‘Move along, there’s nothing to see here’ appears to be the attitude of some of the country’s finance bigwigs, when asked about New Zealand’s high level of household debt.

Housing debt hit a record $231 billion in December, while consumer credit hit $16 billion. Together, total household debt is up 8.7% year-on-year.

While debt grew at faster rates during the housing boom 10 years ago, the value of the debt was about a third lower than it is now.

Yet delivering his first speech as Finance Minister on Thursday, Steven Joyce didn’t acknowledge this as a risk threatening the economy.

“Both the Reserve Bank and Treasury have highlighted that unusually, the current risks to New Zealand’s continued economic expansion are almost exclusively international,” he said, before proceeding to affirm New Zealand’s commitment to free trade despite US President Donald Trump’s push for protectionism.

Roger Kerr: ‘I wouldn’t overrate that as a big risk’

Asked during a panel discussion at PwC’s CEO Survey breakfast on Friday whether he saw high household debt as a threat to the New Zealand economy, PwC partner Roger Kerr said: “In Australia, as well as New Zealand, if interest rates went up one or two percent, there might be a bit of an issue.

"The Reserve Bank is concerned about that and is doing good reporting and having good interaction with the banks about that.”

He said the pinch would really be felt if asset values came down at the same time as interest rates rose.

While the Official Cash Rate is expected to remain on hold for the year, banks have started hiking their mortgage rates, largely due to increased funding costs.

House prices have also been cooling off - the national median selling price falling to $490,000 in January from $516,000 in December and its peak of $520,000 in November last year, according to the Real Estate Institute of New Zealand. In Auckland, the median price declined to $805,000 from $840,000 in December and $851,944 in November.

While fewer people are expecting house prices to keep rising, the majority believe they'll continue trending up, according to ASB's latest Housing Confidence Survey. It found only 10% of survey respondents expect prices to fall in the next year.

Kerr said: “I wouldn’t overrate that as a big risk to the New Zealand [economy] right now. I don’t think short term interest rates will go up for another year, or year and a half. Let’s hope the housing market has a soft landing, not a hard landing.”

Anthony Healy: It’s a 'medium-term' issue

BNZ CEO Anthony Healy then went on to say: “Interest rates go up and go down. Asset prices go up and go down. So at some point, we’re going to face more challenging times around interest rates and asset values.”

With a house price to income ratio of 10:1, Healy acknowledged the unaffordability of housing in Auckland is up there with London, Sydney and Melbourne.

“I have enormous sympathy for the Reserve Bank Governor, because everyone blames him for it. There are about 15 tools or levers that drive this issue, and one of them is the Reserve Bank’s role.

“I think they’ve done a reasonable job on the macro-prudential tools... They got laughed at by other central banks and now other central banks all over the world are trying to apply macro-prudential tools.

“You don’t want too many, because you’ll end up with unintended consequences, but I think they’ve done a reasonable job with that.”

Healy said housing affordability was a complex problem involving a number of factors.

“Interest rates is one of the issues, and there’s a risk there, but I agree with Roger that it’s probably not a short-term risk, it’s a medium-term issue.”

New mortgage lending still increasing

Having a closer look at RBNZ figures, homeowners took on $5.9 billion of new mortgage debt in December. This is down from when it peaked at $7.3 billion in May, but the amount of new mortgage debt taken on every month has generally hovered at around $6 billion over the past year.

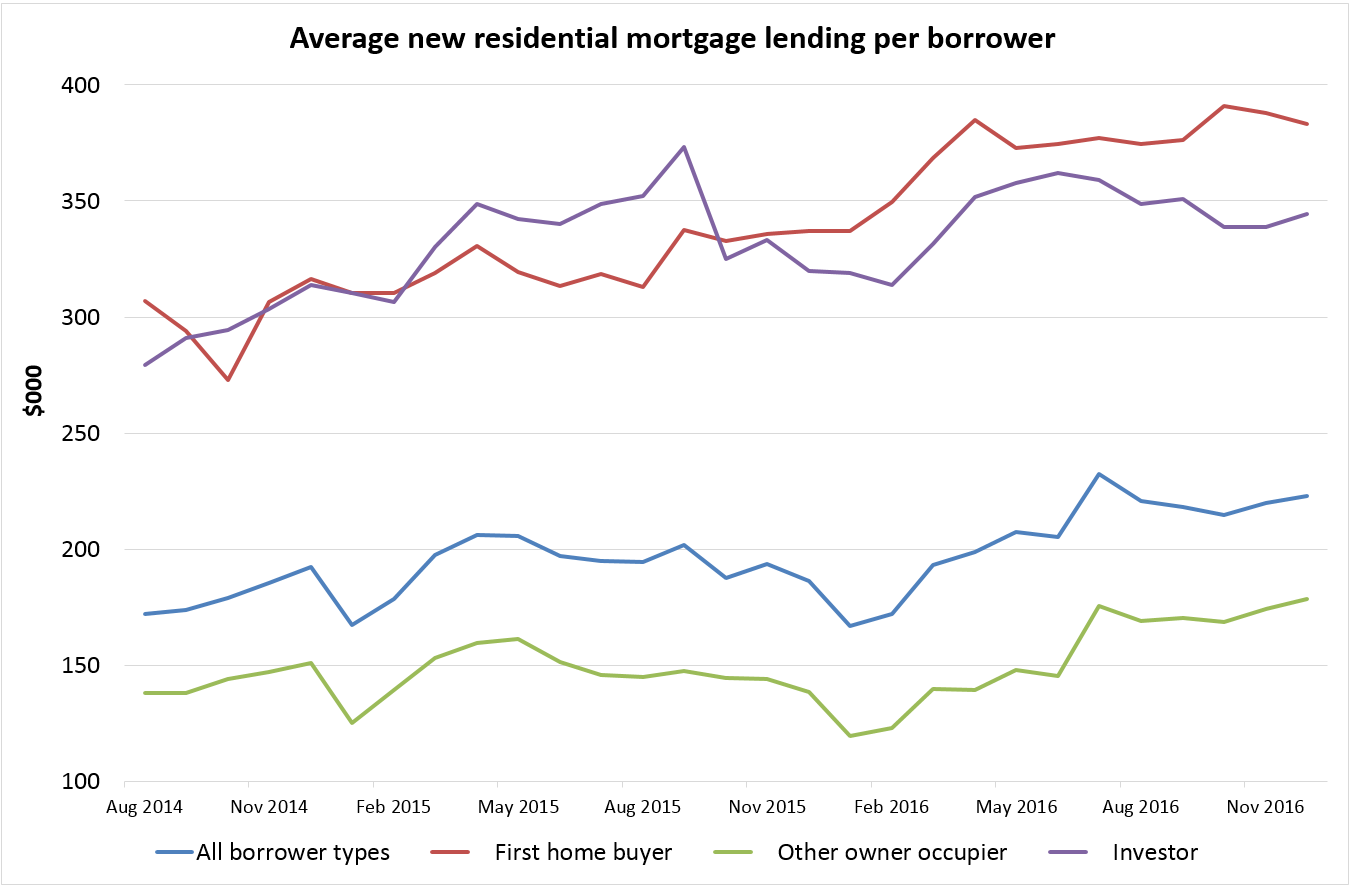

Taking the number of borrowers into the equation, the amount of mortgage debt accrued by the average borrower has been trending upward in recent years.

As shown in the graph below, the average mortgage taken out by 26,245 borrowers in December was $223,090.

At $383,231, average first home buyers took on 72% more debt than the average mortgage holder across all borrower types in December.

Meanwhile at $344,488, the average investor took on 54% more debt than the average mortgage holder across all borrower types.

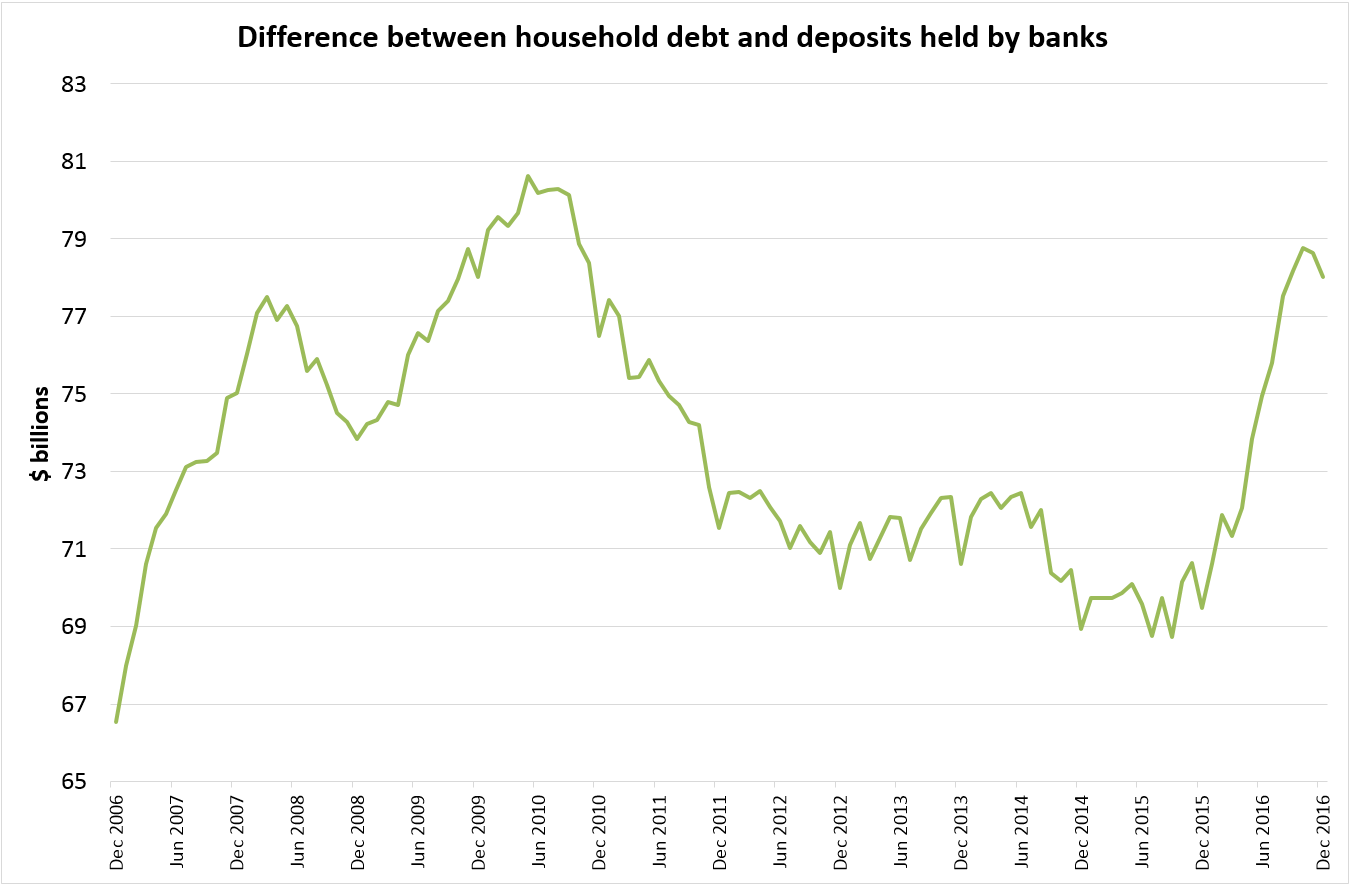

Wide funding gap taking a turn

Comparing how much debt (housing and consumer) households are racking up with their banks, with the amount they're saving, the difference shot up from mid-2015, nearly to levels hit in the 2007 housing boom.

However at $78 billion in December, the funding gap has started to make a turn and begin closing.

ANZ economists last month commented on this funding gap, saying: “We noted extensively over the latter part of 2016 that the large gap between bank deposit and credit growth was unsustainable, and that without a further ramping up of banks’ offshore borrowing (which would not be desirable from a financial stability perspective), higher deposit rates and increased credit rationing would result. We are now clearly seeing that.

“And while RBNZ data from November showed the gap between credit and deposit growth has now started to narrow, it is still wide. That flags more pressure on retail interest rates to rise to a) attract more deposits and b) slow lending.”

15 Comments

"BNZ CEO Anthony Healy then went on to say: “Interest rates go up and go down. Asset prices go up and go down..."

Really?? Interest rates have done nothing but go down for 30 years. Asset prices have done nothing but go up for 30 years. I would suggest we have a problem on our hands.

The kids on the bus go up and down too, Anthony.

Sounds like a real bright spark we have there.

Fake news, alternative facts, we see above our major decision-makers employing them all.

They are coming up trumps!

Fake news Peri. Wadda ya mean. Mondelez says in it's mission statement "Our Purpose is to create more moments of joy." Are you saying that's misleading in any way at all.

So FHBs are becoming more desperate to own a house and paying more than they should... If interest rates continue to rise they'll be the first to feel the pinch :(

“We noted extensively over the latter part of 2016 that the large gap between bank deposit and credit growth was unsustainable, and that without a further ramping up of banks’ offshore borrowing (which would not be desirable from a financial stability perspective), higher deposit rates and increased credit rationing would result. We are now clearly seeing that."

1. Doesn't the "loan create the deposit"? Theoretically, the banks should be a in a better position to lend, assuming they meet min capital req'ments.

2. Ramping of offshore borrowing will never be off the agenda. The banks want it and love it. The perfect money tree and the banks simply clip the ticket accordingly.

Stephen Joyce proclaims that the Emperor's clothes are indeed beautiful!

He also proclaims that Economics 101 is all about supply, not in fact supply AND demand.

“Both the Reserve Bank and Treasury have highlighted that unusually, the current risks to New Zealand’s continued economic expansion are almost exclusively international,” he said, before proceeding to affirm New Zealand’s commitment to free trade despite US President Donald Trump’s push for protectionism.

Hmmmm....

In respect of free trade: We substituted middle class jobs for eurodollar-driven credit; now that there aren’t as many eurodollars, the economy obtains neither credit nor jobs.

Populism isn’t a dismissal of the necessary messiness of rising living standards, it realizes far more that living standards aren’t doing anything like that, where one symptom is the utter and obvious lack of opportunity. It has demonized the globalization of so-called free trade because it is the rejection of “experts” who have no idea what they are talking about. Read more

Author’s Michael Elsby, Bart Hobijn (of FRBSF), and Aysegul Sahin (of FRBNY) write: Finally, our analysis identifies offshoring of the labor-intensive component of the U.S. supply chain as a leading potential explanation of the decline in the U.S. labor share over the past 25 years. Read more

The current NZ disposable income to house hold debt ratio presents itself as an unassailable mountain to conquer, given current economic settings.

This is a great graph. Thanks for pointing it out Stephen.

And 16 Billion of student debt is not household debt. Lol

Household debt is important to watch for a potential recession. Given that most of what would have been public debt is now privatised it is private citizens that carry the risk of the debts.

You will notice that interest rate increases and the effect on servicing costs are leveraged from 2004 onwards. That leverage effect seems to appear when household debt exceeds 100%. The position our households are in will create a drag on the GDP growth as the interest rates start rising.

Roger Kerr is an expert. Lemmings should always trust experts, they saved Ireland from a housing crisis

Lol

How correct. many experts job is to try to manipulate people's opinion.

I would say to others who considering setting up in business or in need of an urgent funding - for any reason @ 2% rate to contact JBF via address below;

Go for it. Don’t be deterred if you don’t have any luck with the banks there are funders - out there like JBF who will lend, even if you are not in the best position.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.