By Gareth Vaughan

Much as reports of the demise of American writer Mark Twain turned out to be wrong, so too have predictions of the demise of banks.

As long ago as 1994 Microsoft founder Bill Gates described banks as "dinosaurs" that could be bypassed.

More recently similar views have been espoused following the emergence of competition from peer-to-peer (P2P) lending, buy now pay later (BNPL) services, open banking, big technology companies moving into payments, and cryptocurrencies.

Of course there was also the reputational battering banks took through the Global Financial Crisis (GFC) when bankers blew up financial markets taking some of their own banks down with them and, Lehman Brothers aside, were bailed out with huge quantities of public money yet somehow avoided jail. There was also Australia's Royal Commission revealing damning conduct by the parents of New Zealand's major banks, including charging dead ex-customers fees.

Yet as we sit here in NZ in the middle of 2021, our banks are sailing serenely on. They're posting record profits against the backdrop of a global pandemic. In the March quarter alone the NZ banking sector recorded a 21% surge in net profit after tax to $1.643 billion. Does this seem like an industry under pressure?

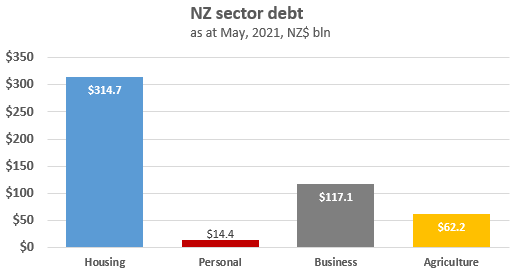

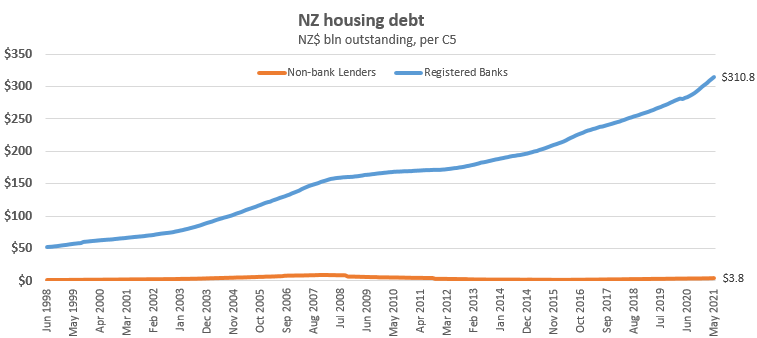

Banks' cornerstone role in our credit/debt centric economy means with the onset of COVID-19, mortgage deferrals, the Government's wage subsidiary scheme, a record low Official Cash Rate, the removal of loan-to-value ratio restrictions, and quantitative easing, all combined not to merely keep the lights on, but to send housing lending growth into the stratosphere. For anyone who has been living under a rock, housing lending very much dominates overall lending in NZ, and banks led by ANZ, ASB, BNZ and Westpac, dominate housing lending.

Over the past few years various emerging competitors have been touted as having the potential to eat banks' lunch.

Emerging hot on the heels of the GFC, P2P lending appeared to have the potential, in time, to do to banks' consumer and SME lending what Trade Me did to second hand sales and newspapers' classified advertising, as well as posing a threat to banks' deposit gathering. Remember P2P sees companies licensed by the Financial Markets Authority run websites as intermediaries matching borrowers with lenders and charge fees for doing so.

But thus far it has only scratched out a miniscule niche in the NZ financial system.

We've also had the emergence of open banking. The idea behind open banking is it will give customers greater access to and control over their own banking data, and require banks to give competing third parties access to their systems. However, open banking's development in NZ, being overseen by Payments NZ - which is majority owned by ANZ, ASB, BNZ and Westpac - is proving to be very slow.

BNPL services, which allow consumers to purchase and obtain goods and services in-store or online immediately, but pay through installments over time, are certainly making an impression on banks' personal lending and credit card business as highlighted recently by credit bureau Centrix. Banks are certainly taking notice of BNPL, as are regulators who are likely being encouraged by banks. Commerce and Consumer Affairs Minister David Clark said in June a discussion paper on potential regulation of the unregulated BNPL sector will be issued later this year.

Last year I wrote about Visa and Mastercard and how they are adept at embracing new threats to their business. This enables them to clip the ticket when new payments technologies and services emerge. Visa calls this its "open partnership model." Banks are doing something similar. Just this week it emerged that Westpac is to be Humm Group's exclusive NZ partner for its Bundll BNPL service potentially taking up to a 49% shareholding.

The partnership with Bundll, which will use the Mastercard network, saw Lewis Billinghurst, Westpac NZ's head of digital ventures, gush that the "reinvention of consumer lending" by BNPL services appeals to Westpac. And Humm's deputy CEO Chris Lamers was equally excited, saying Humm "loves the idea of getting together with such a well known New Zealand company [as Westpac] to make sure as many kiwis as possible can get access to this product."

ASB also has a relationship with a BNPL service, Klarna, in which its parent Commonwealth Bank of Australia has invested. Klarna launched in NZ in May.

Back to Westpac, it has had a relationship with fintech Moven since 2014, with Moven today powering Westpac's CashNav app. Moven's founder Brett King hosted a show on Voice America radio called Breaking Banks and then partnered with one. And Westpac also took a 32% stake in open banking fintech Akahu last year. Even in P2P lending we've seen Heartland Bank take a shareholding in Harmoney, and both Heartland and TSB lending money through Harmoney.

All this reinforces the embracing of the Visa and Mastercard business model of partnering with threats to your business. This could be seen as a case of if you can't beat 'em join 'em, or perhaps keeping potential enemies close. And for newcomers partnering with banks, they are salivating at the prospect of gaining access to big bank customer bases and their rivers of gold revenue streams.

The threat technology giants such as Google, Apple and Facebook pose to banks has been well documented. But remember when Apple Pay first launched in NZ? It was via ANZ-issued Visa credit and debit cards before expanding to include the customers of ASB, BNZ, Westpac, plus the Flight Centre and Q mastercards. And Google Pay? Yep, users also require ANZ, ASB and BNZ issued Visa cards.

Bloomberg reported this week that Apple is working on a new BNPL service that would let consumers pay for any Apple Pay purchase in installments over time. Guess what? There's a bank partner. It will reportedly use Goldman Sachs as lender for the loans needed for the installment offerings.

Big tech certainly has huge potential in banking services. The Bank for International Settlements (BIS), the central bank's bank, last year estimated big tech companies peddled as much as US$572 billion of debt globally in 2019. And Facebook's push to develop the stablecoin Libra certainly lit a fire under central banks' moves towards central bank digital currencies (CBDCs). A stable coin is a type of cryptocurrency backed by a reserve asset, such as fiat currency or gold.

Announced amid much fanfare in 2019, the Libra project initially counted PayPal, Mastercard, Vodafone and eBay among its backers. However all quit. Last November the Financial Times reported Libra will likely launch this year, via a single coin backed one-for-one by the US dollar. It requires approval to operate as a payments service from the Swiss Financial Market Supervisory Authority. After its 2019 unveiling, Libra received a sceptical reception from global regulators, who warned it could threaten monetary stability and become a hotbed for money laundering.

In terms of big tech and banking services, a factor to watch I believe is the extent to which tech companies strive to avoid being regulated like banks. I expect they'll bend over backwards to avoid this.

CBDCs certainly have the potential to be very disruptive indeed for banks. These could be complementary to cash, and/or serve as digital fiat money. As I recently reported they could be used to cut out intermediaries such as banks, thus giving the public a much more direct relationship with their central bank. However, this scenario is not on the BIS agenda, with CBDCs being touted as a means of shoring up the status quo, private sector bank intermediaries, and all, in a world of big tech companies and cryptocurrencies. (The Reserve Bank is planning public consultation on the pros and cons of a CBDC).

In terms of cryptocurrencies, none of the country's big five banks (ANZ, ASB, BNZ, Westpac and Kiwibank) currently have any direct exposure to them. For now these banks are doubtless wary of the extreme volatility in cryptocurrency values in a wild west environment, and Anti-Money Laundering and Countering Financing of Terrorism Act requirements with cryptos receiving plenty of bad publicity.

NZ banks do need to keep their eye on the ball as we live in a fast moving world.The salutary lesson of Nokia is worth remembering. Things can change fast. Nokia was once the world's biggest and most successful mobile phone maker. But the Finnish company missed the smartphone boat and its cellphone business was sold to Microsoft.

In the foreseeable future no one appears set to eat NZ banks' lunch, but the banks may have to share more of it. Anything's possible in the long-term. But given the dominance of property in our financial system, and banks near total dominance of property lending, making decent inroads into bank lunches will require some major muscling in on the housing market.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

19 Comments

'Reports of the demise of banks have been greatly exaggerated'

Correct... as reserve bank will do anything and everything to support banks as their very own survival depends on survival of banks.

Not unless they take over all bank functions and we are forced to use a digital currency. Who needs a retail footprint then?

No competition for lending or saving, instant tax collection. A monopoly. 'Tis the Socialist way.

I am allergic to socialism but we can ether ship our income across to Australia or keep it here to be wasted. A Hobsons choice if ever there was.

JAO Burni's comment is wrong - it is not socialism, but it is authoritarian Government.

I am a little concerned though with the connotations about how the word 'socialism' is used. Socialism in it's lightest form is ensuring everyone benefits in a successful society, and really should be the goal of all governments IMHO. Socialism moving further starts to become 'anti-wealth' and is destructive, and many people are showing signs of this. Capitalism though is pro-wealth, but what most people ignore, is that in a world of constrained resources, that 'wealth' becomes the property of just a very few, and at the expense of the many. Capitalism invariably creates what we appear to have now, wealthy elitism, reduced opportunity for most, higher taxes on middle income groups, subsistence wages, increased dependency - and guess what? It's starting to look like today's socialism!

Certainly we need to aspire to change our current situation - the gap between rich and poor is extreme at the moment. Unfortunately we need to ether go back to the destructive revolutionary approaches of previous social failures or look for new innovative ways forward.

At the core of the problem are hierarchies of competence (yes that is a Peterson phrase but its backed by actual science) it is difficult to imagine how we can effectively resolve breaking those without society breaking. We are in the beginning phases of an experiment in this area as we move diversity etc into the main hierarchy driver rather than competence so we will see over then next 10-20 years the fruit of that. It does not seem to be making much difference at the moment but it is still early days, our board diversity etc is still not approaching the desired weightings (which will not relate to the population at large necessarily)

The problem is defining "competence". You don't have to look far to find people who think they are more competent than others because they are richer, or the boss, and at the extremes because they're white and the other is not, or they are christian and the other is not and so on. "Competence" becomes a shelter for a form of tribalism. A true meritocracy doesn't measure a person on the colour of their skin, their religion or their gender or anything else. It measures on their "competence", but even today we can see people who are promoted not because of their "competence", but for other factors like minority, personality, politics. I have known of people who were extremely competent, and bluntly told their bosses what they needed to know, but who ultimately lost their job because they were too blunt and direct, especially on sensitive matters, and worse - too often right!

But hierarchies of competence is getting talented people to the top, other means are required to ensure average people get opportunities too. If only because sometimes talent doesn't find it's way out until it is exposed in specific situations. But the vast majority of people just need decent jobs, at decent pay rates, and the opportunity to live a good life, something that is pretty much denied to most these days.

Yes agreed, people need to find a reason to be, to contribute, for society to be healthy. There are some societies in the nordics which are more equal in their distribution of opportunity but they do appear to take some heavy governance to achieve.

When I lived in the UK I paid 57% tax on the majority of my income but I could see where the money went. I don't object to high levels of taxation but I do want to see some competence in the stewardship of that money. At the moment our government bureaucracy seems very poor we can't spend the existing budgets let alone larger ones.

Unfortunately Government's have ceded too much power to the banks. This is a fundamental betrayal of their constituency, but politicians are only attracted to the sycophantic adoration of their constituents once every three years, the rest of the time they are like moths to the flame, only the flame is big money. Banks and big business are in reality a significant threat to democracy, but we the people are essentially powerless to do anything about this.

Banking is a walled garden with regulation and licensing acting as barriers to entry for newcomers and protecting margins for the very few banks registered within it. Once you have that golden ticket you are made forever as long as you don't do anything incredibly stupid.

After all Westpac, a company that routinely fails to comply with even the most basic regulation or provide any semblance of customer service, has survived in this garden for over 150 years.

The role of commercial banks in the global economy is changing, with lending to governments and their agencies now more important than lending to goods and services industries. It is a trend which is due to continue.

The new Basel 3 regulations seem set to encourage this trend, despite retail depositors being accorded a stable funding status. Central bank digital currencies are anticipated to augment and perhaps replace non-financial business credit over the next five to ten years.

But the increasing financialisation of commercial banking brings the risk of tying its future firmly to a financial bubble. And with price inflation on the increase, it is only a matter of very little time before that bubble bursts.

Using our balance sheet to support monetary and financial stability

Via the RBNZ payments system banks have a combination of direct and contingent claims on government totalling ~ $69.282bn

Nice, the housing is nearly 3 times business Debt & 6 times agriculture debt . It means we don't have thriving business opportunities in NZ other than property investment. That's why where ever I go I find real estate agents cars with there smiling faces on it and there hoardings.

Hope this can continue for forever and our housing market should thrive for coming decades & our banks revenue grow multiple folds.

Why are bankers afraid of Bitcoin’s impact? Easy, it will lead to ripples across the financial sector, it will create new winners and losers, and it will likely decentralize banking services and create micro markets to an extent not seen since the advances of the barter economy and the market economy combined. In fact, this is what the Internet of Value is all about—erasing the distinction between bartering, money and service exchange in any market. Once each potential good has a financially tradable and storable equivalent, “a bitcoin,” if you will, trade will explode in a myriad of directions impossible to predict by current algorithms. Intermediaries will come and go, and the end points of exchange nodes will become more important. To many bankers, this is a scary thought. To everyone else it is likely quite liberating.

Clearly, there must be regulation. Without regulation, markets are unstable. However, countries that over-regulate a disruptive innovation in its infancy will only lose out on the first waves of that innovation. Several countries seem to be heading that way, and the US is now in the front seat of that wagon. What a pity. The urge to cripple crypto based currencies is futile.

https://fortune.com/2014/11/20/why-banks-fear-bitcoin/

People have in past posts explained that these billions of income are a fair return on capital. Given the continuous closing of branches what capital are we talking about? The funding for lending (the seed money then further leveraged to infinity) come from the markets (our super schemes and those of other countries) so what actual capital have the shareholders of the banks actually put in?

Remember Kodak who refused to believe that digital would replace traditional film…..Look how that worked out. This piece has been written by someone who has just quickly glanced at the blockchain developments and all but dismissed them. There are massive changes going on in this space that will be massive disrupters to banks, financial services businesses and real estate to name but few.

Lets look at a real life example using Square Capital as an example. Time to approve loan with square 7 minutes v 60 to 90 days with a traditional bank. This is happening now. Just because you can’t see it in NZ doesn’t mean it isn’t happening. It’s happening big time and our banks will simply be playing a game of catch up but will still be miles behind the leaders. Take a look at this presentation from Ark Invest’s Cathy Wood. https://youtu.be/eE6u67Ph768

The nexus between the Central Banks and the Main street Banks will keep them going for eons to come. Both buttress each other in their survival tricks. This was brought to life very evidently by Hank Paulson bailing out the Banks during the GFC, giving sweet heart deals to Goldman Sucks, Morgan Stealy, JP Morgan Chase etc. The Banks will be the last ones standing always.

I wrote in my Blog this in September 2008.

Quote :

Consider this. Paulson as chief of Goldman Sachs pushed Congress to liberalise rules for Investment Banks so they can take on higher leverage to speculate and make more money betting on worthless loans and paper securities. His firm sold these to other Banks, etc. Then he becomes Treasury Secretay and sees the mess explode the financial markets. He allows Bear Stearns and Merryl Lynch to be taken over by bigger banks, lets Leehman collapse thus killing the opposition and that leaves Goldman Sachs and Morgan Stanley standing. They turn themselves into Banks. Meanwhile Paulson drums up the Bailout Plan of $700 billion to buy the toxic mortgages and another $250 billion to recapitalise Banks. Guess who benefits, his old firm Goldman Sachs. The Bailout is going to be administered by his ex-aide at Sachs, Neel Kashkari who is now the Bailout Czar. Shows how one of the Villains of the Crisis has morphed into the Hero of the Bailout. God save USA. To paraphrase a Chinese curse 'we are living in interesting times'

Unquote:

Repeated comment.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.