By Jenée Tibshraeny

More borrowers are finding bones to pick with their banks as interest rates drop to record lows.

The Banking Ombudsman Scheme in its 2014/15 Annual Report notes it has received more complaints from bank customers about early repayment costs to break fixed-term loans, since interest rates started falling this year.

The Banking Ombudsman Nicola Sladden, says that of the 28 cases regarding these breaking costs dealt with over the year to June 30, it received 24 from January.

In fact, since the start of the new financial year in July, it’s already received 24 complaints regarding early repayment costs to break fixed-term loans.

The average two-year fixed mortgage rate across all the banks that operate in New Zealand has fallen to a record low of 4.84%, from 6.35% in August 2014.

Sladden says “People are generally aware there is a cost associated with breaking their loan early, but the rise in complaints has been caused by people not fully understanding how the early repayment charge is calculated.”

Banks use complex formulas to calculate these costs, which are based on the length of a loan, and increase if wholesale interest rates drop.

Sladden says customers are often shocked this charge can increase by “quite a few thousand dollars” in just a few weeks.

She maintains banks disclose adequate information to customers about these break costs when they take out loans, but the miscommunication arises when people want to change their loan agreements.

“The key is for banks to better explain how the cost is made up so people can better understand it and make informed decisions when they go to change their lending arrangements,” she says.

The Ombudsman’s observations correlate with those which two mortgage brokers and a bank chief executive told interest.co.nz about earlier this month.

They said low interest rates had prompted an influx of borrowers to consider breaking their fixed-term contracts, to capitalise on the cheaper rates on offer.

Squirrel Mortgages managing director, John Bolton, said he had a number of clients who fixed at mortgage rates in the mid-5%s and were now suffering from “post-fixing dissonance”.

Systemic failures picked up regarding credit card fees and currency conversions

Issues related to ‘cards’ make up the third largest area of contention the Ombudsman has dealt with over the year.

“When it came to cards, specifically credit cards, customers’ chief concerns were excessive or unfair fees, particularly for international transactions and late payments, and banks’ refusal to compensate customers for fraud or theft involving their cards,” the Scheme’s annual report says.

The portion of ‘card’ related cases the Ombudsman has received has risen over the past few years, as the amount of credit card debt New Zealanders owe has increased by 15% from $5.678 billion at the start of July 2012 to $6.547 billion at the end of June this year.

The Banking Ombudsman Scheme’s annual report highlights a “systemic” failure it picked up, after it found a bank wasn’t straight up with a customer about when they would start being charged annual fees for their new credit card.

It noted the bank had sent the customer a letter with “confusing information” about when the fee would take effect, so got the bank to agree to contact customers before they charged them, so they knew what they would be paying and could cancel the card if they wished.

It also points out a "systemic" failure it came across with currency conversions at ATMs:

“After upholding a complaint about high currency conversion rates applied on EFTPOS card withdrawals at a bank’s ATMs, we asked the bank to see whether it had incorrectly charged other customers as well.

“The bank reported that it had identified and reimbursed a small number of customers affected by how it had applied its conversion rates to such withdrawals.”

A 2013 Treasury report into the competitiveness of the banking sector has described some bank fees as “concerning”. It says, "While banks compete relatively fiercely on headline interest rates, it is possible that they use the lower level of scrutiny surrounding fees to extract uncompetitive profits."

As for interest rates on credit cards, Sladden says “The complaints we received are related to how the interest is being applied in a particular case and how charges are being made, and don’t relate to the actual interest rate, even though I’m aware this is a broader question.”

As shown in this interest.co.nz report, credit card interest rates have been increasing over the past couple of years, despite the overall lower interest rate environment and the Official Cash Rate decreasing.

While the Reserve Bank of Australia has pulled banks up for this in a submission to an Australian Senate inquiry into credit cards, New Zealand’s Minister of Commerce and Consumer Affairs Paul Goldsmith has told interest.co.nz he isn’t going to get involved.

Bank customers dub notice periods for breaking term deposits "unfair"

The second largest category of cases the Ombudsman’s addressed over the past year, relate to ‘bank accounts’, with the portion of these complaints and disputes it’s handled rising to 25%, from 19% in 2013/14.

The Ombudsman Scheme’s annual report says savings account problems have contributed to this rise, with these complaints and disputes tripling from 28 to 93 in a year.

It notes, “This year, the bigger banks began to introduce explicit notice periods for customers who want to break their term deposits. The intention is to maintain liquidity levels.

“We received 51 cases (40 enquiries, seven complaints and four disputes) on this point. Customers felt the change was unfair, or that banks had breached existing terms and conditions.”

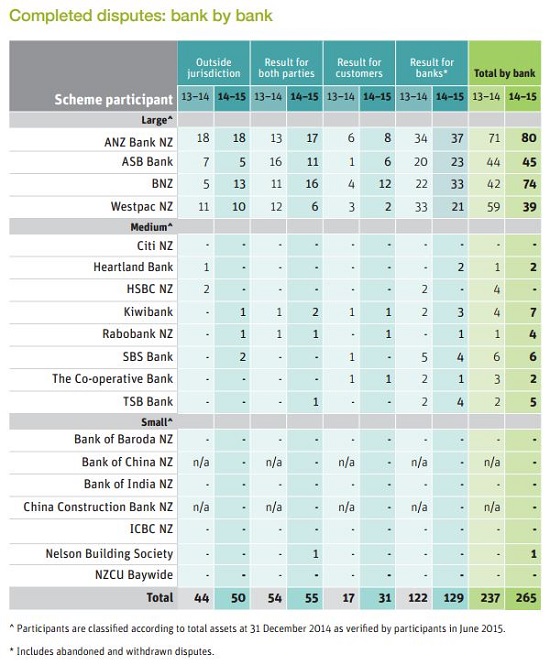

Number of disputes involving BNZ has increased 43% over the year

Comparing trends between the big banks that have been at the centre of disputes dealt with by the Ombudsman, BNZ appears to be an outlier.

While since 2013/14 there’s been a decline in the number of completed disputes the Ombudsman’s dealt with involving ANZ and Westpac, and basically no change in the number ASB’s been party to, the number of disputes BNZ has been at the centre of has increased by 43% to 74.

Sladden won’t go into detail about why BNZ customers have been unhappy, but says, “We’ve been actively managing and monitoring it [BNZ], and we’re satisfied they’ve taken some steps to address that.”

BNZ says, "Our increase in disputes were largely in the categories that the Ombudsmen outlined - early repayment costs, savings accounts and fees. The services of the Ombudsman is something we're very proactive about offering our customer throughout the disputes process."

Of the 265 disputes resolved by the Ombudsman over the year, 49% ended in favour of banks, 12% in favour of customers, and 21% favourable for both banks and their customers. Around 19% were considered out of the Ombudsman’s jurisdiction.

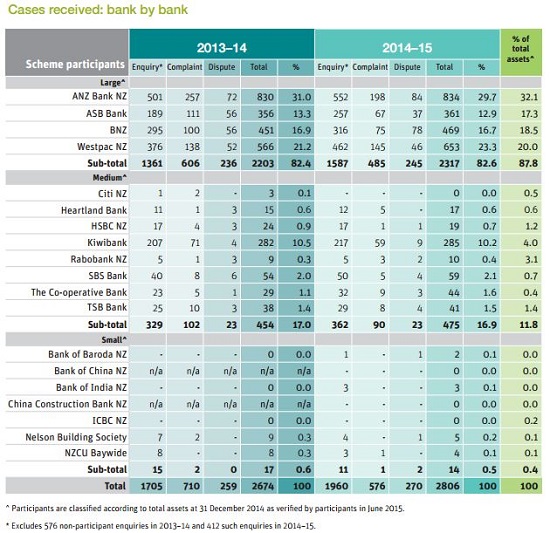

See these table from the Banking Ombudsman Scheme’s annual report to further compare disputes completed and cases received, between different banks.

17 Comments

Grumbles from depositors who are not being rewarded for the (OBR) risks we are taking to help the Aussie banks gamble on ever rising house prices, with no risk to their CEOs rapacious thick skins.

Indeed, though the depositors can withdraw their money right now, it isnt compulsory to keep it in a bank deposit account.

Though any investment has a risk of loss and indeed should, I dont think anything is paying enough for the current risk and size of impact.

The OBR is now an explicit statement that your money is at risk of not being bailed out by the Government where before its arguable a bank deposit was not risk free anyway.

considering the stealing-through-inflation thanks to the banks increasing the money supply.. it's kind of mandatory to keep savings in a bank :)

What options other than keeping cash under the mattress do we have?

Are foreign currency accounts (in a NZ bank) subject to OBR despite not getting any interest for these deposits?

Inflation indexed government bonds?

What about depositors accessing the 15% interest rate, personal loan/car loan/ credit card business... Much higher interest rates than residential mortgage rates, is the business really that risky?

Sure, that was the finance companies, remember how that went?

Yields for finance companies have never been better. The public has limited access now though as they are either owned by wealthy investors, or funded by the banks.

Um no. Inflation is 0.4%, has been for a while and is likely for years (if we are lucky) hardly grand theft. Its mandatory for you to make your money work for you, not for the tax payer (and future ones) to cover your losses through your own laziness/fear/ineptitude.

Hugh Hendry said an interesting thing, I paraphrase "in such a major event I can end up a giant amongst dwarves if my losses are small compared to others." Which is the crux of it, ie ppl always consider they have to make profit on their capital and therefore take on insane risk, where actually their goal should be to protect their capital if the circumstances so dictate.

"What options" this is where you, a) take independent professional advice and pay for it up front, b) educate yourself to act on this advice independently.

Take the Great Depression as an example to model against. My suggestion is, while things are stable or declining (1929 to 1931) is cash like things which might be something like short term Govn bonds, ie 6 to 12month terms. No private investment, eg shares, property, corporate bonds will be safe at all and will I assume take big losses. You then (about 1932~33) have to move to something else as the Govn will be in dire straights and inflation is possible. That might be property, or gold...

Of course a Great Depression model is just one possibility you have to build a plan against.

On the bright side you have capital and not debt (mortgage) like me which means that you have more freedom to act. My plan is very simple, pay down the mortgage as fast as I can so I have freedom to act.

In order of risk/return:

- inflation linked government bonds

- government bonds

- low leveraged housing

- overseas government bonds

- corporate bonds

- junk bonds

- p2p lending

- high yield shares

- high leveraged housing

It's a bit cheeky of the banks, who not so long ago were saying 'fix! fix! fix! record low rate!'. Not only do they lock in a borrower at a higher rate, they ping them again when they try and break and return to the market rate.

Indeed, if this was the USA I'd have expected a class action by now.

You just have to suck it up or pay a break fee. I was on a fixed mortgage of 8.6% for 7 years, it was great for about 3 or 4 then interest rates hit record lows. You cannot have it both ways, if the rates go up your not going to go crying to the bank are you ? Just count yourself lucky that the rates are so low now regardless compared to only a few years ago..

I have fixed from time to time and accept that break fees are part of the deal that I signed up for. Recently I did ask for a quote on the fee and got a number that sounded about right. But the number did not work for me on what I wanted to do. But thats the deal so no grumbles.

On the other hand some years ago the same bank quoted an enormous amount to break the fix even though it was only a month or so from the end. A clear extortion attempt. Wasn't happy.

It's all about the amount of the break fee, not the agreement as such. Sometimes it's reasonable and sometimes they are ripping you off.

Break fees must only reflect cost to the bank - otherwise you'd have recourse through the Ombudsman. That said, banks do tend to interpret the CCCFA differently. One of the issues you have as a customer, is that you don't have visibility of the relevant wholesale rates (past and present) which go into calculating an ERA. If you believe you've been ripped off and the bank won't budge, take it to the Ombudsman. Although it's likely the bank will be able to prove their case.

Never believe banks when they cry "interest rates about to rise" and "better fix now as rates are at the bottom". Since 2008 until now these cries have been wrong.

Interest rates will not be rising for many years to come or until after the global currency reset.

Keep your fixing short-term.

Forecasting interest rates is a mugs game - but, they will be right at some point, and that point is only going to get closer. I don't see retail home loan rates going much lower, but I'm just another mug.

rjn1 - you've proved that you're no mug with that one statement alone - the mugs are the ones that think that they know what's going to happen, and in my experience, always seems to be the ones hanging the most out there when it goes wrong and get hurts the most accordingly.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.