New Zealand banks bid for just $200 million of the $2 billion on offer Friday morning at the Reserve Bank's first auction to support banking system liquidity as the coronavirus crisis continues battering financial markets.

The Reserve Bank offered $2 billion worth of three and six month loans to banks after announcing the Term Auction Facility (TAF) alongside other measures earlier on Friday. The Reserve Bank will lend to banks for up to 12 months, taking Government bonds, residential mortgage-backed securities, and other bonds as collateral.

"This basically ensures banks will be well-funded for the foreseeable future. This will prevent an increase in the cost of bank funding, which in turn will help ensure that short-term interest rates for businesses and households remain low," says Westpac NZ chief economist Dominick Stephens.

The TAF will be offered daily at 9.30am, offering loan terms of about three, six and 12 months. The Reserve Bank reserves the right to alter both the volume and maturity dates at its discretion, and says the facility will be reviewed in 12 months' time or sooner if demand diminishes. Friday's auction saw $200 million of bids accepted across three and six month loan terms at 0.26%.

"Banks currently have robust liquidity and funding positions and can manage short-term disruptions to offshore funding markets. The opening of the TAF will provide confidence that the Reserve Bank stands ready to support the market if needed," Reserve Bank Assistant Governor Christian Hawkesby says.

The Reserve Bank also says it's providing liquidity in the foreign exchange (FX) swap market, to ensure this form of funding can be accessed at rates near the Official Cash Rate (OCR) of 0.25%. Hawkesby says this activity will increase in coming weeks to support funding markets.

"Banks sometimes borrow money from offshore and swap the debt back to New Zealand dollars. In recent days the cost of performing this swap has exploded. Left unchecked, this could have caused an increase in the cost of funding New Zealand banks, which in turn could have led to higher interest rates in New Zealand. The RBNZ has essentially offered to facilitate some of those swap arrangements, which will keep the cost of overseas funding contained," says Stephens.

US dollar swap line established

Meanwhile the US Federal Reserve and the Reserve Bank have established a US$30 billion US dollar swap line. This will enable the Reserve Bank to borrow US dollars if it needs. The Fed has put these facilities in place with a number of central banks and describes them as temporary US dollar liquidity arrangements, or swap lines. They will be in place for at least six months, the Fed says.

"These facilities, like those already established between the Federal Reserve and other central banks, are designed to help lessen strains in global U.S. dollar funding markets, thereby mitigating the effects of these strains on the supply of credit to households and businesses, both domestically and abroad," the Fed says.

The other steps the Reserve Bank announced on Friday morning include it providing liquidity to the New Zealand government bond market to support the market functioning. Finally the Reserve Bank says to support the implementation of monetary policy, it's removing the allocated credit tiers for Exchange Settlement Account System (ESAS) account holders. This means all ESAS credit balances will now be remunerated at the OCR. Under the previous framework, banks were charged a penalty rate on deposits of cash balances above their allocated credit tiers.

Stephens says the ESAS move means the Reserve Bank is now paying the OCR on all cash balances banks hold at the Reserve Bank. Previously banks were paid a lower rate if they held large balances.

"This will give the RBNZ greater control over short-term interest rates, keeping them closer to the OCR," says Stephens.

In terms of the government bond market he says the Reserve Bank move there means it's now actively buying NZ Government Bonds on the open market, in an effort to provide liquidity.

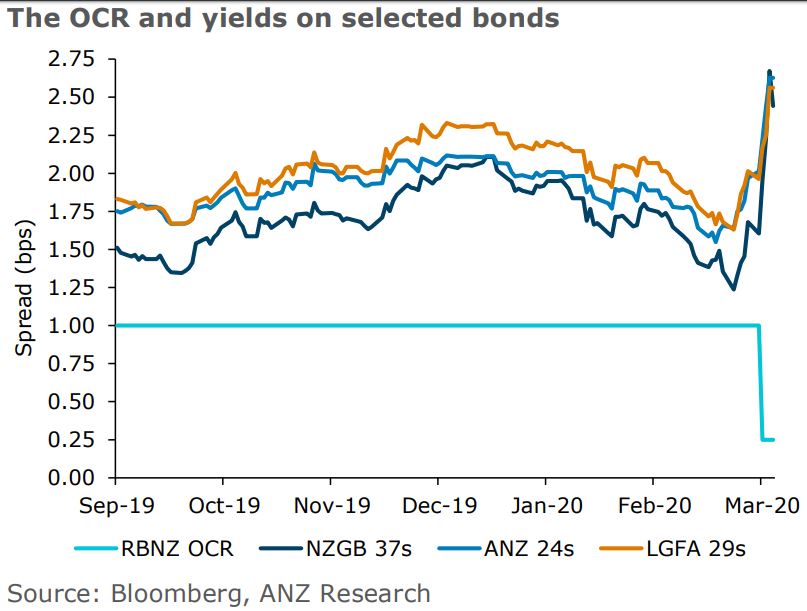

"However, the amount of liquidity provided seems tiny so far, and has had little effect on longer-term Government bond rates," Stephens says.

"As we noted yesterday [Thursday], the interest rate on New Zealand Government bonds has shot higher because bond market liquidity has dried up. Yesterday the NZ Government borrowed at 2.6% for 17 years, whereas last week the interest rate would have been 1.3%."

Hawkesby says the Reserve Bank is actively involved in financial markets to ensure smooth market functioning despite the global uncertainty from COVID-19 (coronavirus).

"Regular market operations continue to ensure there is ample liquidity in the financial system. The measures we are implementing today provide additional support to domestic financial markets. We will ensure our operations make financial markets operate smoothly,” Hawkesby says. "We are working in tandem with the banks, the wider financial market community, and the Government."

Additionally Hawkesby says the Reserve Bank has an established role to provide liquidity in the New Zealand dollar foreign exchange market in periods of illiquidity or dysfunction, and is operationally ready to undertake this role if required.

Bank economists still tipping QE

Despite the assistance announced by the central bank on Friday, bank economists are still expecting more.

ANZ NZ chief economist Sharon Zollner says in addition to Monday's move to cut the OCR 75 basis points to 0.25%, committing to keep it there for at least 12 months, and delaying increases in bank capital requirements, it's a long list of significant measures the Reserve Bank has now taken, consistent with the enormity of the problems. Zollner on Friday reiterated Thursday's call for large-scale asset purchases, or Quantitative Easing (QE).

"Large-scale intervention in the bond market is needed urgently. The Reserve Bank actually has a mandate to do this now, outside the scope of 'unconventional policy,' to ensure that the market can trade in a manner consistent with monetary policy settings. But over and above that, even more monetary easing is required in order to provide more stimulus, calm market jitters and ease credit strains," Zollner says.

"A move to large-scale asset purchases, quantitative easing, or QE, is needed very urgently, We expect QE to be announced very soon indeed, and it needs to be large given how dysfunctional markets are at present. We expect QE could be in the order of $15 billion to $20 billion per year. That’s big; somewhere in the order of 5-7% of GDP."

Stephens is also expecting QE.

"We suspect the RBNZ is going to have to begin a Quantitative Easing program very soon, similar to the Reserve Bank of Australia’s move yesterday. This would involve buying large quantities of Government bonds, which would reduce long-term Government bond rates," Stephens says.

"The other way to keep longer-term Government bond markets calm is for the New Zealand Government to ensure that any future stimulus measures are temporary. Markets need to be assured that the Government has a plausible path to repaying the large debt it is going to incur as it cushions the economy through the Covid-19 recession."

41 Comments

Sorry, Dominick. "Markets need to be assured that the Government has a plausible path to"....

The only Plausible Path this crew has, is how to spin their responses well enough to get re-elected....that's as far as their planning horizon extends.

Let's Do This!

Zorro's worried his 10% house price rise prediction will look really stupid

The bonds will always be repaid as long as the treasuey can tap some keystrokes into an excel spreadsheet and the bonds are in nz dollars. The rb can control yields via qe whenever it choses. Sure, excessive stimulus could create inflation but in nominal terms the bonds will be repaid. Excessive inflation is unlikely given the shock to demand we are in. Stop pushing the austerity barrow. It's the last thing we need.

I agree, inflation unlikely in the short term. But governments all over the world keep backing themselves into a debt trap. Inflation will be the only way after that. I think we will see annual inflation peaking over 10% before the decade is over.

Interested in other viewpoints.

So you wouldn't take a $500,000 mortgage to buy the 'average' NZ house right now? (guessing if inflation 10%, where will interest rates be?)

Assuming 10% inflation and 1% interest on mortgages by the end of the decade... I'd like to take out a $2 million loan for my beach house, please!

Inflation will come if spending from any source G I C or X outstrips the productive capacity of the economy. That is unlikely to happen for a long time. Look at Japan with its massive public debt and ongoing deficits and low inflation.

What bonds are likely to be QE'ed if the RBNZ caves to the banks? (and what's the best way for a retail investor to go about buying some?)

I can't see this issue going away as some of the longer bond yields are looking much closer to deposit rates.

Edit: Anyone got any ideas on why bond yields are so high? Is that no one got any money or do they just believe our currency is on a one way track down. Does our 20 percent GDP to debt count for nothing?

I only watch specific US Treasuries. The 10 year is hilarious and the short dated ones have gone to zero or less.

What happened with the 10 years is people sold shares and bought bonds. They when it got worse they wanted to shift to cash so they sold bonds causing 10 years to go from 0.5% to 1.2% rapidly.

The short dated bonds are being used as collateral for Fed repos. At the same time some of the supposedly non-junk corporate bonds in the US have been repriced as junk so the interest rates have shot up as they are being dumped to buy Treasuries so hedge funds can get cash instead. There's a complex storm of transactions going on the US and no one has a complete picture.

I don't follow local bonds so I have no idea what's going on with them.

https://www.interest.co.nz/charts/interest-rates/government-bond-rates

I think this correct page.

10 years at 1.63% and 5 year is at 1.19 both just shot up this week after the OCR cut. This will be seriously limiting any cuts to deposits and mortgages especially if it goes a little higher.

And then there was this but I don't know if of when that yield will be available to retail investors (I would break my TD for this):

https://www.interest.co.nz/bonds/104147/nz-govt-bond-tender-717-weighte…

Someone is dumping bonds, or the liquidity has dropped. I'm wondering how many people are overreacting to seeing the changes in their Kiwisaver accounts. Denominating them in NZD is not good for people who don't understand markets. Are we having a flight to cash here?

Are Banks contrived carry trades really the pressing problem?

Sounds like a couple of derivative books are cooked.

Don't confuse a banks corporate survival and a broad system thing.

Bad luck for the corporate end borrower that they meet the all singing derivative salesfolk.

Think of them the transactions as synthetic Swiss Franc Loans, (BNZF, DFC, EuroNational, FayR etc.... ).

There is the non-trivial issue that currency linked loans haven't been done for decades, but don't let me stop you.

The banks don't want to buy it. They want to get it given to them.

Not a very consoling greeting from Rabobank when trying to move some funds about!

"We're sorry, an error occurred.

The page you are trying to access is temporarily unavailable due to a technical error."

The Bank Of England itself tells us that banks don't borrow to fund their lending, that no reserves are lent and that loans create deposits, as explained in their bulletin here.

https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

Where do bank reserves come from? The government creates them through its spending as it creates new currency when it spends. When the government borrows it is only borrowing back money it has previously created, spending must come first before taxing and borrowing. Listen here to economist Stephanie Kelton explain it.

https://www.youtube.com/watch?v=WS9nP-BKa3M

Looking at US deficit issue can be very misleading. US has an exceptional position in the world that its currency is not only the currency of its own national but the currency of the world trade. As long as your total (including import) spending is all in your own currency, then the equation is true, all the deficit in Government budget is surplus in the non-government sector. However no other country can do what US does. They cannot pay their foreign trade with their own currency (what US does). They will need to get USD for that. So if the have trading deficit, the deficit spending in those government does not mean surplus in their national saving. It means their currency is being devalued. The difference between deficit in Zimbawe and US is that. Sure, Zimbawe central bank will never go bankrupt (unless the country has USD loans to repay! because they will not accept worthless Zimbawe currency for it) no matter what how much more money they print. But what they can get with it in an economy that does not produce anything? nothing.

So refreshing to read something sensible

Not according to Stephanie Kelton and other economists such as Bill Mitchell, any country that issues and spends in its own currency and doesn't borrow in other currencies operates like this. NZ has been referred to by them more than once. We may trade in US Dollars but we can only buy those dollars with our own currency which someone ends up holding so there is no real difference. The three sectors to the economy must always net to zero, a foreign sector surplus (current account deficit) plus a government surplus must equal a private sector deficit, (S-I) + (M-X) + (T-G) =0 . Also stock flow consistent modeling shows that government debt must equal private saving. (Wynne Godley)

Zimbabwe had a massive supply shock through mismanagement of agriculture when trying to right colonial wrongs. If you print money with decimated production you get hyperinflation. The situation in sovereign currency issuing nations like nz who run persistent current account deficits is very different. Sensible ongoing government deficits can in our case accommodate foreign and domestic savings desires whilst ensuring enough spending to allow genuine full employment. See Japan.

A government deficit and a country trade surplus or deficit must be looked together. When there is a teade deficit, it means that you will need USD to pay for the greater value of your imports. How do you get that? Borrowing in USD not in NZD. And you will need to get USD from your exports to pay that. So eithet the nz gov or its private citizen end up owning USD to foreigners no amount of nzd will cover that. Nz will need to produce more goods that others can accept. In this scenario all deficit spending does is devalue nzd and incewase cpi.

And so every 10 years we're just going to bail out the banks are we? They lend like drunken sailors between 2012 and 2016, driving up asset prices.

And then when the sh*t hits the fan, they've got the gall to say "Oh yes, the RBNZ has an obligation to implement QE" Which translates to "We've screwed up, but we don't want to go out of business, so save us please."

https://debtmanagement.treasury.govt.nz/tender/nominal-bond-tender-717

I don't know anything about bond tenders but DC's analysis last night was that 2.56% yielding government bonds are being settled next week. If that yield becomes available to depositors then deposits and mortgages will have to go up. I guess the reserve bank has some responsibility and mandate to enforce the OCR even if devalues our dollar and will cause no end of problems in the future.

Why borrow at the TAF (FAT) ... when they will buy all your junk through asset purchases?

Gotta keep the banking overlords record profits income via asset ponzi protected. I really wonder if all the retired folk trying to live off their hard earned saving's actually realize that Winston is a party to destroying their life's work/savings.

Something to think about.

Shows that there is funding stress in the financial system. If the banks are facing liquidity stress, they are able to access liquidity from the RBNZ.

Now what about those that are unable to access liquidity from the RBNZ such as a non bank?

1) Will a non bank be forced to sell assets (i.e loans) at depressed prices to obtain liquidity?

2) New borrowers - As a result of funding stresses, non banks may be unable to raise funds at a reasonable cost (or at all) and non banks may be reluctant to issue new loans (such as to fund property development, property & investment)? These can be bullet payment type loans, (not P&I loans). This may result in contraction of credit by non banks. Property investors may now be unable to finance purchases, property traders may be unable to finance their purchasers, property developers may have difficulty with existing projects under development.

3) Existing borrowers - If an existing borrower with a non bank is expecting to roll over their loan with the non bank, will the non bank refinance the loan? or demand payment? What happens to the borrower from the non bank who is unable to refinance with the non bank and now needs cash to repay the loan? Where will the borrower get the cash to repay the loan?

i) for property investors, they may sell the property?

ii) for property developers who are in the middle of their project and need the next tranche of construction finance? will the non bank be able to finance their next tranche?

Unexpected financial stresses create potential credit crunches, and catch out those with high amounts of debt suddenly and unexpectedly.

But this wasn’t obvious from the GFC - yet we modelled the same behaviour and then if you called people out for it you got labelled a DGM?

Many of the next generation have entered the workforce and may not have experienced firsthand the GFC. That would be many who are aged say between 18 to early 30's. Most are also unlikely to have learnt from history.

Also many who did experience the GFC, may not have been affected personally, so remain unaware. Or they may have entered into property only after the GFC. I recall going to a property market update given by Tony Alexander in 2016 - there were so many aged in their 50's and older in attendance. Went to watch a property auction at Barfoots to see the bidding frenzies going on at that time and the FOMO.

Also went to a property mentor workshop in Auckland in late 2016 to see what was going on. Some fellow attendees at the property mentor workshop were people were in their late 50's with lots of equity in their homes (due to large price rises), who were being persuaded by property mentors to take on debt by leveraging on their home and use the funds to purchase investment property so as to provide an income for their retirement. One of the potential students was nearing retirement from his company accountant job and his wife (so they are financially literate but did not know how to value residential property assets beyond the comparable transaction method commonly used for real estate). A lot of personal success stories of property investors who owned multiple investment properties financed using equity release / deposit recycling techniques were trotted out to persuade them that it was a good idea. They were told there is a shortage of houses in Auckland, there is inward immigration, property prices have doubled every 10 years for the last 50 years in Auckland, so property prices can be expected to double every 10 years into the future. Property mentors were charging students $25,000.

I believe that people should be provided with information from both perspectives so that they can make a fully informed choice / decision. Most of the media gives a one sided perspective due to their vested financial interests, so people often do not hear a different viewpoint.

All you can do is provide the information, so that they can make a fully informed decision. Ignore the name calling - that disrespectful behaviour is an indication of their mental maturity level - people resort to name calling if they are unable to express their viewpoint clearly, unable to understand the points that you are highlighting, or unable to provide adequate counter points to the point that you raise.

If people choose to ignore the warnings, that is entirely their choice. However they must know that they cannot choose the consequences of their choice.

Your warnings have resulted in some readers on interest.co.nz who have acted. We can only help those who choose to help themselves.

Anecdotal story.

Saw an property investor applicant for a loan from a non bank to buy another property.

The non bank has raised their interest rates to new borrowers.

At the higher interest rate, does the property investment still make economic sense?

New Zealand banks bid for just $200 million of the $2 billion on offer Friday morning at the Reserve Bank's first auction to support banking system liquidity as the coronavirus crisis continues battering financial markets.

Hmmmm .... 10% uptake - do the banks have the necessary collateral or don't they really need the funding? Same happened when the Fed recently fired off a "bazooka".

The reactive Fed continues to play catch-up, fighting a battle it is ill-suited to handle given its outdated tools and intellectual framework. Jay Powell’s not fighting with one arm tied behind his back, he’s over across the street making sure there are enough light bulbs for people to use during the day.

FRBNY’s big announcement has been boiled down into wickedly small potatoes. Two auctions, half a trillion each, those along with a coming third were together the “bazooka” aimed at calming everyone down. Dealers bid for $78.4 billion of the first one and a paltry $17.0 billion in today’s. Yes, a total of $95.4 billion out of a possible $1 trillion, or less than 10% of what was made available.

As I wrote yesterday after the first shot of their dud-zooka:

Either things aren’t nearly as bad as they seem (literally no one is buying that scenario), or something is wrong in bank reserve-land. Perhaps dealers just don’t want them, or maybe they don’t have the spare collateral to post for them.

With the way now UST coupons are behaving, very 2008-ish, I seriously, seriously doubt it’s the first one. A crisis is upon us, the scale of which we won’t know for some time, and no one wants the Fed’s “money.” Link

Maybe the money is too expensive..... if it is then we could see banks liquidity dry up, as has been reported in the US.

Contrast this to Air NZ taking money at 6-8%. The Banks will make a good profit out of onlending at a juicy margin, won't they ?

I agree with this move to avoid a total collapse.

Lending is going to tighten as jobs get lost and loan default, if interest rates were to explode as well it would be catastrophic

Govt. and corp credit yields are going to be bludgeoned lower sooner or later.

And so once again banksters never need to worry as central banks will be there to rescue them. By contrast the banks won’t be there for the mortgage defaulters.

Both of them Gareth, pretend to buy bond.. but liked to administer the QE II (not our current head of state)

Just thinking random thoughts as I drift off to sleep:

Look at the yields available on shares at the moment: very tempting 5% to 15% a lot of them, (admittedly based on pre-virus earnings). How much will the earnings of these companies decline by over the next months and years?

Now share values have fallen about 20% from pre-virus values because of the virus.

In the 1929~1936 Great Depression American stocks fell 80% to only 20% of their value.

I can't see any reason why interest rates won't stay low and even fall lower.

So, people with term deposits expiring in the future will have to decide whether to reinvest their money in the bank at virtually 0% interest and hope just to preserve their principal despite the possibility of the bank going bust just like happened in the Great Depression, and there being no bank insurance, only an untested OBR government intervention, a purportedly partial government bailout. Hmmmmm......

If the plague is dealt a death blow in the near future, say 3 to 6 months, then putting your money, or some of it, into shares will be a good idea..... zzzzz........zzzzzzz.........zzzzzzzz.......zzzzzzzzz

I mean commerce will have to continue, farms will still make food which supermarkets will buy for citizens to consume. Society will get by.... it won't come to a full stop will it?

What have I got to protect me and my family such as it is? They say in the Black Death Plague of 1351 society did stop and the physically strong forcibly took the food from the weak. Is this the real reason some people insist on their rights to own guns, so the weak can protect themselves from the strong in such circumstances.

They're coming through the back door now! Hellllp ....I'm paralysed and sweating!...What What............ the.......Phew!...What the.....I'm sorry it seems I've just awoken from a horrible nightmare!

streetwise. The issue that scares Reserve Banks is deflation especially when an economy is dependent on it for growth, like NZ is, on increasing the debt bubble. When money in the bank earns nothing then the next best investment is to pay off debt.

yep, the stuff of nightmares indeed.

So no independent thinking here, just following the US Fed's action. Oil prices plummeting and US 10 year bond yield below 1% again spells big trouble in the markets. What are they trying to achieve. You can't solve a massive debt problem with more debt. Just off to Fantasyland now to stock up on fairy dust.

We are about to face a huge demand shock as people stop spending. This will be highly deflationary, which is very bad for NZ which has huge household debt. This opens up massive fiscal space for the government to spend new money into the economy without causing inflation. It needs to go to people though, not corporations, so we can get out of the coming debt-deflation recession.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.