Kiwibank economists think the Reserve Bank's limits on high loan-to-value ratio (LVR) lending - introduced as a temporary measure - in 2013 are set to become permanent.

But in their Kiwi Economics Weekly Update Kiwibank chief economist Jarrod Kerr and senior economist Jeremy Couchman reiterate that RBNZ is set to loosen the LVR restrictions again in its Financial Stability Report being released on Wednesday.

And they say their preference is for a loosening in the speed limit on high-LVR owner-occupier loans "because the availability of credit should be extended to first home buyers in particular".

The economists have already indicated they think the RBNZ may loosen the 'speed limit' on the amount of bank new lending that can be advanced on loans to owner-occupiers above 80% of the value of the property to 20% of that new lending from 15% now. And they think the deposit limit for investors may be lowered from the current 35% to 30%.

But in their latest update, the economists speak in favour of the central bank actually going a bit further and loosening the 'speed limit' for owner-occupiers to 25%.

"A lifting in the speed limit to 25% would ease access to a difficult market, in our view. An easy argument to make politically," they say.

"The deposit on investor lending could also be eased (again) to 30%, and the speed limit to be lifted a little without adding much fuel to the fire. Credit growth is subdued, and credit to investors has been reined in since 2016. A loosening in LVR restrictions would loosen the availability of credit, and add a little to credit growth next year."

The economists say though that the “temporary” measures that are the LVRs, "are unlikely to remain temporary, but become permanent".

"The levels at which these measures become permanent will most likely be looser than the current settings. So, as an interim step between temporary and permanent, we expect the LVR restrictions to be loosened again. It was this time last year when the RBNZ loosened the LVRs just a little. And we expect a little more loosening this year. Risk in the system is being managed."

The RBNZ has maintained that the measures are meant to be temporary, but they have now been with us for five years.

Kerr and Couchman say a loosening is in line with the RBNZ’s three criteria:

- Evidence that house price and credit growth have fallen to around the rate of household income growth.

- A low risk of housing market resurgence once LVR restrictions are eased.

- Confidence that an easing in policy will not undermine the resilience of the financial system.

"We argue all three criteria have now been met. The need to guard against excessive leverage building in parts of the system remains. But credit quality has improved materially since 2016. We believe the 2nd and 3rd requirements are easy to argue, now that the housing market has cooled, with Auckland’s lead."

They say that the LVR restrictions have clearly worked, "if not initially".

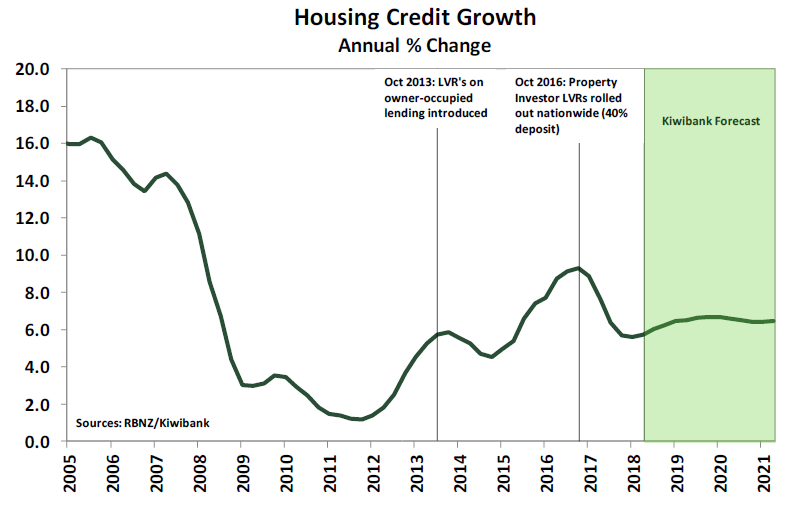

"They were difficult to implement, but clearly worth the effort. Our chart shows the LVRs reducing risk in the system. But now the market has cooled, and temporary measures need to be looked at. We prefer a loosening in the speed limit of 15% on owner-occupier loans with <20% deposit. Because the availability of credit should be extended to first home buyers in particular."

28 Comments

Yeehaa, pump that bubble up once more baby!!

Bigger the Bubble, the Bigger the Crash !

It's not a Bubble......

But a steel-belted radial.

Refuses to puncture/deflate.

TTP

It's a steel belted radial with a nail in it.. slowly leaking, and being run flat, and soon enough the sidewall will be compromised and the whole tyre is headed for the shredder.

Loosen it for New Builds, but keep it tightened for existing housing.

Thought they had an exemption already

Oh you're correct!

Agree.

Do you think Phil has a big cheque in the with Kiwibank's name on it sitting in his top drawer? Just waiting until they can lever down the LVR's. Then together they can get some creative financing options going to get those bloody Kiwibuilds sold. Because the Aussie banks can see what's coming and they don't want that kind of risk right now.

Does the chart above say that credit growth is just above 6% and then they mention that household income is in line with credit growth? Wonder if they took inflation into account on that household income figure....

Inflation is part of what causes growth in credit so you dont X-out inflation from income when comparing it to credit growth.

Even though credit growth in Australia is decelerating, Australian banks are still experiencing a persistent credit-deposit gap.

https://thistimeitisdifferent.com/australian-credit-growth-september-20…

https://www.businessinsider.com.au/rba-deposit-growth-bank-funding-cost…

Hi RP

So Aussie total mortgage debt and Canadian mortgage debt has grown around 70% since 2008. US is negative at 1% or so less than 2008, UK 11% more than 2008 and NZ has gone from around $140 billion in 2008 to $253 billion today.

And the winner is 'NZ is diffrunt' with an astonishing increase in outstanding mortgage debt that is 81% larger than before the GFC hit!!!!

And your point is?

You have to remember that all credit vs servicing ratios is relative. i.e. If the earnings or GDP rises at rate x% then credit can also be allowed to rise at x%. NZ has vastly increased its Earnings/GDP and therefore the rate of servicing over the last 10 years. Therefore the RBNZ can, if they wish, to ease the credit in the system.

Sure - what could go wrong? Credit growth has decoupled from income growth completely it seems to me. As long as everyone is clear about the likely outcome let's roll the dice.

First Home Buyers should not be buying new houses generally!

All that it is doing is encouraging young ones to borrow more money on mortgage and then they continue to expect everything new.

Anyone that has become financially successful in any

business including property investors, have started at the bottom and worked their way up!

This reduced deposit for new builds is a load of BS and should be knocked on the head, especially in Auckland where the prices are ridiculous for the crap box’s they are trying to sell for 650k.

I would always advise the first home buyers to buy something under true market value with upside!

Providing you are reasonably handy and prepared to work then you can still become financially secure by the time you are in your mid 40’s or earlier.

Problem is that too many nowadays think that they have done well living in a new home with a massive mortgage.

Reality is that they haven’t and will not become financially secure ever unless they are on massive income!

Dunno if you've noticed, but saving the 10% for a new build is easier than saving 20% for a run down shack that boomers have flipped multiple times and stroked the value up by a factor of three, often without so much as a lick of paint.

Some new builds are more affordable than existing homes due to the land size and require no extra money to upgrade or make the home liveable.

It's all very well to say FHBs shouldn't be buying new houses, but have you considered the shocking quality of NZ housing stock?

Many houses in NZ are long past their use by date. FHBs could very well buy these rubbish houses and find their health diminish, never ending repairs are required, huge heating costs and that the house isn't up to the demands of modernity.

With second hand homes being so expensive and dated, a better option for FHBs is to buy a NEW unit, apartment or townhouse. The best option of course, if homeownership is your goal, would be to move to an Australian state like WA or to America.

Consider your options and don't be in a hurry to leverage up on debt. There is a real possibility that unless you have a huge deposit, negative equity could be waiting in your future .. and its' desire is for you!

Who wants to save a deposit only to see it disappear month after month, year after year!? A good exercise would be to look at what you could get for the same money in places like Florida, Texas and Perth.

It's almost like the consenting issues, building material costs and previous generations of real-estate raiders have eliminated the entry level housing stock and the chance to buy something that needed a bit of work to become a family home.

The problem is people put their lives on hold until they have stable accommodation, and things like having children operate on biological timelines, not economic ones. So "don't be in a hurry" is all well and good, but life doesn't work like that.

Well you know the best yields can be found in entry level housing stock. Buy something that needs a bit of work, do as little work as possible, and then profit from it. This is how TM2 does it.

In the bigger picture the GFC was in some part a result of unfavorable western demographics. The central bank countermeasure (ie accommodative monetary policy instigated worldwide) has resulted in worsening demographics with many people putting off having children well into their 30s or 40's because they cant afford housing.

"long past their use by date" - you do realise that in other countries, people are still living in houses that are hundreds of years old. The idea that in NZ a house is past its use by date because its 50 years old is ridiculous. Renovating them into a modern home is still far cheaper than knocking them down and building new. Unless you knock them down and replace them with multiple cheap and nasty dogboxes. Which is hardly "improving the quality of housing".

The saying is that you get what you pay for!

These crappy boxy houses that Aucklanders call KiwiBuild are not value for money!

Too many contributors on here on,y talk about the overpriced hyped up Auckland market where the housing market is totally different around the country.

Some people on here say that NZ housing is poorly designed and built but this is totally incorrect!

ChCh. as we all know has had tens of thousands of earthquakes.

We owned houses before the quakes in ChCh and have purchased quite a no. Rental properties since the quakes.

I can tell you that not one has been in an unliveable condition and every single one has stood up to the quakes remarkably well.

We have not had a single one written off and 2 that we have purchased as is where is have both now got insurance and basically very little wrong with them, and easily fixed for little cost.

As for being cold and damp, that is also a fallacy.

Every one of our properties are fully compliant and have been soon after we have purchased them.

Never once has a tenant complained about being cold or felt unsafe in our property.

You can all have your opinion about housing in NZ, whether you think they are overpriced and are Hoping that prices crash so that you can afford one!

What I will say is that it personally doesn’t worry me what other people do in their lives, it is their business obviously!

It is up to each individual to make the most of what they have and stop blaming others for where they are.

Successful people make it happen, they don’t whinge and groan!

It's pretty easy to be successful when you tilt the playing field in the favour of an entire generation.

But of course, it's all hard work, isn't it?

Sorry, but my generation generally worked pretty hard to get where they are today.

Not everyone but most of my generation do not just expect everything to fall into their lap!

Personally I can tell you that we have worked hard to get where we are today, and speculated to accumulate and never once expected others to provide for us!

My generation is not the lucky generation at all,

Any generation is lucky if they are prepared to work, not sit on their butts and prepared to do more than just a 9 to 5 job.

Working for wages is so overrated on the whole!!

I thought a significant proportion of your wealth came from an inheritance that your partner received?

I wish the Land Transport Safety Authority would follow this logic. "We announce that since we lowered the drink drive and speed limits, road accidents have reduced. Therefore we are now raising the drink drive and speed limits again, as we believe drivers will be more considered".

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.