While everybody will be interested to see what happens with the New Zealand housing market this year, one of the key elements to watch will be what happens with the first home buyers (FHBs) - or at least the would-be first home buyers.

As the housing market went from the ice cold of lockdown April to white hot as quickly as August (and it's only got warmer since), one of the impressive features for me is how well the FHBs as a group were seemingly able to compete and to get their share of the houses.

But there are limits to everything.

Probably the crucial dynamic to observe as the housing market develops this year is the extent to which investor activity may or may not moderate and what happens with FHB participation levels.

The housing market is an extreme area of vulnerability for the Government. Arguably no more is this the case than with the FHBs.

Images of fresh-faced young kiwis, with perhaps a baby or two in arms, looking mournfully at a house they can't afford are much beloved by television and are lethal for whoever the Government of the day is. It's a bad look. Kiwis deprived of their birthright.

In terms of Government reaction to housing issues this year then I think its safe to say this will be very much led by how well, or otherwise, the FHBs can continue to compete in the hothouse that is the house market.

Badly locked out

The FHBs did get very badly locked out of the housing market in the 2013-2016 period.

This was a direct result of the initial introduction by the Reserve Bank of bank limits on high loan to value ratio (LVR) lending in 2013.

The original iteration of the LVR limits, which made no distinction between different categories of borrower, ended up hugely disadvantaging the FHBs, who were reliant on raising enough cash for a deposit, while investors of course could use equity in existing properties to easily borrow and outbid the FHBs.

So, during the 2013-16 period we saw FHBs relatively existing on crumbs, often having an under 10% share of the mortgage monies being advanced by the banks on a monthly basis.

This only really changed after the RBNZ in mid-2016 started applying more rigorous measures specifically targeted at investors. Initially in 2016 investors had a requirement to find 40% deposits slapped on them. This was subsequently loosened to 30%, which is the level that applied at the time the LVR limits as a whole were removed by the central bank in May last year.

And of course, once the LVRs are reapplied in March (although banks are already treating the rules as if they've been reintroduced now) that 30% rule for investors will be back in place.

To say that removal of it had quite an impact is to say nothing.

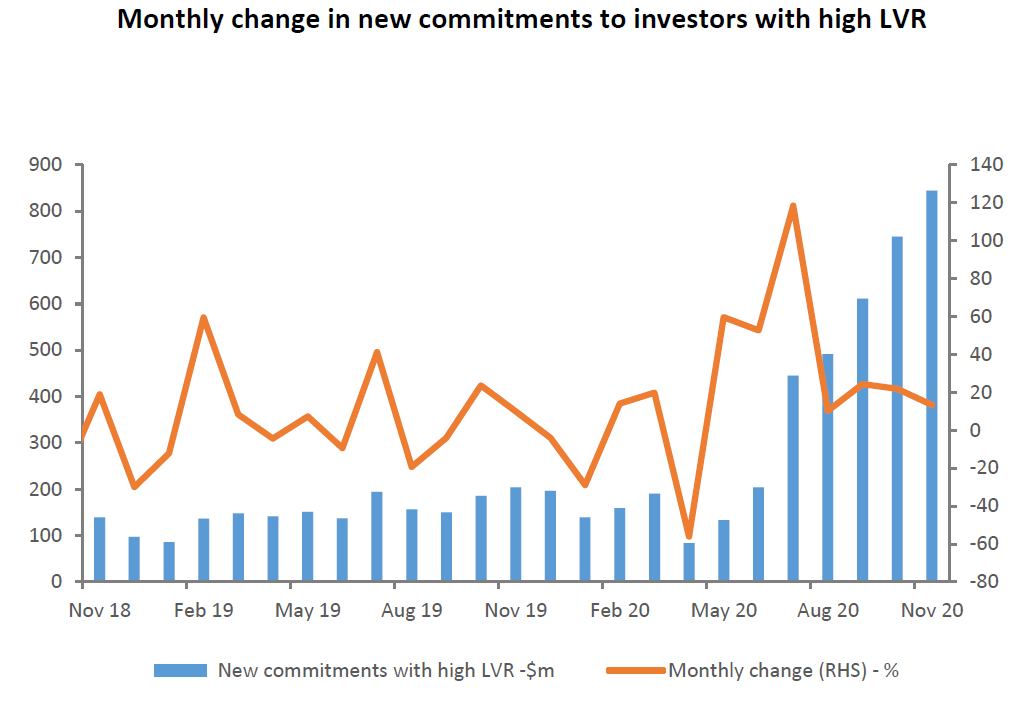

In November 2020 banks advanced $844 million to investors with deposits of below 30%. This compared with just $204 million worth of high-LVR lending to the investor grouping in November 2019.

So the amount of high-LVR lending to investors more than quadrupled in a 12 month period, as the banks took advantage of the extra wiggle room afforded them by the lifting of the 30% deposit rule for investors.

The RBNZ's latest monthly mortgage data that will cover December, are not out till the end of this month. The November figures (on which the above RBNZ graphs are based) were released on December 23, 2020 in the shadow of Christmas and so therefore didn't quite get the attention they deserved.

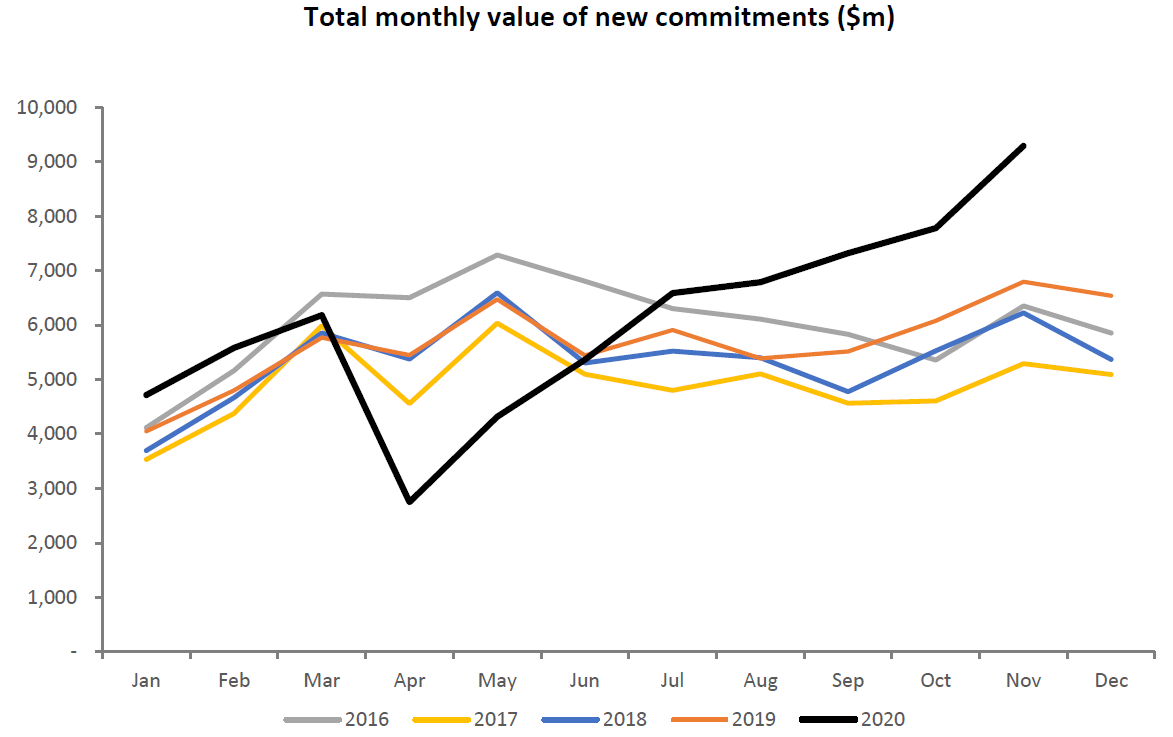

They were, in a word, spectacular. The total amount advanced, at $9.3 billion, was an all-time record, absolutely smashing the previous record of $7.8 billion set just the previous month.

How did the FHBs do in all this?

On the face of it, very well. They borrowed a record high monthly total of $1.605 billion. And for those readers who prefer to talk about actual people rather than dollar terms, the number of mortgages taken out by FHBs in November was also a record high, at 3221.

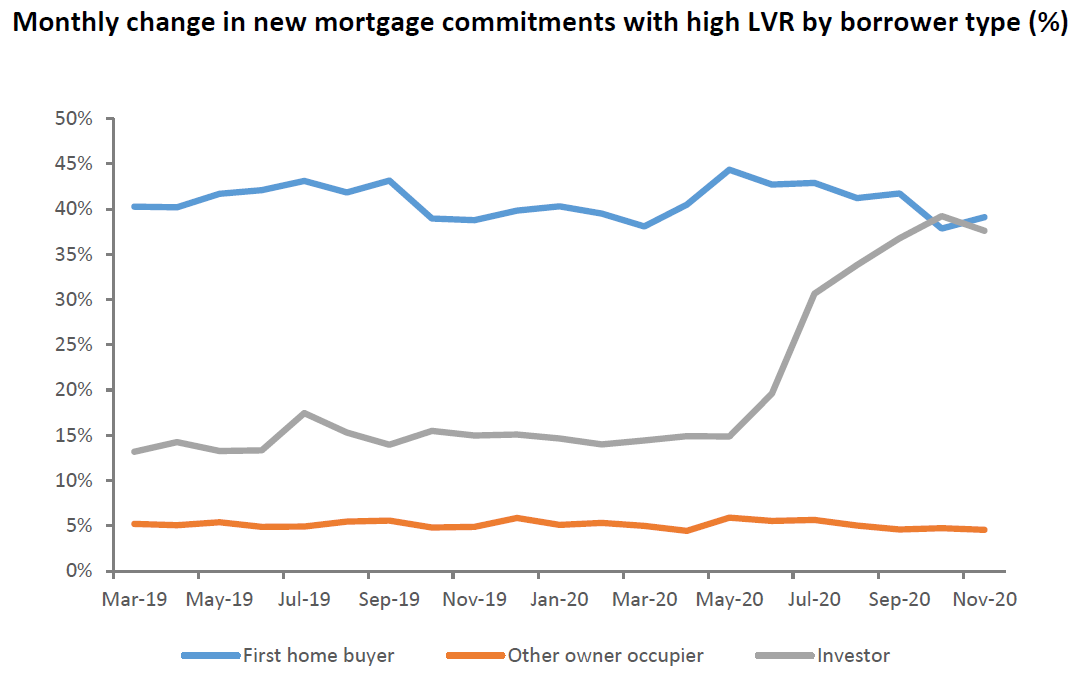

However....the FHBs share of the monthly spoils is dropping, and appreciably so.

In July 2020 the FHB grouping borrowed $1.344 billion, which was a record high 20.4% of the total amount advanced by the banks that month.

Since that high water mark, however, while the monthly FHB borrowing figures have continued at high levels, the overall share of the total amount borrowed has been falling, to 19.8%, in August, 19% in September, 17.9% in October and 17.2% in November, which of course as stated above was a record month for FHBs in terms of amount borrowed.

Feeling the heat?

It raises the obvious question of whether we would have seen much higher amounts of borrowing by the FHBs in the past few months if there hadn't been such a massive rise in investor borrowing. In November, investors in total borrowed $2.246 billion, which was that grouping's biggest total since mid-2016, and was up some 64.8% on the $1.363 billion borrowed by that grouping in November 2019.

So, really the question is what is the potential size of the FHB market? And to what extent are the FHBs now already being crimped by the resurgence of the investors? You have have to imagine this is happening to some extent. But without knowing exactly how many wannabe FHBs there are out there trying and perhaps increasingly struggling to compete, it's very hard to say to what extent.

All of which brings us back to the point that the next few months will therefore be crucial as we see whether the FHBs can continue to successfully buy houses in this current market, and the extent to which investors either do or don't pull back from the market again with the reintroduction of 30% deposit limits.

Personally, on the latter, I think there's now so much heat in the market that investors are unlikely to be dampened by the 30% rule, and I reckon the RBNZ may yet have to kick it up a gear and go for a 40% or even higher deposit rule.

Time will tell. All you can say is it is hot out there right now and the FHBs must be feeling the heat.

91 Comments

I know of a few youngies who have said to hell with ponzi Grant Orr promoted house prices. Instead they are investing into their own businesses.

The choice between ridiculous high housing debt and employee for life .....or rent for a few more years yet and controlling their own future.

All power to them.

@rastus: You're definitely onto something.

When investors use equity, the mindset is that of buying a $10,000 Lounge Suite on credit (24 month, credit-card, whatever).

If you've saved $10,000 for the couch.. well.. when you get to the store you might realize you value your Hard-Earned-Money more. OR, demand a way being deal and not be afraid to walk away.

Regarding Property:

Many speculators are dependent of increasing house prices and the banks letting them leverage (unrealized equity) into more property. FHBs actually have money. It's interesting. Good point @rastus.

The problem is the banks get the money regardless, unless FHBs stuff their money under the mattress or take out term deposits with non-bank deposit takers/credit unions.

Banks can magic up as much money as they want, but they need credible borrowers.

True, good point I didn't think of it that way. With house price inflation the way it is, I'm sure the banks are starting to run a little thin on credible borrowers.....until the next interest rate cut.

How timely!

Global independent economic researchers Capital Economics see the Reserve Bank as needing to lift interest rates from next year as economic conditions improve beyond expectations:

https://www.interest.co.nz/business/108667/global-independent-economic-…

I don't think I believe it but interesting to hear an outfit predicting a hike.

if the OCR don't stop going down , not far are we from the days where drinking water will need to be purchased on the exchange and you 'll need to preapprove the loan with the bank to purchase it. Basic need are commoditized - housing, power, water next

I believe there are huge investment opportunities out there these days. Just a matter of knowing what's going on, which makes them easier to see.

Ax someone who did exactly that, I will point out that getting capital from a bank without a home to secure it against is a nightmare and why new company start ups are down by nearly fifty percent on twenty years ago...

"I know of a few youngies who have said to hell with ponzi Grant Orr....."

Can't possibly be true, Rastus....... Reserve Bank Governor's name is ADRIAN ORR.

TTP

Since the election last year, our home has risen in value by $3,000 per day. In an attempt to put TD cash into property we have been blown away by the heat in the market. 2 bedroom sausage flat sold at 159% of last sale in 2017. Pauanui beach house listed at $1.189m sold for over $1.3m with seven bidders. I can’t see how FHB can compete. BTW it doesn’t help with the Government telegraphing likely changes to the brightline regime. Get in now and make it five years. Wait and it’s 10 years.

Property investment should be relabeled as social leaching. What good does it do for NZ society to have people with assets and a day job also buy property on the side as an ''investment'' by leveraging their current assets to borrow from the bank? This is not investment, it is asset grabbing undermining a fundamental need for all people to have a home. This is turning NZ into an extreme society of the very wealthy and the very poor. It wont be long before the wealthy begin to live in fenced off compounds with 24hr security to keep out the impoverished. Is this what we want.....?

Exactly. I remember transiting in Manila for a night a few years back and I booked a B&B equivalent in an area that was geographically close to the airport. I got in the taxi and we weaved through some of the worst slums I'd ever seen. I thought the taxi driver would stop and pull out a gun to rob me, but in the distance I saw this huge concrete wall thats seemed to go on for miles. We approached an opening in the wall and the car was searched, including under the chassis, by very heavily armed men. They let us through to the waiting beautiful houses with fountains, mown lawns, and well dressed kids playing in the street. Outside of those walls was abject poverty. I remember thinking, If we're not careful this could be us.

That's a bit dramatic don't you think?

People can still have a "home" through renting. Lots of countries in the OCED have low ownership rates and civilisation hasn't collapsed

And lots of countries in the OCED have tenancy laws that NZ "mum and dad" investors would never accept. Rent a property in Berlin or Copenhagen and your landlord is likely some massive superannuation fund or pension scheme. They have no interest in kicking you out - and very little ability to do so anyway. And any repairs required to the property are an almost inconsequential line on their massive balance sheet.

If we are moving toward being a nation of renters, then we need laws that properly protect renters. That's going to cause a lot of difficulty for small scale landlords, but we as a nation can't have it both ways.

Perhaps the ownership of such property can include shareholders, which could include the tenants that live in them, if they so choose

I have been following a property investors blog on Facebook .. I think it has 46k members.

It’s pretty typical to see a post asking for advice by a landlord complaining a tenant hasnt weeded a garden, complained about something etc.Quite often a barrage of posts will come from other landlords advising to get rid of them, turf them out.

It’s a sad indictment on New Zealand society and mob like attitude against renters.

Many new landlords today don’t realise that in the past they needed to visit the flat every week to collect the rent in person a d therefore keep some sort of amicable relationship. Now they just communicate via text or the property manager.

One can see an area like Ponsonby turning for the worse.... the jobs in the supermarket, petrol station, dairy, barbers, retail shops, hospo are predominantly going to immigrants. One outcome of this is the growing problem of homeless and destitute. It’s pretty depressing passing the beggars in the street and the rough sleepers in the park.

Give them all a state house. As in, give it to them... free instead of rent. This'll upset so many millions who worked hard for what they've got but part of me does wonder maybe with all the money thrown at social housing maybe it would just be easier to give it to the hom(p)eless and let them find out how costly it is to keep and maintain a house. Only problem is if they burn it down and don't have insurance they're back on the state list wanting another new house.

Cynical maybe but just got the inspection report for a property I rent to HNZ, now KO... every door handle ripped out of the doors leaving holes in doors, holes in the gib walls, graffiti on inside and outside walls, mould from never opening windows (apparently this last one is somehow my responsibility). No matter... KO will pay for it all, subsidized rent and on it goes.

Nope... dunno what solution is. Pretty sure mhud, also renamed ttkk has a plan for shared ownership UK style... maybe this is a good idea for those with jobs.

The new RTA gives more rights to tenants. This makes it harder to get rid of tenants so landlords will become increasingly wary of taking onboard any form of risk. If you as a tenant thinks this benefits you, think again. Maori, solo mums, look a bit rough (nice neck tattoo bro') will rightly/wrongly be increasingly viewed as less desirable. The demand for low end housing will go up. The unintended consequence will be increased demand for social housing. Given it is in short supply, expect to see more homelessness. Nice one Labour!!

Social housing, lots and lots and lots of it, is exactly what this country needs if we are to get people back having a stake in society and their community, social housing that gives permanency and even, in the long term, ownership.

The way our tenancy laws are is still best suited to a day (long ago now, it seems) when people left home, flatted for a while, till they married and purchased their first house, very often in the 20s on one wage, we need to aim for that again, even if we struggle to reach it, we need to heading in that direction. Expecting people to maybe have to rent for life under the threat of landlords tossing them out on whim, demanding how they live their lives is unsustainable and imho is in no small part to blame for people increasingly not giving a tinker's about the house they occupy as it will never be a "home". It is damned tragic what we have allowed to happen since the era of Roger Douglas.

gnx

Re: "It’s a sad indictment on New Zealand society and mob like attitude against renters".

There again, there is no need to look past this site to see a mob-like attitude against landlords. Last year Foreign Buyer put up a post "All landlords are leeches" and it got over 70 up-ticks. :)

The reality is that government will not provide social housing for all so there is a need for rental properties; this means there is a need by tenants for private landlords, and landlords need tenants.

I agree that there are some very good and very poor landlords . . . just like there are some very good and very poor tenants. Its the same with any any business; some business owners are great others not so, and some customers great and others not so great especially in paying their bill.

Landlords have handed over an asset worth many $100k so they need to trust the tenant and it is essential that they develop and maintain a good relationship. And yes that involves some contact with the tenant without disturbing the tenants entitlement to peace - a gift at Christmas is well worth the investment.

Note that landlords are reluctant to just turf tenants out. There is considerable time in interviewing and checking new tenants, work in bringing the rental back up to a tidy standard, and of course down time in rent coming in. Accountants suggest budgeting for 48 weeks a year occupancy, good landlords aim for 52 weeks a year.

And as to a tenant not maintaining the gardens and lawns in a reasonable tidy state - well that is what the tenant has agreed to do. The standard Tenancy Services agreement states: "6. Tenant’s responsibilities: . . . . › Keep the premises reasonably clean and tidy . . . ". Drive around a suburb with a mixed private and rental homes and it is easy to spot the rentals with a pretty good degree of accuracy.

The only people that say all landlords are leeches are those who have never left home. We've all flatted at some point, many professionals relocate and need to rent. There is a need for good quality rental accommodation.

The issue in NZ is that there is a shortage of accommodation, not that landlords are buying rentals. If the rental market was in equilibrium and landlords continued to buy rentals - then the rental market would be in surplus and rents would fall.

NZ should focus on the insane cost of building rather than landlords. The latter prosper because of the former.

What we will increasingly see in the coming decade is the creation (by default not design) of caravan parks for people who cannot afford to own and who are a part of the group of ''avoidable tenants'' ie people no one will rent to. This group will grow massively in the wake of the new tenancy laws.

Good investment opportunity now in selling caravans?

Knew a guy dealing in second hand caravans does an absolute roaring trade fixing them up. Old caravans pulled out of farms and the like. All cash sales. He also does a brisk business renting to untouchables again cash only on proviso the houses never have any work done on them, ie no insulation, no heating, nothing. If boards fall off the house stays as is. If the tenants break windows and don't fix it and water comes in so be it. The tenants are all alcoholic and drug addicts on benefits. They pay cash and never complain and the landlord has no maintenance ever.

What a sad business to be in...if that’s your friends life and what he gets a kick out of good luck to him... not much different to loan sharking or drug dealing

Nah, loan sharks are the lowest of the low.

I don't begrudge hands-off, lowest-common-denominator landlords in these cases. It's probably for the best. There are so many people around who need intense help... from social workers, rehab services, etc. There's not a lot that landlords can do in these cases.

I'm picking NZ will see an increase in people living in caravans. Communal kitchen and toilets etc.

Maybe the cold hard facts indicate that the "avoidable tenants" need to lift their game, quit the drugs/alcohol abuse and asset vandalism and become desirable tenants?? Either that or get used to living in a caravan park run by Kainga Ora.

To sam-s. Think about the zombie suburbs of South Auckland. Been troubled for some decades. And then, just in the last year or two the trouble has been guns and people getting shot. Quite new, but the trend is one way.

"Leeching", but yeah. I call it economic cannibalism or people farming. It disgusts me daily to see what this country has become and how housing has become a never lose casino for the privileged and a source of social deprivation for those that are farmed by the people farmers.

Easy to solve Pocket Aces in 3 steps ....but not palatable with the landlords, banks etc etc

Step 1: - an "empty home" tax in high demand urban areas - well, if the taxpayer has to pay an accommodation supplement towards the "Ponzi" scheme, so can the property owners, when that property could be providing accommodation for the so called "housing shortage".

Step 2: - Capital gains tax on all residential property - except the family home and "immediate" penalties for those individuals found to have an interest in more than one property.

Step 3: - All undeveloped land in major urban areas to be taxed, so encouraging landowners to release this land.

With all this "printed money" (which eventually has to be paid back) going into the housing market, it can be used to start up new companies and ventures etc etc

At least it would be a start to get NZ off this property "train" and develop new industries/technologies etc.

I like 1&3 but am still not sure about 2. I've lived in a country with a CGT and severe deterrents for landlords but they still have a housing crisis. I think the problem is much more complex.

It's income and employment not just how housing is taxed. We have house price inflation but not wage inflation. And the same issue has occurred to varying degrees all over the world. We also have low interest rates.

So why is there no wage inflation? Why are the working and middle classes shrinking in the under 50s? Because big multinational corporations can outsource labour and factories to anywhere in the world, which is deflationary to local wages but not local house prices (if central bank and residential bank sector lending in loose).

The issue is financialisation, globalisation and to a lesser extent, local tax policy.

There's been a few discussions on CGT recently.

The conventional wisdom is that they don't stop runaway housing markets. They almost certainly don't.

But some commenters suggested they might mitigate. As was rightly pointed out, Australia's market doesn't look as crazy as Nz's. Maybe - maybe- a CGT *might* be a factor in that...

Might have a small effect. But i'd say the sprawling developments ie, plenty of supply is a much bigger factor.

On its own, no, a capital gains tax won't work, but not taxing unearned income, especially on something so vital as housing is pretty ugly, I would make it on housing alone, simply because we cannot have something so vital to human life being used as a never losing casino for some, a source of misery for others. I am getting to the point that I am okay with brutal measures to turn around the brutal situation that now exists in housing.

Any monies from it can go toward social housing.

Nah won't work, have to tax all houses including family home otherwise get the mansion effect like Aus and that's the dodge we've already got... people flicking their "own" home on a multiple basis and no tax to pay. IR never checks up so that's what I call a win win. Biggest impact on property prices by far, the mum and dad "home" owners not investors subject to bright line tax.

FHB going for million dollar plus house, with 5% to 10% deposit is getting riskier by the day and more riskier more measures will be introduced to support the ponzi as government and RBNZ have locked themselves in a situation, which is only win win to speculators.

In NZ particularly in Auckland most money and activity is only in housing market to make fast buck and rightly so as everyone knows that hosing ponzi is in a position to blackmail government and RBNZ to support and promote at all cost.

It is this belief rather than just supply that is pushing the house price higher as today everyone wants to get into at what ever cost - FOMO .

Meanwhile In Australia I see the RBA announced the following yesterday

"The Reserve Bank and the Australian Prudential Regulation Authority are prepared to tighten lending standards if record low interest rates result in a housing boom that could leave new home buyers in negative equity or risk them taking on too much debt"

A governing body that is obviously prepared to make the tough decisions and ensure that housing remains equitable. That said a huge factor for sensible decision making could be because the RBA board is made up of representatives from a wide range of society including social welfare reps, retail, mining and construction unlike the RBNZ where the majority of board members have strong interests in the property sector.

I can see more young kiwis looking over the ditch again - if the RBNZ and Labour government allow the runaway train to pick up even more speed.

Wow. Really shows NZ up for what it is, a self-centered, greed-driven society.

Pa-keha = People of the parasitic village.

That is a blatantly racist statement. Are you saying it is european people that are the parasites?? @#$% you!!

People of colour are never racist, can never be racist. Didn't they teach you this? You silly racist white person :)

Tighten them from what? The Australian Govt just abolished Responsible Lending Laws. Its probably easy to say that rules will be "tightened" when there are currently none.

The RBA also recently stated that rising housing prices are one of the means by which QE stimulus is passed through to Consumers - its not a bug in the system, its the main design feature.

Interested in the type of first homes FHB are buying today. Buying a small starter home now could mean doubling your mortgage when you need more space. Do you roll the dice, lock in a low rate now and go straight to the four bedder, double-garage standalone, or do you follow the path less trodden and look for a decent three bedder in a less-than-spectacular area and commit to paying the market rate for a four bedder when space becomes an issue?

That's the issue with the current house price inflation. The more you can borrow, the more you are leveraged, the more you "make" when prices increase. I was prudent when we first bought in 2014. Bought a small 2 bedroom that was well within our approved bank lending. If we'd maxed out that lending, ie bought something bigger/flasher, we would have made more on the eventual sale. Insentivising FHBs to max out borrowing is not great!

Tell you what, in twenty years time, that house you bought new, mortgaged to the eyeballs and beyond, will be falling apart, such is the quality of building materials and fittings.

Yep and worth 5 mil

Why do people need more space? The average family is Mum Dad and 1.8 kids - so a 3 bedder is ample room. A few generations ago people raised 6 kids in 2 bedroom cottages and made do. Maybe these buyers would be better off realising that they don't need a second lounge or media room, or a spare bedroom, or a triple car garage. They could then live well within their means.

Could it be that the 'average family' is small because housing prices and other living costs are so out of control and people have to put off having kids later and later? Nah, why treat the disease when you can just blame the symptoms on the patient.

To keep the property ponzi ticking over, just like in Australia, I can guarantee that Labour will introduce a FHB grant. They'll also be hoping to win back some much needed love from that voting sector.

Unlike the Reserve Bank of Australia (yesterday), the NZ Govt appear to be content to sit on the sidelines and simply watch as the situation here gets worse. In fact, according to Ms Adern, she expects house prices to keep going up.

Labour will come out with something, the vitriol has become too great.. something useless no doubt.

You just know the plan will be to push more taxpayer money IN to housing somehow.

I was part of the voting bloc that got this govt in, but by hell, housing really could be the Achilles heel of it, and I am not afraid to state that out loud

Yes, same here - because of the Govt's response to Covid, but housing is the next crisis and Labour are looking like a 1 trick pony.

So you voted for a Party that did what "Blind Pew" would have done without looking at the rest of their manifesto?? Awesome!!

No wonder we have such shallow short term thinking in Govt... the electorate rewards it

"Kiwis deprived of their birthright"

It's certainly better to own your own house but is it a birthright?

It may not technically be, but morally, absolutely, and we should retrieve that sentiment and kick the greed creed to the kerb

'The Greed Creed', I love it! So true.

Yvil never lived in NZ when it was a *relatively* egalitarian country.

It's definitely NOT a "birthright", and never has been. It's an aspiration. Unfortunately, thanks to Govt largesse, loosening of Kiwisaver and low debt costs it's now deemed to be a "right" that is increasingly unachievable. Perhaps what is needed is for the market to find it's own equilibrium and for some (even if it's a generation) to accept that ownership is out of reach. If life gives you lemons - learn how to make lemonade.

So continue to protect one generation of investors from any and all risk at the expense of another's basic access to stable shelter? Why is the people who caused the problem taking the pain never on the table like it is for other types of investments?

Russia 90% home ownership I believe?

I'm amazed at the impact of LVRs (or removal thereof) on investor lending. The average loan-to-value ratio in the absence of LVRs must obviously be much higher than 70%, but I wonder why?

Are most investors not capable of scraping together a 30% deposit? Or are they simply reluctant to put that much of their own money into the housing market?

They dont put any actual money into the purchase, they leverage the equity in their home. It literally costs them nothing to buy another property (assuming its cashflow neutral or positively geared). So if they were sitting on 40% equity, they can tap 20% of it for an investment property. If the LVR goes back to 40% then they will need 60% equity in their own home. Since house prices have gone up more than 20% in the last few years, everybody currently has 40% equity to leverage into an investment property or holiday home - hence the demand. If house prices go up another 20% then everyone who has owned a home longer than 3-4 years will have 60% equity in their home so the LVR restriction will make zero difference.

The removal of the LVR's by the RBNZ in 2020 was a catastrophic mistake, one most readers on Interest saw right away, why Orr couldn't see the mistake is beyond me.

Because housing affordability is not Orr's mandate

No, but maintaining the stability of a system that now forces people to allocate a higher and higher portion of their already low wages to accommodation costs is his mandate. Gonna be hard to get consumer-driven inflation when everyone's spending 100% of their incomes on mortgages, but that is where we are heading.

Actually GV the Banking system is totally stable. It's been stress tested several times and passes. When Joe FHB finally realises that spending the majority of their income on a mortgage is unsustainable then prices will stabilise. Buying a million dollar house to rent out doesn't generate much yield so things will self regulate. But it'll take time.

In other words the housing market given current market settings will only stabilise when landlords become actual lords and tenants become serfs. Surely there is a better option.

I dont think it would have made much of a difference, as of pre-Covid 2020 house prices had already increased 33% since 2015. So anyone who owned a home for longer than 5 years would already be sitting on 50% plus equity (assuming an original LVR of 20%) and able to tap 30% of it for an investment property. Add in the 20% gain over 2020 and now everyone has 70%+ equity in their home to leverage. And since the Brightline Test was introduced there are lots of owners holding properties for longer and accumulating equity in them. Low interest rates and a flood of easy credit has simply unleashed them.

I'd say Orr is smart enough to know exactly what he was doing, curious to know what his property portfolio consists of and how this has changed in the last 6 months. Remove the shackles holding back house price inflation using Covid + economic ramifications as a scapegoat for personal gain?

Nzdan... I would say it is more to do with them realizing how dangerous this situation (they have got us into) is for the whole system. I think they are very concerned that a slide in house prices could well turn into an absolutely unstoppable landslide that would likely endanger our whole financial system, including the banks. Nobody wants to be remembered for causing that.

I've been watching the B&T Auctions, the prices are insane, way above current CV. Prices are just so removed from incomes, normality. The low rates are absolutely 100% responsible. RBNZ just like the FED have firmly boxed themselves in a corner. Total dumbasses.

Yeah. I think they are hoping the inevitable currency collapse can be recovered from with their new bottomless digital currencies - fiat with a lick of techno paint. Fiat on a Phone - Oooh - phone good!

The problem is just how hard it is to get finance to invest in the productive economy of business, and how simple it is to get finance to buy another house.

My brother owns a fairly successful hospitality business, owning his own building for it as well.

He has been looking to both expand the business by upgrading their commercial kitchen, and just bought his first house as well. Getting the finance for the house was simple, but getting a loan 1/10th of the size to invest in his business has been very hard work.

The home loan and the business loan would both be serviced from the same income, but the bank overwhelmingly preferred to finance the house.

I’m hearing the same thing regarding farming as well, can’t get finance to buy a reasonably profitable farm, but the bank will be happy to use that deposit to give you a loan on a few negatively geared rental houses.

I'm an accountant in an established, sizable company - about 20 million revenue. The director who has a property portfolio borrows money against properties then lends this to the business when necessary. Despite being a well established, reputable, well financed company the business can't borrow directly as the banks as this will require the business to sign a general security agreement (GSA). The director won't sign a GSA as this will give the banks the power to appoint receivers as they see fit. He doesn't want to get caught out, as if there is some sort of crisis in our industry the banks could potentially call on loans & use the threat of appointing receivers if we don't pay up immediately. Even if these business loans were for say 5 years, this still doesn't prevent the banks from appointing receivers anytime or at least threatening to do so if we don't pay now. Therefore It is a lot easier to just borrow against a property for 5 years (held in another entity), then transfer to the business.

What I find interesting is that the RV of my properties have gone up by 72% and 104% respectively from 2017 to 2020. Turns out local councils are quite happy to cash in on the rates payments at an even higher rate than what the actual value of the houses are.

thinktank

Your comment demonstrates a total lack of understanding on at least two fronts.

It's amazing how many people that read property articles on this website have no idea how Council rates work

thinktank

I see you have got a couple of up-ticks so this is just to correct your misunderstandings to avoid spreading misinformation.

Your two incorrect assertions are:

- "local councils are quite happy to cash in on the rates payments at an even higher rate", and

- "at an even higher rate than what the actual value of the houses are".

Firstly, in response to the second of these that house values are higher than they really are:

Ratable values are calculated by CoreLogic (formerly QV, formerly Valuation Department) quite independently of the local council. These are based on an algorithm of recent (previous three months) sales of similar properties based on a number of variables such as location, area of land, floor area of building, age of house, design, building materials, (and I think other variables such as aspect, other improvements, view) etc.

The new RV of a property is provided to the home owner who has the opportunity for it to be reviewed and in not doing it suggests that one agrees with it.

I am not sure what you base your assertion that this is at "an an even higher rate than what the actual value" - CoreLogic has based the RV on recent sales of similar properties . . . and if you think differently (and can justify it) you have every opportunity to have it reviewed when you are notified.

As to your other incorrect assumption "councils are quite happy to cash in on the rates payments at an even higher (property values"):

Each year councils prepare a budget based on their perceived needs - this is simply a budgeting process done totally independent of house prices. Once the community has been consulted, the budget is approved by council - this is all done without consideration of property values. It is only then that the total rate take is apportioned to individual ratepayers being based on both some fixed charges and other through a multiplier applied to on one's RV.

The movement of property values have no influence on rate take - property values can actually fall but rate take increase (as I have experienced).

Any increase in the total rate take is simply due to council's desire to increase its expenditure not increased house values - and even then although one's property's RV has increased it is quite possible that one's rate bill could theoretically be less if one's increase in RV was less than average.

Actually printer8 I'm gonna call you on that. If the property appreciates by say 20% over 3 years and the rates demands are a fixed ratio of the Capital value then the Council income increases by a commensurate amount. The appreciation % of property has far outweighed the appreciation % in maintenance costs. Given the Councils generally hike rates by 2-3% pa (if you're lucky) it seems the Councils are on the winning side. Given most towns and cities are in dire need of infrastructure investment (blatantly ignored/deferred by Councils) it seems the extra funds are channelled into pet projects, vote buying initiatives and various other wasteful expenditure. It's time NZ had an independent body to rein in the excesses of Local Govt and force a cost/benefit case to be presented to ratepayers - the satisfaction score of pretty much every council in the country indicates that Councils employers and funders (the ratepayers) are less than "less than" happy.

Hook

Absolute utter rubbish

Rates are NOT calculated on a fixed ratio. While RV are usually for three years the multiplier (the ratio you allude to) are actually calculated annually to meet rate take demand required for that year’s budget.

Total rate take is based solely on annual budgeting completely divorced from property values.

If you are unhappy with increasing rate take, it has absolutely nothing to do with increasing property values but rather council desire for increases spending.

Check your annual rate demands; you will see that the multiplier/ratio is not fixed but varies annually.

End of story.

If you are unhappy with increasing rate take, it has absolutely nothing to do with increasing property values but rather council desire for increases spending. - Absolute BS. The rates are increasing, the infrastructure is falling apart and the Council largesse is out of control. Councils are the biggest unchallenged parasites who have no measurable KPI's.

As for the "multiplier" I'll check the last 7 years of rate demands - I know you'll be proven wrong

Hook

Yes, you go check that annual multiplier - but be prepared to find that it is not fixed but that it varies annually.

I wait for your acknowledgment.

Still waiting for Hook, but in the meantime hopefully this will put things to bed.

Each year local councils prepare a proposed budget. Yes, there is there is a history of increases in budgets exceeding the rate of inflation and there are on-going issues associated with this. It is widely considered by many ratepayers that rate increases are becoming excessive and it is that – and not increasing property values – that are the cause for individual increases in rates. Hook; it is in councils budgeting you should be directing you comments and note that increasing RVs have nothing to do with it.

Councils are required to consult their community on their proposed budget and new items and specific expenditure will create debate. This is where people need to put in submissions – for example is a 10% increase in the rates budget justified, should Auckland Council be paying for either yoga classes or the America’s Cup, and is that water upgrade expense really necessary?

On the basis of that consultation, council confirm their budget – that is on budgeted needs and not property values.

Methods of determining individual rate assessments vary from council to council but are usually determined in two ways:

1. Uniform or fixed charges applied to each rate payer (this could include fire protection, refuse collection, recycling and sewage), and

2. A variable charge based on individual land and/or capital value

There may also be use charges such as for water if that is metred.

The uniform charge is clearly separate from one’s RV or property value.

The variable charge, based on individual land or capital value is simply about SPREADING THE SHARE each rate payer is expected to contribute. It DOES NOT INFLUENCE COUNCIL’S BUDGETTED TOTAL RATE TAKE. (The wealthy with more expensive properties and higher RVs will pay more than the less wealthy with lower RVs).

That variable is determined by a multiplier on either land and/or capital value; this will vary annually over the usual three years of fixed RV period depending on the council’s annual budget. Each year the council boffins look at the predetermined budgeted total rate take from variable charges and divide it by the total capital value to get that multiplier - that is then applied to each rate demand.

With new RVs:

Yes, if one’s RV increase is greater than the average, then one’s share will be greater than the average rate take. However, if one’s RV increase is lower than the average, then one’s share will be less than the average rate take (but given the levels of councils’ increased spending that is likely to mean some increase albeit not at the same level as other rate payers with higher increases in their RVs).

A fall in property values and consequently RVs will not reduce councils’ total rate take.

So please: increases in RV or property values DOES NOT INCREASE COUNCIL RATE TAKE, rather RVs are used to simply determine one’s SHARE of the budgeted needs.

I cannot be bothered reading all this but I call BS.

thinktank

Sadly your response says a lot.

"I can't care if I'm wrong, can't be bothered with knowing the truth, happy to remain in denial, happy to remain ignorant".

If you are going to post - then make sure you get it correct as this site isn't "Trump land".

I agree with all you say except the bit about community consultation setting the budget. What councils do is set their budget, then go and pretend to consult, then do what they wanted to in the first place, taking absolutely no notice of any community feedback/input.

P8... so are the One Roof valuations done in a similar way to CL and if not what are the differences? Also are the One Roof valuations reasonably accurate?

Karl

Both are similar in that they both use algorithms.

However, their data basis is different.

CoreLogic takes data from all property transfers over a three month period based on property transfer registrations with LINZ.

I am not sure what data One Roof use, but I suspect that knowing their affiliations it is probably based on REINZ data. This is based only on the previous month and properties which have gone unconditional (but are not yet settled or registered which can easily take one, two or three months more).

While CoreLogic data includes all transfers and its data is over a longer period it is delayed - it will include agreements signed up to four or five months previously as these have not only gone unconditional, but have also been settled and then registered with LINZ.

REINZ data has an advantage that it is more immediate but it is also has a number of flaws - prices can fluctuate monthly (due to weather events, sample size, and holidays) and only include properties sold by REA, etc.

With currently very high inflation, clearly One Roof can be arguably considered a better current indicator due to its immediacy.

While CoreLogic data is slow/dated, it is considered better for reflecting individual values for RV purposes as the sample size is larger (being all properties and over a three month period) and negates fluctuations due to variable events such as weather etc.

How accurate are CoreLogic and One Roof (and Trade Me's Property Insights)?

Well they are only algorithms and while based on a number of variables there is also many assumptions such as the condition of the house (e.g. the paint work, non-consentable improvements**, etc).

These algorithm based estimates are far better than RVs as they are based on more recent data (RVs can be two years old) but they are no or low cost so provide a good starting point and a great tool when starting to look although given their limitations (such as the actual condition of the house) too much weight should not be put on them.

A registered valuation will involve an inspection by a registered valuer who will consider the general condition of the house (but not issues covered by a builder's report) as well as other recent sales data and is deemed to be more reliable - but will cost $500 or $600 so one needs to be pretty sure about one's intentions.

From what I am hearing from a number of sources is that banks are more accepting about using algorithm data (usually CoreLogic) which saves the buyer the cost of a registered valuation as was typically required when I was buying properties 20 to 40 years ago. It seems that banks are only asking for registered valuations when there is some uncertainty as to value, or the buyer is very highly leveraged.

The bottom line is that the actual value of a house is what the seller and buyer agree to . . . and just how much value is the school zone or location worth to a particular buyer.

In these times of high inflation of house prices and price uncertainty, many sellers are going to the additional cost of going to auction to confirm the market price.

** Knowing a property that sold, had much consented work done on it (e.g. additional bedroom and new deck), the council adjusted its RV and this in turn quickly feed into both CoreLogic, One Roof and Property Insights descriptions and estimates of values.

P8... thx for such a detailed reply. Was just curious as One Roof just sent me a valuation showing my house increased $1000 a day since I bought it 9 months ago. Not selling so no more than curious as to whether things are as crazy as the valuation suggests. I am guessing that because it is in a low volume area of New Plymouth their valuation is likely skewed a bit by lack of sample size. In the end, it doesn't matter to me anyway. Thanks again.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.