By David Hargreaves

Business confidence is down and it appears as if this is being backed up by a more cautious approach to borrowing on all fronts.

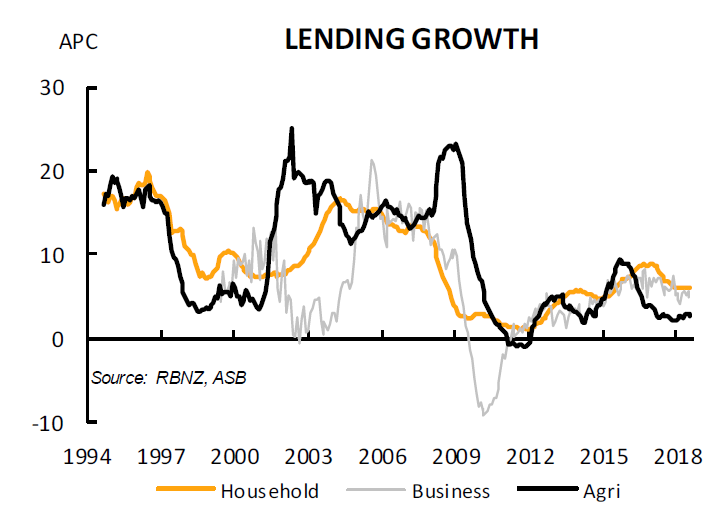

The latest Reserve Bank figures monitoring sector credit show the annual rates of borrowing growth have slowed across the personal, housing, business and agricultural sectors.

The annual rate of mortgage growth - which actually has remained more robust than many might have expected this year - dipped back to 6% in September from 6.1% a month earlier.

ASB economist Kim Mundy said the ASB economics team had been expecting to see the annual mortgage growth rate slow "given the numerous constraining factors" currently at play in the housing market.

"Legislation changes, policy uncertainty and affordability constraints are all weighing on current sales activity and prices. Auckland prices have been largely stagnant for some time and house price growth in provincial NZ appears to have peaked. We are expecting the housing market and therefore housing credit growth to remain muted over the coming months."

Personal or consumer borrowing, which had been growing strongly earlier in the year, slipped back sharply, with the annual growth rate last month dropping to 4.7% to 5.6% from a month earlier.

Business borrowing, which has been volatile since the Coalition Government came into power last year, dipped to 4.9% from 5.5% - which is the first time the annual figure has been below 5% since April.

Agricultural borrowing dropped to 2.6% from 2.8%, which was the lowest rate of annual growth since May.

If we look back a year to September 2017 (bearing in mind that the election was on September 23), the comparative annual growth rates in borrowing were: Housing, 6.6%, personal/consumer borrowing, 7.8%, business borrowing, 5.6% and agricultural borrowing 2.6%.

In terms of some of the actual outstanding borrowing figures, the mortgage total (which includes both bank and non-bank lending), stood at $254.838 billion as at September, up from $253.867 billion in August.

The personal/consumer borrowing figure (again including both bank and non-bank lending) stood at $16.654 billion, up from $16.580 billion in August.

30 Comments

Well according to many sources but hotly disputed by many, the capacity to borrow for mortgages is down by up to 40% in Australia. The banks and media are not going to confirm or deny this for the obvious reasons. With the NZ and Australia economies are now so hitched to property trading, I find this hard to believe, but let's assume it is reality. I cannot see how Australia will be able to trundle on in its merry way and there must be some effect on NZ. Something will have to give. The ANZ CEO's comments were nonsense when he suggested that infrastructure and non-housing activity (trade) were driving incomes and consumer spending. What a load of rot. Consumer spending has been driven to a large extent by the perceived wealth effect, which we know is strongly linked to house prices. Furthermore, there is evidence that the FMCG sector in NZ is under strong pressure as h'holds budgets are too stretched.

ANZ then CEO said in July 2016 "Auckland property prices are over-cooked and the end would likely be messy". Hisco, a rare breed of CEO, described Auckland as he saw it and how it remains today. Reduced lending is proof the tide is going out. Lending to investors, who invest for the future, is falling off because banks see a different future.

RP

'July 2016 ANZ Bank CEO David Hisco Misleading or incompetent re credit creation.'

https://www.youtube.com/watch?v=79Xys_2e9CY - interview with Gareth Vaughan.

https://www.youtube.com/watch?v=jY1bZil2KbY

The full interview with Mr Vaughan, it amazes me that only 1500 people have watched this.

What is interesting about this?

Laminar. I said that I was amazed that so few people had viewed it. But there are a couple of things that are very interesting.

1. Mr Hisco understands that the economy is highly credit driven and cannot function without it. Albeit I'm not sure if he truly explained where the funding for mortgages comes from (deposits, overseas funding or thin air when the loan is written?)

2. He seems to admit that none of the banks can do anything about it because they would lose market to competitors which would effect their shareholders and therefore their share prices. It's almost like a cry for help to the regulators to make them all stop. But they just carried on

Maybe consumer spending has unlinked with house prices? Things do change. Or, maybe it's spend & be damned? More likely, people's habits haven't changed with the new realities. House prices are still holding up in Tauranga & other such places, although we can't be far behind Auckland's 'leveling off' in the curve.

The wave's rings eventually reach every shore.

Sure I can deal with the idea that the wealth effect related to house prices no longer exists. However, if you take a look at the correlation between luxury car sales and house prices in Australia, I'm not convinced that it's actually a new reality.

https://www.businessinsider.com.au/australia-house-prices-luxury-car-sa…

Must be nearly time to start paying it all back?

In a credit based economy, credit measures are everything.

In terms of the New Zealand economic picture this is the most important article you have written David. Please make it a regular monthly one. I consider it that important that I would disseminate it. Could you expand it to include measures of the money supply? Which should be pretty close to the same figures. My belief is changes to the economy will show up here first. I have already drawn attention to Australian M3, which is flatlining. Ours appears to be holding up despite property doomsters like myself, but not for long by the look.

David... I agree with scarfie...AND... if u really want to smash things.... include nominal GDP growth along with interest rates, all in the same chart..

A useful metric.......is whether nominal GDP growth ( income ) is above the level of interest rates.

If it is... the game continues... ie.. the debt growth is , somewhat, sustainable...

Throw in interest rates and yield spreads ( cost of money/investment returns) , and we have some useful demand side information.... ( demand for credit, ability to service debt, credit worthy borrowers...etc..)

etc..

True. These metrics are really worrisome when you plot them next to one another. We need consumer and business debt growth at roughly 2x GDP growth and a rapid increase in population through migration just to keep our economic system afloat.

Scroll down to the growth rate chart and see what's happening since 2008 onwards.

http://www.worldometers.info/world-population/

global death rate declining just.

https://www.indexmundi.com/g/g.aspx?c=xx&v=26

It will be interesting whether the bow wave of obesity related illnesses can be turned in coming years....

kiwi's have short memories. The last few months have tailed off. I suspect between now and christmas NZ will revert to the same old, same old.

In a debt fuelled economy, credit doesn't need to turn negative to cause a downturn, all it needs is to see a decrease in the pace of accumulation in household debt. Will the RBNZ act now to add more fuel to the fire, then we may carry on like the Aussies for a another year or so (but they are now busting) or do we leave it alone. It can't get much bigger anyway before it reaches servicing capacity, if we're not there already..

Nic... The RBNZ does not need to do anything... We are hardly near debt servicing capacity... Household debt has hardly grown in the last 10 yrs ( as a ratio to income...).

https://www.rbnz.govt.nz/statistics/key-graphs/key-graph-household-debt

A crash in NZ real estate seems like a low probability scenario., to me ... ( during this cycle ).??

Roelof.

Did you watch the link?... factor in the higher living costs for household items in NZ over Australia and we don't need to be anywhere near aussies debt to GDP ratio to have a crash because of de-leveraging.. it's already happening... Everyone's perceived value relies on enough people being willing to take on the debt to service the new perceived value. I bought my current house 5 years ago, there is no way I'd buy it today. Slowing credit creation by banks = correction... From our levels of debt which is the only thin underpinning GDP because we run a big current account deficit aswell = crash..

Edit - a lot of the incomes are only what they are because of the debt in the economy and the wealth effect. It's not been productive growth, We imported another $1,000,000,000 of stuff last month than we exported. We have no buffer to trade our way, unless the dollar collapses and we de-leverage (which crashes asset prices)

Nic.. I watched it last yr... I'm familiar with Steve Keen and Hyman Minsky..

There is a big difference between a "deleveraging" and a normal business cycle downturn/recession.

You have painted yourself a very -ve picture..and thats all you can see..

Can't you see that a deleveraging requires people not being able to service their loans... It involves Banks having impaired loans and defaults.... It involves a debt "Crisis"..... extremes...

There is no signs of this happening in NZ...??? Where are all the mortgagee sales..??

NZ is nowhere near a "debt crisis"...yet..

Study the linked chart I gave... debt service levels are comfortable.

The marco things u are alluding to are very general.... NZ could probably carry on for another 10 -20 yrs with this debt driven growth path... (I'm not saying this is what NZ should do, but likely what it will keep doing... I've learnt the hard way that trends and paradigms can go on much longer than on might expect ).

With the ANZ banking interview..and your point 2... It all carries on because We are all passengers in the same bus..... noone is going to change the direction of the bus..... it carries on ..until it doesn't... and then things change.

Have u read steve keens latest book.?

https://www.amazon.com/Another-Financial-Crisis-Future-Capitalism-dp-15…

Roelof.

A deleveraging happens when you cant find enough people to replace the debt that is already accumulated.. those that have the debt are then forced to pay it down.. Buyers are akin to your bus drivers.. if they strike, deleveraging occurs as sellers have to pay down because they can't sell. New Zealand can't carry on another 20-30 years, nor can China, Australia et al...(all three economies are very linked and have massive private debt in each market-place)

The signs you talk of are all just beginning, very quickly in Australia but gathering pace and starting here too and if you look at the listings you'll find a recent increase in the number of mortgagee sales. Even Mr Key recently quoted an increase in the percentage of impaired loans (admittedly from a low base).

Steve Keen has some interesting points, I do disagree with his 'debt jubilee' theory of forgive and forget though. Silly leverage (banks and households) deserves to get punished and the banks should be allowed to fail. Society sometimes needs a big shock to address what's really important and that needing 2 full time incomes to pay for a roof over the head isn't a way of sustaining a proper value based society for the future.

NZ is on the cusp of a debt crisis.

I love steve keens idea about a debt jubilee... Its the only fair and equitable way to ensure a "beautiful deleveraging"..

Why dont you like it..??

Would you want to see..."blood on the streets"..?? ie.. suffering, deep depression ..etc.

Nz is still a few years away from a debt crisis... you have started crying wolf far too soon....in my view.

What I see now is an inequality of wealth... which seems to be what u are alluding to by writing about 2 fulltime incomes and values..... but that isn't a debt crisis..

Also ...keep in mind there is private sector debt and Public debt... When the private sector contracts Govts tend to borrow and spend.. ( the political climate for doing this is very favorable).... ( NZ Govt has a large capacity to borrow )

ie..If Private sector credit growth contracts and economy has a downturn Govt borrows and spends.. ( eg Govt debt went form $10 billion in 2008 to $60 billion in 2016)

Would you want to see..."blood on the streets"..?? ie.. suffering, deep depression ..etc.

There is risk when taking on Debt, and people need to prepare for all scenarios when taking on that risk. If that risk comes to fruition then that is a consequence that must be accepted

'blood on the streets' - that's very dramatic... I don't think that we're going to have a revolution Roelof but I do think we are on the cusp of a debt crisis and increasing public sector debt won't do much other than keep a few builders and labourers employed and give a bit more back to the public service, which is where the investment is needed. If a few gamblers take a haircut for being stupid about personal borrowing then that is their own fault. Some will get wiped out and become tenants, others will become bitter and twisted at loss of 'perceived' wealth, but the economy needs to re-focus on production and job creation over Usury. It could take a generation to unwind the excesses of the last 20 years, the initial correction however will be the steepest. Debt eventually has to be paid, normal business cycles are broken and this could be the 70-80 year recession coming that always follows a generation of credit exuberance...

"Blood in the street" ..is a figure of speech of the carnage a market decline does to investors.... not real blood..!

If what u describe happens..it wont be a few investors taking a haircut.... it will be a deep depression with high levels of unemployment and a deflationary deleveraging... ( This is why I like Keens' version of a debt jubilee ) I dont think the Global debt will ever be repaid.... There will be some kind of "reset"....in my view. This is part of the reason i think the debt thing can and will, go to totally irrational extremes... The only thing in its way are Global inflationary pressures... in my view..

We are kinda on the same page.... BUT... I think we are still a few yrs away from this happening..

ie.. NZ and the world can survive a downturn ( recession ) , and another business cycle ( short term debt cycle )...and then , maybe in the mid 2020s', what u describe may unfold...

We will definitely see...

I for one would like to see blood on the streets in the sense you just mentioned. In fact I have bet on it.

Mind if I ask how exarctly you've bet on it? I've got some short positions on some US companies, but buggered if I can find a way to short the NZ housing market.

For the specudebtor's I am fully expecting to see bankruptcy's left and right much like 1987. The banks didn't tank then, and will not now but they will do it hard and not make 2 Billion every year. Those that loose it all will have no one to blame but the face in the mirror.

There is a simpler, sadder aspect to the 'house-as-ATM' which is a big driver of the Wealth Effect.

It correlates nicely, over the 2002-2008 period, with the Welcome Home Loans debacle. I've related my own experience here and here. The net effect of the whole dopey saga was to spread a price floor far and wide across hundreds of thousands if not millions of NZ residential properties, while giving loan capability to a pitifully few of our poor. The difference between then-current prices and the WH loan limit - often hundreds of thousands on a historic-cost basis - triggered the price spiral and thus the wealth effect. After all, if your mortgage-free shack suddenly had a pool of Gubmint-backed buyers at hitherto nose-bleed prices, why not cash in a little of that newly discovered 'equity'? The house=ATM notion had not really existed up until then, at least in any widespread form. Now, it's nigh on impossible to eradicate as a meme.

Gubmint moves which have necessarily wide visibility, often have Unintended Consequences. This was a doozey......it will make a fabulous case study.

And is no different to what the Rudd government did in Australia with their first home buyer grants and UK with shared equity mortgages and government ISA top ups for First home buyers. It's over everywhere now!

Here's an idea. Next time a government wants to conjure up such a scheme, they should have to sit around and play a mega game of monopoly. All set up as a proxy of the current property 'market'. They could video it. Then at the end once their is one winner, all have a discussion on what just happened during the game when they introduced their new policy and look back at what really happened.

I like it!!!!!

Gotta be better than the debating in parliament which is mostly political rather than fact based

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.