By Gareth Vaughan

Despite some pressure on New Zealand's big banks from an increase in US dollar funding, which was highlighted in the Reserve Bank's Monetary Policy Statement (MPS) on Thursday, any movement in residential mortgage rates appears more likely to be down than up in coming weeks and months.

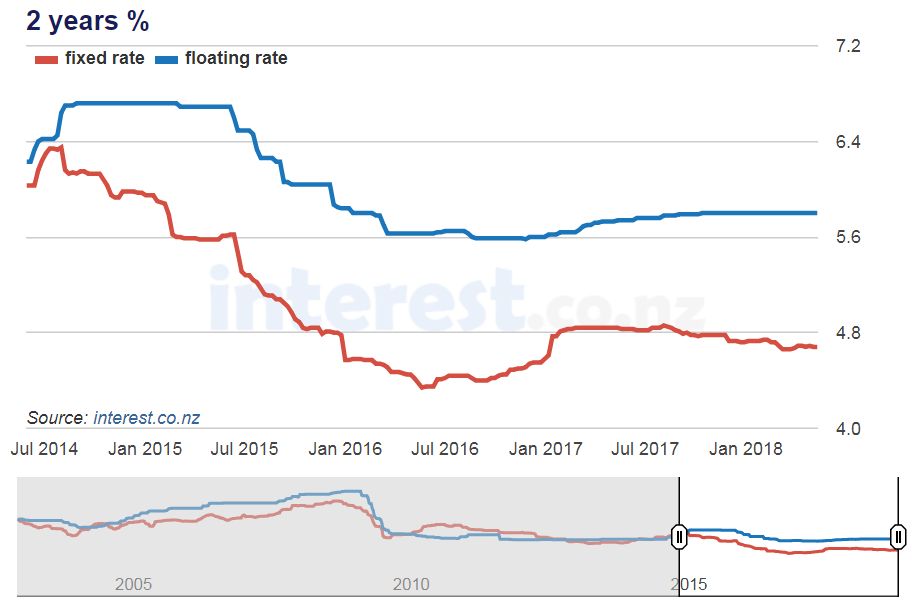

As new Governor Adrian Orr delivered his first Official Cash Rate (OCR) review, interest.co.nz's David Chaston was publishing an article about both ASB and The Co-operative Bank cutting mortgage rates. As our chart below shows you have to go back to January 2017 for the last material rise in fixed-term mortgage rates. Reserve Bank figures show, as of March, 79.1% of residential mortgages by value were on fixed-terms, rather than floating.

But, with the Reserve Bank highlighting that the cost for banks of borrowing short terms in US dollars has "increased markedly" since February, are borrowers about to be hit by a series of mortgage rate rises?

"For New Zealand banks, higher US dollar borrowing costs typically feed through into their cost of funds, which could flow through to retail interest rates in New Zealand," the Reserve Bank says in its MPS.

"Domestic 90-day bank bill rates have risen around 15 basis points since the February [Monetary Policy] Statement, and this is feeding into longer-term interest rates. The cost of swapping offshore funding into New Zealand dollars has increased by up to 15 basis points, depending on the term, since the beginning of the year. If this trend continues, it is likely to put pressure on banks' net interest margins, and it is possible that retail interest rates could rise."

"New Zealand banks appear to have been largely resilient to US dollar funding pressures thus far," the Reserve Bank added.

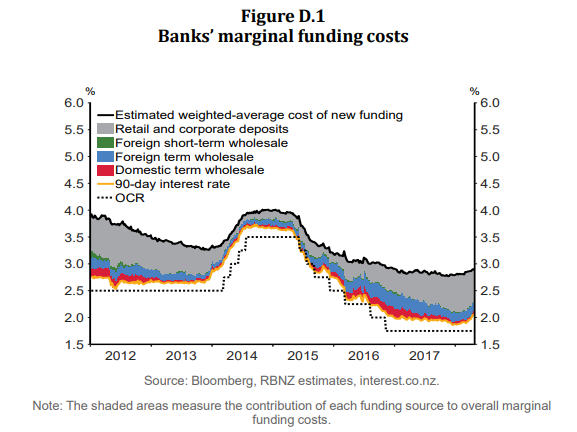

The lowest funding costs in at least 31 years

One factor in this resilience is the fact bank funding costs are at historically low levels. I highlighted this in coverage of KPMG's annual Financial Institutions Performance Survey (FIPS) in February, emphasized by the headline; Annual FIPS shows highest profit & lowest funding costs in survey's 31-year history. The average funding cost across the 20 banks surveyed for the FIPS came in at 2.82%.

It's also worth noting that short-term US dollar funding is not as important to NZ banks as it once was. A key reason for this is the Core Funding Ratio (CFR). The CFR was introduced by the Reserve Bank in April 2010 to reduce NZ banks' reliance on short-term offshore funding. The CFR requires banks to meet a minimum share of their funding from retail deposits, long-term wholesale funding and/or capital.

As the Reserve Bank puts it; "The basic notion underlying the CFR is a comparison between an estimate of the funding of the bank that is stable and can be assumed to stay in place for at least one year (‘core funding'), and the core lending business of the bank that needs to be funded on a continuing basis."

The minimum CFR for individual banks is 75%. As of March, the industry-wide CFR was 88.4% with core funding of $361.322 billion against total loans of $408.736 billion. Measured monthly, only once has the industry wide CFR been higher than in March, when it reached 88.7% in December last year.

Rising net interest margins

Additionally bank profitability, demonstrated by net interest margins in the half-year financial results from three of the country's big four banks over recent days, is strong. Westpac announced a 19 basis points rise in net interest margins year-on-year to 2.15%. BNZ's net interest margin was up nine basis points to 2.24%. And ANZ's net interest margin increased seven basis points to 2.37%.

A net interest margin measures the difference between the interest income generated by banks from loans, and the value of interest paid out to their lenders such as depositors.

Orr was asked about US dollar funding pressures on NZ banks in the Reserve Bank's MPS press conference. The issue was broken out into its own box in the MPS.

"That is a risk and that's why we put it in the box, and we have been interested in the fact that it hasn't been passed on [by the banks] as much. We try our best to understand what the dynamics have been. What I would point out is that the banking sector is very competitive and so just simply being able to pass on all costs, unfortunately can't just happen like that. So the competition in the banking sector is a really key feature for us. That's not to say they won't pass it on. And if they do pass it on, we [the Reserve Bank] have higher interest rates and we have more work to do than otherwise," said Orr.

Asked whether the Reserve Bank would cut the OCR in reaction to higher mortgage rates, Orr said; "I would say at that point a butterfly has flapped its wings and the world is different. We'd have to reassess what we're doing."

And asked about banks' increased net interest margins, Orr said; "They've been very profitable so I imagine competition pressures will rise."

'People fight harder for a share of a smaller pie'

Finally there's the attitudes of the banks themselves. The latest Reserve Bank sector credit figures show housing lending growth of 5.8% in the March year. That's relatively low by historic NZ standards. As recently as December 2016 the annualised growth rate was 9.3%, and in the rarefied pre-Global Financial Crisis world it was in double digits.

House sales volumes have also been soft. The latest Real Estate Institute of New Zealand monthly figures show sales volumes down 854, or 9.9%, in March year-on-year to 7,768.

When I interviewed him on Monday, Westpac CEO David McLean said this housing slowdown suggested competition between lenders will increase.

"Because the housing market has slowed quite a bit, I think most of the banks seem to be pretty well funded in terms of deposits. And therefore we're likely to see competition switch back to people fighting for lending in a quiet lending market. Often when you see lending growth at lower levels people fight harder for a share of a smaller pie. So we're expecting the housing market particularly, will see more intense competition," said McLean.

The chart below comes from the MPS.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

58 Comments

your point about "higher net margin" is history, as mr orr said, the higher funding cost has started to rise from the beginning of this year, and the results included a very small part of that, so if you looked at their net margin in the last 3 months, you would find a different outcome

also your analysis about rates falling, if the government were to increase supply of new builds (as it claims), that is going to put massive pressure on funds, banks will have to source more of their moeny overseas (and rising cost will have an impact)

My point, and maybe it wasn't clear enough, is they're coming off historically low funding costs, are flush with deposits and the housing market is soft. Thus if rates suddenly spike housing activity goes in the opposite direction which I don't think banks want right now. Govt housing initiatives in NZ won't happen overnight. The risks, as usual are overseas, - the Aussie Royal Commission & what it might mean here, and rising US rates, plus any unforeseen circumstances...Cheers.

Good summary Gareth

There is a tendency for some to be a little miopic

The macro view is the correct one

I agree the banks won’t wish to raise rates when the market is leveling off . Time to let the market find its own equilibrium without any stress from raising mortgage rates

I see the Aussie Royal Commission & more particularly US rates rising to be the current factors to keep watch on in my opinion

Of course others here will have their own view

As per government's announcement this week, they are no longer adding 100'000 affordable houses to what the private sector is building. Instead the government is encouraging the private developpers to keep building by guaranteeing a fixed sale price.

... yes ... as Duncan Garner has said : this government has had 9 years in opposition , and have not used that time wisely .... their 100 000 affordable homes pre-election promise is as bogus as their 1 billion trees planted promise ...

Either they lied to us ... or they promised wildly any damn thing they could to win our trust ...

... that trust is fast disappearing Miss Taxinda !

Or both, how could anyone imaging that these Activists muscaraded as Ministers could pull such big tricks out of a bag.

We all remember the last few weeks of the election open auctions for housing, trees, water, doctor's visits, and the Homeless !!!

and Apparently, with the biggest surplus in decades, we are led to believe that we are poor and cannot afford most of the above - but we can dish out millions to the Islands, student fees, and the regions, let alone the 75 odd Committees and working groups which will report to this CoL by the end of its term on what to do next !

Circus

Gummy please enlighten me what JohnKeys National govt strategy was again ?

Yeah right

Or they believed and aspired to deliver these outcomes but are stymied from doing so.

I doubt someone you would trust Labour anyway, so frankly no change.

And what difference does that make, the previous government did crap all to bring affordable houses to the market.

Stop being so angry HO, the difference is clearly that there won't be MORE houses built as originally promised.

Why would you think I'm angry. You obviously don't like beans being spilt on your beloved ex government, that encouraged you serpents

I'm not talking about the previous government. I'm discussing what is, not what has been. I'm just explaining you that there won't be more houses as expected

BTW it's your use of words like "crap" & "serpents" that show that you're angry

No. It's called stating the truth. If the cap suits you, wear it

Wrong !

National did their very best over 9 long years to allow as many new migrants into NZ as possible

bringing with them valuable skills like massive importations of pseudo ephedrine thus reducing the cost of illegal drugs on NZs streets

The Nats also succeeded triumphant in opening the gates to foreigners speculating in Auckland property

and allowing the free flow of untaxed capital gains back to foreign speculator bank accounts

Truly enlightened governance

Now tell me how bad Jacinda is again ?

Really HO - where do you dream up this shit. I suppose it says it in your name. Did you even read what the writer is saying in this article??? It's an absolutely fair point. I'm been offered better rates now than ever last few weeks. There is intense competition for a small amount of buyers historically compared. The banks not meeting their lending targets as not enough sales. People like you will continue to say this overpriced crap forever. I spent the day in Sydney today and even here the locals are saying that all talk of massive price reductions is rubbish. The only things that are going down is apartments and some rubbish townhouses. Prices in Sydney are still going up, yes the rate of growth has slowed but that's what most people don't understand.

Dear Chessmasta

So you don’t see any problems arising from the current worldwide debt bubble then ?

Oh I am so relieved

Yeah look all over the world for problems. I'm too busy looking at opportunities and thinking future is bright. Don't read too much into Doom and Gloom stories. These have been around forever, Isis, North Korea, dictatorships, etc, etc. Nobody gets rich waiting for shit to hit the fan, you gotta make your own opportunities and make money. Ask any financial expert what will happen in 3, 6, 12 months. They have no idea and will give you nothing without disclaimers saying their crystal ball might be inaccurate.

Hi Chessmaster I think debating anything with HO or RP is totally fruitless they have a very negative view of wealth and personal success. Naturally they support a Labour lead Col so any criticism of them is deeply defended. They despise people like you and me who see the world as it really is and take opportunities that arise hence leading to a us and them situation. Governments are seen as being responsible for everything including house prices of which rose faster under the last Labour Government but that is never mentioned. Lastly there seems very little acknowledgement how and why the Economy is so strong even after GFC and Earthquakes maybe good Government?? Just a wild guess but they would never acknowledge that would they.........

shoreman, clearly shows your pathetic view of the overall state of the economy.. in your eyes, as long as your asset is growing in value, you are satisfied.. that is the personalities of people like you and chessmaster.. but ignore all other aspects that the National led government have neglected..

As i said to chessmaster.. keep doing what you're doing.. we'll see who'll have a laugh at the end..

happy buying

https://www.nzherald.co.nz/sponsored-stories/news/article.cfm?c_id=1503…

HO don't waste your time with them coz they have their blinkers on again. You are right, there are many aspects in our lives that have been neglected for too long. Our motorway traffic during peak hours are shocking out west, and people don't realise it unless you live there. I had to drive to Massey yesterday and it had opened my eyes.

I dream that shit, due to specimens like you

I bet you suck at chess, another fake specimen

Nice. I'm actually very good at chess thanks.

Shouldn't you be wishing me good luck to make my next $1m profit in the Auckland property market :-)

Seriously guys like you actually help me pick up bargains, so with all my heart I genuinely thank you.

Keep going, shows you're lack of maturity, when you state you're too busy to notice international events. . Similar to a horse, feel contended with what you can see, completely blindsided. ..

It's called blinkers on.

Thanks dgz :)

Guys, it's all good. Just keep worrying about everything and hope for a crash. At least the current govt is on your side and wants to do that too.

Talking of overpriced, how is ffn $550k for 1 bed room dwelling affordable?? HO - your govt is going to make your username last a lot longer. That is far from affordable. Someone please correct me if I've got these govt build prices wrong. I heard him say $500 and $550k for one bedroom apartments. This is insane and will just drive existing house prices up further.

Can see the frustration growing. Empty vessels make the most noise. Very appropriate for you

I think it was the previous government that decided $550k was affordable.....?

Are you shorting the market in some manner?

Chessmaster,do you have an Elo ?

Good question :-).

Ranges between 1650 to 1750 - depending on of course how you feel on the day. Some days you can see everything and other days you miss the most basic attacks.

The "grandmasters" and "experts" are rated over 2000. I'm no Grandmaster as I'm not that geeky, just play for fun.

Pretty decent score

Very good player, I'm on 1574 right now (generally between 1500 & 1600). Are you on chess.com ? If so we should play a couple of games

X

Thanks a lot for your article, Gareth.

I'd like to re-pose a question I asked 2 days ago and to which, I unfortunately never got a simple satisfactory answer.

In the MPS Orr said.

“The key risks to a rate cut would be international growth faltering, or more importantly, international financial market conditions tightening,”

In other words, a rise in long-term interest rates, which could feed through into New Zealand lending rates.

Why would Orr consider cutting the OCR if long-term overseas interest rates rise? Is it simply to keep some NZ interest rates (the short end) low?

Gareth? Anyone else?

I think what he means is if offshore financing of our debt becomes more expensive, then our OCR will need to rise (i.e., the risks to a cut are...)

Of course!

Thanks Kate, that's what I thought too but no, I have listened to his MPS presentation and his statement was clearly in response to the question: "what would trigger an OCR cut". (it's around 4min 30sec in the video posted 2 days ago on this website of the MPS anouncement).

Hence my question remains: "why would Orr CUT the OCR if offshore interest rates rise?"

I think what he means is if offshore financing of our debt becomes more expensive, then our OCR will need to rise (i.e., the risks to a cut are...)

There's always Japan. Why can't the carry trade work it's magic or will the Japanese demand too much in risk premium?

Anyway, in the case of NZ and Australia, there's only one direction for the OCR and that's down, Expect NZD to get hammered at some point. Just like in the GFC, NZD and AUD were smashed against JPY in particular. Nothing has changed: Our h'holds live beyond their means and carry the economy on their debt. That profile has only strengthened over the past 10 years.

We could ask Gareth but why when we have J.C. and his usual dissertation on Japan ?

Hilarious

LOL, yes I'd like Gareth's view, Gareth please?

We could ask Gareth but why when we have J.C. and his usual dissertation on Japan ?

Considering that Japan was a primary source of the carry trade, it's relevant considering that NZD and AUD were and are key targets of the carry trade. The RBNZ devoted a commentary towards it last November. Go look for yourself.

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Bulleti…

If the cost of JPY is so cheap, do you not think it's a useful source of financing for NZ?

so does that mean the Australian Banks will only make slightly more acceptable profits from its Kiwi customers insetad of the gouging that has been going on ?

NZ mortgage rates, contrary to bank/media spin, are not low.

At nearly 6%, floating mortgage rates are very high given low inflation, low-ish OCR, very low global interest rates.

The only direction now for NZ mortgage interest rates is down.

If all those jumbo recent Auckland mortgages hit higher interest rates, then banks will have some issues.

Steady as she goes, or lower for longer.

Too big to fail huh?

Maybe. Wonder how many mortgages over 500k have been taken out in the last 5 years?

The opening of this article was:

“Housing mortgage rates are more likely to go down rather than up”

This government is encouraging the private developers to keep building by guaranteeing a fixed sale price-encouraging to build is wise but acting as a guarantor is foolish - extremely risky use of tax dollars. I would rather let the developers/INVESTORS take this risk- one of whom was always happily ready to take this risk but have been hosed out by this anti investor regime. Nothing wrong in discouraging speculators but most investors are buy and hold ones and these are the ones who have been stopped in their tracks by this anti investor govt. what a mess this govt guarantee to developers will cause.

Yeah I think a better way would have been to simply force councils to open up more land for development by rezoning and use the rates to penalise land bankers, maybe call them special housing areas, and make it easy to develop.

At the moment cumulative portfio mortgage loan growth expectations exceed the market growth rate so retail banks will compress margins to chase business. If you are coming towards a rate renewal, and you're not tied to the bank by any other agreement, an astute customer should be able to negotiate a very substantial discount to advertised rates as banks will be looking to limit portfolio churn.

The problem is rates will eventually go up, if a person has a 30 year mortgage I'm picking somewhere in this timeframe the rates will rise. So buying a house at the most unaffordable time in history, with a massive millstone doesn't make sense, especially while prices are stagnating and have potential to fall.

Household prosperity comparison by local board:

1. Ōrākei 9.8

2. Upper Harbour 8.8

3. Franklin 8.1

4. Howick 7.8

5. Devonport-Takapuna 7.6

6. Hibiscus and Bays 7.1

7. Albert-Eden 6.9

8. Rodney 6.9

9. Waitākere Ranges 6.8

10. Kaipātiki 6.5

11. Waitematā 5.7

Auckland 4.7

12. Waiheke 4.0

13. Puketāpapa 3.1

14. Henderson-Massey 2.7

15. Whau 2.7

16. Papakura 2.4

17. Maungakiekie-Tāmaki 2.1

18. Manurewa 1.8

19. Māngere-Ōtāhuhu 0.9

20. Ōtara-Papatoetoe 0.7

https://interactives.stuff.co.nz/2018/05/a-tale-of-two-cities/

.

Looks like the diversity is inversely proportionate to the prosperity. Throwing more courses, money and publicity at the problem has done less than nothing, it appears to have made it worse. Entrenching the victim mindset instead of forcing people to take responsibility for their own life.

That's exactly what the current government is doing. Any problem's response seems to be "spending $X millions on it. I'm not sure spending money = improving any situation. Yes you need money to fix some issues but money alone does not solve a problem

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.