A picture tells a thousand words they say.

Is a graph a picture? I'll leave you to discuss that among yourselves, other than to say that graphs can also say quite a lot.

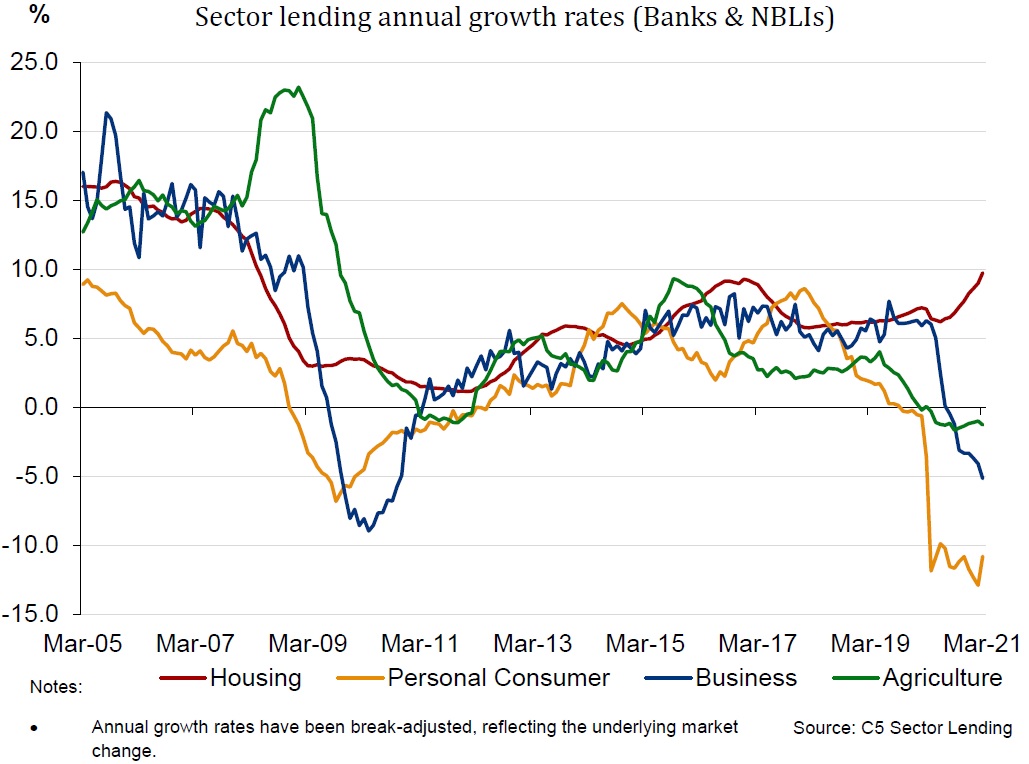

And the Reserve Bank stats people have produced a beauty (graph, that is) to accompany the latest sector lending figures published at the end of last week. It tells us more than words can possibly say.

But a few words first anyway.

For the record the figures show us that personal/consumer borrowing is continuing to atrophy. The rapid ascent of buy-now-pay later (BNPL) is presumably largely the reason for this - but as figures for BNPL debt are hard to track down it is difficult to precisely quantify the impact.

Agricultural lending is continuing to drift lower, with an annual rate of decline in this sector for every month now since April of last year. I think you can expect to see this continue.

Business lending actually increased a little in the month of April (emphasis on 'little') but the rate of annual decline went over -5%, which is the biggest rate in annual decline seen in about 10-and-a-half years since the aftermath of the global financial crisis.

So, it's all down, down, down for lending, apart, from well, would you believe it...housing.

It's been going up a bit.

As the earlier-released monthly mortgage figures showed, Kiwis borrowed a thumping $10.5 billion for new mortgages (yes, it was a record for a month) in March.

Perhaps not so surprising then that total housing lending stock increased by $3.7 billion (1.2%) in March. Both the numerical amount and percentage increase were records, bringing the country's mortgage pile up to $308.7 billion.

The annual growth in the housing stock rose to 9.7%, which was its highest level in just under 13 years.

So, here's what this all looks like.

Ladies and Gentlemen, I present to you The New Zealand Economy:

As you can see, all of the lines there have gone subterranean, apart from our old friend housing. Some might say we are putting all our eggs in one basket. (Again).

But I guess as long as we can keep swapping houses among ourselves at ever-increasing prices, we don't need a 'real' economy. After all, what could possibly go wrong?

78 Comments

In a nut shell. ..to hell with it they say, why try to run a business when I can invest in housing. I’ll just sit on my arse and the gummit and mr orful will print like there’s no tomorrow to ensure it will work out for me.

The government is not in the business of financing housing mortgages, that is why it licences commercial banks to create credit money for this purpose. Quantitative easing has nothing to do with giving banks money to lend, it is all about reducing interest rates which falls under the mandate of The Reserve Bank.

The Reserve Bank explains this here. https://www.rbnz.govt.nz/research-and-publications/videos/money-creatio…

QE is not new money in any case, it is only The Reserve Bank returning money to bond holders which is money that the bond holders already own. Only government deficit spending can create additional NZ Dollar Currency.

Give it up mate, that 'leveraging of the balance sheet' that is going at the Reserve Bank is an increase in the money supply. They buy the government bonds with MONEY created out of thin air, and the government goes and spends that money.

Are you guys talking about where most money comes from? It comes from bank loans, not from the RBNZ. The RBNZ sets rates through the OCR and UCM, but the actual money that ends up in the system comes from the loans banks make.

I am talking about QE, and I also understand about fractional banking.

Fractional reserve banking is not the main way money is created. Banks do not require any deposit at all in order to make a loan, the loan itself becomes the deposit. This was detailed in the BOE 2014 "Money creation in the modern economy": https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/20…

Are you the same person as treadlightly?

Have you read the document you supplied a link to?

The amount of money created in the economy ultimately depends on the monetary policy of the central bank. In normal times, this is carried out by setting interest rates. 'The central bank can also affect the amount of money directly through purchasing assets or ‘quantitative easing’.'

That document explains that it is not fractional reserve banking that creates the most money, which is why I posted it for you. I'm not anyone other than me lol, what? Yes, the RBNZ set rates, which affects the willingness to borrow, but the literal function of money creation is largely through the process of bank loans, but NOT through fractional reserve functions.

- 'The central bank can also affect the amount of money directly through purchasing assets or ‘quantitative easing’.'

Yes, and? Are you trying to tell me that a lot of the money in the real economy is QE, it isn't. Or are you trying to say that it is a method of how money can be created, it is. But my post to you about the BOE document is to explain it is NOT through fractional reserve banking. MOst money, and almost all the money in the real economy, is created through bank loans that are not fractionally reserved, they are created with no deposit at all because the loan itself is a depsoit.

The idea that banks can just create money with no reference to the deposits they hold is horrifying. We are all on the hook for what they are doing, there should be no bail-ins or bail-outs if / when this all goes belly up.

banks have to hold capital of 10% of lending and they have other liquidity requirements, they also need reserves to operate their exchange settlement accounts which can be used by the government if it needs to support the banks. A list here of liquid assets. https://www.rbnz.govt.nz/-/media/ReserveBank/Files/regulation-and-super…

Indeed, this is the manner in which bank loans are restained, the capital adequacy ratio. This is a separate ratio from the loan/deposit ratio, bank capital is the bank's money, not depositors' money.

Yes, correct, customer deposits are held in their reserve accounts at The Reserve Bank and are not lent out except to another bank if it is short of reserves. Reserves may also be transferred to the Reserve Banks capital account and held in the form of bonds and in this manner interest rates are controlled.

We don't know exactly what assets are being purchased or what the companies do with the money after the receive it though. If the government is just buying back its own debt that is held by pension funds and so forth. They may just leave the money in their bank accounts and do nothing more with it, they might reinvest in something else but they certainly won't be spending it.

Economist Prof Bill Mitchell explains here why governments issue debt and it has nothing to do with financing the government. http://bilbo.economicoutlook.net/blog/?p=45106

Warren Mosler has this to say about treasury bonds.

Proposals for the Treasury

I would cease all issuance of Treasury securities. Instead any deficit spending would accumulate as excess reserve balances at the Fed. No public purpose is served by the issuance of Treasury securities with a non convertible currency and floating exchange rate policy. Issuing Treasury securities only serves to support the term structure of interest rates at higher levels than would be the case. And, as longer term rates are the realm of investment, higher term rates only serve to adversely distort the price structure of all goods and services.

I would not allow the Treasury to purchase financial assets. This should be done only by the Fed as has traditionally been the case. When the Treasury buys financial assets instead of the Fed all that changes is the reaction of the President, the Congress, the economists, and the media, as they misread the Treasury purchases of financial assets as federal ‘deficit spending’ that limits other fiscal options.

https://www.huffpost.com/entry/proposals-for-the-banking_b_432105

The Bank of England tell us this about QE,

QE is intended to boost the amount of money in the economy directly by purchasing assets, mainly from non-bank financial companies. QE initially increases the amount of bank deposits those companies hold (in place of the assets they sell). Those companies will then wish to rebalance their portfolios by buying higher-yielding assets, raising the price of

those assets and stimulating spending in the economy. As a by-product of QE, new central bank reserves are created. But these are not an important part of the transmission mechanism. This article explains how just as in normal normal times, these reserves cannot be multiplied into more loans and deposits and how these reserves do not represent ‘free money’ for banks.

https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/20…

Smoke and mirrors nonsense. "QE does not represent 'free money'". This is known. But QE is done to 'game behavior' (or else it would be be the most unnecessary action undertaken by central banks).The argument as to whether or not it's money printing is superfluous. The MMTers do themselves a big disservice by arguing that the mechanisms and behaviors somehow exist in an alternate universe and are not attributed to the problems caused by constant expansion of the money supply.

I do not believe that the Bank of England mentioned MMT or supports it. MMT describes how our monetary system operates, it recognises the purpose of taxation and savings in controlling spending in the economy and of the money supply. MMT tells us that the governments spending should be used as a counterbalance to what is happening in the private sector so as to maintain full employment and to avoid large swings in the business cycle where we go from booms to busts.

The irony is that we are being set up for the mother of all busts.

ONLY because the new money created has mostly been spent in the wrong areas. Channelling to non productive, non infrastructural growth areas. Our economies have been converted from productive to rentier economies.

Yes, because true capitalism died some time ago.

And what exactly do you expect to happen when interest rate goes down? money supply increases. What is the ultimate objective of granting commercial banks liquidity (via QE) if not to underpin more credit creation?

It is true that the commercial banks create M3 by mortgage lending, not the RBNZ, but some of the most influential parameters underpinning commercial banks lending are directly set by the RBNZ or the RBNZ (or Government) has strong influence over.

Yes that's all correct, expect to say that the RBNZ is a mechanical function chasing inflation and employment. Its hands are basically tied. Never the less in Nov 2019 and Feb 2020 Orr warned the government that the RBNZ response to an economic downturn would be rate cuts and UCM, both of which could reasonably be expected to impact house prices and worsen wealth inequality. He expanded to say the Government has the powers to manage those externalities and that use of those powers would be warranted. Robertson retorted saying he was skeptical of the link between interest rates and house prices and then did nothing until it was much too late.

Sure. I personally do not beleive the independence of the RBNZ. Specially after Labour party changing the RBNZ. Orr is appointed by the Labour party. I personally see all these to be Labour party performance. The RBNZ is just a very good curtain to hide behind.

Labor is trying to blame the RBNZ, but the RBNZ is not yet a pawn, it behaving genuinely independantly. The RBNZ is doing, pretty much, what it has always been trying to do; keep inflation between 1 and 3%. I would actually hazard to suggest Orr and Robertson are hostile to one another.

The Reserve Bank is doing, pretty much, what is has been doing since the GFC: following in lock-step with The Federal Reserve and slashing interest rates and implementing QE. The Reserve Bank is far from independent!

It's independent; it must effectively follow the Fed but that not because of a lack of independence but rather because of how exchange rates work to push or pull inflation out of an economy.

“Yet” being the operative word here. Having ones remit significantly amended 3 times in the course of 1 term of governance (5 years) does not bode well for their independence.

Yea I agree.

Worked for us. Not hard to see why punters jumping in.

Listed the business for sale day after 2017 election when I knew that was the end of meaningful profit. Went all in on property. Over 1M CG last year alone.

Yes it's wrong but after 30 years hard slog in horrible jobs earning zero I'm not trying to win any medals.

A posterboy of boomer-bribery success story from Orr/Labour globalist ponzi scheme to rort young working kiwis/create brain drain whilst creating excuse to bring in cheap labour. Every body happy.

So where is the top, when incomes are not going up at anywhere near the same rate & interest rates cannot be cut forever? Are the 'punters' jumping onto a frying pan while those who have cashed out count their millions? Should those gains be allowed to be kept if it all goes belly-up, and it is confirmed that the banks have been running a Ponzi scheme? Who should have to pay the piper?

The Reserve Bank tells us here that it is buying back up to $100b of its own bonds for the purpose of reducing interest rates and so it is a repayment of money and not new money.

https://www.rbnz.govt.nz/monetary-policy/monetary-policy-tools/large-sc…

When (eventually, 6m after the time period) we get some accurate idea of what national income has gone up (Not GDP, but GNP) we can see how much debt increase is exceeding income increase. As output per head was anaemic in years 2011-19 approx, the lack of immigrants in last year will we assume do nothing for productivity .

So, debt will continue to outstrip income, meaning that servicing the debt requires lower rates? Which are pretty much off table now. Problem

In actual fact on Reddell's blog a little while back, he quoted official figures that showed productivity rose 2.5% from Dec 19 to Dec 20, probably because of declines in low productivity tourism and hospitality industries. Immigration does nothing to improve productivity, we've had high levels for near on a decade and our productivity continues to decline.

Keep in mind too that these are growth rates. So a flat horizontal line on this graph would indicate exponential growth in absolute (dollar) terms.

I wonder what that little hockey stick at the end of the housing graph looks like in absolute terms.

In the same way that the 2000 period while worse in percentage was lesser in absolute terms.

Absolutely horrific. And under Labour they have clearly made the situation dramatically worse, when they came to power saying they would do the opposite.

As if we need any more evidence of the utter incompetence of our leadership...

Blobbles how would you have tackled this problem if you were elected?

Why deflect attention away from the party which campaigned on it?

No deflection at all - simply asking a valid question due to the many posts offering no solutions but daily blame gain. Its tedious seeing the same comment daily - how about a deep dive into why kiwis are so obsessed with property valuations?

Halve the income tax on income derived from rent. This should cause a surge in investor demand allowing housing that was previously not sufficiently profitable to be built whilst everyone tries to become a property investor. The surge in supply will eventually drive rents down as all the new investors compete for tenants. Eventually there will be more dwellings constructed than there is demand for, as developers build based on historic (3-5 year) demand models. This will drive prices down. The best part is that it will all have been paid for by those who can afford to buy rental properties and they did it eagerly! Only a fool tries to work against the market, it is far easier to work with the market. The problem is that the government is ideologically opposed to implementing solutions that work if they look like they may in the very short term benefit the wrong demographic (ie. they lack the ability to plan for the medium / long term).

It takes time for the construction side of things to ramp up, it's unclear how much of a difference this would have made besides pricing fhbs out of the market. House prices are so exorbitantly high already we should be building like crazy, but the costs (land, council fees, construction labour/materials) are also extremely high compared to other countries.

A properly incentivised market can work miracles. With enough demand you could get a third player in to disrupt the existing materials duopoly. Where currently developers prefer to build McMansions, you would shift preference to compact (higher density) investor units. I believe this was implemented in Malaysia when they had an affordability crisis. 4 years on they now have a massive oversupply of investor grade dwellings. Their supply response is faster because they permitted Chinese developers to enter the market with their own temporary workforce (paid in China).

https://www.propertyguru.com.my/property-guides/rental-income-exempted-…

Whilst the initial demand spike may temporarily price FHB out of the market, in a few years once the oversupply develops FHB facing lower rents will be better able to save a deposit & investors will be keen to sell off the rental properties that become difficult to rent out, resulting in investors essentially subsidising the homes of first home buyers.

Q. Why were LVR's lifted as soon as it looked like prices might fall?

A. To ensure a new pool of punters to enter the Ponzi to keep prices up and the bubble bouyant.

It's tedious this mentality we have in NZ that because prices haven't fallen that means commentators were wrong. There has been a massive and ongoing bailout. If I fall out of my boat continuously and each time have to be rescued am I really a great sailor? It is only due to the actions of the Reserve Bank and government continually bailing out the housing market via ultra-low interest rates, QE, record deficit spending, and mass imigration that the thing stays upright and still inflating. Add in intransigence on the RMA, talk about infrastructure but no action, and the utter failure of 'KiwiBuild' and you have another set of governmental failures which have contributed to a problem they don't seem to want to fix.

No lol, they did that to boost consumer spending and keep inflation and employment at target levels. Just read the RBNZ remit. The second half of what you are saying though is spot on, we need to, and can, build more houses.

Just to elaborate briefly though, if you are a commentator and don't understand the RBNZ remit, and your projections on this don't work out because of the RBNZ actions, then you sir are the bad sailor, because the RBNZ actions are the result of a publicly available remit.

I would have thought that removing LVRs was designed to ensure that our building industry did not shed its workforce thereby exacerbate a housing shortage.

Furthermore is the LVR not designed to be removed in the lead up to any sort of economic uncertainty? Just imagine the margin calls if a LVR were strictly enforced during a crash.

The CGT and Fair trading Act prohibit 'margin calls' on most property lending. But to answer your main point, the RBNZ remit is inflation targeting and its actions must always be toward that ends, or in some cases regualtory.

The way inflation is being calculated is not fit for purpose. The weighting given to housing is far too low.

GDP as a calculation of economic strength / growth is not fit for purpose either, since rather than reflect an economy that is humming along with excellent output and productivity a large part of it simply captures government spending and 'investment' - which these days is more often than not malinvestment. Bidden is presiding over the deficit spending of trillions and trillions of dollars, and that is being portayed in our media as a US economy that is thriving.

Inflation uses things like hedonic adjustment which creates a very misleading indicator, so I agree but I'm not sure why you are saying this to me? GDP is a dog pile of problems as well yes, but again why am I involved with this?

Because you are talking about a fundamental remit which is if fact monitoring something that is fundamentally flawed, so the whole thing is a farce.

Imagine I have a watch dog monitoring a barn full of chickens. The front door is closed, but all the chickens are escaping through a hole in the back of the barn. The watch dog is apparently doing a great job on the surface of things, yet the appearances are not as they seem: in actual fact my erstwhile watch dog is presiding over a fiasco.

I personally agree the RBNZ remit is flawed, but that is not the RBNZs problem and not directly related to what i was replying to. If you read the post i was replying to youl see I was simply explaining that the RBNZs actions were not to shore up the building industry, but rather to shore up inflationary expectations.

Because you are talking about a fundamental remit which is if fact monitoring something that is fundamentally flawed, so the whole thing is a farce.

Imagine I have a watch dog monitoring a barn full of chickens. The front door is closed, but all the chickens are escaping through a hole in the back of the barn. The watch dog is apparently doing a great job on the surface of things, yet the appearances are not as they seem: in actual fact my erstwhile watch dog is presiding over a fiasco.

Until people understand that until you have a free market land supply policy, it is almost impossible for anything else to work any other way than what it is doing, ie people speculating for capital gain, resulting in unaffordable housing, then there is no solution that can be implemented without causing pain to one group or another.

Once you understand the importance of the right land policy, then you will understand its relationship with all the other inputs and if implemented then all these other inputs self-correct as well, resulting in far more affordable housing.

That old saying, 'if the land is wrong, then everything else is made wrong,' is true.

Labour's problem is that their ideology is counter to having affordable land supply, irrespective of demand.

USA, Canada, Australia..just to name a few countries with exactly the same problem, must be a coincidence or something bigger afoot..were is bobbles?

The point is, that you would have not said that if National was in charge. You would have attacked them relentlessly. You would never have said, you know guys, there are greater powers than National in play, so this cannot be attributed to them.

Having so much bias is not limited to you, me or other commentators. But it is certainly a massive barrier in our way in searching for a real solution.

"You would never have said, you know guys, there are greater powers than National in play, so this cannot be attributed to them." WRONG of course I would but at the same time would have been probably recovering from Coivid hopefully. And once again another post raving on about political parties. Its a world wide problem and if you really think that little old NZ government can sort it in a few months your barking mad.

Your generalizing too much about the USA. California is akin to what we are doing, Texas is what we should be doing. It's chalk and cheese.

Blobbes was not elected dope

'There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.'

- Ludwig Von Mises

No one has yet been able to produce a mathematically sound model that demonstrates that.

While not a fan of the gold standard the Austrian economists supports among some other things, their business cycle theory intrigues me.

Banks expand credit well beyond their own assets and by the funds of their clients, often supported or encouraged by the setting of low interest rates by a central bank. This additional credit flow into the economy from increased borrowing for capital projects stimulates economic activity. Projects which would not have been started before, seem now profitable, creating malinvestment. They increase demand for production materials and for labor and their prices rise, which, in turn, leads to an increase in prices of consumption goods. If the banks would stop the extension of credit, the boom would be rapidly over. To prevent the sudden halt of this boom (and the resulting collapse of prices), the banks must create more and more credit, and the prices will rise even more.

"ABCT tells us nothing about exactly when the boom will break. The theory claims that eventually costs will rise in such a way that make it clear that the longer-term production processes falsely induced by the boom will not be profitable"

banks are licenced by the government and so the government can apply any regulations to the banks that it wishes to. Monetary policy was chosen as the option to support the economy through the covid crisis and so maintain spending in the economy and to support jobs. Using fiscal policy would have been the other option where the government spent into the economy itself and this would have lessened the increase in house prices.

In the US the President gave out money directly to consumers to spend.

The RBNZ requested the government do its part and use fiscal spending, but Robertson failed to deliver on the scale needed, saying, ~'hes not sure he believes in Modern Monetary Theory'.

"Projects which would not have been started before, seem now profitable, creating malinvestment."

That is misleading. Yes, it reduces the level of profitability required for a business to succeed which should lead to an increase in malinvestment, but that does not mean it is better or worse because malinvestment is not the only variable, it also increases the number of profitable investments and reduces the number of profitable failures that occur when a crash cuts too deep. Those points are just the start of a complex set of modeling problems. None of the models proposed by hard money advocates or anti-stimulatory advocates have ever been both sound and able to show why exponentials require a correction. Exponentials can be easily transformed to liners, showing its at least mathematically sustainable. The only argument i have seen which had merit was rate of change arguments. But there is little to indicate the rate of change itself is yet a problem, nor a well explained mathematical model that could be reasonably expected to transition us to an unsustainable rate of change.

Still there isn't much to prove the system is fine either, and certainly, Picketty has found good evidence that wealth inequality is likely a serious and building social issue that is unlikely to be arrested by means other than catastrophe

Laminar - Steve Keen has a model which demonstrates this. See his Minsky model.

Good to see the conviction.

The activities surrounding housing transactions is also a big part of the economy and can be considered "real" and productive.

Ahh I was wondering where the NPCs had gone.

https://www.trademe.co.nz/c/property/news/average-new-zealand-house-pri…

Is this the data Robertson and Orr were waiting for before the Big Announcement by Mr Orr on 5th May or will it stillbe Wait and Watch........Wait for God to do a miracle to solve the housing ponzi created by them.

People want what they want despite nanny state telling them they’re being naughty.

David, last month you were telling us all how Labour's policies would stabilise house prices. The modest home I bought in November just saw a $30k value rise from last month. That's as much as the total four months previous.

Is a rise in the price some people are prepared to borrow to pay for houses actually the same thing as a rise in the value of a house? Are the houses really _worth_ that much?

I was born in New Zealand but I've lived here in Tokyo for almost 25 years and I have to say I'm struggling to comprehend the prices of houses in New Zealand. What makes buyers think they're worth the vast sums they're paying for them? Japanese house prices have been falling for many years and show no sign of doing anything else. Kiwis may like to think the New Zealand housing market is somehow 'different' from ours but really it isn't. Not in the fundamentals. The only difference is Japan's property bubble burst long ago and New Zealand's property bubble still hasn't. May the gods help you when it finally does go, because you're going to need all the assistance you can get.

When I was looking to buy at the end of last year, most properties in the $450k to $600k range were certainly not worth the amount being asked for, or what was paid.

Our lawyer suggested getting something bigger rather than be a part of the massive competition between investors and FHB's in that price bracket. He was right. We ended up paying $700k for a house with an RV of $630k, but which was valued at $710k before we even moved in.

Fortunately my father was able to gift us $20k to add to the $120k (mix of KiwiSaver, TD's and ETF's) we had saved up over the last 8 years, so we got to put down a 20% deposit. And, since we had just finished paying off the mortgage for the 1LDK in Saginomiya for my mother-in-law, we have no problems servicing a $560k loan.

But comparing the 2 properties is like apples and oranges. The place in Tokyo is a 1 bedroom, 1 lounge, 1 dining/kitchen, 3rd floor apartment of about 38 m2 in an 8-story building only 3 minutes walk from the station, worth around ¥23 million (NZ$293k). Our home here is 4.5 bed, 2.5 bath, single story, 198 m2 on a 800 m2 section about 15 minutes drive from work.

Like Mark Twain said, "Buy land, they're not making it anymore."

こんにちは外国人外国人. A fellow gaijin here. (I'm a little ways southwest of you.)

Unn Zudd uss duff'runtt unn spusshool.

Only, it isn't. NZ's residential property prices have been talked/bid up to insanity heights by people convinced they can never lose, no matter how much they pay. These are dank pine and gib rot boxes on muddy sections in a country most people can't even find on a map of the world, and most wouldn't waste their time trying. But of course Kiwis are eternally convinced "the whole world is watching us, and everything we do puts Unn Z'ulln on the map!", despite all evidence to the contrary.

What could go possibly wrong borrowing millions to get on the property ladder, mate? It's not the house, it's the land! When the zombie apocalypse/alien invasion/global pandemic hits, everyone on Earth will rush to Unn Zul'nn to buy up all the houses at top dollar and we'll be rich! Rich! RICH!

A fool-proof plan concocted by and for fools. xD

Government has your back with property. Eventually some future government may commit political suicide by openining up the supply side but it's unlikely to be any of New Zealands three most preferred political parties. They know the game, as long as house prices keep rising the middle class turns out to vote for them.

What that graph tells me is that housing is sucking the life out of our economy and that the governments moves to to stimulate the economy by flooding the economy with liquidity is having the opposite effect.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.