Time can be a very deceptive beast.

In looking back through the interest.co.nz archives to find information on the Reserve Bank's, I would say, embattled efforts to get itself a debt-to-income (DTI) tool to aim against the housing market, I discovered, somewhat to my horror, that I've spent about six years of my life following this increasingly tortuous quest.

The RBNZ's battle for a DTI measure to slip into its 'macro-prudential toolkit' has simply been running for even longer than I thought.

In fact, clearly our central bank was starting to have regrets and beginning to think DTIs were a good idea not so very long after it had signed off on the creation of the macro-prudential toolkit with then Finance Minister Bill English in 2013. Why on earth the RBNZ did not seek to have a DTI measure at the time the original macro-pru kit was being put together remains one of the great mysteries. The RBNZ could have saved itself a lot of time and anguish if it had simply sought the inclusion of DTIs then - because it most definitely would have got Ministerial sign-off for them.

By 2015 it was clear the RBNZ was regretting the omission, as it was starting to compile a lot of info on debt-to-income ratios, whilst at that stage not admitting to coveting them. But then in May 2016 after releasing one of the most unremarkable Financial Stability Reports ever, there was a most remarkable media conference at which, first the then Deputy Governor Grant Spencer revealed the RBNZ's enthusiasm for DTIs, and then this was confirmed and further commented on by then Governor Graeme Wheeler. This apparently unscripted reveal was very untypical of the RBNZ, certainly in pre-Adrian Orr-days.

But then again, It was not obvious at that stage just how political the whole issue was becoming around the housing market and RBNZ efforts to control lending. Loan to value ratio (LVR) limits had been included in the original macro-pru kit and of course they had been in use since 2013. And with the initial iteration of those LVR measures having clearly disadvantaged the first home buyers, it seems politicians across the house had become very leery of these macro-pru measures. For some reason politicians appear to develop an aversion to anything that might be toxic for them in the ballot box.

So, the short version of what happened subsequently is that in 2017 then Finance Minister Steven Joyce neatly pushed back at the RBNZ's efforts by getting it to undertake public consultation - which delayed/got us through to the 2017 election, after which the whole issue then got swept up in the incoming Labour-led Government's moves to review and overhaul the RBNZ.

And now it's getting towards the end of 2021 and the RBNZ will get its DTIs but issues remain, not least the vexed (from a political perspective) question of what treatment the FHBs get.

All of which helps to complicate a complicated picture.

While people might think they know what they will get with imposition of a DTI measure, the reality is it has never been spelt out exactly what might be applied. And given all that's happened, I don't think we can make any sweeping generalisations about what we will get, or when.

I guess the general assumption has been that a DTI limit when applied here would be some kind of limit that relates to the number of times the size of mortgage exceeds the annual household income. So, in very basic terms a DTI limit of five would mean someone on an annual household income of $100,000 could borrow up to $500,000.

But in its desire to get get Finance Minister Grant Robertson to sign off on the DTI measure, the RBNZ came fairly close to promising it wouldn't set a limit of under six and maybe even seven.

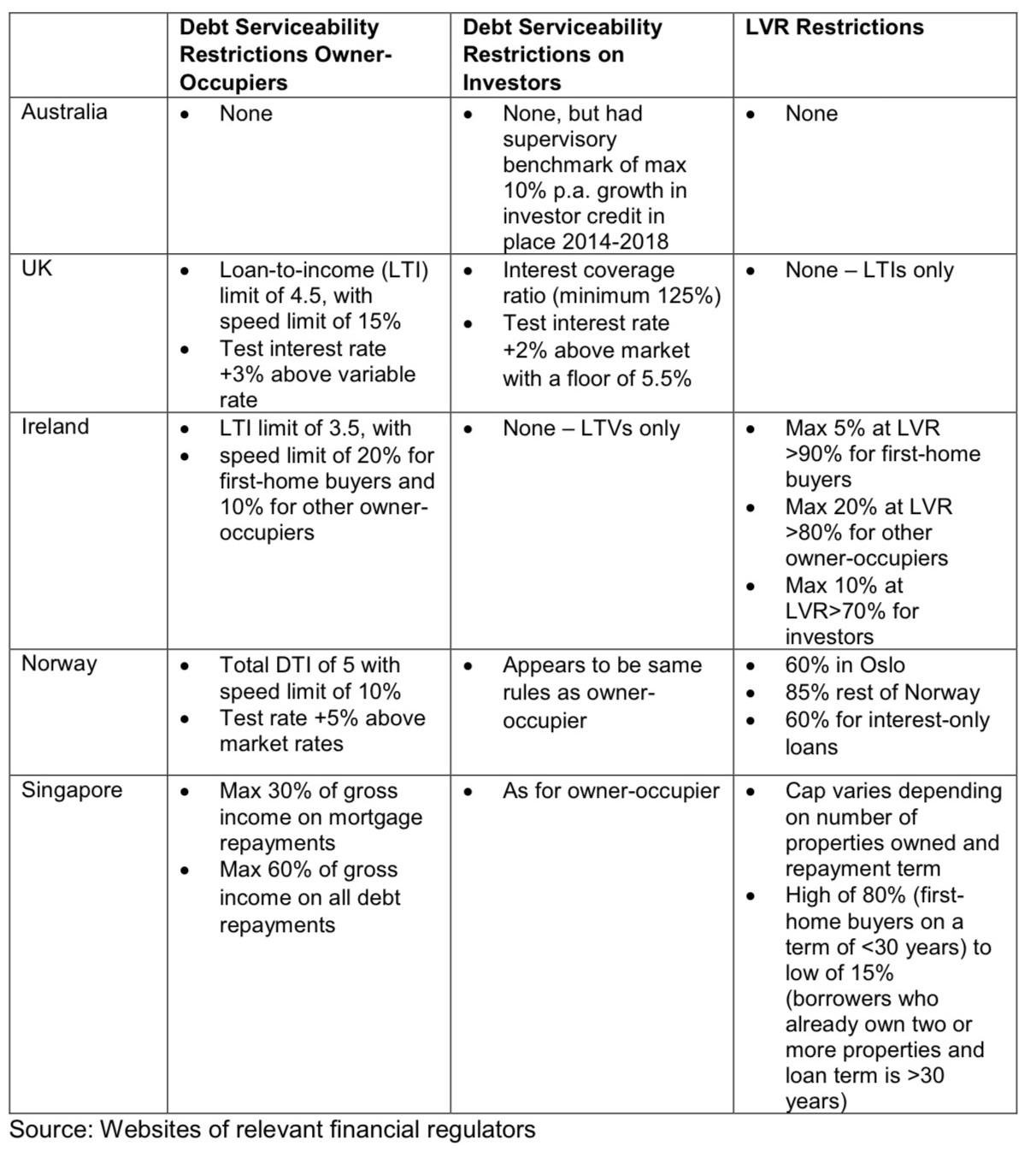

It's worth at this point dropping in (chart is from the RBNZ) details of what some countries that have DTI measures actually apply. A DTI limit of six or seven would certainly put us well above what some other places are doing:

The Singapore one looks interesting.

And it's worth refreshing recent memories of what the RBNZ is considering - because clearly the straight out DTI limit as we've imagined might not be what we end up with.

This is three potential options as canvassed in the rejigged Memorandum of Understanding between Finance Minister Grant Robertson and RBNZ Governor Adrian Orr:

- Debt-to-income ratio restrictions – cap on mortgage debt (or total debt of a borrower including mortgage debt) as a multiple of income;

- Debt-servicing-to-income ratio restrictions – cap on the percentage of a borrower’s income that can be allocated to servicing debt payments;

- Interest rate floors – floor on test interest rates used by banks in their serviceability assessments.

So, option one is the DTI limit as we've imagined it.

Option two is more the Singapore style - and I do wonder whether we might be better to go down this path. Somehow I reckon an absolute limit in this way might be less ambiguous.

The other thing is - if the RBNZ really would be forced for the sake of FHBs/Finance Minister to make an overall DTI limit as high as say seven, then this could be pretty meaningless. Applying a more specific case by case, more direct style of limit could work better. And it might focus the minds of folk on such limits a bit better.

I hope this second option is carefully considered. Yes, I do see potential problems with it (what happens if your mortgage payments go up to the point you suddenly exceed your income ceiling) - but arguably that also makes it a more responsive way of operating a debt-to-income control than simply saying at the outset you can borrow seven times what you earn. It would better capture the ups and downs of interest rates. It just looks more hands on and much clearer. It would also possibly allow for some differentiation, if wanted between buyer groups, IE say an FHB could have an income-to-mortgage limit a few percentage points higher.

All this of course is going to take time. The RBNZ is not planning to begin consultation till October.

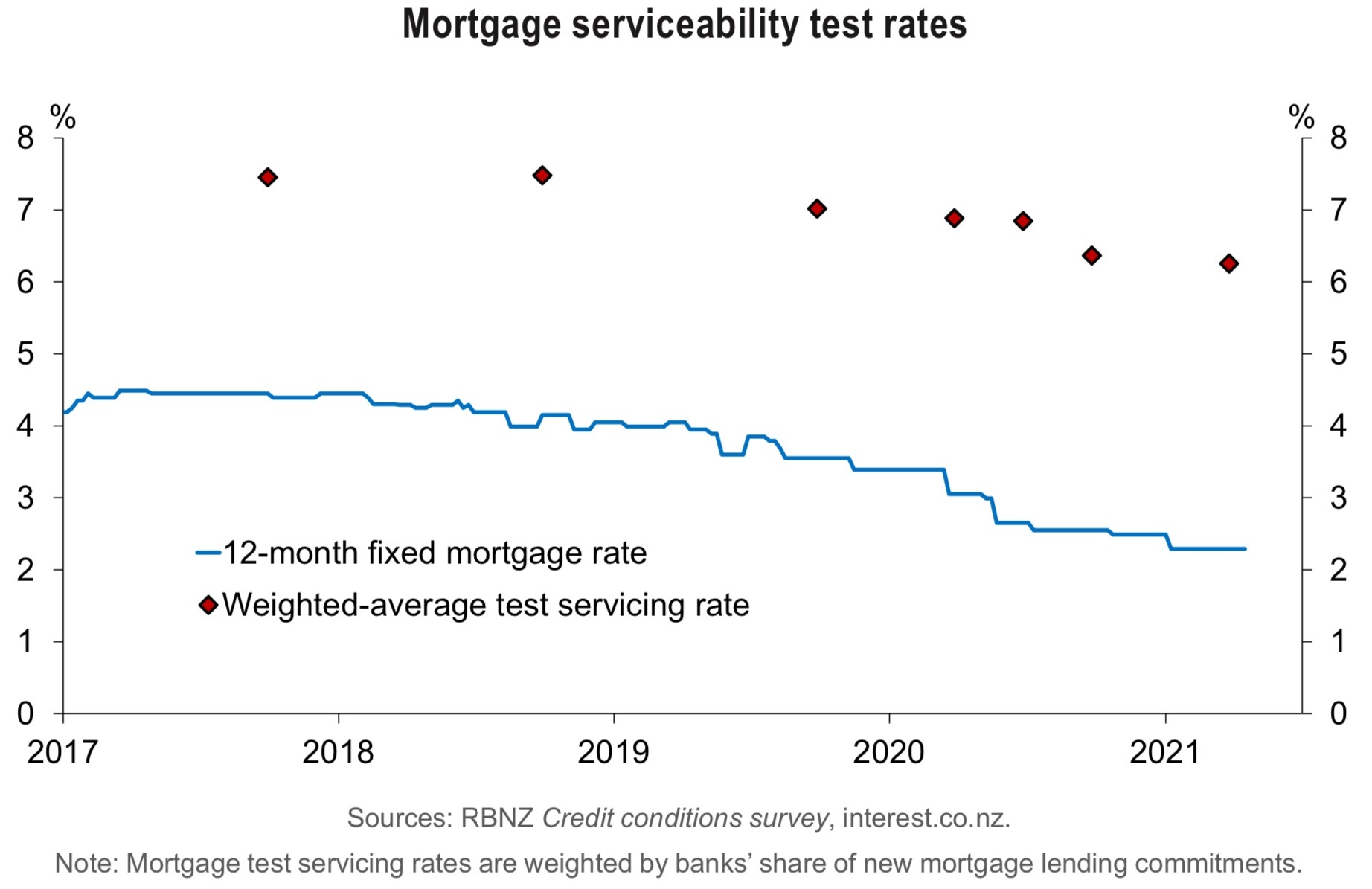

Before we get a DTI 'proper' we'll very likely end up with the third option on that list above, the 'interest rate floors'. These are something the banks themselves have stated a preference for and could be implemented at short notice. Basically it would involve the RBNZ applying a standard 'test' interest rate for the banks with new mortgage applications.

The banks of course all apply their own test interest rates (set above prevailing rates) to check that would-be borrowers have the flexibility to meet changed payment requirements. As real interest rates have fallen, then so the rates applied by banks in their tests have fallen too. As can be seen in this graph from the RBNZ's May 2021 Financial Stability Report:

It is to be imagined that a standardised interest rate floor would work quite well as an interim measure. Indeed, I can well imagine the banks might yet be pushing for this measure to be implemented instead of a DTI measure.

Actually I don't see why you couldn't have both.

But there's clearly a lot to be resolved here. Not least of the issues also is how any DTI regime would fit in with the LVR limits. Would it replace them, or could they be complementary?

Given what's happened in the housing market, and the number of measures that have already been thrown at it, from the Government's March tax moves to the new RBNZ tighter LVR rules, there's arguably now no point in trying to urgently put these DTI measures in place.

Better to get them right. And having waited so long, too long, for them, there's probably no point rushing them now.

It is going to be very interesting to see how it all evolves though.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

107 Comments

Every armour has a chink; we just need to see the armour first.

Specially if Mr Orr is in charge.

He will do everything under his power to delay and dilute when forced under pressure to act and now we are in that situation - not that he wants to act but is forced as housing ponzi touching new height by his blessing so WAIT AND WATCH as is his policy how he plays dirty, once again with FHB in support of his colleagues and friends - investors.

As a residential investor any RBNZ measure that keeps potential FTBs in rentals and out of the market is music to my ears.

Again, I'd like to thank Governor Orr and Prime Minister Ardern for their steadfast commitment to supporting property investment as a leading New Zealand industry. I'm very much looking forwards to border normalisation to offer the next wave of demand.

The impact on FHBs may be smaller than you are imagining. Most recent data from March 2021 shows that only ~23% of mortgages to FHBs exceeded a DTI of 6, so likely ~10% would be affected by a DTI of 7 as seems likely.

Investors who have to spread their salary (if any) over a whole portfolio will be much more constrained by this.

https://www.rbnz.govt.nz/statistics/c40-residential-mortgage-lending-by…

Yeah I agree.

Many of the FHBs I know have taken on mortgages of circa 500-600k, and have household incomes typically of 100-150k.

In Auckland what does find in $750000 (deposit of $150000 and mortage of $600000) - most in that earning bracket are managing $200000 plus and mortage of $800000 to $900000 plus ( how they do - check with finance broker for ideas like paying guests.......or........).

Average unit in Auckland is now $800000 to 1.3 million and house from 1.1 million to 1.6 million plus and town houses from million to 1. Million plus.

RFEALITY CHECK

You can still buy new 2 bedroom apartments and townhouses in Auvkland for circa 700k

So they have to have another 400/500k from somewhere else then. These types of FHBs are rare.

The average FHB loan is for around 500k at the moment, so either a large portion have access to that kind of money or they are aiming for cheaper houses than you think. I suspect the latter.

True and they will be the only ones buying once DTIs come in. Anyone without wealthy parents who can afford a small gift of half a million dollars will be locked out of the market forever

Not just salary, also their rental income. What's the best option to increase income for an investor with four properties who needs to increase income 10k to make a deal work?

Less avocado on toast and coffee.

Unfortunately DTI ignores silly things like living expenses (including brunches). So a couple earning 200k with 6 kids paying $4000/month in childcare and another $1000/month on smashed avo can borrow the same as an individual earning 200k under a strict DTI.

No. The DTI is just another layer on top of all the other measures including higher test rates, monthly surlus figures etc etc. It just means if you do get a pass on a lending roposal the DTI at say 6.1 can scuper the loan

Yep it's a blunt measure which is far less sophisticated than the measures the banks have been using for decades to stop themselves from losing money when they literally give it away. Banks lending money on a 30 year term have a far greater interest in getting it back than regulators or politicians do in stopping them from lending it out for political reasons, which is why they have many, many more checks. DTIs are a very blunt measure which ignore silly things like how much repayments are at different interest rates and anyone who thinks DTIs are a useful measure of anything at all is likely pretty blunt themselves and should probably be considering either retirement or a new career path.

Have the company that holds the rental properties borrow some working capital and pay it to him/her/it self as a salary for a few months to make his income look higher?

From Wolf with a special mention of NZ

This Reddit Lament Sums up Wonderfully What Lots of Home Buyers Will Grapple with as Housing Market “Normalizes” and Work from Home Fizzles

by Wolf Richter • Aug 10, 2021 • 17 Comments

The price of FOMO.

By Wolf Richter for WOLF STREET.

Here is a Reddit lament by a self-admitted FOMO-home-buyer in Canada. The couple, mistakenly thinking that working-at-home (WAH) was permanent, had bought for that reason a house “hours away” from Toronto six months ago. But turns out, WAH was transitory for them, and now they need to sell the house.

But in the two weeks that the home has been on the market, they didn’t get offers that would allow them to make a profit or break even, as the market is cooling – a horrifyingly bloodcurdling stupendously surprising situation of having to sell a house without being able to make an instant profit.

And they can’t even rent out the house profitably in their estimates. What kind of horror show is this??

This is the horror show of having bought a house in what has been identified as the #2 Housing Bubble in the world, behind New Zealand, and now this housing bubble is “normalizing,” or “cooling,” or whatever, and suddenly the plans go kaput.

I see that moron Church is saying today that housing isn't a human rights crisis...

A moronic, right wing shock jock.

He's reached his point of hysteria

And idiocy

Let’s be clear here, the ability to be housed is the HR issue, not the price of houses. Human Rights are universal and if owning a house was a right then there would be UN missions to build houses in every country. It’s the fact there aren’t enough houses for the Government to provide that is the HR issue.

Like you, I also believe that anyone who doesnt agree with me is a moron!

I think any push back from Banks about certain measures over others because of operational reasons is very questionable. A DTI limit for each borrower can be calculated very easily with a pocket calculator, I just don't buy it.

The interesting wrinkle for me is how is rental income considered on the 'I' side? If it's disallowed or relevant expenses counted against it (rates, insurance, ~1-2% of property price for maintenance, allowance for vacancy etc), then this will really hamstring debt driven investors.

Thank you for further restricting FHB's from buying their first property and making it harder for them to purchase a home! I'm sure the investors are loving this news since majority of them have made so much money over the last decade from flipping their properties that they have money up the whazoo~!

#rentforlife #thankyoulabour

As above - a DTI of 7 would likely only remove the top 10% of FHB loans in recent months. Investors relying on debt to buy new properties (i.e. the vast majority of them) will be heavily restricted.

Remember, most investors actively growing their portfolios are absolutely not flush with cash as they roll equity from previous properties into new ones. Often properties are not hugely cashflow positive, if at all.

What they have is a large collection of assets with a corresponding large pile of debt. Until the debt pile is worked down, a DTI will stop them in their tracks.

The LVR rules at 40% on a 2 million dollar property mean $1,200,000 of debt against 200,000 of (10%) income from the investment itself (meeting the 6x DTI before adding in the investor’s salary). Ie. The LVR rules as they stand now are effectively the same as a DTI of 6.

Also the majority of prudent investors will have a mix of real estate and shares in their portfolio, income from shares will drive up the max DTI that they can afford.

Where on earth are you finding 10% yields? I think 5% is more realistic these days. You're also assuming that gross income rather than net income will be counted for the DTI which seems inappropriate to me, but I guess we have to wait for the rules.

I agree most prudent investors would have a diverse portfolio, but the mistake you are making is assuming most other property investors are prudent. I wouldn't be surprised if the majority of property investors in NZ have no other significant assets - many are downright scared of shares.

$2k a week rent on a $2m house in Auckland? Even that's a big call.

Not a chance. A $2m house in the inner suburbs rents for max $1000 p/w. The purchase prices are driven by developers looking to demo and build multiple units, or upmarket owner-occupiers; if they're tenanted, it's just to defray some expenses until the demolition or resale.

And once the developer demolishes the old units and builds a block of new units on the site then sells the block all at once to reduce holding costs and avoid agents commissions, what kind of yield do you expect that the new owners of these high density units will be making?

Would that change if someone offered to buy all the units off the plans early on and partially fund the development so that he has guaranteed sales, lower holding costs and can take that to the bank for funding on better terms?

Sounds like you're a property developer, and would know better than me; but it seems likely to me that the developers selling new units at say $950k each will do better than any investors buying them at that price, unless we see big rent increases. Seems like yield must be zero for anyone buying new builds to rent out, at current prices; but of course, they're thinking more about the capital gains. No doubt the yields are a lot better if you bought a few years ago, or at a certain level of density.

Yes, there is bound to be resistance at any rent asked above $750. Very few takers for them. Only Corporate executives may be.

With stand alone dwellings as the value increases the yield decreases due to a lack of demand for rentals at that level. However with high density multi unit dwellings yields are generally lower for cheaper units due to competition from more investors who can afford them. Multi dwelling units in the 2-5 million range will usually have returns of about 10% in my experience. I recently acquired a block of units that was returning 8% due to it being leased to Kaianga Ora, once that contract expires we expect the yield to climb to 11% partially due to the removal of all the Kaianga Ora units from the area causing a certain amount of gentrification.

Sounds like you are operating in a different area to most investors - your experiences likely don't relate well to the typical investor competing directly with FHBs.

How do you arrive at income of 200k?

Several of the $2 million properties I know of in Auckland return about 50- 60k per annum

The higher the density the higher the yield usually, yields are generally lower for cheaper units due to competition. Multi dwelling units in the 2-5 million range will usually have returns of about 10% in my experience. I recently acquired a block of units that was returning 8% due to it being leased to Kaianga Ora, once that contract expires we expect the yield to climb to 11% partially due to the removal of all the Kaianga Ora units from the area causing a certain amount of gentrification.

This kind of thing is very rare, you are doing well if you have that.

If we are talking about single apartments or townhouses (rather than a whole block), you will do very well to get above 5% yield.

I am too terrified of body corporates to own anything with shared walls unless I own enough to control the body corporate outright.

Just wondering now, that interest is no longer a deductible expense, that could increase their income at least on paper.

Never thought Labour would bring me wealth. Thanks incompetent Labour for giving us investors so much love.

It was always a case of vote labour for more money for me now and National / Act for the long term good of the country.

The lack of stability / proclivity of leftist governments to spring surprise policies on us is fertile ground for market volatility. Investors win regardless if the markets are moving up or down, a flat market is what we fear the most.

The GFC saw the rise of many a fortune whilst the ordinary people bore the brunt of losses. There is no reason to believe any new crash will be different.

National / Act for the long term good of the country

With their promise of flooding the country with foreign property speculation money and low-skilled migrants? Or their 'do nothing and let our oligopolies solve our socioeconomic problems' attitude towards policymaking?

To be fair, Labour and National both have used mass migration and housing speculation to inflate our economy; the only difference being Labour wants us to believe that they'll eventually get us onto a real economy while National wants to double-down on the ponzi.

Both political factions are party to the destruction of living standards and wealth of the NZ working-class in the long run.

I can see so much hate for labour every where (on this site and in general reaction of people I meet) because of policies & decisions which are taken by our PM.

Hold on guys the term is not ended, we have more surprises to see in coming 2 years. Definitely this govt will try hard to push the market up by not taking any action, as there is still some space and as usual RBNZ will play there favorite game of wait and watch.

You must have no borrowing over your rentals. Labour nailed investors with no interest deductibility.

Too late to rein in speculation money now. Unfortunately, shutting speculators out of the market completely at this stage will just pull liquidity away from an overinflated housing market.

This could devastate the residential construction sector and plunge NZ into another financial crisis.

It's a valid point...

Unintended consquences

If there's a property crash, all those newly unemployed builders can stop doing unnecessary renovations and get to work on the massive state housing programme we need. When capacity comes free, Kainga Ora can step up.

Fair point. Hopefully we can get our numbers up to OECD frontrunners in social housing (Sweden's social housing makes up 20 percent of all housing stock - nearly half the rental sector in volume).

Can’t wait.

Consultations don't start until October? That simply guarantees additional capital gains over the summer months.

If you are looking to sell, sell this summer because DTIs will increase the level of FOMO.

I support the DTI's but you are certainly right that this may incentivise an uplift in demand to 'beat' the introduction of DTIs...

Also a valid question is what happens if you are currently borrowing over the specified dti amount. Does this mean you cannot ever switch banks as this will be new borrowing. The banks may take advantage of these newly vulnerable.

"YES - we are finally getting DTIs - but what exactly will we get and when?"

David, you have hit the nail...will it be in right earnest or cosmetic and bigger question is WHEN. We need it now and should not be that hungry now and Mr Orr cones out that will be planning the menu soon, than will procure the stuff and finally cook and serve you next year. So please hold your hunger - till now this has been his approach, play with time to delay or dilute.

"The RBNZ's battle for a DTI measure to slip into its 'macro-prudential toolkit' has simply been running for even longer than I thought. "

If RBNZ has been after DTI since ages, am sure they have the blue print ready, if asking from government specially now, when they knew the way the ponzi was going ( doubling house price in a year or two) than must have alrwady done their homework and is now talk...actually more than talk is informing the banks/lender to impliment just like LVR.

"How will they protect FHB'

Simple just like LVR, Can have two benchmark, one for investor and another for FHB ( Though personally even one benchmark is fine or alternatively not include rent income when calculating DTI)

David DTI is must to protect FHB as are witnessing that FHB who are able to enter are buying over normal and any change in situation may be disaster but FOMO overtakes rational thinking ( FOR FOMO MR ORR AND ROBERTSON ARE PERSONALLY RESPONSIBLE).

If under DTI FHB are not able to stretch beyond and buy will be initially disappointed but better than buying and than repenting when repayment bites besides may be after sometime the fire ignited by Orr calms down than may be will be able to buy within DTI, the way it should be.

DTI is more to protect FHB from making irrational purchase under FOMO and any reduction in demand is bound to help FHB in long run.

For investor will know if Orr has intent as exception circumstances require exceptional measures - raise LVR got 60% and let the market run its own course.

Besides IF RBNZ TAKES ACTION IN RIGHT EARNEST NOW (NOT COSMETIC) WILL BE ABLE TO REEDEM SOME RESPECT THAT HAS BEEN LOST BY MR ORR APPROACH OF WAIT AND WATCH

How is irrational defined.. if the housing market is always going up, any price for a FHB may be rational. The issue is that for decades housing speculation has been tax free. This created an ever increasing market because at the same time borrowed money was free. This was a corruption of sorts.. people making legislation benefitting from the very legislation they implement. Now IF it changes previous generations walk away with the spoils and the FHB is bankrupted.. Wealth must be taxed to right the wrong ... either that or jail the policy makers who created this.

Speaking as a potential first home buyer who is cautious with his money, I am locked out of the market. Its only getting worse. Let me tell you first hand, theres nothing they can implement now to the housing market that could possibly punish me at all. I'm not even in the game. So bring on the harsh DTI's.

So what's the plan? Moving overseas?

Why can’t they DTI the investor and not the FHB that would help a fair bit I would have thought.

It needs to be a "operational objective" of the RBNZ to target investors. At the moment it is merely a Government policy so RBNZ decisions still focus mainly on financial stability rather than helping FHBs to buy a house.

See https://legislation.govt.nz/regulation/public/2021/0029/latest/LMS45502…

Me too. It's just been entertainment for years.

Still hoping to see a negative ocr to top it off.

This is what Jacinda Arts in has done - taken away the aspiration and dream of many.

This issue has been apparent for more than a decade. Show me on the doll where Jacinda hurt you.

DTIs will not solve NZ’s housing affordability crisis. It will just add further administrative expense & complexity. Who benefits? Renters are affected more than FHB because they have less money so why isn’t there more focus on them?

Printing of money & extremely low interest rates has caused NZ’s housing affordability crisis. Interest rates need to be raised so that housing prices & rents become more affordable.

This government has ignored renters & focussed on FHB. This has created the unfortunate situation of an ever increasing need for emergency housing & all the social problems that go with that.

Agree their idiotic obsession with the FHB has cost them an absolute fortune and created no end of a crisis for them for the renter population.

Another day, another smoke screen, another red herring to add to the list of "this will fix the housing market"

What have we had so far -

- Removal of depreciation

- Introduction of the Brightline test set at 2 years

- Introduction of LVR's

- Foreign buyer ban

- Anti money laundering tighten up

- Extension of the Brightline test to 5 years

- Healthy homes legislation - THAT DOES NOT APPLY TO OWNER OCCUPIED HOUSES

- Rent rises restricted to once per annum

- Introduction of tighter Tenancy legislation favoring tenants

- Removal of interest deductibility

- Extension of the Brightline test to 10 years

- DTI's ???

What have we ended up with ??

- All of the above have added to higher prices, higher rents and less houses for sale !

Naïve leaders that really have NO idea other than the next lightbulb moment.

My properties are now worth $4,000,000 more than when Labour came to power, I suppose I should say thanks but this market is not over yet !

Are you claiming the above actions caused your $4m gain?

Seems unlikely, better question is if none of the above were in place what would your gain be?

Indirectly those actions did contribute to his gain.

Many of them are misguided attempts to do ( or be seen to be doing .. ) SOMETHING about the house prices - while still keeping interest rates ridiculously low.

Good post. Astonishing just how many measures these Draconians have implemented on the market apart from the 2 year bright line which was National.

LVRs and the removal of the ability to claim depreciation were both introduced under National also.

The trouble was these measures were introduced separately after much discussion and debate. Imagine what might have happened if they were all imposed all at once, without any notice or debate ? Like the Demonetisation done by Modi in India to curb black money ? It brought down house prices a lot, removing dodgy money in housing.

Stopping interest only loan would actually work....hence No one even talk about it.

A DTI limit of 7 would not be meaningless. If the current average is 10, that would basically take out the marginal buyer and cause prices to converge to the 7 level over time. That is a significant price impact.

Its waaaaay too late. There will be nothing to ease the pain of the coming speculative implosion for NZ property nuts.

Yawn.

Bring

It

On

Otherwise it's a snooze first.

It is in some ways fascinating, certainly a mess, and I am always keen to see what interest.co readers see in their respective crystal balls. Preferably skipping the blame game and creative name calling.

I wonder - any property investor who sees this potential introduction of DTI as a boon for them, damaging only for FHB, what is their logic? Does it rest purely on the deeply held belief that property values will only go up, and up and up...?

Such that their approach is still (A) get loan approval from bank (B) find decent property without too many competing offers (C) purchase and wait for capital gain, (D) recalculate equity and repeat.

If DTI knocks out some potential offers, great, its a simpler game for them.

But others of us are predicting DTI or something will eventually grind capital gains down to a halt. Do property bulls just not believe that is possible?

Ireland , cash rate 0.0 percent, Norway 0.0 percent, Singapore 0.07 percent , Australia 0.1 percent. United Kingdom 0.1 percent . Central bank failure did not happen overnight( well almost ) and New Zealand is not unique.

DTI...Death To Investors ? Dream on, RBNZ.

I wonder what would happen if the DELTA strain comes into NZ. Does that mean we go backwards again and decrease the interest rates back?

Housing market boom 3.0? Perhaps another 2x from here on out?

If delta did take hold then yes, housing boom 3.0 for sure.

Negative interest rates straight away I suspect.

Maybe some people are hoping this will occur? The rich get richer and the poor get poorer and the wealth divide grows

Surely the way to fix all this interference in a commercial transaction around housing is to remove the RBNZ from it. do like the Americans, the house has a 30 years mortgage at their usual low rates and buyers buy the mortgage. 30 years at low rates removes the penchant to overstuffed governors of nothing from interfering in something which is actually none of the business.

The banks are not shoestring operations and if allowed to fail I suggest they would get their act together. Instead we the taxpayer guarantee them.

Despite making the biggest profits they have ever made with our low-interest rates some are calling for higher rates. Like so many things Kiwi politicians and banks have to interfere in our lives without us needing them too.

Garbage policy, socially regressive and will lead to more inequality. Only impacts on those on low incomes and people without significant assets. The sharks with massive portfolios bought in the 90s and early 2000s will be circling while nurses and tradies looking for an outlet to save for retirement will be fed to them as prey by Orr and Robertson.

Haha

Well when delta gets into nz, which maybe in a week.. We will be in lockdown 4 for possibly a month. Then the DTI will be thrown out the window along with any potential rate increases.

Yet they aren't making scanning compulsory. Less people scanning than ever, so if a case can't be traced, a lockdown could occur. Crazy.

Any new lockdown will cause a revolt (not in a spectacular fashion, just in that keep quiet and dont cooperate character we have). Nz had the opportunity to capitalize and vaccinate everyone quickly and blew it.

David. I think you have not thought out how affective DTI's would be. A DTI of 7 would stop most property investors from buying any more properties, and stop anyone wanting to buy a second property in auckland. Affectively crashing the market, as you still have sellers, but then you have no buyers. Take a Mum and Dad property investor family with salary job of 170k combines, rental income 30k, who has one home and a rental. They can now borrow 1.4m. Well say their first house cost them 900k and their rental cost them 500k. At best. No more rentals. Any family who wants to buy a rental property, will simply not be allowed to, under a DTI of 7. Fine, doesnt worry me, I already have 15 houses. But if Labour and RBNZ want to go further down this socialst communist path of making everyone pay day serfs with one house, then that will be the cost. Mum and Dad investors will not be able to keep their 1 or 2 rentals, and only the rich who have no or little debt, will take over all the property in NZ, along with the chinese residents who funnell money from china contacts and dont need banks. So I dont think you really have a clue do you, just like Labour. Be careful what you wish for. The law of unintended consequences. post note: I dont care BTW if prices crash, I am an investor keeping my houses for ever, prices dont matter. It just means I can buy more at cheaper prices. Its rents that counts, and labour seems to be pulling out all the stops to increase rents in this country which is great news.

'making everyone pay serfs with one house'

You, with 15 houses, think that only being allowed to own one property is some kind of hardship?

I own none, but I wouldn't swap places with you; not knowing what I do, which is that the likes of you are regarded with absolute contempt by everyone under 40, and rightly so.

Congratulations on getting rich, though.

Work harder, get a second job like I did to get my first, buy a little shitter in the arese end of Massey like I did, and renovate it while you are doing 2 jobs. Instead of moaning on here, do a bit of work to get that first house and dont waste your time posting on here. I got my first house when I was 31 with no help from anyone.

Exactly, and to what end are you going to hold those properties forever, are you trying to create a dynasty of property overlords? You obviously have no interest in investing in the productive economy, can you not see the damage your behavior has on society?

To pass on to my children. I am not stopping you working hard to get a house. If you had a second job to save for a deposit you wouldnt have time to waste on the internet. Property investors employ the services of many tradesman, and professionals, thats pretty productiive. My advice to you to anyone who doesnt have a house right now, is to work hard and save, buy something in Invercargill for around 250k, renovate it and make some money, and move into the next house. Dont start looking now for your dream house in a nice part of town.

Ha, as I thought, so after giving me the typical spiel about hard work you go to say the end goal is to pass them it on to your children so they not only don't have to work but live off the hard work of others, utterly farcical. And stop with the nonsense about employing tradesmen, houses (not the land) are depreciating assets if you don't spend money maintaining them ultimately they all go to zero.

Oh well good luck with whatever your plan is comrade Calaverite

Your children will be lost if they don't inherit 15 houses?

Just how useless are you raising them to be?

And here's the *important* bit: What worked for you does not work anymore. Because greed broke it. There are no 'starters in Massey' anymore. You bought them all.

Brisket there are starters everywhere, if you actually look around. I bought a house in Invercargill november last year for 300k. As a first home buyer, you can get 30k deposit together and buy something like that. Then you revalue it after 3 months, its now worth 350k, and you dont have to pay the low equity fee anymore. I hated Massey but I lived there for 2 years, why not try out Helensvile perhaps. There is always a property, cheap, somewhere, that can be fixed up and you can get ahead. But if you dont look, you wont find.

Obviously you don't read the news, how can you be so oblivious to the damage investors are causing?

From yesterday... "Income levels in these small communities are a lot lower than the national average income, but rent is rising a lot faster," "The rising levels of rent is really concerning not only across the country, but particularly for these small communities that have limited employment opportunities and lower wages." https://www.newshub.co.nz/home/money/2021/08/housing-crisis-investors-b…

Well actually thats Jacinda's fault rents are rising. All these extra costs she is putting on the property investors. Making interest non deductible will just increase rents more, unfortunately. The replacement cost on these small communities for new stock is a minimum 600k when you look at say services costing 100k, land 100k, and new house 400k. Marginal cost to create new stock 600k, so prices for existing stock will rise till they hit that. Councils and land restrictions, and Labour Governments actions will push both rents and house prices higher. I much prefer when National is in, as at least their is some semblance of control.

Kinda agree with some of what you say.

All the moaners on here all want to buy their first house in a top suburb and are not prepared to live in a rougher area to begin with.

I grew up in Epsom and never set foot in the area we are currently in before we bought. But it’s been ok and now the majority here are people like us buying and lifting the area. We will stay a few years then move onto a better area.

What on Earth makes you think that FHBs are turning down homes in 'rougher' suburbs?

There's no evidence for that -- on the contrary, prices in those suburbs have skyrocketed far beyond any measure of affordability.

Many potential FHB missed their chance as they simply will not compromise. Its also really pointless blaming others for your financial position because it will not change a thing. Typically anyone with multiple properties had to work their arse off to get where they are now and trust me, they have zero sympathy for you. I have only the one house and that was hard enough, I have no time for whiners.

"All the moaners on here all want to buy their first house in a top suburb and are not prepared to live in a rougher area to begin with."

And you know this how? Please present your proof.

Interesting to read the posts by PIs referring to "their" houses, multiples there off. The fine print actually makes them the banks houses untill all debt and bank documents are discharged. The PI's are merely a proxy for the risk while the ebb and flow of income and debt servicing takes place.

No that is not correct at all.

The certificate of title does not list the banks as having ownership in the property. A mortgage is to be serviced against the property that is all. Not the US model.

Anyone who doesnt have a house right now, only has themselves to blame, you cant blame property investors. Everyone plays in the same sandpit, and you play the hand you are given. Last time I checked, its a free country, although Jacinda would like to make us all communists. I spend the first 20 years of my working life pissing it all up against the wall, till I decided to make a change, think and do some hard work. If you did miss out on getting a house, I have a hot tip and this will get you into the market, dont say I didnt tell you. Buy shares in Audio Pixels (AKP) they will likely be worth 10 to 20 times what they are in the next 2 to 3 years. Put 20k into that now and you will have 200k to 400k to put into a house. DYOR.

You work hard for the first house.

Maybe the second.

The rest is equity at work. Or are you working 15 jobs to pay for your 15 houses?

Seriously, saying things like 'anyone who doesn't have a house right now only has themselves to blame' is so ridiculous that it comes across as a bad conscience desperately trying to justify itself.

Yep I worked my whole christmas once on some of my homes and through January. I however note the tenants were having a great old time spending their dole money on booze and drugs. Not a problem, they are doing what they enjoy, so fair enough. But I couldnt see one of them being planned and organised to buy a house, even if they really wanted one.

A few things, firstly what do you think would happen to house prices if investors were banned from owning multiple properties? Fall obviously, so I think people have every right to cast some of the blame for ridiculous prices at the feet of property investors. Secondly, society is so far removed from your implied definition of a "free country" it's not funny, we have rules and regulations everywhere many of which actually protect existing property owners to the detriment of others. And finally, if you're happy to give out investment advice why don't you take it, sell your rentals and go all in on AKP? At least AKP is attempting to create real value in the economy, unlike a rental property.

Some of those I built, thats what investors sometimes do. Are we allowed to keep any that we build. Or in your communist socialist world, do we have to give them over to the masses.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.