a short term boost to the economy ( Part of Donald Trumps plan ). But we will always pay badly for it during times such as these.

True. Incidentally I think Captain Watson was favored by the former leader of the National Party for her rise to the top. GIven her professional career trajectory, she would be up for axing any regulation that stymies ANZ's progress in any way.

The last paragraph is the most important point.

Why do the powers insist on recession avoidance at all costs?

As much as it will hurt me, we do need a reset.

Can kicking again.

As a shareholder I'd just like to ask ANZ to just manage high-risk lending off the books over the next few quarters. The last thing we want is for a change in commodity prices to impact our bottom line.

Liquidity Event in 3, 2

'Government working capital support' ?

How does it sound juxtaposed against RBNZ's call for increasing the Capital/Reserves ?

Or is this another name for Bailout ? Cheeky as.

Working Capital???

Sounds like the govt will back bank created currency using govt assets.

Facism is corporate and state powers combining isn't it?

Immigration in the western world has boomed the last 10 years because of all the bank created leverage and debt associated with asset hyperinflation.

They have to keep pumping up the economic heroin or its game over. So much for economics 101 and price discovery. The market and economy is so detached from reality nothing is real. If we allowed the market to decide the real price of money we wouldn't be in this mess. The free market must be left to do its job. Rather than this centrally planned central bank ponzi scheme.

Your kiwi saver will be destroyed and the money you put in actually is transferred to someone else. Everything is a wealth transfer. It's rigged to eventually destroy the middle class. A crash of biblical scale is upon us.

Interesting this Bank: When came to CAR? they vehemently opposed, lobbying until Orr gave up from initial 5 to 7 years. But when the free market, showing signs of crunching their credits/bottom line? - suddenly, first quick smile extending hands to govt. hand out plans (aka tax payers burden) - off course, you can call/name it in so many ways.. coop, mou, agreements, partnerships.. etc. - But hell yea, what do you expect? JK/bwanker money still call the shot, but from the other side. BAU - nothing to see or report here.

'We're in a very good position from a liquidity and funding sense'

No s**t Sherlock. Having taken over a billion dollars in profit each year for the last 10 years.

And now they'll help people out a bit. Aren't they lovely?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.