Last month was another searing one in the housing market as far as mortgage lending went.

Figures released by the Reserve Bank show $7.601 billion was advanced for new mortgages, which is easily the most for a February month, though well below the recently set monthly record of $9.652 billion in December 2020.

The February figure was some 36.2% higher than the amount borrowed in the same month a year ago ($5.579 billion).

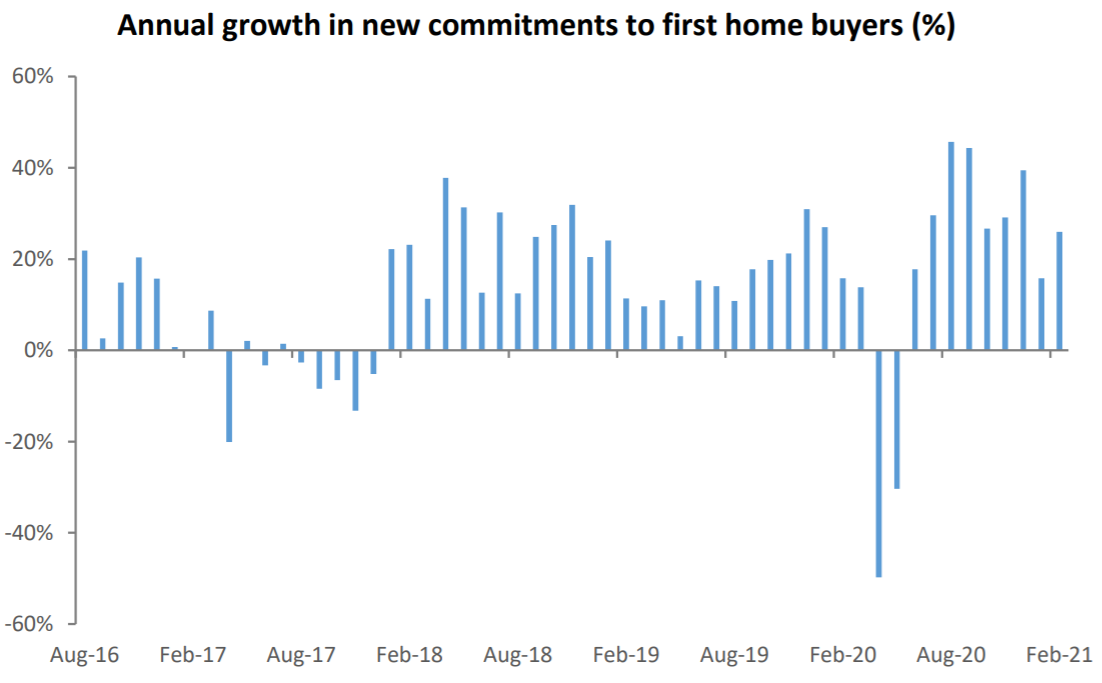

The figures confirm the recent trend that first home buyers are getting squeezed out of the market.

The FHB grouping did borrow some $1.182 billion in February, but this made up just 15.6% of the total - which is the lowest proportion captured by this grouping since August 2018. If you go back to July 2020 the FHBs were claiming 20.4% of the mortgage money.

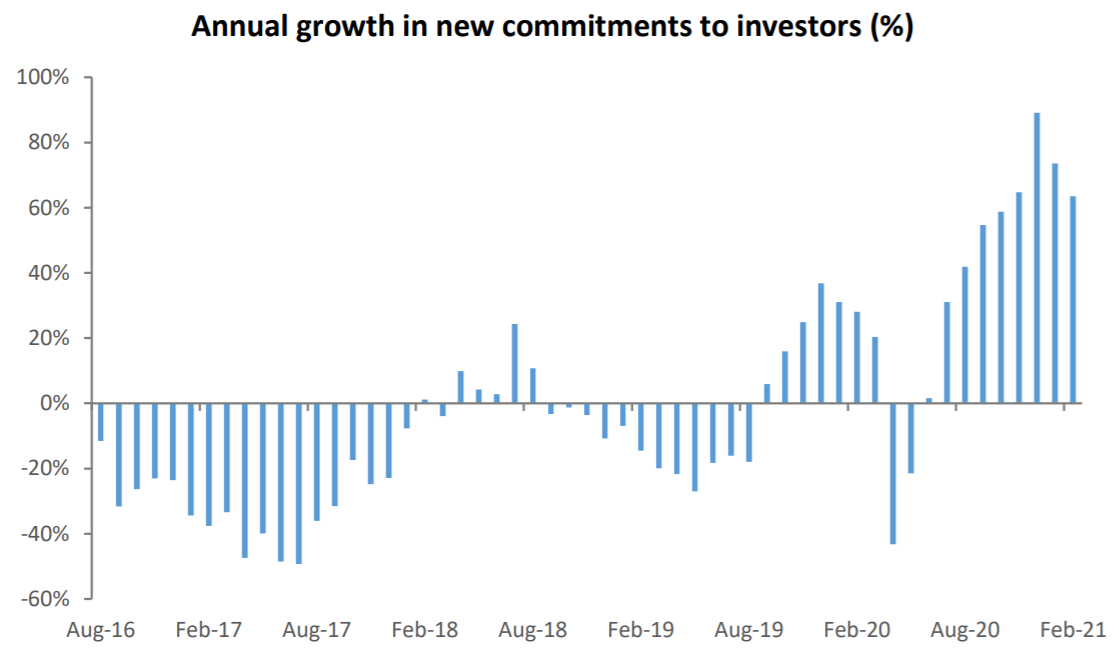

Investors again thoroughly outstripped the FHBs, by borrowing $1.856 billion in the month of February, representing 24.4% of the total.

These figures cover the last month of mortgage lending prior to official reintroduction of the RBNZ's loan to value ratio (LVR) restrictions on March 1.

The restrictions were removed as of May 1, 2020 in response to the Covid crisis with the intention that they be off for at least 12 months.

However, in November in response to an incendiary housing market the RBNZ announced the measures were going to be coming back. Many banks began applying restrictions from the time of the announcement.

Remember also that as of May 1 this year the restrictions for investors will be further tightened and they will need 40% deposits, up from the 30% they need at the moment.

And there are certainly early signs that the investor surge is beginning to tail off.

In January the investors took 26% share of the mortgage market and 25.4% in December.

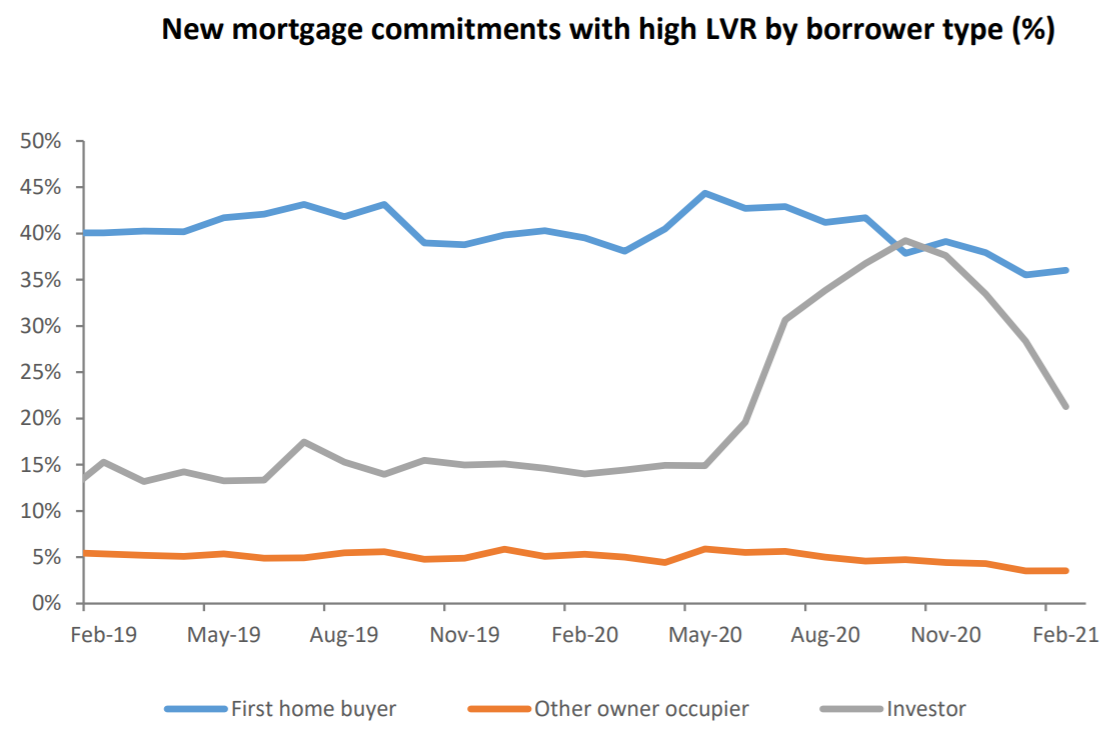

But much of the lending has been fuelled by high LVR borrowing (currently being defined for investors by the RBNZ as as loans for more than 70% of the value of the property).

In dollar terms the peak of this surge was November, when the investors borrowed $844 million worth of high LVR mortgages.

However, as the banks have started to adopt the tougher lending standards ahead of the official reintroduction of the LVR limits, these numbers have been coming down.

In February $395 million of new investor borrowing was at high LVRs, which represented 21.3% of all investor borrowing.

In January, of the $1.651 billion borrowed by investors $469 million of it was for high LVR mortgages. So, that $469 million represented 28.4% of the total borrowed by investors in January.

This compares with a percentage of 33.5% of high LVR borrowing by investors in December and 37.6% in November. In October, before the reintroduction of LVRs was announced, as much as 39.2% of the investor borrowing was on high LVRs.

So, the high LVR lending to investors has been dropping quickly from very high levels.

Separately, the RBNZ's figures highlighting interest-only and revolving credit borrowing show that of the $1.856 billion borrowed by investors in February, $756 million of it (40.7%) is either interest-only or revolving credit.

A proportion of about 40% of new lending to investors on interest-only or revolving credit is entirely typical and in fact the figure's often been higher than that; in October it was 45%.

The Government has of course made some noise about potentially stopping interest only lending for investors, but there were no decisions made on this in the housing policy announcement this week.

The RBNZ has been playing catch-up with the mortgage figures and various of its other statistics because of the data breach problems. It has now caught up with the mortgage figures.

84 Comments

It’ll fall off a cliff coming into winter.

Again... LOL

Yvil thinks this will never happen.

Yvil, you should buy now then... LOL

All should be ready for high volatility indeed and be ready to lose big if you enter the market at this point, a lot of uncertainty with recent changes and recent price changes might not settle long term.

I predict a huge drop in sales volume in March and April as potential buyers in all classes sit on their hands, followed by a rapid increase in property listings, followed by the inevitable rapid decline in selling price points.

Will be interesting to see. So far there's still hardly any stock.

A-Men sister!

I predict that investors who purchased before 27 March will find themselves in possession of a unique asset that gets special treatment for multiple years and will hold on to the asset at least until FY 2026 when the asset becomes the same as all the others. Why give up an asset that gets special treatment if you know that you will only ever be able to buy ones with poorer yield in the future?

Also incentive to build to rent just went down massively, implying a reduction in supply coming on stream in a couple of years (anything not already contracted will likely pause for a while- whilst waiting to see what the rules are like & because the resale value of new builds dropped massively due to buyers of what you may have acquired as a new build no longer being able to expense the interest - lower resale value = less incentive to build)

a unique asset that loses money.....a third of investors make a loss of on average $8k a year

the best advice for some investors if they need to panic...is to panic first and sell

sadr..."why give up an asset that gives you special treatment". Easy answers to that. Because you cannot afford to service the debt as you are now paying your fair share of tax, the RBNZ bans interest only loans and the Govt announces rent rises will be pegged to wage rises and interest rates begin rising.

Finally the Govt has seen sense and is going to take measures to ensure it is a level playing field for our FHBs. And about time too. No future PM would ever repeal this. Who would want that going down as their legacy; the PM who dashed the hopes and dreams of average kiwis trying to buy their own homes in order to protect the vested interests of greedy property investors.

Didn't incentive to build to rent just go up as you can still deduct interest?

Yes. I'm tracking TM listings by total results by region, broken down by price ranges. I know there are reports I could turn to, but I'm interested in real time. I have stated in previous months, long term holders of property have been selling off 2 beds for months but of course being bought up by newby landlords (as the stats in this article have confirmed) Much as the stockmarket plays out only slower, as selling a house not as easy as a mouse click

Is their a way to know how much is interest only loan by owner occupied and by investor respectively.

The RBNZ's C32 table, available through this link, gives this information. In the latest month 40.7% of new mortgage lending to investors was either interest only or revolving credit. The percentage figure is normally about 40% or even a bit higher.

Thanks David.

If government put restriction on interest only loan, will help in controlling speculative activity as it will deter many or may not be able to so easily buy as they do now with interest only loan.

Hi David, Any idea what the government is waiting to hear from rbnz by giving them 2 months, that is not already in public domain ( will RBNZ has more information) OR is it just delaying tactic by playing with time.

It's your latter point I think. As I said yesterday the Finance Minister and RBNZ Governor are clearly not on the same page regarding introduction of debt-to-income limits because the minister wants these to apply only to investors and Adrian Orr would prefer to apply them generally (if he were to use them). No reason that I can see why they couldn't ban interest only lending for investors now if they wanted to. Maybe the Government wants to see how the reaction to the canning of tax deductibility on interest for investors goes down. Be interesting to see what happens in May.

I suspect that is a very accurate assessment. Labour seem very keen to engineer a "soft-landing", so if the existing changes do not dampen house prices I suspect they will be willing to look at further measures.

I'll be a collapse in house prices is one of their worst fears, so don't want to go "hard and early" so to speak.

Winter is coming...

Not with interest rates so low, tax free capital gains, ridiculously high rents, ridiculously low term deposit interest rates, interest deductibility rules phased in over four years, and plenty of cashed up investors around. There won't be a fall in prices, I think at worst consolidation in Auckland/Wellington and slightly smaller gains elsewhere.

Cross your fingers ah and make sure you have a good real estate accountant on hand!

This sounds like the drivel coming out of bank economists. The way they talk, you’d think they want this ponzi to continue.

dago

"This sounds like the drivel coming out of bank economists"?

What is this "drivel" you refer to?

You referring to RBNZ data in this report????

Tax free capital.gains???

First hint of downward movement and the DGMs are back their droves. You were saying the same thing 12 months ago and have been awfully quiet ever since.

The only DGM these days seem to be property investors whinging about interest deductions and ‘how am I going to get ahead of other people now’ comments

B727...I saw more property investors in the media crying and whining in the last 24 hours than whining DGMs over the last 12 months.

If, as Ardern stated that they will not let house prices drop then the the best we can hope for is that they will remain constant. That being the case they only way that we will get anywhere near affordability is through wage rises and inflation. If we say that this is about 2% per year then it will take 34 years for real prices to halve from their current absolutely ridiculous current price. Given that the average house price for a 3 bedroom house in Auckland is well north of $1 million you will have to wait 34 years for it to get down to the equivalent of $500,000. Even at this price a lot of people will struggle to purchase a home. The message is clear. If you want to own your own home; get out of New Zealand.

Ardern SAYS she doesn't want house prices to drop even though she knows they will. That's why there are rumours of her resigning - to plant the seeds this early on that an early exit is inevitable. Once the market falls by more than 20%, she'll do a John Key and resign with a year left into her term, stepping away due to pressures and stress of leading the country through covid and cite "spending more time with the family" as a positive spin. Grant Robertson will have 1 year to be Prime Minister (1st openly gay PM of NZ?) and bank on the goodwill gained from covid to aim for Labour re-elected against new National leader Christopher Luxon.

Even if it falls by 20%, will still be appox 20% more on yearly basis (after 20% fall) so...house price has not fallen and is what Jacinda said.

To avoid housing ponzi jumping another leap from here, important to calm down FOMO, which is only possible with fall in prices to kill FOMO - No other way. Earlier Jacinda Arden understand, better it is.

RM, great imagination, you know there are better websites than Interest for fictional aficionados

Sure makes better reading than "I hate FHB they gotta stop eating smashed avo and whinging and must shut it and pay moi mortgage instead...UGG! It was hard in moi day! I'm busy counting muh cupitual gaiinzz, Im going to be effluent as and boi 25 properties"

You got the accent perfect! I needed a smile this morning.

One is called OneRoof

Have you noticed Nicola Willis being slowly but gently wheeled out by Nats? Potential surrogate Jacinda?

Yes and head off to London and Sydney to buy one of those 3 beds much more affordable there.

But apparently it’s all going to be down by what was it 20% by the end of the year according to all the geniuses on here oh wait no actually it was 30%.

It was going down in 2020 *without the increased Government and Reserve Bank support that was provided*.

It's the difference between a prediction based on what would have happened without additional stimulus and the dropping of LVR's, and what did happen once they took the action they did.

That was everywhere in the world Amigo and entirely because of covid.

Our OCR was at a pitifully low 1% before anyone had even heard of COVID-19.

You mock, but as I've said before, my sister in-laws purchased a wonderful 3 bedroom detached in a great part of London for about NZ $1.45mil. Drive way, double glazing, huge garden, outhouse, lovely and modern. You couldn't get anything like in for the money in Wellington or Auckland anymore. Plus her wages are double what they would be here.

Where exactly in London? I know it very well having lived there a long time.

And what are you taking about 1.5 buys you an excellent place here.

Hillingdon.

$1.5mil here does indeed. Like for like though, I don't think you could get such a good house for the same cash here. Plus as I say, considerable higher wages. And besides, if you're trapped somewhere unable to buy, why not live somewhere interesting? I just don't think other places being expensive is a reason to halt a Kiwi brain drain (as someone planning their exit).

I had to look up Hillingdon as it’s 30kms NW from the centre. So the equivalent of living in Kumeu.

You can get an excellent house in Auckland only 10kms from the city for the same money so I think your comparison has highlighted if anything that London is a lot harder to get the equivalent which isn’t a surprise.

England is a hell hole, we only just got out in time and that was back in 1974. A few weeks there in 1990 on my OE was enough. You need ridiculous amounts of money to have a "Lifestyle" there like my cousins and even then they were overseas at least twice a year on holiday.

The new legislation will deter new investors / speculators no doubt hopefully meaning there is more opportunity at auctions etc for FHB. Those investors already entrenched will either be holding on as the Brightline effect on equity far outweighs the gradual erosion of tax reduction strategies. I wonder if we'll see a drop in volumes but a stalemate on price change. Buyers will rightly speculate that there may well be a change coming in their favour, while investors sit tight for a while as the net pressure is actually to stay in due to Brightline. In the background we now have forecasters agreeing that the OCR will stay lower for longer. There may also be more FHB's coming back to the market having being fatigued by failed attempts now the landscape is perhaps on the change. Lots of new factors both on demand but also supply. Interesting times.

For investors, I think that the best advice is to take the cash and run. Sitting around pondering whether this or that is going to happen really just boils down to common human frailty of rationalizing in favour of the status quo and doing nothing. More often than not things do not go they way that you hope and this is particularly so given that the current situation is just crazy and the government has decided to unwind it. (Think about all the Jews who, when they could have got out, remained in Germany thinking that somehow they would not be affected by what was clearly going on all around them.)

Ask yourself this. Can you see the current circus carrying on much longer? Even if the government does nothing the market is likely to collapse under it's own weight. (I suspect that this probability is a big part of why the government acted.)

Investors are incentivised to hold as long as possible (up to FY 2026) due to bright line and special tax treatment of property bought before 27 March that they will never be able to get again. Also there is a chance a future government will reverse these changes, which when added to the existing incentives to hold will likely really really thin the volumes of property coming to market.

Paying tax on a profit is far better than no tax on a big loss that follows you regardless.

Personally, provided everything is worked out correctly, the more tax that I pay, the happier I am.

They ain’t stupid, most of them also own investment properties. This will slow the market down a bit for now ( which isn’t a bad thing consider how crazy things are)

Once things settle a bit they will announce they are not going to go ahead with it or they will keep it running it for a couple of years and then reverse it.

The potential impact is quite significant, a client who runs a painting company had 7 quote requests cancelled since yesterday’s announcement and this is just one industry. Imagine the flow on effect, everyone will suffer down the line.

Yes. If highly leveraged, particularly on a recent purchase, if there is any capital gains to be had, surrendering the tax on them is far, far better than being unable to afford the mortgage due to reliance/establishing the yield based on the now 'old' tax rules.

As in any ponzi scheme, the last to enter the fray are the most at risk of losing their 'stake'. When that 'stake' is a highly leveraged, interest-only loan - exit sooner rather than later. Otherwise the debt on an asset you no longer own will follow you.

I suspect the banks will be reviewing the numbers on interest-only investor loans and taking a pro-active approach to contacting these new-comer customers, if there are a lot of them.

I agree Chirs

Regarding the possible collapse I went and had a look at the bank dashboards....interesting to see that westpac bad loans have more than doubled in a year...its not a good trend

We are in a democracy. If there's votes in it, then the hammering of the landlording class will gather pace. keep messaging your local MP.

This is no news for if house price rose by 10% in just a month in February, it is obvious that activity was high, which will require mortage, which too will be high.

Banks are leading these enormous unprecedented sums.....and Banks are sounding increasing warnings about the housing market.

It all seems a bit schizophrenic. It's like an addict crying out for help while at the same time continuing to indulge in the same behaviour. No bail-outs if it all goes pear shaped!!!!

The 'bail-in' method (OBR) already exists. Savers are trapped, i.e., try asking for a million in cash :-). I suppose you could get a bank cheque and put that under the mattress?

Listen if interested

https://www.newstalkzb.co.nz/on-air/simon-barnett-and-phil-gifford-afte…

Wow - great to hear a professional economist not wedded to ideology and instead telling it like it is. Thanks for the link!

Yes, superb. Very fair and balanced interviewers too!!!

At this rate, nobody will sell and will just sit on their assets (since they have nowhere else to put their capital/money). Supply will again dry up some more. # of buyers continue to build up. Price will continue to go up.

The only difference is, the FHB can now buy houses but the houses are still in the middle of nowhere because that's all they can really afford. FHB will realize they still need to rent to get into a good school zone for their kids (i.e. they still can't afford places like Remuera, Bucklands Beach, Epsom, etc.). But unfortunately now rent prices will go up as investors want to make back the difference caused by the Govt.

Not sure how much blood is left to be sucked out of the 'renters must pay more rent to cover my losses' stone. The productive, income generation economy can only do so much to prop up a bad investment with negative cash flows before it just becomes a bad investment that needs to be sold. The question becomes, do you do that before other people and get out with maximum capital, or do others beat you to the exit.

There's no reason to think property prices will have any meaningful crash as there is a solid price floor.

What people should be concerned about is the rest of the economy being run into ground by people who should never be anywhere near managing a business, much to say a national economy.

I guess this is what happens when you put a socialist back-bencher communication specialist to head the country and a unproven marketing guy to run the economy.

The recent price spike can be an indicator of volatility, all who got in should account for this and be ready for either big gains or losses.

That chart says plenty about what those specufestor parasites have been up to over the last year.

I’m disappointed that Jacinda lied about introducing the capital gains tax.

There was already a Bright Line thingamy in place, they’ve just extended it....

Jacinda is tired, she did this just to say “please don’t vote for me again, I want out”

I am indeed pretty happy she lied about it. It is the fair thing to do.

It's just income tax, paid at the appropriate income tax level.

You mean the bright line test that was initially created under National?

Quite interesting to review some of the players at the time and the introduction of that bright line test.

https://www.parliament.nz/en/pb/hansard-debates/rhr/document/51HansD_20…

Unless the 'investors' purchased in the last three months they will be up c.10-20% on purchase price. No motivation to sell and can easily hold out to next election and vote in party who will repeal. The property party continues. Unfortunate for all of the commenters on this website who talked themselves out of purchasing over the past 2 years. Those on the outside have no one to blame but themselves.

Not everyone had the option to buy 2 years ago.

B727...bad news old chap. No party could ever repeal this. I mean how could they live with themselves if they did? Who would ever want to be remembered as the person who smashed the hopes and dreams of young NZers in order to ensure the playing field remains slanted towards greedy investors who have been allowed to game the system for years.

I guess there could be an argument made that property investment is a real business. But then you also argue that dealing meth is a real business too.

karl

Twelve months ago (to the day) there was tremendous glee at the prospect of 30 to 50% falls from a number of posters (who I can name) that are currently moaning about affordability issues.

I did not see an empathy by these posters for the then FHB who had recently bought and were being bombard with scaremongering comments of 30 to 50% fall as well as facing the uncertainties of employment.

I have long posted about the affordability as an issue for FHB and hopefully it will now improve; however, please don't go down the guilt trip road for those who have property - whether FHB or investors.

Nowhere in the discussion over the past few days have I seen any mention or empathy shown that the Governments has done little to address housing supply in the short term to cater for the numerous homeless - such as the over 1% of the residents in Hawkes Bay currently living in motels. There are varied opinions, but one is that property investors have been essential in providing rental accommodation albeit insufficient and no empathy has been shown regarding that but rather glee that they are being kicked in the teeth.

One quote 12 months ago was "Anyone buying a house now is officially stooped (sic)". So some made decisions which were wrong and they need to live with those. Affordability is improving and I hope that those who were never in a position to do so, will soon be able.

Nothing we didn't know already, stupid money rushing into buying before the introduction of new LVR restrictions, will be interesting to see the picture from March and in the next few months.

March will also be the smashing record, .. until the authority really implemented DTI, real CullenCGT.. right now they're still toying with words.. observe the knee jerk market reactions.. change to slow down a bit? then the DTI or plan of that interest loan only will be out of the door, Another 7 days left? - All the established investors (mostly politicians, local body Councillors, RBNZ staff & other wealthy by papers).. will buy in vengeance. Most of NZ is too much below average intelligent to openly admit that NZ economy is just that = housing economy.

Adrian Orr warned the banks to prepare their systems for (possible) negative interest rates a while ago. Therefore, in the very near future, can we expect him to ask the banks to prepare for the removal of all interest only loans from their books and prepare the system to allow only for interest and principle loans with a maximum term of 25 years by 1 May?

More likely they'll allow terms of 40 years.

Retired 5 years ago so where to invest my hard earned retirement savings - property or shares?? Went with solid blue chip shares and the returns from these investments would be considerably ahead than if I had invested in property at the same time. Also reliable dividends and no worries about all the costs involved in owning property, which can add up over time. Also, shares are very liquid, sell today and money in the bank in a couple of days less a small amount of brokerage, not the ravenous fee's that real estate firms charge.

Great - and at the same time not pricing a FHB out of home ownership by buying a rental. Benefits of financial return, liquidity, and social conscience.

Good on you.

I always had a deeply diversified investment portfolio (with the exclusion of "investment" housing, for ethical reasons), and the only regret I have, after several years, is that I did not invest more aggressively in shares when I could do so.

Buyers in this market are in a casino on margin. Cheered on by the banks and deaf to common sense and history.

A tweet to Choe Swarbrick:

"@_chloeswarbrick is painting us all as millionaires. We don't make any moeny from the homes we own".

Her response:

"To take this on face value: If you're not making 'any money' from something (property investing) and that something is causing immense inequality, deprivation, stress and homelessness (the housing crisis), maybe you stop doing the something?"

God help us.

Some folk commenting seem to believe that NZ and Auckland housing prices can only go up.

They have the last 20 years on their side of course

However, prices did not fallen USA either, for a lot longer than 20 years, up to 2006.

Then they did.

Leverage is a dangerous game and some investors just found out that things are NOT a one way bet.

The next 2-3 months will reveal how burned they have been.

Good news fo rFHB at auctions however.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.