The slow, relentless, but orderly slide in term deposit offer rates continues.

Today, BNZ ended its 4% one year special rate, reverting it to 3.85%.

Rates in the high 3%s are where this market has settled down to.

But there are exceptions, and among those there will be opportunities. To be fair however, when rates get this low there are only relative benefits to be found.

Rates above 5% have virtually disappeared, even among non-bank deposit takers (NBDT). But there is still one, from Gold Bank Finance.

Rates above 4% from banks are now only offered for the longer terms of three years and longer (although Westpac still has a 4% rate for two years).

Among banks, for terms less than one year, only Rabobank, Bank of China, and ICBC still offer 4% or more. The chance these will last much longer is low, however. Among NBDTs they are vanishing too, although these 4%+ offers may last a bit longer.

The rate curves have flattened notably. The difference between six months and one year has fallen to eight basis points and is no longer significant. This world is essentially flat.

If you rely on term deposit interest for part of your income, the lower rates go, the more attractive a switch will seem. There may be historic memories lingering about the risks of depositing with NBDTs, but that risk has now substantially passed, and can be managed by splitting investments between institutions.

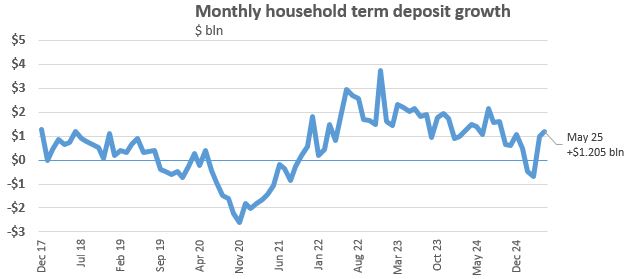

Funds flows into household term deposit accounts is still rising at more than $1 billion per month, which is likely more than banks need at present.

There is plenty of evidence that mortgage borrowers are quite comfortable switching banks, but that evidence is sparse on the deposit side. Bank deposit books 'replicate' strongly still, even when rates are low. With little rate variation and the actual reward being low, motivation to change will be low too. But at least now the field is open a tiny bit wider with the taxpayer guaranteeing accounts to $100,000, even at authorised NBDTs.

When you invest, always check how interest is compounded. Depending on how much you are committing, compounding more often is materially better. But some banks advertise their "interest at maturity" rates different to their compounding rates, which for some can be set a little lower. Both Kiwibank and Rabobank do this, although most other main banks don't.

Use the calculator at the foot of this article to see the differences.

We should also point out that after-tax returns can be enhanced for some savers with higher tax rates by the choice of PIE structures. Not all institutions offer these, but most of the main banks do. For a nine month bank offer, they can be boosted by about 30 basis points going this way. In some cases that will make up any difference, or more.

Always ask a bank for a better rate. Many bank staff have discretion to offer more than the advertised rate. (And check your bank's app offers as they too are often enhanced to retain you). But in this environment don't get your hopes up for a positive response. Carded rates are likely to now be the 'best rate', except in quite special circumstances.

Use the term deposit calculator here, or the one below the table, to calculate your expected net after-tax returns.

The latest headline term deposit rate offers are in this table after the recent changes over the past month. The pink background colour-code indicates 5%+ rates still available. The yellow colour code for those under 4%. Bolded rates are the "best-bank", the highest carded rate from any bank at this time.

This table only lists institutions covered by the Depositor Compensation Scheme.

| for a $25,000 deposit July 24, 2025 |

Rating | 3/4 mths |

5 / 6 / 7 mths |

8 - 11 mths |

1 yr | 18mth | 2 yrs | 3 yrs |

| Main banks | ||||||||

| ANZ | AA- | 3.50 | 3.90 | 3.85 | 3.80 | 3.80 | 3.90 | 4.00 |

| AA- | 3.40 | 3.90 | 3.85 | 3.85 | 3.85 | 3.90 | 4.05 | |

| AA- | 3.55 | 3.90 | 3.90 | 3.85 | 3.85 | 3.90 | 4.00 | |

| A | 3.55 | 3.95 | 3.90 | 3.80 | 3.90 | 4.00 | ||

| AA- | 3.45 | 3.90 | 3.85 | 3.80 | 3.90 | 4.00 | 4.10 | |

| Kiwi Bonds. 'risk-free' | AA+ | 3.00 | 3.00 | 3.25 | ||||

| Rating | 3/4 mths |

5 / 6 / 7 mths |

8 - 11 mths |

1 yr | 18mth | 2 yrs | 3 yrs | |

| Other banks | ||||||||

| Bank of China | A | 3.75 | 4.05 | 4.00 | 3.95 | 3.95 | 4.05 | 4.10 |

| China Constr. Bank | A | 3.25 | 3.70 | 3.70 | 3.70 | 3.75 | 3.85 | 3.90 |

| Co-operative Bank | BBB+ | 3.50 | 3.95 | 3.90 | 3.85 | 3.90 | 4.00 | 4.10 |

| Heartland Bank | BBB | 3.60 | 3.90 | 3.90 | 3.85 | 3.90 | 4.00 | 4.15 |

| ICBC | A | 3.75 | 4.05 | 4.00 | 3.95 | 3.95 | 4.10 | 4.10 |

| A | 3.55 | 4.00 | 3.90 | 3.90 | 3.95 | 3.90 | 4.00 | |

| BBB | 3.50 | 4.00 | 3.90 | 4.00 | 4.00 | 3.95 | 4.00 | |

| BBB+ | 3.60 | 3.90 | 3.90 | 3.85 | 3.90 | 4.00 | 4.10 | |

| Non-Bank Deposit Takers | Rating | 3/4 mths |

5 / 6 / 7 mths |

8 - 11 mths |

1 yr | 18mth | 2 yrs | 3 yrs |

| Community institutions | ||||||||

| First Credit Union | BB | 4.00 | 4.25 | 4.25 | 4.25 | 4.15 | 4.15 | |

| Heretaunga Bldg Society | 3.50 | 4.00 | 3.95 | 4.05 | ||||

| Nelson Building Society | BB+ | 3.25 | 3.75 | 3.75 | 3.60 | 3.80 | 3.70 | 4.00 |

| Police Credit Union | BB+ | 3.70 | 4.00 | 3.95 | 3.90 | 3.90 | 3.90 | |

| UnityMoney | BB | 3.30 | 3.75 | 3.75 | 3.60 | 3.50 | 3.55 | 3.55 |

| Wairarapa Bldg Society | BB+ | 3.60 | 4.00 | 4.00 | 4.00 | 3.95 | 3.95 | |

| Finance companies | ||||||||

| Christian Savings | BB+ | 3.50 | 4.00 | 3.95 | 3.95 | 4.00 | 4.05 | 4.15 |

| Finance Direct | 3.75 | 4.10 | 4.25 | 4.65 | 4.15 | |||

| General Finance | BB | 4.10 | 4.50 | 4.50 | 4.70 | 4.50 | 4.50 | 4.50 |

| Gold Band Finance | BB- | 3.75 | 3.75 | 4.95 | 5.10 | 5.05 | 4.99 | |

| Liberty Financial | BBB | 3.70 | 4.50 | 4.55 | 4.65 | 4.65 | 4.55 | 4.35 |

| Mutual Credit Finance | B+ | 4.75 | 4.75 | 4.95 | 4.95 | |||

| Xceda Finance | B+ | 4.50 | 4.70 | 4.60 | 4.50 | 4.50 | 4.40 |

Term deposit rates

Select chart tabs

Daily swap rates

Select chart tabs

Term deposit calculator

4 Comments

Interesting article. In a fiat currency monetary system what is the purpose of savings? Savings withdraw money from circulation - income that is surplus or accumulated in the private sector. Savings helps to control the money supply as an inflation fighting tool. The problem for banks is that they lose money on savings. Banks can only make money if there is a lot more in loans than deposits.

The saver has a choice to hold their surplus income or to spend it on consumption or real world assets. So why are saving rates increasing in NZ even as the returns fall? Why is there still high demand for government bonds from savers even as debt to GDP expands?

Keynes,

You must have known the answers before you asked AI. The greater the level of uncertainty, the more companies and individuals will delay/abandon capital investments. A prime example is Berkshire Hathaway, now with over US$300bn in liquid assets.

Even in boom times, cash always has a place in an investment portfolio.

Chat GPT:

So why are deposits still rising even as returns are falling?

This is where things get interesting. It suggests behavioral and structural caution:

1. Lack of Better Options

-

Even with falling returns, term deposits are still safer and more rewarding than a volatile housing market or stock market right now.

-

For example, a 5% return on a 6–12 month term is still appealing if you think equities might go nowhere or housing could decline further.

2. Liquidity Preference

-

Households may want access to funds quickly — term deposits provide that (especially short-term ones) with a fixed return and no risk.

-

In uncertain times, people want low-risk, cash-like assets over long-term investments.

3. Delayed Consumption & Investment

-

This signals continued deferred spending and delayed capital investment, both of which weaken aggregate demand.

-

Households and businesses are parking cash “until things become clearer.”

Most of my money is in TDs because it's easy and I find thinking too much about finances is bad for the soul.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.