Kiwibank economists are now seeing a "risk" of three Reserve Bank interest rate hikes next year, which would take the Official Cash Rate to 1% by the end of 2022.

The RBNZ in its latest Monetary Policy Statement last week reintroduced its estimates of the future levels of the OCR and economists and financial markets were surprised at the levels, which showed the OCR hitting 1.75% by mid-2024, compared with just 0.25% as it is now.

"Financial markets were already sensitive to anything deemed hawkish," the Kiwibank economists said.

"And last week's statement only fuelled the fire in financial markets. The Kiwi dollar and wholesale interest rates were propelled higher. We see further upward pressure in coming months.

"As we noted last week, 80% of the collective mortgage book across the industry will have the opportunity to refix in the coming 6-12 months. That's a huge chunk of refixing as we head into a tightening cycle. We may see a self-fulfilling pop in wholesale interest rates as banks cover refixing flows."

While the RBNZ's new 'OCR track' suggests the central bank's first hike of interest rates will come in the second half of next year, financial markets are already anticipating the first rise could well be in May 2022. Kiwibank economists are in this camp.

"Of course, a move in May means a follow up move in August and introduces the risk of three hikes to 1% next year," the economists say.

"That's the risk we believe is more likely to take the market from here. And we'd expect to see all interest rates rising in response."

(The writer adds, just as a quick example, the average-sized new mortgage in April, according to RBNZ stats, was $336,000. Assuming a mortgage of this size and a current interest rate of 2.25% on a 30-year term, and assuming all 75 basis points of OCR rises were fed through to mortgage rates (IE going to 3%), this would add $163 to each monthly payment and nearly $50,000 to interest and fees costs through the life of the loan. These figures are produced through the interest.co.nz mortgage calculator.)

The Kiwibank economists say we need to keep in mind that the OCR track "is not made of concrete" and the projections are conditional on several assumptions.

"...But that means there's potential for rate hikes to come sooner rather than later. The expected timing around rate hikes will be influenced by how the market interprets economic data and covid developments over the coming months. If the data surprises on the upside, expectations of rate hikes will naturally be brought forward. In the same way, downside data surprises or future community outbreaks may extend the current OCR on-hold stance."

They say the first test comes June 17, with release of the March quarter GDP figures. The RBNZ is expecting a -0.6% figure for the quarter, which would technically put New Zealand into recession again (two negative quarters in a row).

"But activity appears to have held up well at the start of 2021 all things considered," the economists say.

"The Reserve Bank's prediction of a double dip recession may prove too bearish."

BNZ head of research Stephen Toplis is another economist seeing a likely better outcome from the March quarter GDP figures than the Reserve Bank. He's forecasting a 0.0% (IE flat) outcome.

"...There is a very good chance the data actually surprises in a manner that adds more weight to the need to reduce the current pace of stimulus," he says.

He also notes that the latest ANZ Business Outlook Survey supports the view of the BNZ economists that the demand for labour is exceeding potential supply and inflationary pressures are rising at an accelerating rate.

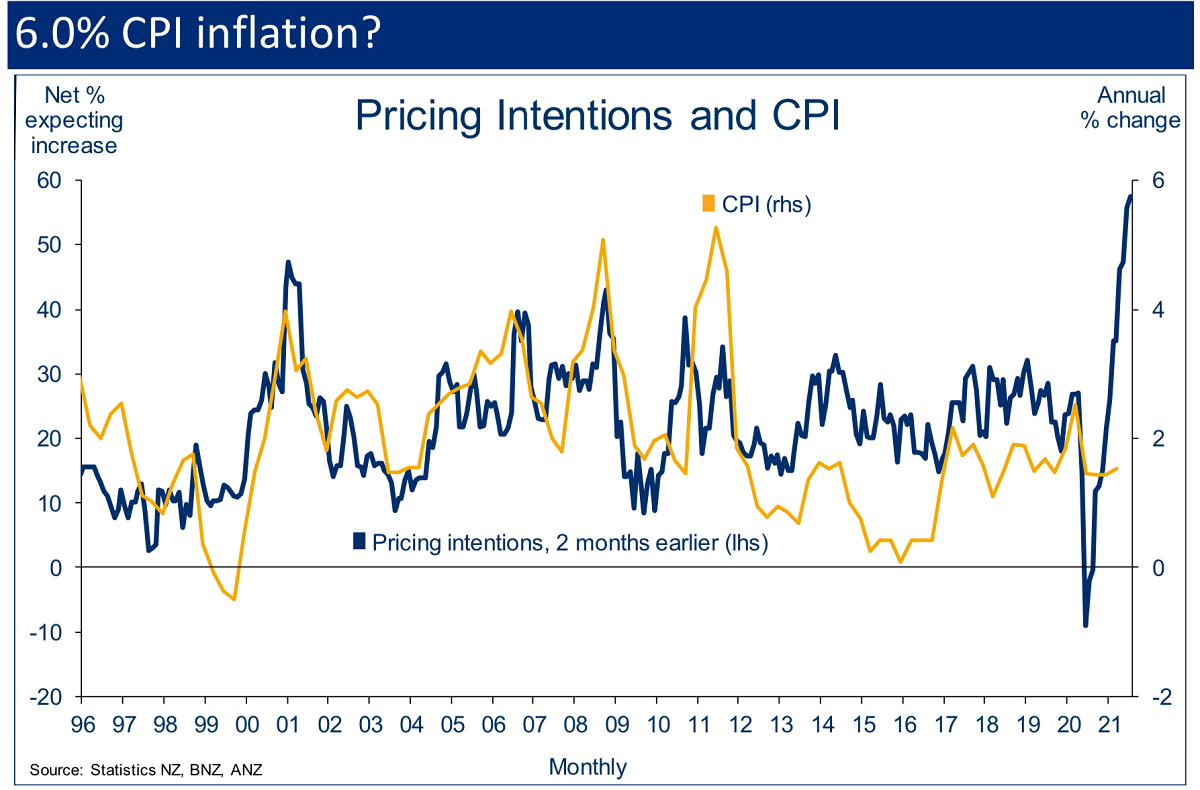

"A net 57.4% of businesses intend to raise selling prices. By past observation this would suggest annual CPI inflation rising to almost 6.0%!

"We are not forecasting this but the direction of pressure and risk is clear. The reading would have been markedly higher had it not been for a relatively conservative agriculture sector. A net 66.1% of retailers intend raising prices, a net 72.1% of manufacturers and an unprecedented net 80% of builders. Inflation expectations also rose to 2.22%, its highest reading since November 2018.

"Everything about the survey supports our long-held view that the cash rate is headed higher next year and, potentially, sooner and by more than many folk expect," Toplis says.

ASB senior economist Jane Turner also noted the results from the latest ANZ survey.

"The Covid-19 pandemic has disrupted global supply chains, seen shipping costs surge. The NZ border restrictions have also disrupted the labour market," she says

"For the first time in over a decade, there is genuine concern that current supply shocks and price movements could trigger a sustained lift in inflation pressure.

"Only time will tell how much of the lift in prices over 2021 will be transitory and how much will become more persistent. A strong demand environment (as indicated by business sentiment) suggests businesses should be able to pass on higher costs to consumers, which in turn points to that some of the inflation could become more persistent.

"The Q2 CPI inflation read, in July, will be closely watched to see how much price pressure is coming through. Wage growth is another key area to watch going forward."

ASB economists are also forecasting a May 2022 OCR hike.

53 Comments

There are no greater crooks and thieves in the world than central bankers.

What has always fascinated me is how few people appreciate the most powerful economic body in the world, the Fed, is run privately for the key purpose of protecting banks (originally from bank runs but now... just protecting banks).

Yes. Your own interests are low on the priority of the Fed and other organizations like RBNZ.

Wages unlikely to rise more than inflation.

That means fall in standards of living and disposable income.

If rates rise too, that is a double combo to contend with.

As borrowers have been handed sweeties to incentivise further borrowing, since 2014, now the sweeties will be removed and visit to dentist pencilled in. Reality arriveth (the broken clock etc...)

Agreed re wages, possibly worse than inflation if immigration comes back on line.

Agreed.

If rates rise? "Over 10 years the average household rates bill will go up from $2810 to $4018 and the average water bill from $1069 to $2261. That's an overall average increase of 62 per cent in council costs for a typical Auckland household" and "Wellington City councillors have agreed on their Long-Term Plan, a budget of infrastructure, resulting in a 13.5 per cent rates rise for the incoming year." and Hamilton "A 3.8% average increase for existing ratepayers in 2020/21" etc...

Not sure I can see interest rates rising much at all, far too much leverage, they might, might reach 1% sometime 2024 but they won't be able to increase much from there surely - a medium house in Otara will be $2m by then right? :)

Fake news.

Speculation.

Trying to talk down the market.

Speculators have called the RB bluff. There is no tapering of borrowing (mortgages). There will be no rate rise. The ponzi must continue.

RB doing what they do best. Jawboning. If it ain't happening overseas it ain't happening in little 'ol NZ.

Amen

Interesting to see in the NBR today there was a column blasting the RB for going out of its lane on various issues (e.g. corporate social responsibility). Their jawboning is vast indeed

LOL

A CPI increase to 6%. This would put the RBNZ into a corner. i guess they could use their full employment mandate to justify not raising interest rates while claiming the CPI increase is temporary.

I can see the phrases "pent up inflation" or "the inflation we need" or "years of below target inflation figures" or "remove that from the CPI" being bandied around in the near future... any reason to keep rates low. It's a grand game of "who will blink first" between central banks now.

Here we go.

Brock and Rosenstein slagging off - I'm not sure whether it is either an overinflated false sense of their ability or simply their ignorance.

Anyone who makes sound financial decisions will read a variety of opinions of value and come to their own conclusions. When bank economists produce statements such as this I would be giving it serious consideration.

The reality is that when the common opinion amongst the RBNZ and bank economists - who have an influence on OCR and mortgage rates - that the OCR is likely to have upside, and I had a mortgage or other debt I would be listening very carefully and noting it.

Brock and Rosenstein totally ridiculous comments. Best advice to you both - don't bother wasting your time reading similar articles from bank economists.

Anyone who makes sound financial decisions will read a variety of opinions of value and come to their own conclusions. When bank economists produce statements such as this I would be giving it serious consideration.

Agreed. But bank economists are not seers nor are they wizards. They're employees and they're employed to promote the interests of their employer through a veneer of neutrality.

J.C.

Not necessarily so.

Pre GFC when I had a few mortgages on investment properties, I recall Alexander was chief economist of BNZ. His weekly commentaries had a section called "If I was a borrower what would I do?". I followed his comments, breaking at appropriate times and there is no question I save many, many thousands of dollars.

A few weeks ago I posted two or three time that there was likely up side to interest rates and that the then BNZ five year rate of 2.99% was both attractive and would not last. It didn't last . . . now those looking longer term are paying higher interest rates.

I don't claim to be a clairvoyant, nor was I making baseless assertions. It came from forming a view after reading a number of bank reports and their comment were not in their self interest.

Quite simply; sorry son, you are talking a lot of bollocks.

It is about time some of the conspiracy theorists on this site got a little bit real. I find it amusing that there have been 50,000 FHB (RBNZ) who have got into their own homes in the past year. Those on this site who seem to wanting the same but are either besotted with conspiracy theories (such as you present here) or simply moaning, or slagging-off, or blame shifting really need to start to question themselves as to why they aren't one of those 50,000.

No, its not easy for FHB, in fact getting a suitable deposit is a challenge . . . but simply being a conspiracy theorist, slagging, moaning or blame shifting achieves nothing.

Perhaps Alexander should have been a mortgage advisor.

Anyway, the idea that banks are looking after your interests is specious. At the end of the day, they're evaluated on what they deliver to the bottom line. Bank economists are prominent in the media for that reason. They're not there to scare the sheeple.

But what's this conspiracy theory you speak of? Are you suggesting that bank economists are somehow all-knowing? Or are you perhaps suggesting that the mouthpieces of banks should dictate the behavior of the general public?

What, exactly, is "ridiculous" about my comment Printer2?

Do you know of greater crooks and thieves than the central bankers looking the other way while their inflationary policies rob the entire population of workers and savers of their purchasing power to the tune of several percent per annum?

Would like to share with us who you think the greater crooks and thieves are?

Brock

If you don't understand what is ridiculous about your comment, it clearly illustrates what your major problem is.

If you want to be a FHB, ask yourself why aren't you one of the 50,000 who moved into their homes in the past year.

If you are serious, you need to start getting over the bollocks and prejudices coming through in your conspiracy theories such as that posted. Pull your head out of the sand, read, consider, and start thinking and acting constructively.

A potential and serious FHB would be looking at this article and be considering the implications . . . . not bollocking around with ridiculous conspiracy theories.

50000 FHBs who may possibly have negative equity and a crippling mortgage.

Burni

How often does it have to be said:

The ability to service one’s mortgage is more important than short term market fluctuations.

This is from one who has experienced three falls in the housing market.

A property - either a home or investment property - is long term, next mortgage payment short term.

The issue is a confidence to service one’s mortgage . . . and the bank in their vested interest has truely considered that.

And a not insignificant number probably got help from 'the bank of mum and dad' . Many don't have that luck.

Hi Printer2,

You are very quick to judge and very slow on the uptake. Why would I need to ask myself that, when I've repeatedly said that I relocated to New Zealand only a few months ago?

Are you trying to win the clown of the year award saying that inflation is a conspiracy theory on an article about interest rates and inflation?

Brock

Your rambling is not making sense.

So what if you have just returned to NZ; your initial comment is still ridiculous conspiracy theory.

You asked "If you want to be a FHB, ask yourself why aren't you one of the 50,000 who moved into their homes in the past year."

So, that's uhh... the answer... to your question...

My initial comment that central bankers are the greatest crooks and thieves [because they rob us with inflation and look the other way]?

Total whacko conspiracy theory stuff? Inflation is made up by the lizard people right?

I'm starting to wonder if your username contains your IQ.

B L,

I'm with Printer 8( not 2). Your comments are absurd. I don't know where you relocated from, but in doing so you have raised the IQ of one country and lowered it here.

You have of course no evidence to support your conspiracy theories and i wonder whether you have read The Creature from Jekyll Island by G Edward Griffin. In it, he proposes that the Fed is indeed a vast conspiracy. You would love it. Mind you, he supports many other conspiracy theories and also firmly believes that Noah's Ark is located in Turkey.

How boring. Imagine repeating that sad little kiwi IQ comment again..... yawn.

P8. I had you for a rational person there. In what parallel universe can an economic system that exists on ever expanding borrowing, support higher costs of servicing those loans? This isn't rocket surgery. How will they raise rates?

Rosenstein

How will RBNZ and banks raise interest rates? Quite likely and quiet easily.

The important consideration for one on this site, is how likely are rate rises, when and by how much are they likely to rise, and what are the likely implications for me?

If I had a large mortgage in answer to those question I would be asking some key questions: should I be looking to fix longer term, do I need to look to pay down (especially high interest) debt, and should I start looking at discretionary spending.

The last thing I would be doing is rubbishing reports by bank economists.

As to the wider economic situation; when out sailing there is nothing I can do about the weather - I can only make decisions to make the best of those conditions. Criticising the weather, or coming up with conspiracy theories, or burying my head aren’t productive.

I'm not critiquing the weather, I'm critiquing the weather forecast. I am a voice for rate rises being 'unlikely'. Not conspiracy. I just look at what they're defending, which are asset prices and consumption and furthermore I think they know rate rises are implausible. As for deriding bank economists: I can't think of a more socially acceptable class of parasite. Maybe career politician.

If I had a large mortgage in answer to those question I would be asking some key questions: should I be looking to fix longer term, do I need to look to pay down (especially high interest) debt, and should I start looking at discretionary spending.

Here is the problem. If people start looking at discretionary spending, then the S really starts to HTF. It's really discretionary spending that makes you reach for the 'nice to have' products on the supermarket shelf. NZ is flooded with craft and niche products and services. These are also the businesses that can go under relatively quickly and trigger an avalanche. That whole sector of the economy is on tenterhooks right now.

J.C.

I agree with you.

While nothing is certain, I see RBNZ being reasonably conservative on raising rates - both slowly and testing by little steps.

The rationale is the reality is that both discretionary spending and perceived (note “perceived”) wealth (including home) have significant influence on the economy. RBNZ isn’t going to take action to upset that.

Further to that, while many on this site wish otherwise, within RBNZ’s ability, they will not be wanting considerable correction in house prices. Yes, some downside in the market possible especially in the short term, but outlook for a flattish market in the medium to longer term. Statements by Treasury, Robertson and RBNZ seem to support that.

From comments coming out from RBNZ and banks is that FHB need to consider is a likely relative stability in house market but increasing mortgage interest rates. This situation along with Government’s action means that the party with considerable capital gains is well and truly over for speculators.

Serviceability as a rule of thumb is about 6% for most NZ banks at the moment so I think we will be some time before servicing is the issue. Should someone experience a problem in servicing at this level there is likely to be cascade of defaults. Times change between bank funding and interest rate rises, families can be started, illnesses encountered, divorces initiated. Many normal life events can make servicing even at slightly increased levels very hard.

I actually think the reason they can't raise interest rates (on top of the actions already carried out) is the effect it will have on the property market pricing, particularly as supply seems to be improving and immigration is slower (with the Aus attraction effect as well as border closures).

JAO

A post with some sense.

Yes, banks have applied a stress test of around 6% (and considered many other factors) when lending.

However that stress level is breaking point - the point at which one goes under (i.e. likely a gone burger forced sale).

However, as interest rates rise, one should expect quality of life diminishes as one cuts back on discretionary spending.

Will RBNZ and banks raise interest rates indiscriminately and rapidly? Personally I don’t think so; the reason being they don’t want to see a collapse in the housing market for the same reason for their actions during both the GFC and Covid. While they will be endeavouring to avoid that situation, if I had a mortgage or a potential FHB I would be considering reports such as this and the the implication that mortgage repayments are going to be getting a bit tougher.

The last thing I would be doing is rubbishing the report or coming up with conspiracy theories.

What's wrong with having an opinion different from those of bank economists and RBNZ economists, especially when said economists have been very wrong on many occasions. Not to mention their vested interests.

Skepticism of the RBNZ, I believe, is justified.

Printer8 I am sure there are plenty of property investor forums where you can go for an echo chamber to reinforce confirmation bias.

I for one appreciate the variety of perspectives on offer here, including the ones I strongly disagree with.

Buisnesses may increase costs but will the market accept them long term? My best guess is no. Way too many deflationary forces at play. Ive heard it all before. Rates may blip up then they will drop to new lows.

exactly right

you wont outrun deflationary pressures

consumers only have so much to splash round .. and its dwindling

Steel up 50% in 6 months while stimulus projects ramping up. They have no choice but to accept them for commited projects. Then try and recoup them from future jobs for the ones that were fixed price or variations. Be interesting to see what "short term" means. 1 year, 2, 3 ... 5? I think it's a bump up hard and fast and be sticky on the way down.

Not happening.

OCR of 1% is a non-event, just puts it back to where it was Feb last year

Not going to effect anyones ability to pay their mortgage as they are stress tested at 5+%, but it will have an effect on disposable income and consumption

The situation can change, they passed the stress test before doesn't mean they can pass it now.

Cost of living increases can eat into that calculus

"A net 57.4% of businesses intend to raise selling prices. By past observation this would suggest annual CPI inflation rising to almost 6.0%! "We are not forecasting this but the direction of pressure and risk is clear.

One year NZ Government TBills tendered today at ~0.2775% are not forecasting this either.

Talk of acute financial repression is not priced in NZ financial markets - are all the pro bond traders simple?

Back of an envelope 10 yr NZ government breakeven inflation yield is ~1.851% - 10 year nominal yield 1.751% +~ 0.1%, (3.0% 20-09-30 linker yield)

One year is not the window though? I know a couple of pro bond traders, clever clogs both.

addressed above.

Needs to be 1% by the end of this year...

The underlying theme, mostly unpronounced, of those who have trumpeted price, price , price as what the market is, on here, is this: that price rises are good and prices in th medium to long term always go up (despite fact that figs recorded only go back to 1992). Others (majority) theme on here, including me, is that the market has to include what is affordable and rational. Which implies that prices are too high and should come down to be rational. Not a little self-interest or satisfaction seems to inform the minority group where the majority group is just labelled DGM. This division will not resolve I suspect. However, clearly the cycle of interest rates and inflation has turned and rates cannot fall further and hence the 7 year sweetie giving is over. When the economy fails to return the dream of 3% growth (nominal or real?) we will see how prices and sales do into a deleveraging debt economy where people realise they overpaid at least $100k relative to their strapped means. That time is rapidly approaching.

Won't happen. I wish it would. But it won't as NZ is now addicted to debt.

As someone said in another article...

QE Hotel California... you can never leave.

Over the short-term the Reserve Bank of New Zealand has many options but in the long term it has only one. That's why he trajectory of the reserve bank has been to promote credit growth so vigorously.

House prices will never be managed back to 3x to 4x income that they where 15-20 years ago. 10x+ will be the new reality by the time our economy has recovered. Next time they will go even higher.

There is no inflation, just opportunistic suppliers jumping on a supply chain squeeze that wont last 6 months.

Ah, some background noise.

With the exception of mainly African countries, global population is not only ageing but declining leading to declining demand for almost anything except elderly care and funerals. In NZ, in the absence of a reinstitution of open the gates immigration, our population is declning too for, as reported on this site, we are losing over 5,000 education and work visa holders a month to which can be added the usual Brian drain to Australia and elsewhere.

This along with the growing unpopularity or high cost of having children. NZ's birthrate having fallen to about 1.6 births per woman.

Saturated product markets. When Sony was one of my main clients in Japan in the late 2000s and early 2100s there was a long line of graduates waiting to get in and business was booming. Now my son, who works in the same building in Shinangawa where his daddy used to work has been looking for a job in a different industry. The came is true in many other markets - think automobiles.

The New Cold War and the Thucydides Trap - bd for trade and markets.

Sorry, but any economic forecasts provided by Kiwibank are regarded by me with some skepticism these days. I recall a lengthy interview with Kiwibank's Chief Economist Jarrod Kerr on this very platform about a year ago when he talked about the soon-to-come negative OCRs and how the value of the NZ dollar would be one of principal victims as a result. Well, we're still waiting Jarrod.

Have you drunk the Kool Aid ? ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.