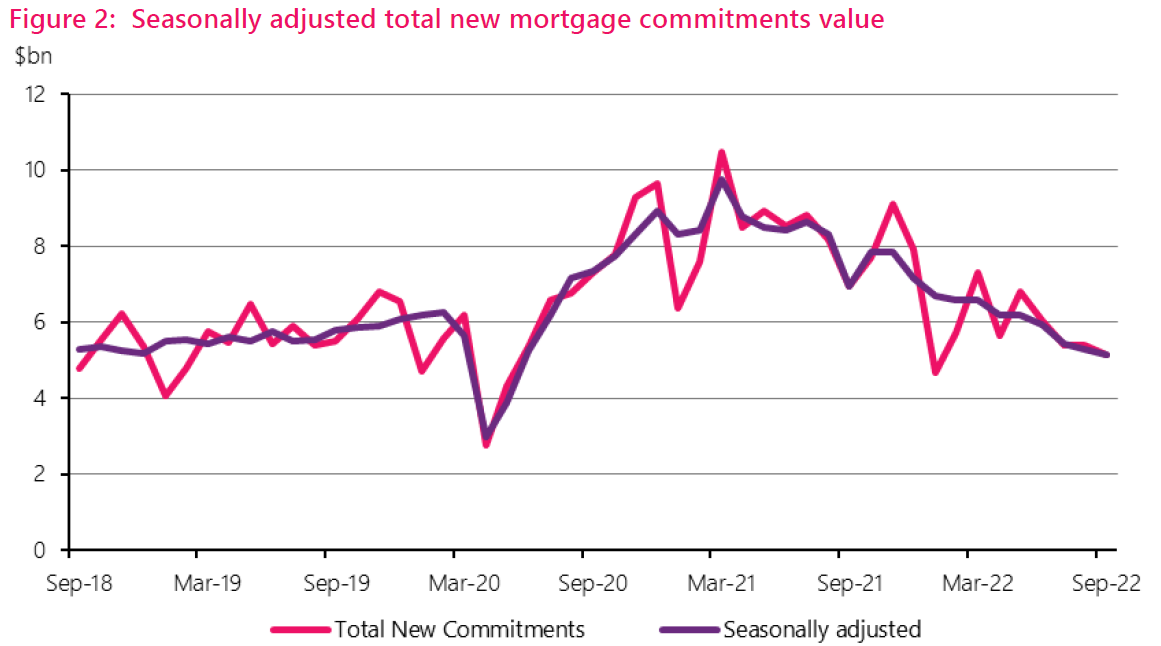

The amount of mortgage borrowing is still flagging, with the latest Reserve Bank figures showing the $5.135 billion advanced in September was the lowest this year - if you discount the always slow month of January.

But separate quarterly figures detailing residential mortgage loan reconciliation show that the amount charged in interest during the September quarter rose above $3 billion for the first time since 2017.

And in fact the $3.21 billion charged during the quarter was the highest figure the RBNZ has recorded since it started this data series in 2014.

With the interest added, it meant that there was some $5.622 billion of scheduled repayments during the quarter - which is also a new high water mark for this series.

Repayment deficiencies were $202 million, which is up quite a bit from $156 million in the previous quarter. However the deficiencies did get well above $200 million and even $300 million during 2021. But nevertheless these figures will be worth keeping an eye on.

However, reflecting what's going on with the monthly mortgage figures, the stock of mortgages increased by just $2.588 billion, which apart from the Covid-affected June 2020 quarter, is the smallest increase in seven years. The stock total stood at $337.395 billion at the end of the quarter.

Going back to the monthly figures, the RBNZ said there were 14,578 new mortgage commitments in September, down 3.5% from 15,109 in August. Compared with September 2021, new mortgage commitments were down 27.0% from 19,961.

And, yes, September 2022 had the lowest number of commitments for a month of September since data collection began in late 2013.

The slightly over $5.1 billion advanced during the month was down some 25.9% on the over $6.9 billion advanced during September 2021 as the previously white hot market was just starting to cool. RBNZ said on a seasonally adjusted basis, the September 2022 figures were down 3% from the August 2022 figures.

Also, RBNZ said the average value of new mortgage commitments across all borrower types fell for a fourth consecutive month, down 1.7% from $358,263 in August to $352,243 in September.

"However, this decline is smaller than those observed in July and August, and the average loan size across all borrower types was still up 1.4% annually," the RBNZ said.

Among the buyer groups the first home buyers are still hanging tough, maintaining a close-to-record share of the monthly mortgage money.

During September the FHB group borrowed $1.064 billion, which represented 20.7% of the total advanced - down just slightly from the record level of 20.8% in August 2022.

Investors are still in large part heading for the sidelines though.

They borrowed just $808 million in September. This meant their overall share of the mortgage money advanced in the month decreased from 16.7% in August to 15.8% - which equalled the record low of this grouping in July 2022.

15 Comments

All points to further decreases in house prices...

Imagine being a Mortgage Broker right now ? Or owning the company like Squirrel Mortgages.

Did I invest a decade and a half of healthy earnings wisely?

Was a time when banks were there to partner with their individual customers in the interests of both individual and social progress. The local branch managers were respected and active members of the community. They recognised and greeted their customers in the streets of the district.

Surely someone who is an historian of banking can tell us when that changed and why.

It seems unbelievable that banks can continue to grow record profits at a time of wider socio-economic crisis.

.

Yeah its gross..

Professor Richard Werner: A whistle stop tour of modern banking https://youtu.be/2e7gme3CZbo

ANZ $2billion profit dwarfed by Shell announcing record 9.5billion profits ! seems that there's a global crisis going -- except in Banking or oil and gas -- if we need to wonder where all the government/taxpayer borrowing has gone -- Wonder no more!!

LSP and a fuel discount that simply increased retailers margins and profits massively ! -

Shell's profit is global, ANZ's was just the excess they sucked out of NZ

The why is easy- GREED-PURE GREED.

How people couldn't see they were being gamed into a lifetime of being debt serfs is an astonishing testament to human gullibility.

So having to pay for the benefit of living under a roof, be it by rent or by mortgage, is a life of servitude. What nonsense, why would you expect to live in house for free?

Paying a reasonable price for a depreciating consumer good = practicality. Paying an entire lifetime of average savings for the benefit you describe = insanity (or financial slavery).

OK and? What did you expect people at an individual/household level to do about it? Go and live in their local park?

Vote for change

You might want to check the platform on which the government specifically campaigned on to get elected in 2017.

Many people already voted to change. If you've sat on the sidelines waiting for it for the last five years then you not only got a shitty deal but you've probably also deferred some significant life milestones for the point of feeling smug about how much smarter you are than everyone else.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.