The Reserve Bank’s (RBNZ) seemingly hawkish decision to pencil in interest rate hikes from as early as September next year has sent the New Zealand dollar almost a cent higher against the US, and caused swap rates to rise.

ANZ senior strategist David Croy believes this is where rates will stay, while BNZ head of research Stephen Toplis says the strong market reaction isn’t “excessive”.

Toplis acknowledged the RBNZ was always going to have to walk a tightrope in its quarterly Monetary Policy Statement (MPS) released on Wednesday; recognising inflationary pressures without prompting a premature tightening of financial conditions.

“What the Bank has done should be seen in the context of positioning to remove the emergency stimulus that was provided to protect the economy as it was clobbered by COVID,” Toplis said.

“It should not yet be perceived as representing any urgency to normalise monetary conditions.”

Orr warns mortgage holders

RBNZ Governor Adrian Orr was conscious of striking the right balance in the press conference following the release of the MPS.

On the one hand, he stressed projected Official Cash Rate (OCR) hikes were “highly conditional” and a lot could happen before mid-next year.

On the other hand, he issued existing and prospective mortgage holders with a stark warning: “Think in a long-term sense when you’re considering mortgages; when you’re considering buying.

“Don’t get excited about the current mortgage rate. Think about what mortgage rates might look like on average through time…

“Interest rates are very low and certainly below what we would consider a neutral interest rate globally… Be wary around your ability to service a mortgage.”

Dovish language splattered between hawkish projections

The RBNZ walked this tightrope in its Statement too.

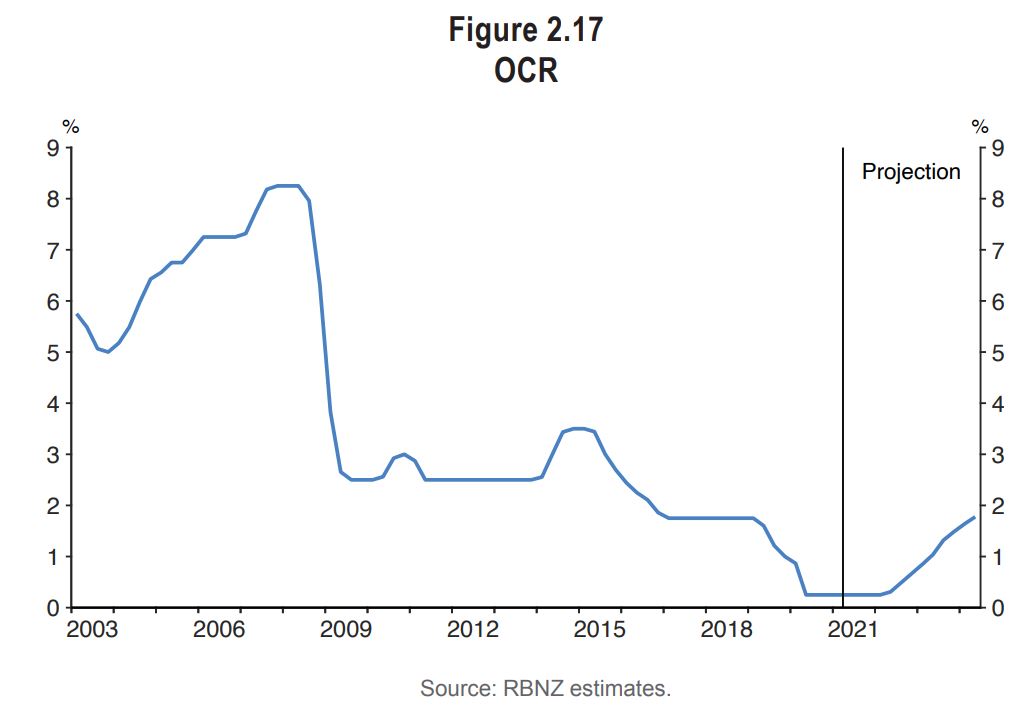

Notably, it reinstated its OCR outlook. While economists were betting on it lifting the OCR from 0.25% next year, they didn’t expect it to project 150 basis points of rises through to 2024.

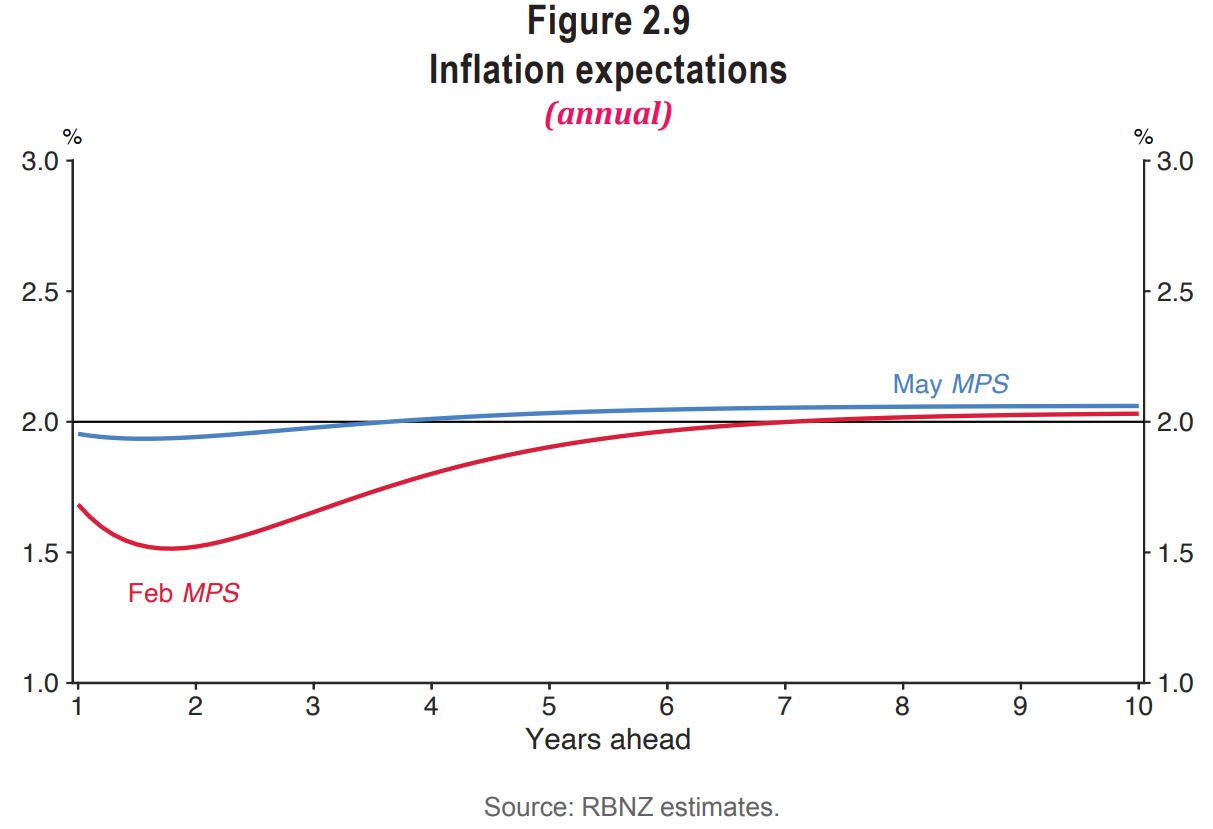

The RBNZ also revised up its near-term inflation expectations from its February MPS, recognising higher commodity prices, the strength of the construction and housing sectors, capacity constraints, high oil prices and disruptions to global supply chains.

As for its other target - employment - it pointed to the "maximum sustainable" level possibly being lower than during normal times.

"The skills of those who lost their jobs in industries such as tourism are not necessarily well matched to sectors demanding more workers," the RBNZ said.

"Until demand returns in tourism-related industries, the level of employment that is sustainable without generating inflationary pressures is likely to be lower.

"It is unclear whether, or how quickly, maximum sustainable employment will return to its pre-COVID-19 level."

While markets focussed on the RBNZ’s hawkish projections, its introductory comments repeated dovish phrases used through the COVID-19 crisis around it taking a “least regrets” approach towards loosening monetary policy, and requiring “considerable time and patience” for inflation to be “sustained” at the 2% midpoint of its target.

The RBNZ also coined some inflationary pressures “temporary” and “expected to abate over the course of the year”.

Some economists bring forward OCR hike forecasts to May

The MPS prompted ASB and Kiwibank economists to bring forward their projections for an OCR hike to May. Meanwhile BNZ economists maintained their projection for a hike in May, and ANZ economists upheld theirs for August.

Westpac economists took a completely different view. They believed the RBNZ was overstating the tightness in the labour market in the face of uncertainty around border and immigration settings. They held their view the OCR will only be hiked in 2024.

Economists generally believe the RBNZ won’t be able to start hiking the OCR until it winds down its Large-Scale-Asset Purchase (LSAP) programme.

By most of them forecasting hikes before the LSAP programme is due to end in June next year, they’re suggesting it could be wound down early.

Orr reiterated both the LSAP programme and Funding for Lending Programme will remain in place until June 2022, as planned.

The RBNZ did however acknowledge it won’t reach the $100 billion limit on the LSAP programme, as Treasury isn’t issuing as many New Zealand Government Bonds for it to buy, as forecast last year.

To date, the RBNZ has figuratively printed about $53 billion to buy bonds on the secondary market via the LSAP programme.

Market reaction

Coming back to the market reaction, Croy believed the New Zealand dollar and wholesale interest rates would remain elevated on the back of the MPS.

Pricing is all about relativity and the RBNZ’s hawkish position is a stand-out globally.

However, Croy suggested “the tail may wag the dog”. In other words, the RBNZ may cause markets to bet more on other central banks following its hawkish turn.

78 Comments

Well worth repeating for both current mortgage holders and potential FHB to note.

Orr: “Think in a long-term sense when you’re considering mortgages; when you’re considering buying. Don’t get excited about the current mortgage rate. Think about what mortgage rates might look like on average through time… Because globally interest rates are very low and certainly below what we would consider a neutral interest rate globally… Be wary around your ability to service a mortgage.”

Yet on the other hand he's got no worries about house price inflation and continuing to lock out FHBs

Of course It bothers him, but it's not the primary objective. The primary objective is keeping the nz economic engine chugging along in spite of the global pandemic. Also to avoid getting our dollar out of sync by doing anything vastly different to other central banks.

Hey now, we dont like logic and reason around here.

The logic is that if house prices keep rising at the current rate then NOBODY will be a able to take out a new home loan, is that not killing two birds with one stone ? Job done no new mortgages at all so nobody will get into trouble when rates rise. Rates rises way to slow, OCR should already be at 1%.

Also to avoid getting our dollar out of sync by doing anything vastly different to other central banks.

This. I sometimes wonder what it would be like for little old NZ if the rbnz ran their books more like a household, and less like a printer.

What do you think this would mean for NZD?

You wonder why they haven't been warning them for a long time. Even 8 % is low, but some banks were apparently stress testing borrowers in the 5-6% range. Some of these borrowers will have never experienced interest rate rises before.

So sit on the sidelines and watch houses pump another 100k between now and Sept next year, until interest rates rise and there is a flattening or tiny correction

Yes FHB have been forced to take either the risky position of over leveraging, or the equally risky position of waiting until they have saved a higher deposit and possibly being forever a renter.

No option of a safe decision unless they consider moving overseas to somewhere more affordable. The boomers will only get to see their kids and grandkids via Skype, until the day comes when the kids fly home for the week to move them into a rest home. Nobody should be thrilled with high house prices.

NZD moved strongly today up about 1.2% against USD. Team of 5 million punching above its weight. Kia kaha.

.

It's like Orr's trying to create FOMO - get in and get cheap mortgage rates while they last. I suspect more people are going to rush into the market and get low long term rates on the back of today's announcement.

Well if you are still paying ridiculous rent costs and you can get 1.79% at ASB why on earth wouldn’t you.

Longer term everything is up including rent that does nothing for your life

1.79% if you build. How much does land cost & the build in major city? How long does a build take? You have to pay rent at the same time as build cost/mortgage... Sound good?

And it's a floating rate.

Depends on the build terms actually, where not,

Yep sounds pretty good to me.

Cheaper than buying an old house and fixing it up.

Not really.

Cost of construction and materials are rapidly rising as we speak. Lumber shortages and prices going up

Skilled tradesmen will be leaving in droves for better money overseas.

He is actually saying the exact opposite. Literally warning FHBs not to be tempted by artificially low rates, and people buying now should enter the market cautiously with a long view.

"get in and get cheap mortgage rates while they last." frankly, only idiots would jump in with that mindset given the low rates are only for 1 to 3 year fixed rate loans.

Wait and watch...If you see house prices continue to get away from you and rates low for a 'limited time', what do you do?

I would think about long term, not many can pay off their huge mortgage after 5 years. Yes you still can fix a fairly low rate now for 5 years. But what are you going to do after 5 years? How is your house valued by then? These are the questions FHB and investors need to think about. Houses are in for long terms.

Buy only if you need to, but take on the smallest amount of debt possible. Still be prepared to take advantage (more leverage) of any future downturn. Don't go all in.

Not at all Nifty, quite the opposite. Literally warning FHBs not to be tempted by artificially low rates, and people buying now should enter the market cautiously with a long view.

Serious question, who interviewed Orr for his current role?

Seeing as how so many (mostly right leaning) commenters on here seem to hate Adrian Orr and the Labour government, could you elaborate on your statement? It would be good to understand your reasoning as to why you're making this blanket comment.

I voted for Jacinda at the last election and have been rewarded with a $500,000 tax free unrealised gain on my home. I can imagine those without a home would question her competence and that of Orr. But then I suspect you are just being political. Read the room. FHB are apoplectic.

Plus nice growth in NZX. Irony is making more money in the 3 1/2 year Labour term than in any equivalent period previously but being a rabid right leaning voter. QE has worked a treat for the 'Haves' but screwed the 'Have nots.'

I never understood wealthy people who voted left until the past 12 months. But now I get it. It’s like some combination of left policies and unintended consequences that create arbitrage opportunities for the wealthy to accelerate the growth but those opportunities cannot be taken advantage of by those who do not have capital.

"Ask not what you can do for country, ask only what you can loot from your country (and future generations)"

"It's only a rort if you are not in on it"

----------------------------------------------------

"Greed is good" - Gordon Gekko

Worthy of a general reply - Labour aren't left. It's also extremely convenient to ignore the 40 years of, yes, you guessed it, neoliberal policies that brought us to this point as well. But then that would expose the issue as being complex, which we're all aware it is. I don't have access to the interest archives - were you all making the same points about the key government?

All I see is a bunch of self interest keen to keep the status quo

Wealth is relative. I’d call myself financially comfortable. I still work for a salary. I voted Labour because I didn’t think National deserved my vote and I wanted Labour to not rely on the Greens.

You mean left leaning commenters hate A Orr ? (you said right leaning)

In his early days, Orr seemed the breath of fresh air. Often the maverick, he spoke out against the then policies and rationales presented, even though he wasn't stepping too far from the throne. Additionally he showed that he had a sense of humour, a bit of a rarity in that position. Funny - today that humour seems to be dead and buried, has he has learnt that no matter how good or powerful he might think he is, the real world will still deal out lessons in humility.

Orr looks to have 10 years in 3 and a bit years.

The Reserve Bank Board.

“Following the Reserve Bank Board’s unanimous recommendation to me, I have appointed Adrian Orr for a five-year term at the completion of Acting Governor Grant Spencer’s term,” Grant Robertson says.

https://www.rbnz.govt.nz/news/2017/12/adrian-orr-appointed-as-new-reser…

Groat

"Serious question, who interviewed Orr for his current role?"

Two serious responses:

Firstly, a question that is not serious as it is not Orr who makes decisions, rather a committee, and

Secondly you simply see RBNZ actions over the past year as having a singular consequence and are not seemingly able to see nor acknowledge (nor debate) those.

Still warning, No action.

Did Mr Orr had any clear response to questions on housing at today's press brief.

Actually today he reconfirmed again that it his not his job to worry about housing crisis but his actions / inactions does effect housing market, so how could he ....

Actually today he reconfirmed again that it his not his job to worry about housing crisis

Correct. Not his problem as he constantly reiterates. Only as it relates to financial stability.

But that didn't stop the journos from focusing on housing. They can see through the BS I suspect.

How come not his job. It is his action that effects housing market and he is the pioneer of current housing ponzi by reducing interest rate and removing LVR.

Reducing interest can understand but rushing to remove LVR overnight and now supporting speculators with interest only loan.

He gets away as no journalist counter him. Did any media asked him about DTI and Interest Only. Why did he not announced on 5th May, What he did today, What was he waiting for. Fact is both Mr Orr and Robertson playing with FHB. Check media, No one has highlighted shy, he created a hype for DTI and Interest Only. Have advised DTI to Robertson but their is nothing new to it.

House prices are outside the mandate (outside financial stability). Watch the press conference. Journos stepped up to the plate (within their boundaries).

Unfortunately boundaries are too limited.

To ask legitimate question, their should be no boundaries and politness ( not rude but firm and persistance) specially when one can see through the hollow response but than here most media and experts too are a part of the elite club.

Are you saying they're only therefor the cheese rolls?

My job is to push this button, but where the cruise missile hits is not my mandate.

That's why this system has huge flaws. Housing is definitely heavily related to our financial stability. But the tricky part is, we don't see it or feel it until it gets to a ridiculous level of risk with some kind of "black swan" event to pop the bubble. So these RBNZ fellas will just keep their eyes closed until that time. It's all politics.

I think rates might blip up but they will stay down or go lower shortly after until we are get to the point of a UBI being pretty common around the world. The deflationary forces around the globe are way too high. Of course thats just my 2c tho

There are no 'tools' - that is copying a physical activity, so as to appear 'real'. Real stuff is done with tools, just as real investment is of time, energy and resources - not debt-issued digits.

No Central Banker - here or anywhere - will ever dare REALLY lift interest-rates again. They will crash their so-called 'economies'. No Central Banker will ever see the current debt 'repaid', and to attempt to inflate said debt away is so far removed from current understanding of the relationship between a dollar, and the resources/energy it expects to buy, that it's a joke. They're painted into a corner and opening a new can every day.

https://www.amazon.com/Blip-Humanitys-self-terminating-experiment-indus…

Download it, read it, and weep. Then start asking questions......

Mad max, but in EVs. Witness me!

pdk,

I have just ordered it. I have now read that mining report several times and forwarded it to an academic friend in the US, who is also a consultant to the Federal Reserve of Chicago on the automobile industry. He has been asked to be part of a study on EVs.

I think that your posts, always on this issue, have started to have an effect on my thinking. I am going to become better informed and this book will a good starting point. Perhaps where you and i still differ is on when a tipping point may be reached. based on my knowledge of psychology, I think the day of reckoning will be pushed further out than you might believe.

“Don’t get excited about the current mortgage rate. Think about what mortgage rates might look like on average through time…"

Reminds me of the warnings on the edges of cigarette packets in the 80s. Smokers gonna smoke..

At least he can say he tried to warn people from his low interest drugs

He also said house price growth will grind to a halt. Why has that not been reported?

Because it's not an issue. The only issue is if they fall. Then the sheeple might get the fear and the house of cards falls.

Try doing the numbers as on a rental when there is no, or very low capital growth.

They only work if you can put rents up a lot, or if prices fall a lot, or some magic combo of the two.

And Robertson has said rents are not to go up.

DP

PM have put kiwis high on hopium "sustained moderation" & now this addiction will lead to don't know what.

Why Orr came back from sick leave better pass on the message of no change from his subordinates, as we only expects warnings from these drumheads, I don't know what data he is waiting for, how hard reality need to hit before current govt wake up.

Next time by any chance if they even feel that house price is falling again they remove LVR, open foreign investment & can also take interest to negative, there is no going back from here.

If I was a FHB, I would be shaking my head. The Reserve Bank is handing out cheap money, but saying perhaps it's not the right time to spend it.

Market is definitely losing its frenzy if not cooling. A house in Wellington that had listed in late March for $2.4M sold yesterday for just $2.0M. A number of houses that failed to sell at tender and then listed with a price have been taking anywhere between 50-100K off the listed price to get them sold. Whilst houses are still going for high prices - in most cases 300-400K over RV's - fewer are going above their valuations and the ridiculous prices seen in Feb and Mar have definitely gone away. Doesn't mean real estate agents still aren't listing at ridiculous prices but these houses certainly aren't selling in a hurry anymore

Reduced number of sales but high prices. The usual scenario, Kiwis stop selling their houses when they don't think they can get enough for it. Even at very high prices.

Perhaps the landlords who have had enough of Robertson's bullying cashed out and took the profit. I did, and got an inflated price which was crazy but useful for me. It was supposed to be a long term savings plan not a speculative investment, but Robertson made me fit the definition of a speculator. I was outside the bright line, and didn't re buy, or sell another.

The buyer is doing work to it so the house is unoccupied and has been for 3 months. That tenant lost their home and had to move in with other family because they could not find a place to live, their rent was more than $100/wk cheaper than other similar but smaller houses. Certainly not what Robbo hoped for I imagine.

Haven't seen this level of jawboning since Maui hauled up Te Ika.

Government attacks housing market with a sledge hammer in terms of investor deductibility whilst RBNZ does its best to continue to overheat it after lighting a bonfire under it already.

Would useful if they worked together

Did someone forget to tell Grant and Treasury who forecasted no lift in the OCR until 2024/25 as a key plank of their budget forecasts?

One economist I watched raised this as an issue on Budget day, together with inflation pegged below 2% in every period other than 2021 (only around 2.5%).

I work in the grocery industry, seeing all price increases around the 10% mark at present. Every supplier to our factory is 8-15%, ocean freight is up 300% and getting worse, commodity raw materials at record prices for the foreseeable future.

What is going to happen to Fonterra Brands with milk price to farmers hitting $8 and what will this mean for your bottle of milk or block of cheese?

How will inflation stay at 2% when prices are lifting in most of the 11 CPI groups: groceries spike, utilities up 30%, building materials scarce and rising fast, fuel is back to pre COVID pricing, cars can't be sourced so won't be discounted, ingredients are unavailable, and household goods like fridges/laptops are long delayed and in limited supply?

The answer is simple and was alluded to yesterday in an excellent article.

If the RBNZ doesn't want inflation but there is inflation in existing goods included in the CPI calculations, they will remove those goods from the CPI calculation.

Done, back to low inflation. You can see this now with housing costs making up a small percentage of inflation, while for many people, they represent a much larger percentage. You can also see this recently with Stats reports on how inflation affects different income groups.

Bait and switch. Oh wait, I mean wait and watch.

Perhaps they are trying for Goldilocks solution. Credit is restricted.Existing home prices remain flat. Interest rates stay under 4%. It is somehow still profitable to develop land and build new dwellings. 5 -10% Inflation takes hold for consumer goods and services only. Immigration is curbed.Wages to rise. Home prices come closer in alignment with incomes.Some of the existing consumer debt burden is eroded by inflation. Good luck with that.

Nice, lock in another few hundy this year, lock in a nice low interest rate for 2/3 years after that and ride this pony home

Yep BOOM thats another $100K on my house by Christmas. Thought is would take till Christmas to hit the $1Mil but its already there this month. Early Christmas present from Labour and I didn't even vote for them.

If want to read

https://www.ft.com/content/9f9d00da-afb1-4b51-9a0f-6344df914bd8

The market has been impacted by a number of significant artificial drivers over the last decade. High immigration/foreign students, high foreign property sales, mass domestic income tax avoidance via interest on debt, low residential construction, and record low interest rates focused on protecting banks/debt fallout from GFC and now Covid. All of these things have ended, or are signaled to end in the near future. Now we have rampant inflation globally, which the worse it gets, will pressure interest rate changes at the Fed. We will follow the Fed.

How does Orr sleep at night. History wont remember why the house of cards collapses, they will just remember whose hand (asleep or not) was on the steering wheel.

Sorry, accidentally reported.

Rampant inflation.... No its not, wow, you can't just say crap from reading some headlines haha, slight inflation yes, rampant hahaha no

Not rampant yet, but enormous 'cost push' coming down the pipe. hahaha?

STOP PRESS: RBNZ announces that they will give more free money to bond buyers next year leading to positive market response.

Orr is striking a Dovish / Hawkish pose. "It's a funny sort of creature the Dawk, neither one thing nor the other".

At once courageous, yet afraid. Both clear sighted, and blind. Understanding yet wilfully ignorant.

Error

You might as well warn alcoholics to watch out for booze. So many people are drunk on debt that you can smell the Stachybotrys from their breath hanging in the air.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.