The massive buying splurge housing investors went on after the lifting of loan to value ratio (LVR) limits last year has seen their monthly share of the mortgage market heading back towards the high levels seen in mid-2016 prior to them being hit by deposit restrictions the first time around.

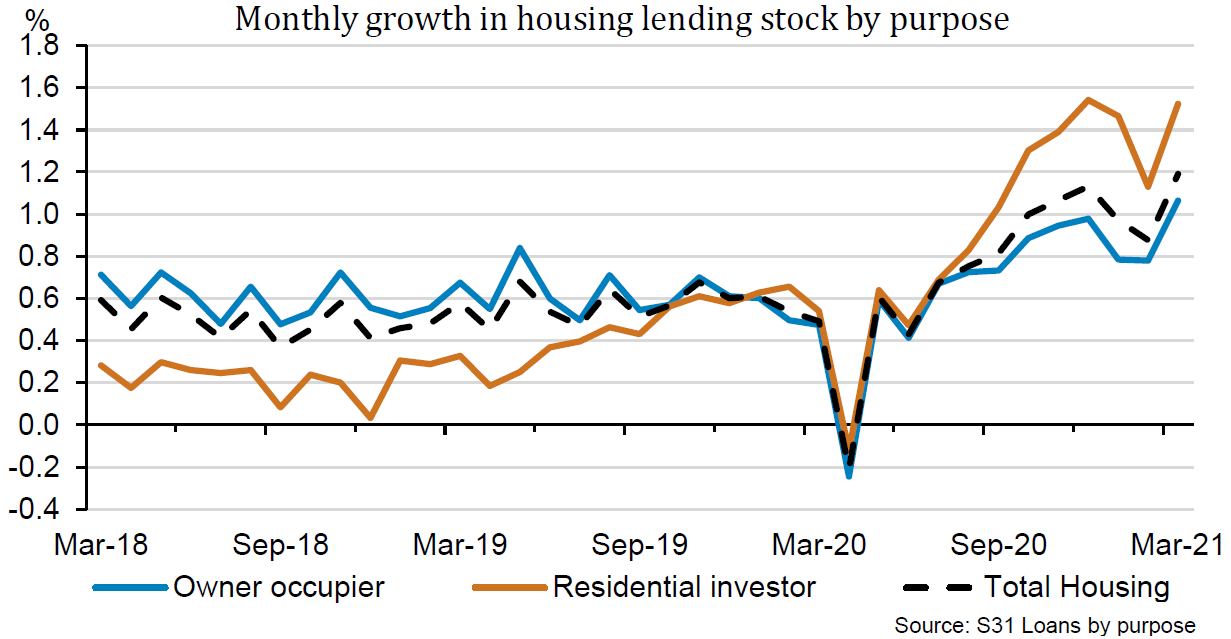

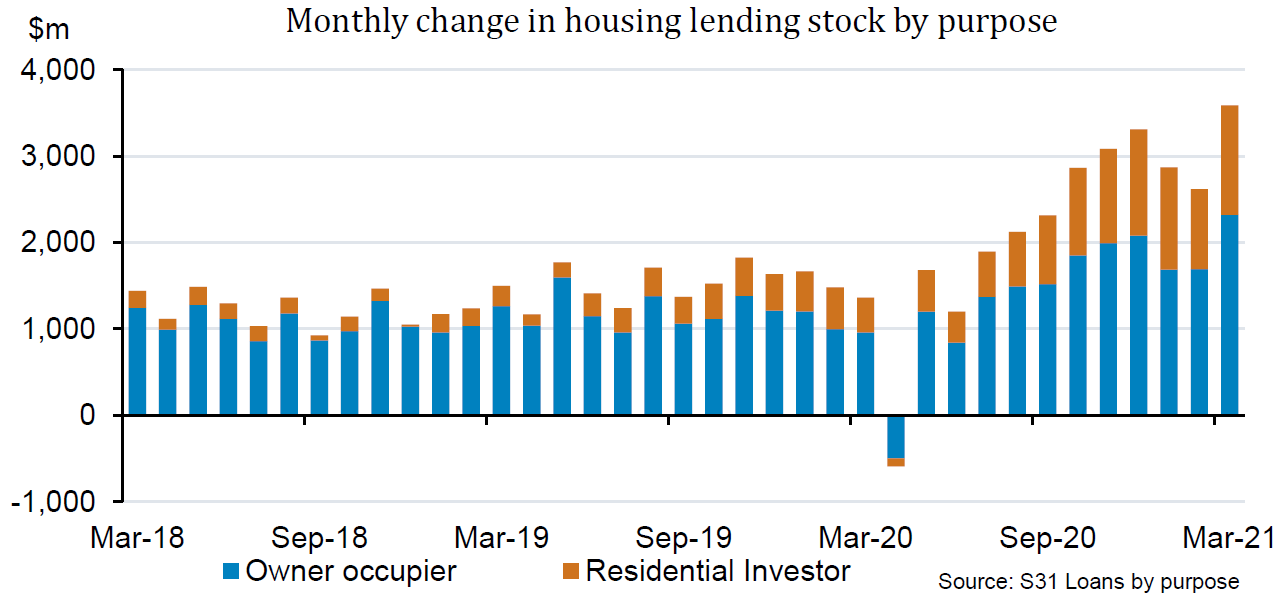

And figures in the Reserve Bank's latest bank loans by purpose monthly release show that in the six months to the end of March 2021 investors increased their share of the mortgage 'stock', the total amount outstanding for mortgages, by $6.713 billion. That made up some 36.6% of the $18.346 billion increase in the total bank mortgage 'pool' during the six month period. Total bank mortgage debt outstanding has now topped the $305 billion mark. There's been a recent string of record monthly additions to the overall stock total, with more than $3.7 billion (new record) added in March.

It's worth taking a snapshot of where we are with these various figures at the moment because the recent re-imposition of LVR limits and policy changes by the Government could see things changing quickly in the months ahead.

In terms of the overall share of that mortgage stock, investors now have $84.323 billion outstanding in mortgages, which makes up 27.6% of the total outstanding mortgage stock. In the six months to the end of March that share increased quite sharply from 27.1%. But it is still some way shy of where it was at the end of 2016 (which is as far back as this data series goes), when it stood at 29%.

Through the early part of 2016 the investors had regularly been accounting for about a third of new mortgages every month. But that was stopped when the RBNZ clapped 40% deposits on them in mid-2016.

Now of course as of the start of May, we officially have 40% deposit rules for investors again, so, it will be very interesting to see what happens to their share in coming months. (And that's before we even start considering the impact of the Government's recent housing policy changes.)

But in the past few months its been all onwards and upwards for the investors.

In the six months to the end of March, the investors increased their share of the mortgage pile by some 8.6%, so an annual growth rate of in excess of 17%. During the same six month period the amount outstanding in mortgages for owner occupiers (a figure that includes first home buyers), rose by $11.633 billion (5.6%) to $220.716 billion.

In terms of where the investor interest has been coming from, both recently and historically, it was interesting to note that Ministry of Housing and Urban Development material recently released relating to the Government's housing policy changes, stated that about 20% of current private rental properties had been bought in the past two years. This information came from CoreLogic.

The material went on to state (again from information supplied by CoreLogic) that purchasers owning multiple properties have made up between 35%-40% of property purchases over the last decade. Over half of those purchases were made by owners with between two and four properties - and that normally included their main home. Fewer than 15% of multiple property purchasers owned 10 properties or more.

The point is: A lot of properties have been bought as rentals in recent times, with seemingly a lot of those bought by people who might not be seen as "serious" investors (IE perhaps just buying one or two rental properties). So, it could be pretty interesting if these smaller scale investors do start deciding to quit their investment properties. There's plenty to look out for in coming months.

Dairy debt down

Changing tack somewhat, the same RBNZ loans by purpose figures give a detailed breakdown of business and agricultural lending.

The agricultural lending figures have been soft for some time and have shown an annual rate of decline every month since last April. But those 'headline' figures, if you will, don't tell the real story, which is the large drop off in dairy lending.

Dairy lending has fallen $1.3 billion between August 2020 and March 2021.

And if you go back two years to March 2019, the amount of outstanding dairy loans is now down nearly $3 billion - or over 7% - since then. (It's gone from $41.309 billion to $38.38 billion.)

The Reserve Bank's Financial Stability Report last November talked of banks seeking to diversify their agricultural exposure, while there was "limited appetite for new dairy lending".

ANZ chairman John Key said last October the banks were "all full" on agricultural risk, so its the only area they can "reprice"

It will be interesting to see if the extremely buoyant dairy prices that have been seen this year - and are likely to continue - will encourage any change in thinking by the banks.

13 Comments

Tell us something new.

David, it is people like Robertsons and Orrs that have to realise ( stop ignoring and denying), that unless and untill they been in power decide and act, it will not stop in the real sense.

Understand that both the hero of the housing ponzi were waiting for some data / information till may before taking action against speculators by stopping interest only loan ( otherwise why would they not act in March itself, if not before).

Now are they convinced or will they still keep on avoiding / delay as are masfer in fibbing and manipulationso finding excuse to not act will come naturally to them

Interesting : Question of the : Will Mr Orr follow Wait and Watch Approach or will he......

The reality.

Low interest rates is just one contributing factor to recent house price inflation but that is a result of BOTH investor activity and also owner occupier's (including FHB).

Investors however seem to be currently the popular target both by posters and by Government.

The reality is investor activity has been far from historical highs and FHB above historical lows.

RBNZ mortgage data shows that for the nine month* period June 20 to Feb 21 investors accounted for 36,873 mortgages, where as for the same nine month period June 2015 to Feb 16 the number was 48,975. Since Sept 2016 the number of monthly mortgages to investors has been under 5,000 but for 18 months over 2015-16 the monthly figure was generally over 5,000, often over 6,000 and a high of 6,926 in May 2016.

And FHB have not been totally squeezed out to historic lows. For the same 2015-16 nine month period the number of FHB was 16,999 whereas in the 2020-21 period there were 25,080 FHB.

While low interest rates and IO have been a driver, the other equally significant contributing factor not generally considered is housing shortage. And please don't tell me that there isn't a significant problem - with 1700 people in motel accommodation here in the Hawkes Bay (1.3% of the population) and similar problems in Rotorua, Hamilton and Auckland. It is for this reason there is upward pressure on rents and compounded by the need for accommodation supplements as a consequence.

Unfortunately poster on this site tend to focus on just housing affordability - that which affects what is seemingly the middle class, white, young and reasonably well-educated cohort which seems to frequent it.

Government and RBNZ actions may slow house price inflation but until the root cause of a supply issue is addressed housing the housing crisis will continue.

Discouraging investors is simply going to reduce much needed rental supply. For FHB the shortage of houses will mean that they are going to remain largely unaffordable and a significant correction in the short term is unlikely.

As for IO - well just under two thirds have gone to OO. By all means, stop IO loans as it may cool the market further, but that is not going to produce one additional house.

As for rents - until the supply problem is sorted and while the Government continues to make it more difficult for investors, there can only be upward pressure on rents. Recent Government and possible RBNZ actions are going to simply compound this. To most renters - the chances for a rent reduction before Christmas 2022 seems most unlikely.

* The nine month period was taken to avoid the initial temporary impact of Covid.

While low interest rates and IO have been a driver, the other equally significant contributing factor not generally considered is housing shortage.

Nah. The biggest driver is the monetary system that enables banks to lend into existence primarily through mortgage lending thereby destroying the value of labor, particularly for young people and low income earners.

J.C.

“Destroying the labour of the young”

So why then is FHB activity currently at a high? Nov and Dec two highest months for number of FHB since RBNZ data first available for 2014.

I appreciate that it is tough, but remember over 60,000 FHB with goals and initiative have got out a purchased a house in the past year.

I said 'destroying the value of labour.' That is exactly what money printing does.

All interesting info.

However, as so often with contributors, you do not distinguish (and neither does 90% of MSM) between demand and supply for owned/mortgaged property v rented property

As I have repeatedly complained, NZ has a huge shortage of good quality, 3-4 bedroom property for rent, at an affordable rent. This combined with lousy median wages and dominance of part time working compared to its level of 35 years ago, is major cause of increase in homelessness and food poverty since 2015. Government does little to nothing about this and focuses on needs fo social housing type tenant and FHB, leaving out the largest group of need by number.

Government refuses (as gov did in 1950-76 approx) to build such rented accommodation with DLO labour force, demonstrating its slavish conformity to treasury ideas of what can be done and by whom. Builders happy to build for profit in places people I have identified do not need. That increase in supply does nothing for such people

Old news

When did the RBNZ remove LVR requirements? Was it in May 2020? How long did they need to reinstate it? While the house was burning, raging they were still thinking about it!!! They removed the LVR requirements in a heartbeat but reinstating it took forever with ample notice. Why? Who are they really working for? How do they see investment in residential property as a economic measure? Also why are they still thinking about the interest only loans? What are the reasons? They should declare their vested interests.

Passerby

Interesting banks collectively introduced LVRs around October 2020.

Do you really think that the big four banks did this individually on their own initiative, and that RBNZ may not have a presence in the collective decision? After all, RBNZ communicate with the banks all the time and FLP is one aspect that they will jointly have agreed upon - and that would not have been decided on in isolation of other decisions.

There is good reason for RBNZ not to act in haste in this instance. Significant outbreaks of Covid have been a risk and any RBNZ action requiring it to be retracted has significant consequences in the message it sends - banks can readily to this without wider consequences.

Rather than looking at it simplistically that RBNZ hasn't acted or was slow in doing so; think a little deeper and ask yourself why did the banks act and it was unlikely not simply in their own risk assessment. That may well be a likely possibility.

Agree.

They are the boss and they can choose when to follow ' least regret' and when to follow ' Wait and Watch'.

Arguments in anything can be presented in favour or against but truth prevails and truth is that now they stand exposed and instead of acting when is clear, what the effect of their policy has been on housing, still are in denial mode.

If anyone has any doubts,wait for tomorrow's announcement or silence by Mr Orr.

This is the problem. It's old news to us. But it's absolutely scandalous that it's gotten to the point where it's basically boring.

I could be inclined to just ignore any of these things totally, but money spent on bigger mortgages is money not spend on discretionary spend, having families, investing in business and making us a better place to live or improving our well-being.

Robertson should have to justify why we are feathering the nests of Australian Bank Executives and why meaningful change that stops an erosion in NZer's living standards is happening at a glacial pace, if at all.

Our banks have contacted us a couple of times over the last 6 nonths to offer us pre-approved mortgages if we wanted to extend our investment portfolio. New Zealand commercial banks seem to have an unconstrained appetite for growth at any risk level, just ten years ago it was the exact reverse with every dollar being scrutinised and needing to be signed off by a manager. They can't be working to any business strategy or plan, there is no continuity or approach to managing risk.

I view the figures with some suspicion.

CoreLogic attempt to match the ownership details of a newly purchased property with any other property already with that owner.

If they find a match, then that new purchase is classified as an investment property.

But - consider the following recent statement from John Bolton of Squirrel Mortgages:

"The problem is if you are wanting to change your house you can't buy subject to the sale of your house, you have basically got to take the plunge. People pretty much need to buy first and then sell because you don't want to sell and not find anything."

So, in that case, such a purchase of a property intending to be owner-occupied when the purchaser does sell their previous property would be falsely classed as an investment purchase.

As is often said, statistics can lie.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.