Analysis produced by the Reserve Bank suggests that house price falls would need to reach in excess of about 20% in order to cause seriously large numbers of homeowners to be in the dreaded negative equity with their houses.

The RBNZ, which itself sees house prices falling by around 10%, has crunched the numbers in its latest Financial Stability Report.

It notes that the housing market is vulnerable to a downturn.

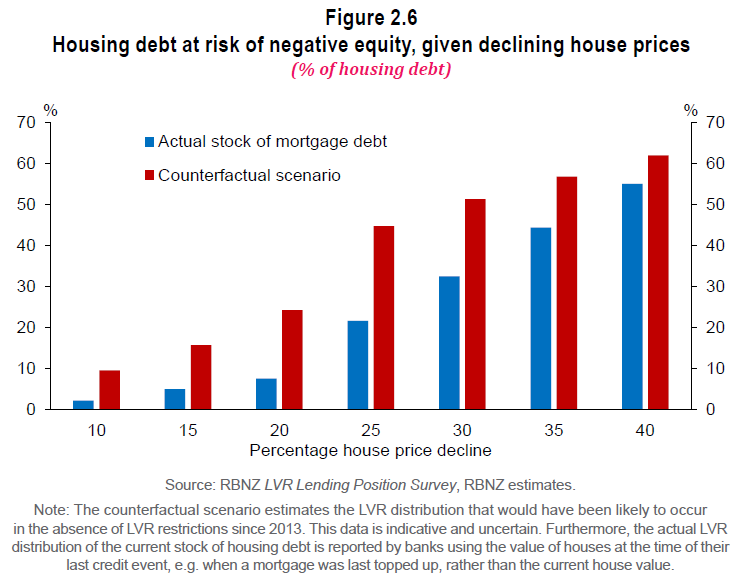

The data analysed by the RBNZ suggests that at house price declines of 20% only around 7.5% of the stock of mortgage debt goes into negative equity.

However, a price drop of 25% sees the amount of mortgage stock tipped into negative equity climb sharply to 21.5%.

"Household stress could be accentuated by declining house prices. After nearly two decades of house price growth generally exceeding the growth rate of incomes, the current economic downturn could bring a significant correction," it says.

"Declining international arrivals, as well as the departure of temporary workers from New Zealand, may weigh further on housing demand. With the ratio of the median house price to median income near an all-time high, a major correction would test the resilience of households and lenders."

It stresses, however, that the loan to value ratio (LVR) restrictions that were put in place by the RBNZ in 2013 have "contributed to improved household balance sheets".

Indeed 'counterfactual' data crunched by the RBNZ, which estimates what might have happened if the LVR restrictions had not been put in place, suggests that a 20% price fall could have tipped 24.2% of the stock of mortgage debt into negative equity, while a 25% drop in house prices could have seen as much as 44.6% of the mortgage debt in negative equity.

"The proportion of households with low equity buffers has declined substantially since 2013, and is well below the Reserve Bank’s estimates of what it would have been in the absence of LVR restrictions.

"While LVR restrictions have had distributional impacts, overall they have been positive for financial stability. Household balance sheets are generally now able to absorb a greater decline in house prices without going into negative equity (figure 2.6).

"This leaves most borrowers in a position where they would be able to restructure debt to withstand temporary income losses. As a result, there will be fewer non-performing housing loans and fewer mortgagee sales, which reduces the chance of a negative feedback loop causing a more severe decline in house prices," the RBNZ said.

As of May 1 the LVR restrictions were removed for a period of 12 months, at which time the policy setting will be reviewed.

The RBNZ says this was done so that banks would not be inhibited in assisting customers who may be experiencing temporary stress, "and is not expected to result in banks materially easing their lending criteria in the current environment".

"The removal of the policy now does not undo the resilience benefits that have been made since 2013. The benefit of the LVR policy comes from having the restrictions in place while the housing market is rising, so that subsequent corrections will be less severe."

The central bank says rising unemployment will put some households under financial stress.

"Households face income shocks through two key channels: an increase in unemployment from redundancies and business failures in sectors most directly affected by COVID-19; and reductions in pay as firms across a range of sectors look to offset pressures they face during the period of reduced revenue.

"The support packages for businesses, in particular the Wage Subsidy Scheme, have meant firms have been able to maintain more employees through the lockdown period than they could have otherwise. For the household sector as a whole, debt-servicing burdens are not very high by historical standards, reflecting historically low interest rates.

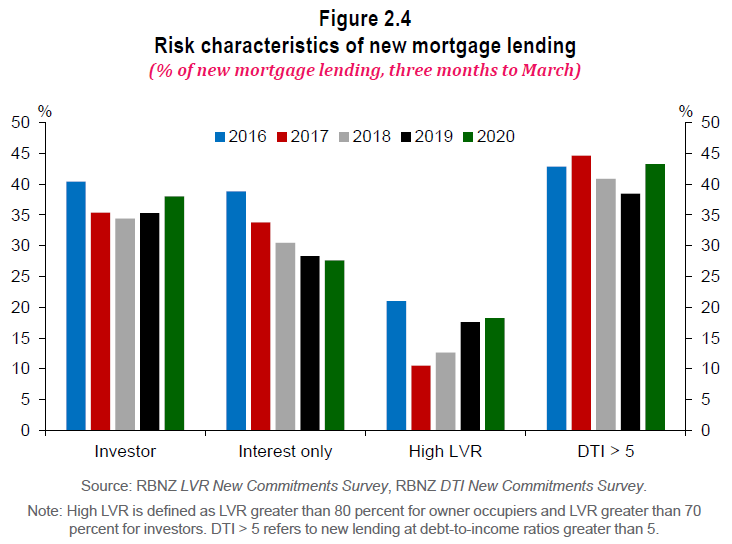

"However, a high proportion of recent entrants to the housing market has taken on debt at high debt-to-income ratios (figure 2.4). These households will have less resilience to absorb declines or losses of income, and are more likely to be left in positions of being unable to service their mortgages."

"Banks have supported mortgage and consumer credit borrowers with options to switch to interest-only terms or defer payments for up to six months, allowing them time to adjust to temporary income shocks without entering into arrears. As at mid-May, banks have reported granting payment reductions or deferrals on 13 percent by value of total household lending. However, by shifting loan repayments to future dates, payment deferrals ultimately increase households’ debt servicing burden over the remaining term of their borrowing. If current pay reductions and elevated unemployment persist for a longer period than expected, households and banks may find that more substantial loan restructuring or remediation is necessary when deferral periods end."

156 Comments

What a bunch of nonsense. Everybody knows that house prices double every seven years.

What a bunch of nonsense. Everybody knows that house prices double every seven years.

7-10 actually.

wooosh

But do the RBNZ know how many people raided mum and dad’s equity for the 20% deposit and how many boomers are hitting retirement with that remortgage debt and expecting to clear it Ultimately from the sale to the Downsize, seemed like a great idea while house prices were always going up! Can Tony Alexander be held accountable for that advice from the seminar I went to?

please tell me you have sarc switch on, as hard to tell :)

Actually, if you look at NZ house price data series, you'll find that there have been periods where house prices have doubled in 5 - 7 years.

Through time, investment in housing has shown a remarkably good return - especially when rental yield is added to (untaxed) capital gain.

TTP

Yes there have been periods - but that cannot indicate future performance.

Not even you could believe that prices will double every 7-10yrs forever.... making median house price like $8m in Auckland by the time my 10yo is 40 (plus it still has to catch up on the last 2-3yrs of essentially nil)

Surely it's possible. Just whack mortgage rates into negative. $8 million mortgage at a negative 30% interest rate will be paid off in 25 years.

Mortgagee sales will be a thing of the past.

Not now they won't. Watch the glut of properties coming to the market

Last chance to sell before suckers stop buying and prices start falling.

Short call auctions/deadline sales brought forward before a flood of listings hit market creating a vortex sucking prices down as no one will want to pay to much as prices will be falling and it will go down twice as fast as it went up until price hit long term median.

Mean reversions do tend to overshoot.

When do you think buyers should make a move? 20% drop? 30% drop?....

Negative Equity doesn't have to gallop over the horizon this afternoon to affect the economy.

Just static prices will stop borrowing-and-spending from continuing at its recent historical pace.

And once spending reduces, the job market contracts and then we will hear the hoofbeat of panic in the markets - all of them.

Its a slow painful train wreck to watch when this happens to property.

Taking a huge hit in the sharemarket sucks, but at least by the end of day 1 you know where you stand (if you haven't sold the day before).

Imagine waking up in a house that you're stuck in, regret purchasing, can no longer afford let alone sell, and do that for 365 days in a row. Ouch.

Imagine the people in Japan who took out 100 year mortgages to buy at the peak and have been observing 30 years of declining prices - double ouch!

but a 100 year mortgage is something that your children can inherit. Imagine the possibilities.

A whole extra level of loading up future generations so we can enjoy more living it up! Boomers and National MPs are going to be salivating over that.

There will be a whole lot of people feeling a whole lot happier now they know other people are worse off.

Sort of like being given the death penalty and being happy you are not the first in line.

Misery loves company, but only other miserable company.

Imagine waking up in a house that you're stuck in, regret purchasing, can no longer afford let alone sell, and do that for 365 days in a row. Ouch

Ipsos did some research last year among homeowners. Approx 60-70% said that they couldn't afford the home they own. What that means is that the market price for their home was far too high for their ability to earn and live.

I am a firm believer in personal responsibility.

If someone saved for a deposit to obtain a $800,000 mortgage from 2010ish onwards, but got approval for up to $1,000,000 did that person keep looking at $800,000 houses? Absolutely not.

If property prices always go up then yes, the greater value of the house more than likely will result in a greater return. You're just up a certain creek without a paddle if property prices go down and stay down.

Couldn't agree more. I am glad I didn't spend to my approval limit, so DTI could remain lower than average.

so they removed the LVR so that the banks didnt call in loans and make a downward trend even bigger.

still say we should have gone with a DTI

I like Steve Keen's idea that the maximum loan for a residential property should be capped at some multiple of imputed rent. Natural handbrake when price rises are outpacing incomes. Sort of like a DTI but for income potential of the property. (Obviously doesn't imply for development land, etc.)

It's called 3 x median income and works if you set up the regulatory framework for it, which only requires Govt. to set rules so true free markets can form where no one can artificially gain a monopoly advantage as we have with land banking and council service and infrastructure.

Works particularly well for development land because that is the point where most monopolistic rentier capture and speculative gain is made.

Dribble

When national party was in power between 2014-2016, opened the gate wide open to foreign investors and let their money flood into our property market. You should know one day these risks will come after you. Funny thing is, now most of the foreign investors they are loaded with money and left the market, left poor kiwis suffering high housing price and high financial risks. This makes me wonder that whether our "National" Party is our national party or not. To me, they should be called "overseas" party. Covid-19 is not the cause, it's just the needle to burst the bubble. If it's not covid, then it will be something else.

Yes I've been thinking that the last 10 years or so. Instead of National it should be Globalisation Party or similar. Not really National at all.

And the foundation of the party on anti-communist principles, yet they want nothing more than to get further into bed with the CCP, an actual communist party. Bizarre.

Not really, call me cynical but it is all about money - always has been and always will be....

Isn't there something in the Bible about money-changers?

Weren't we warned long ago?

It wasn't always that way. Robert Muldoon, a truly great man, had policies that were the antithesis of those of the current National party.

[ Lay off the petty and childish insults. You can make your point with them. If you can't then please refrain. Ed ] has not sold his Sydney house yet....

https://www.realestate.com.au/property-apartment-nsw-mcmahons+point-133…

It's for auction on 18th June.

We shall see if the horse has already bolted....

One can only pray, in this single instance....But I do feel sorry for others, who multiplied their debt at the cost of others too.

I agree. I personally would like to see a moderate right-of-center party focused on the interests of all Kiwis, and ready to make the necessary hard calls in order to realign and improve the overall efficiency and sustainability of the NZ economy.

National has demonstrated quite poor performance as far as this aspect is concerned. They might have been named the Housing Speculators Party. They claim they have the interest of business first, but I have not seen that in their actual policies and behaviors. Their only outdated and repetitive mantra has been "there is no housing bubble/crisis" and "the solution to all evils is less regulation".

The alternatives are not appealing either: the populism of NZ first, the utter ignorance of even the most basic economics demonstrated by the Green Part, and the dilettantism and lack of proper incisive policies of Labour, they all are quite disheartening.

Who was that intelligent commentator who used to advocate for a "Common Sense Political Party" a few years back, but must have given up, because he was the only one with common sense.

Many a true word, spoken in jest.

I certainly hope the younger Generation do not learn from some of their Elders who all piled in, boots and all and followed the JK Mantra that Houses were an asset to be plucked like a Tulip and flowered with ecstasy and swallowed hook line and sinker.

In the 1980's the philosphy of the neoliberals was to get inflation down and to privatise things. We'll the focus now might be to instead of getting inflation down, to get house prices down. For in the end, that will be what destroys the economy.

IT is not in the Kiwi psychic to have a party that focuses on the interests of all Kiwis. Look after me to hell with you mate

Sad but true. We have become an incredibly greedy, selfish society.

Yes National bad, but tell me, have house prices gotten better or worse under Labour?

Yes it is a rhetorical question.

International Party. Fits well. Good idea.

An economy built on population growth and tourism, without population growth and tourism. Too funny.. watch them twist and turn to get them back again.

Getting calls from people looking for jobs. If for the next 6 months i could hire and fire at my discretion i would hire a few.

Tough for some, opportunity for others. I've had two cold job offers this week out of the blue.

I think you work in ICT ? If you do, I am not surprised.

I do, yes.

LOL I thought so. My almost 30 years international experience in ICT has taught me that, short of a zombie apocalypse event, a professional in this industry who keeps himself/herself constantly updated with the latest trends and technologies will always be in demand.

I did a rebuild in 2013 that ran well over cost and ended owing $330k to the bank. I have paid it off by cashing in my non Kiwisaver retirement fund and paying over $4000PM to get rid of it by mid-2018.

I would not feel comfortable having a sizable mortgage at present, that is for sure. If house values go down 20-30% so be it, but it is still mine. Biggest worry is my money in the ANZ safe long term..........

What were the key elements that drove it over budget?

A combo of myself and a greedy builder.

Sorry to hear that. One of the NZ industries that do need a rebuild is the building industry, that's for sure.

My only recommendation re: your savings, assuming that they are significant, is: diversify, diversify and diversify. Across financial institutions as well as across types of investments and if you can, across countries and currencies. I share your concern about the real solidity of NZ banks: we shall see.

Yeah, am looking at diversifying alright. Have some gold and cash in a safe. Looking at currency elsewhere, AUD/USD.

"Figures produced by the RBNZ suggest that house price falls in excess of 20% would start to produce large numbers of people in negative equity"

Wow, it's like nobody knew this and there was never a risk of this. Certainly very, very little discussion of this in the NZ media over the past, oh, many years (only many international warnings about our market). Would never happen here right, we're diffrunt.

Wow, it's like nobody knew this and there was never a risk of this. Certainly very, very little discussion of this in the NZ media over the past, oh, many years (only many international warnings about our market). Would never happen here right, we're diffrunt.

Yes, but to be fair, nobody could have seen a global pandemic coming. Over the years the NZ media has done a pretty good job of explaining the housing bubble in terms of market distortions and demographics. However, I never once read in the mainstream media about how banks lend into existence for mortgages. I would say that the majority of NZers don't understand this. At least they don't understand the extent to which mortgage lending is based on confidence over capital.

"nobody could have seen a global pandemic coming." No, but the world has had some sort of major economic issue about every 10 years – 2008 GFC, late 90s asian crisis, 1987 stock market crash (which impacted NZ quite hard) – it was bound to be something serious sooner rather than later.

Plenty of people saw the possibility of a pandemic coming.

Yes indeed.

We are so privileged to be living through what will be remembered as an incredible time in history. Bring on the reset.

I have a terrible suspicion that any 'reset' will be carefully constructed in a way to benefit the few at the expense of the many. So far, the reset has been helicopter money for Wall Street, and the protection of the investor class at the expense of future generations the world over. Unless millions of people start to live their lives differently in a co-ordinated way to minimise exposure to a rigged system of private finance, things will go on as they have been going on, except you'll be microchipped and curtailed in your ability to explore this green earth.

Wage subsidy and small business loans helped the many. Also maintaining the increases to benefits and minimum wage from 1 April despite Covid 19 is helping the poor masses.

Yes I agree wage subsidy was helpful, as were small business loans, but at best they can be regarded as temporary measures to mask the structural inequities, and we will be servicing the interest on this borrowing to pay for these things. I think the benefit increase was justified considering the cost of living in NZ, not the Covid crisis, also the minimum wage increase may be absorbed by Maccas or some other big player, but at this time could be the difference between a small business staying viable or employing 2 instead of 3 staff. Not sure about that one. But it all speaks to the same structural inequities which are exacerbated by situations like these. Good luck to us all

I don't expect the Reset to be 'fair' but it will give new opportunities, just as the 1984 Labour Government gave some to me.

I like that attitude. What opportunities did the 84 Govt give you?

It opened up the opportunity of Financial Markets dealing, when the dollar floated.

FX?

FX for a short period then the Rates desk. Law of the jungle in those days. You don’t want to be trading the thirds when Asia wakes up on a Monday. Rates are a lot easier.

Did you ever work with John Key in the FX areas?

All available levers are being pulled. Fiscal and Monetary to keep the fall to 10%. If prices can be stabilised at that level and there has been a plausible case to relax border restrictions. The government-backed creative financing will start up to at least keep the prices going sideways for a few years before a very gradual increase.

Interest rates will be in the low 2's fixed for 5 years. Rather than renting from the bank on interest only, you will actually be able to retire some debt. The house will still be overvalued by international standards. But it will be manageable as long as your job/income is secure.

A 10% decline is what we got in the GFC, this is more than twice as bad and by far more will be unemployed. This will go over 20% down the gurgler minimum.

My personal views is 20% decrease in house prices in 2020. When banks like ANZ state that they forecast 10% to 15% decrease, with the proviso that there is a significant further risk, it is clear that they do expect 20%. Other announcements , behaviors and policies by many actors, not least the RBNZ, all point towards an expected 20% decrease by end of the year, in my opinion.

20% this year and another 5% at least next year.

40% in some places like Q'town.

With the US stacking numbers like 39k new infections yesterday this could get a hell of a lot worse.

I am so amazed that these people are masters of stating the obvious! With a need for a 20% deposit under LVR, if the value of property fell more than 20% of course there will be some in negative equity! IT IS BLOODY OBVIOUS!

after the '87 crash there were quite a few in negative equity. property prices had been going gang busters prior to that one too. The world didn't end. A few got taught salient lessons about borrowing against rising house valuations. And most importantly the Government and banks did NOTHING to stop a property bubble bursting again. Indeed if you look at the situation, they could be argued to have made such an event, irrespective of the trigger, a certainty. So now they are crying into their cups?

to be fair it depends on what the drop is marked to. If you had 20% equity and then the house price went up, then a 20% decline would not put you under water.

EG

$500k property, $100k equity, $400k loan. 1 year later up say 10%, then $550k property, and presuming at least some P&I ... $390k loan. Now, the market drops 20%, so property now $440k and loan $390 = 13% equity, so not negative. Makes you locked in, since you'll struggle to refi, but not negative. Of course, if it was recent purchase... or market in your area had no increase.. then not looking awesome.

RBNZ analyses housing negative equity risks...

Very fact that RBNZ is analysing such a scenarion is worrysome and poosible.

The RBNZ, which itself sees house prices falling by around 10%, has crunched the numbers in its latest Financial Stability Report.

RBNZ sees is actually Hoping that house price falls stop at 10%.

Along with this Governor Orr looking at possibility of banks going bust......

RBNZ says the banks have $40 billion of loans on commercial property with $5 billion of that in development projects.

Rest assure that commercial properties will reach fall of 20% plus very soon, if not already.

5 Billion in development project... Banks have to worry but is more dangerous for people/agency also who are in middle of it as are bound to lose their equity and will be left with unfinished project and Negative equity / debt to bank and also losing collateral (most probaly a house) . Recipe for default / Bankruptcy - domino effect.

Not to be fooled by pause in default/ unemployment data which is a result of all the money being thrown by government as this may be a calm before the storm.

"Rest assure that commercial properties will reach fall of 20% plus very soon, if not already."

Already starting. Kiwi Property Group wrote down their property valuations by 8.5% in their most recent results to 31 March 2020.

Wait until banks review commercial property valuations for smaller mum and dad commercial property borrowers - some may breach debt covenants and require reduction in the mortgage. What will smaller commercial property borrowers do? 1) sell the illiquid commercial property? 2) sell other assets to raise cash (e.g residential investment property, boats, cars, etc)

"While Kiwi Property’s FY20 revenue was largely unaffected by COVID-19, the widespread economic uncertainty caused by the pandemic prompted valuers to soften their assumptions, resulting in a $290 million, or 8.5%, write-down in the fair value of the Company’s property portfolio.

The portfolio was valued at $3.1 billion as at 31 March 20202"

https://s3-ap-southeast-2.amazonaws.com/kp-wordpress/wp-content/uploads…

Their share price has only fallen from a peak of about $1.70 down to about 90c. So only a fall of about 50%.

"Declining international arrivals, as well as the departure of temporary workers from New Zealand, may weigh further on housing demand. With the ratio of the median house price to median income near an all-time high, a major correction would test the resilience of households and lenders."

HAPPY REALIZATION BUT IS IT TOO LATE.

That is inconvenient as a large part of this nation wealth is "made" by inflating asset prices at a rate that is greater than that of wages.

Where's TM2 when you need him to make us feel assured the market can only go up.

Remember to thank National for this when your property finally falls to affordable levels. National were the ones who pumped up Auckland's house prices over nine years by allowing foreign buyers to asset strip!

Not only have they virtually destroyed Kiwis ability to buy a home in their own neighborhood but they've also destabilize our economy over the long term.

nail. on. the. head.

Agreed. Their policy that no one in NZ, who was not leveraged up the a** to the banks, would in their right mind have supported. It has twisted the fabric of society in NZ and supported a model of debt enslavement to working tax payers wanting the security of their own home. Today Mr Orr calls worst case at 18% unemployment and 50% property drop, and banks viability in question. https://www.stuff.co.nz/business/121635138/insurers-and-nonbank-deposit…

Aussie banks bonus focused crappy lending practice, no bail outs. Vote in 120 odd days. Time to open some Kiwi bank accounts I think - cant see the Govt letting it fail as its a tax payers asset.

Hey but you're not allowed to call them out on that because if you did you were a xenophobe - in particular a xenophobe wrt to people from a communist controlled country.

Absolutely correct. When the average Kiwi can't buy a property in his own suburb, this is the clear symptom that something is terribly out of balance.

Many thanks to National and to all self-serving commentators who have been selling the housing Ponzi scheme myth of ever-increasing house prices and of paper wealth built on speculation rather than real wealth built on hard work, productivity increases, and the real economy.

In fairness to National, it was already happening under Labour, and still is. JK gave his pre-election speech in 2007 about bring down house prices, and since Labour has been in, have house prices gone up or down?

They both do not want to do what is necessary to take out the distortion in the market.

Well now, Covid has done it for them.

The question still remains, do they have the sense and then the balls to put in regulations that stop it from becoming another rinse and repeat bubble once this is all over.

The answer is no to both, for both National and Labour.

Yet, on May 8th Hilary Barry was telling FHBs that it was "a good time to get on the property ladder".

https://www.tvnz.co.nz/shows/seven-sharp/clips/how-the-property-market-…

I was seething when I saw this a couple of weeks ago. A shameless talking up of the markets without exploring any of the glaring downsides of an inevitably falling market. I realise they are being paid by ASB here but this is on the publicly-owned broadcaster. TVNZ shafting its own stakeholders.

Most on here can dismiss Ashley Church's and the RE agent's comments for the pro-property BS they are but plenty of FHBs won't be as savvy and will be schooled on the realities of negative equity in the harshest possible way.

Utterly disgusting piece of 'journalism'.

There are a lot of boomer age parents telling their children in their 20's and 30's to buy up property because its the road to riches that worked for them. Could be a disaster in the making.

Hilary Barry is a complete idiot. I am genuinely shocked that anybody would listen to anything she says.

No, actually she is lovely. You on the other hand, are a complete pendejo.

LOL coming from somebody of such a "great" intellectual stature like you, this for me is a great compliment.

I have no opinion on her character or intelligence but her comments on that day were appalling. Perhaps ignorance would be her best defence as the alternative of knowingly misleading young FHBs is far worse.

I would note that her sidekick didn't interject or offer any balance. It was just her comment that jarred with me the most. Nobody associated with that piece should escape blame.

Hillary Barry is mother of the nation and really nice.

Jacinda is Aunty to the nation and Helen is our great aunt.

:-) quite true indeed :-)

and maybe Winston is the crazy uncle ?

Point made was about her capacity for sense

Not looks

Zzzz

She is a presenter. A good one in my opinion. She doesn't write the script.

The lack of a decent current affairs show on tv is woeful. Paul Holmes as least had stories of substance. These days it is mainly stories about the presenters themselves. Just awful.

I strongly agree: Paul Holmes was quite good. I was very sad about his passing. Current presenters are dismal.

I agree.

7 Sharp is sponsored by? Yep: ASB

From 2016- 2020 (except 2019), over 40% of new mortgage lending was done on a debt to income greater than 5.

Imagine if a macroprudential measure of a debt to income ratio of 5 had been imposed by the RBNZ - the banks would have not made some 40% or so of the mortgages that they had made.

And house prices might be 20% lower than they are now.

FYI, applying a debt to income ratio of 5.0x and a LVR of 80%, would mean a house price to income of 6.25x. That is 35% lower than the current house price to income ratio of 9.7x in Auckland.

And it would be still too high.

At 35% lower prices in Auckland, the issue however would be that owner occupier buyers would have significant buying competition from property investors (due to sufficiently attractive yield spread between the rental yield and mortgage interest rates). Owner occupiers would be unable to compete due to DTI limits.

Property investors with excess borrowing capacity via unencumbered equity in their existing property portfolios would be able to borrow 100% of the purchase price of the property (by deposit recycling / equity release techniques).

Those property investors borrowing on P&I loan terms would have negative cashflow due to debt principal payments.

However, those able to borrow on interest only terms would have a positive cashflow investment property at that purchase price and be able to pay more than owner occupier buyers.

For example, at a 35% lower median house price in Auckland ($601,250), the gross rental yield (for a long term tenant) would be say 5.60% vs the current mortgage interest rate of say 3.00%, resulting in a 2.6% yield spread (5.6-3.0) if they borrowed 100% of the purchase price. That yield spread would be sufficient to cover rates, insurance, and interest costs and still be positive cashflow for the property investor.

The yield spread may be even higher for those property investors looking to rent in the Airbnb market, or student housing market (pre-COVID19).

My question would be if the "equity as down payment" model would be retained. The only market I know well is the US and you would get a baffled look if you walked into a bank there and said you were going to use the equity in another property as your down payment. It is ponzi style behavior. In the US you need actual cash and the source can't be temporary borrowing.

It is a serious structural deficiency of the NZ market. The current system rewards people who don't have any demonstrated ability to make money. The people who disregard risk and are willing to sign huge numbers of loans have been the winners here. In my (so far limited) experience of the local market the debt jockeys seem very weak: they don't have basic negotiation skills and buckle at any sign of pressure. People that have battled to own properties don't act like this.

It's worse when you think about it, the greater number of properties an investor has the quicker the accumulation of the next deposit.

E.g. 10 properties with 40% equity across the portfolio at the limit of investor LVR. Each property only needs to go up 5% in value for a deposit in another investment property. 40 properties = 1% etc.

The large cashflow oriented property investors with borrowing capacity, and can borrow on interest only terms have an advantage.

For instance, one cashflow oriented investor I know of has over 10 investment properties, with an estimated LVR of around 40%. Their estimated borrowing capacity could be over $2,000,000, and using leverage, their potential buying power could be say $5,000,000.

Cashflow oriented investors have moved initially from the large cities out to the smaller towns in search of higher rental yields. Look at the rental yields of these towns and how property investors have paid higher prices, driving the rental yields down, and making house prices unaffordable for locals to buy. Some examples of big shifts:

1) Invercargill - rental yields have fallen from 9.5% to 6.6%

2) Flaxmere in Hawkes Bay - rental yields have fallen from over 12% to 6.6%

3) Wanganui - rental yields have fallen from 14.9% to 7.0%

https://www.interest.co.nz/saving/rental-yield-indicator

Look at the locations of the property portfolio of this cashflow oriented investor and how they bought in higher yielding locations around the country - https://www.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=12…

This is how 8% of households in NZ owe 40% of household debt.

"For Brownlee, the trick was to look outside his home city of Auckland and first buy in Hamilton.

Brownlee poured all his savings from his importing job into the deposit, while his parents picked up the rest and guaranteed the loan on the proviso they would be paid back everything they put in.

Then Brownlee sat on the Hamilton home for six months, before getting it revalued.

Finding it had already gained substantially in market value, he used the increase in equity to ask the bank for a new loan for another property.

From there he moved quickly, emulating the strategy of buying homes "below market rate" and making renovations before getting them revalued so he could then borrow on the difference as soon as possible.

He was able to buy his second property at 19 and owned five by the time he was 20 years old.

Now he has 11 properties in Wellington, Hamilton, South Auckland, Hastings, Dunedin, Masterton, Whanganui and Invercargill - having chosen to hold onto all of them rather than sell."

I'm gonna go Wayne Gretzy on you CN: " I skate to where the puck is going to be, not where it has been." Obviously usually things stay as they are but I think a collapse of this magnitude is likely to have regulators, banks or the government revisit if using money that doesn't exist as a deposit makes sense. There is no real skin in the game. In NZ you have been able to turn a $30-$40k deposit 20 years ago into controlling an eight figure property portfolio with little effort.

Mike1

"I'm gonna go Wayne Gretzy on you CN: " I skate to where the puck is going to be, not where it has been."

Yes, I have the same philosophy.

Just highlighting the current situation from recent years. After seeing this behaviour and elevated property price risks, this was the reason for getting out of the residential leasing business a few years ago. There is a high degree of risk to property prices, & high degree of vulnerability to cashflows for highly leveraged property investors in my judgement. There are an increasing number of highly leveraged borrowers who will likely face cashflow stress.

Unfortunately there is also likely to be many home owners who will be collateral damage as a result of the entrance into the property market by a large number of property investors / capital gain speculators which has driven up property prices. This is the reason I choose to comment here. Potential owner occupier buyers should be aware of elevated property price risks so that owner occupiers can make a fully informed property buying decision (rather than rely on the vested financial interests of the property market promoters). Potential owner occupier buyers can choose to entirely ignore me, or to heed the warnings - it is entirely their choice.

Great point NZdan. It's a perpetual motion machine. The problem arises when cash-flow issues kick in. I talked to someone this morning that usually has 180 individual rooms rented out. He's down to 120 and every single person is having their rent paid by Civil Defense. All of those payments end in two weeks.

" All of those payments end in two weeks"

Potential cashflow stress for many highly leveraged property investors. Also when the wage subsidies expire and the mortgage payment deferrals expire ...

The sheer brutality of what is coming is scary. Every owner in the situation above is about to go to zero income. I believe they are all single family residences and the supply keeps going up.

Its nice you have been warning FHB that this is not a normal market. There is no real escape from the bubble here which must have been really hard.

And you think rents wouldn't drop? You can't assume that the same rents will be achieved in such a downturn of property prices. It's entirely possible for rents to drop 35% as well, balancing out the drop in prices.

Blobbles,

1) "And you think rents wouldn't drop? You can't assume that the same rents will be achieved in such a downturn of property prices."

You have raised a very good and very valid point. Thank you for your reminder.

2) "It's entirely possible for rents to drop 35% as well, balancing out the drop in prices."

This is certainly a possibility. Have no idea of the probability of this occurring. Would be very dependent upon credit conditions, unemployment rates, and the rate of recovery in the economy. Could easily see large rents decreases in tourism reliant locations such as Queenstown and Wanaka. Don't know about big cities such as Auckland seeing 35% drops in rent - that seems like a low probability event to me. Would be interested in hearing what happened to rentals (and magnitudes of rent falls) in places such as Las Vegas, Phoenix, and Detroit during 2008/2009 or Ireland during 2008/2009.

I have experienced firsthand, a drop in rents by 50%, however that was in an economy with important structural differences compared to NZ, & different economic circumstances (rapidly rising interest rates) to those currently in NZ.

One method of tenants meeting ever rising rents in Auckland has been increasing the number of income earners per dwelling, all contributing to the rent. Some renting households in South Auckland could have say 4-6 (or higher) income earners paying rent (bunk beds in bedrooms, people sleeping in a garage conversion, more income earning couples in the household paying rent, etc). For instance, there may be a house with 3 bedrooms, and previously it was rented by one family with children (so 1-2 earning incomes). Now it is rented to 3 income earning couples (so 6 incomes), and the garage has also been converted and is being rented to another couple (another 2 incomes means a total of 8 incomes from that same house)

The other point that I was wondering is how much total unencumbered equity there is by property investors in their property portfolios which could be leveraged into further buying power. I recall one property investor with about 14 investment properties with an LVR of about 50%, saying that they were constrained from further borrowing (and therefore buying) due to more stringent debt servicing criteria being imposed by the banks. As a result, I have heard that more property investors are moving to non bank lenders where their stress test rates are lower than the banks (around 6.0%.) Refer this thread - https://www.propertytalk.com/forum/showthread.php?44273-Lending

Rents in Queenstown and Wanaka have already dropped by at least 35%. Advertised prices are suggestions only.

Of the cities you mentioned I know two of them well and lend money in one. Rents followed an interesting pattern in 08/09. In the initial collapse rents actually went up. Counter-intuitive but there was a lack of rentals initially and people were losing their houses. Once the repos started hitting the market rents collapsed. House prices dropped to incredibly low levels so the rents needed to get a decent return were far lower than it had been.

They would have never implemented such a measure. Such measure would have made the further inflating of the housing bubble virtually impossible. This would have been contrary to the unspoken mandate of the RBNZ to keep the housing Ponzi scheme afloat at all costs.

No one ever voted to protect bank profit over the interests of expense of NZ Citizen Taxpayers. Who actually controls the RBNZ again...?

good question mate, good question indeed

Or house prices could go up due to all the RBNZ & Government help...

Always a possibility, but if that's your opinion why sell as you claimed recently? (legit question)

Well done for being open minded, house prices going up is actually not my opinion, I was simply pointing out that it's a possibility (so many people can only see one scenario playing out)

No jobs / decreased earnings, no money to pay over and above for anything.

That's because it's clearly very highly likely prices will fall not rise. There's little point talking about very remote possibilities is it?

Is there any serious and credible commentator who thinks prices won't fall?

No.

Is that a repost from September 2019 Fritz?

I think Yves is right- there is a small possibility that house prices in certain areas will go up with the lower interest rates. Bagrie also pointed to this and said rising asset prices at a time of double digit unemployment will lead to civil unrest. Definitely could happen

There's a small possibility I will win lotto this weekend.

Pointless comments.

What's your point.

"There's little point talking about very remote possibilities is it?"

Fritz,

With due respect, I believe that we should consider all possibilities. Then people can assign their own probability of that possible outcome occurring, even if that probability is extremely low. If the probability is remote, it can then be dismissed. If the possible outcome is overlooked and not even considered, then people can receive unexpected surprises and then label them as a Black Swan event (in the framework of Nasim Taleb).

This is how supposedly Black Swan events can be identified, and then probabilities are adjusted due to new information.

After all, the possibility of property prices even falling in NZ was once considered an extremely low probability event. Now the probability of that outcome has increased significantly. I have seen some property investors still believing that property prices falling by more than say 5% is outside the realm of possibilities.

Some examples of possibilities which were previously considered low probability events:

1) global pandemic

2) NEGATIVE oil prices

3) property prices falling 50% in Ireland, etc

Improved household balance sheets?

Aren’t these folk supposed to be able to add

Perhaps they could state % of GDP currently consumer sector is in debt? It is over 100%

Meanwhile projected gov debt of 53% induces apoplexy in Right wing

The huge difference is that consumer debt is an individual's choice which has no direct impact on me, as I have no obligation to meet it, nor do I suffer if it's not repaid whereas Government debt is a collective obligation repaid through future taxes. I have no say in how it's raised, how it's spent or how it's repaid. The only thing I can control is how I structure my affairs to minimise my exposure, either through tax planning or emigration.

Government debt is NOT repaid, it just revolves on differing level of interest and is eroded by inflation that gov tries to generate with help of central bank.

And huge consumer debt DOES affect others not in debt, when get a housing crisis, a la 2008.

This crisis will make 2008 look like a tea party

I’m banking on it being apocalyptic. Cash, KiwiBonds, TDs, Gold, Occupied home and a few toys.

50% reduction in houses prices, as the Reserve Bank have highlighted as a possibility, would be fantastic.

Prices back to where they should be, so all NZers could have a chance at buying a home.

https://www.stuff.co.nz/business/121635138/insurers-and-nonbank-deposit…

I disagree.

It would be devastating for many people and the economy.

A good outcome would be a 15% drop then general flatness for years.

I disagree with you. 50% decrease would be great to enable average NZers to get into homes. The privileged people who have been scoffing at the trough, can finally share with others.

Think about it...

A crash of that magnitude would wipe out a very large portion of our economy and jobs.

I have thought about it. It shows that the foundations of the economy needs fundamental correction. How can you have the highest property prices in the World, with low wages. A fundamental correction is exactually what is required.

A 50% reduction would put Auckland prices around 4-5 avg income. According to this that would make them "Seriously unaffordable" - something to hope for:

https://www.stuff.co.nz/business/110049950/auckland-ranked-among-worlds…

Very interesting : this from a Property Investor Group on Facebook I follow to help keep tabs on the feeling out there - MADNESS & GREED personified.....

POST AS BELOW FROM EARLIER TODAY - NAMES REMOVED.

Original Poster Yesterday I did some sums on a property I just missed out on. If I won that property It would have been cashflow positive at a 4.65% gross return on 100% finance. If it is that easy to hold property I really dont see how property values can drop. And hanging on to existing property cant be that hard.

Reply

XXX can you explain the term ‘100% finance’ just quickly?

Original Poster· 4h

XXX my numbers were based on purchase price of $545k and $545k debt on interest only.

Reply · 4h

XXX Did you read the article and see what the Reserve Bank Governor thinks?

Original Poster

XXX yes.

There is more useful information in that comment than the previous 100 put together, what suburb was that?

It doesn't say unfortunately. The person appears to live in CHCH from what i can see but honestly this group it appears where people live has no bearing on where they buy rentals..

This sort of comment prevails throughout the group (35k members) around Interest Only on properties / why pay the principal off / counting on capital gains and then use leverage to rinse and repeat.

Ponzi scheme? No never.... We are well and truly overdue for a reset of this type of greed....

Banks should be restricted from this sort of lending and made to unwind the loans as they come due. Its putting the rest of the system at risk. Are banks required to publish how much of this they have?

Yes : https://www.rbnz.govt.nz/statistics/c32

It's about 24% of stock, including revolving credit products.

I'm speculating, but it's highly unlikely they would gear the property in that manner. It sounds to me like they are using this calculation to work out if it's an attractive investment. A bit like using EBITDA as a measure of free cash-flow when valuing a company.

"but it's highly unlikely they would gear the property in that manner."

Property investors are borrowing 100% of the purchase price of the property investment via deposit recycling / equity release techniques.

This has led to the positive price feedback loop, which then enables the property investor to engage in more deposit recycling / equity release techniques. It keeps going, until something unexpected causes the music to stop ...

They used to do this. Don't think they can do it right now, the banks won't lend that much.

Davo36,

I understand capital gain oriented property investors are constrained.

What about for cashflow oriented property investors with low LVR's? Those buying outside of Auckland in high yielding locations such as Wanganui?

"The person appears to live in CHCH from what i can see.."

Could this be our favourite friend TM2???

I know that group. It’s essentially a cult of disciples ring lead by Grahame what every his name is who’s seen as some sort of rockstar for buying up some 50+ negatively geared rentals in the Hawkes Bay.

The people are mostly average joe blow types who believe they they have some type of unique entrepreneurial gift and bravery.

Will be interesting to see it all play out and watch the sentiment change but many have their heads jammed firmly in

"lead by Grahame what every his name is who’s seen as some sort of rockstar for buying up some 50+ negatively geared rentals in the Hawkes Bay."

FYI, Graeme Fowler is a cashflow oriented property investor.

There are other capital gain oriented property mentors promoting their services.

"If I won that property It would have been cashflow positive at a 4.65% gross return on 100% finance. If it is that easy to hold property I really dont see how property values can drop. And hanging on to existing property cant be that hard."

This is an example of a cashflow oriented property investor who doesn't seem to believe that a large drop in property prices is within the realm of possibilities. They don't see what many other commenters on interest.co.nz can see.

Here's a cunning plan:

Buy a $1 million house in Auckland. In 7 years time, it will be $2 mils. Sell that and it will be $1 mil tax free income - that is roughly 200k salary (pretax), I don't really need to work anymore.

That cunning plan was undertaken 7 years ago by a commenter on interest.co.nz

Here are some estimated ballpark numbers:

1) buy house for $1,000,000

2) finance with 80% LVR mortgage of $800,000, equity of $200,000

3) pay interest only for 7 years (at average int rate of 4.5%) - $36,000 per annum - so $252,000 over 7 years

4) ownership costs (rates, insurance and maintenance) of say $10,000 per year - $70,000 over 7 years

5) total ownership costs over 7 years - $322,000

Sale at 2,000,000

less sale costs fees of 3% - $60,000

Less mortgage repayment of $800,000

less 7 years of ownership costs - $70,000

less 7 years of financing costs - $252,000

Net proceeds after costs -$818,000

vs initial equity of $200,000

Annual return on initial equity - 22% p.a. over 7 years.

Gee, why would Kiwis ever seek to innovate and build productive businesses?

Yes they do.

If you keep ponzi scheme going with tight land supply , immigration x population growth up,

of course ,supply and demand.prices

Not to forget ,new schools ,roading ,hospitals ,i Know its been said before.

Can anyone ask govt if we need to keep climbing up with population or is this silly talk.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.