Farmers are feeling pressure from banks. They are worried about access to finance in the future.

A recent survey laid this out clearly. Banks are getting tougher. Not only is cost an issue, but conditions are too.

The main farmer lobby group saw this as a direct consequence of the RBNZ Capital Review. But that is dubious.

The RBNZ is also seeing banks making tighter finance decisions, noting that some of them are adjusting back from relatively loose credit settings. The regulator thinks some of this is overdue.

Rural lending is substantial. The latest data shows it currently totals $63.7 bln. It is a large amount but compared with residential housing at it is more of an after-thought. Households owe mortgage lenders $199.6 bln and investors owe another $71.9 bln. Together that totaled $271.5 on the same date.

And farmers feel they are being treated as a disposable after-thought. After all, banks get to construct their own discounted risk weightings for housing lending, but must keep a full 100% of risk-weighted capital for rural lending. Clearly banks will prioritise residential housing housing when the rules are set like this.

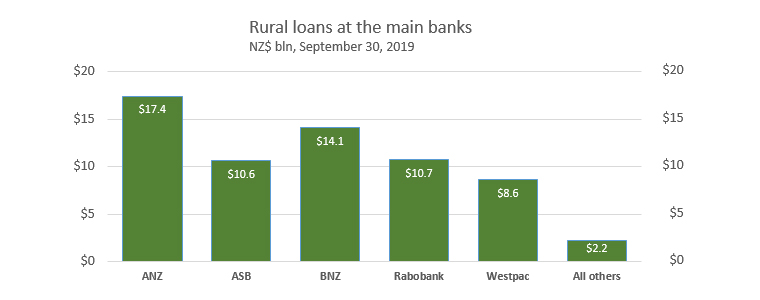

The RBNZ dashboard tells us which banks are exposed to rural loans.

But that same data is silent on which rural sector (dairy, sheep, beef, horticulture, forestry, etc) this exposure is concentrated. Other disclosures strongly suggest it is heavily concentrated in dairy.

The bank with the largest exposure, $17.4 bln and a 23.7% market share is ANZ. That share compares with a housing market share of 30.3%. Over all lending, ANZ has a market share of 29.3% of all debt measured by the RBNZ data.

But ANZ is on a drive to reduce its underweight rural exposure to even lower levels.

And so is ASB.

But the somewhat surprising thing is that other banks have not shown the same risk aversion to the rural sector.

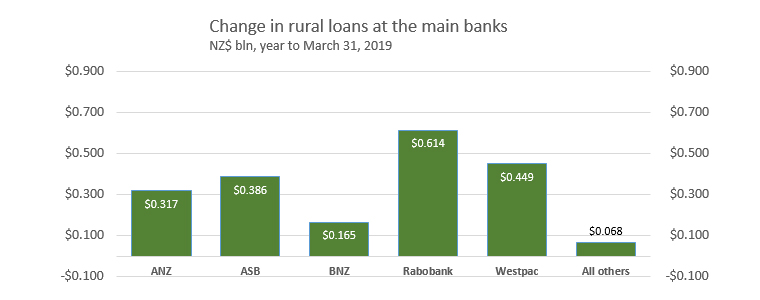

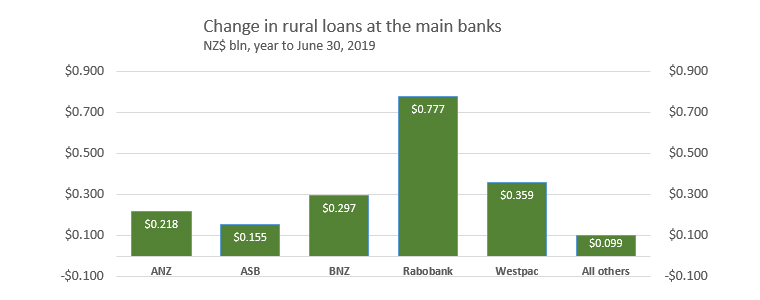

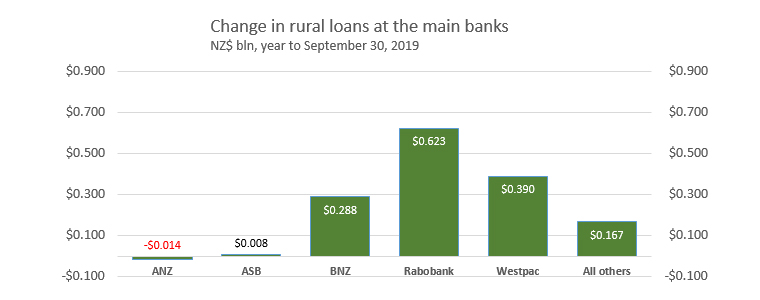

The following three charts track the change in rural lending exposures in 2019 and reveal the size of the moves by both ANZ and ASB.

ANZ's appetite for new rural lending was underweight at the beginning of the year ...

... and it was joined by ASB in mid 2019 ...

... so that by the end of the the September quarter they had frozen all expansion in their rural lending - in fact, ANZ was starting to shrink its exposure.

(In the same year, ANZ increased its housing loan book by +$5.8 bln and ASB increased theirs by +$3.4 bln. This is an unchanged growth track from earlier quarters.)

Also very clear from this data is that it has been business-as-usual at the other main banks - even if none of them are stepping up to fill the void left by ANZ and ASB.

But other lenders are, although while their growth is high in percentage terms, it isn't enough to replace the lost appetite from ASB, let alone ANZ.

Both the banks that are forsaking farmers are ones that have the largest share of urban housing mortgages. ANZ is 30.3% and ASB is second at 21.4%. These two control more than half the home loan market. And they are actively trying to grow their share.

Urban housing is not a productive sector of the economy. It produces much more cost than income, produces no export revenue, and is all an 'asset valuation' game.

Farmers, who all have active real businesses and whose output generates 43.8% of all the nation's export revenue, are being starved of financing by two of our largest banks so they can concentrate on lending for houses. The risk-weighted capital rules are the incentives and both ANZ and ASB are responding to these financial incentives without regard to the social licence of their position.

At least it is only two of five banks turning their backs on their rural communities. Lets hope the others hold on to their broader social responsibilities. If farmers think they have issues now, if all banks respond like ANZ, their stress will multiply sharply.

In any case, it is unfortunate that large first movers like ANZ and ASB can effectively take advantage of the market in this way without regard for the wider national interest.

The RBNZ is hands-off, declaring that "banks have to make their own credit decisions" and that "there may be a case for a reassessment of some rural, especially dairy, exposures". But when just two institutions control more than half the market and they constrict financing flows quickly, everyone suffers.

It is not a normal competitive market - there are a tiny handful of very large suppliers (one of whom is dominant), and a very large set of relatively small customers, none of whom are individually significant. It is a classic power imbalance.

45 Comments

... at the end of the day , are the farmers able to service their loans ? ... Yes !

OK then , the ANZ & ASB will be ceding market share to their competitors ...

... no problem here ....

Great stuff David. Farmers are in the dog box at the moment:

1 The Greens hate farmers and think they should all be shut down and the land returned to bush. Well maybe a few are allowed, provided they are communally owned by members of the Green tribe.

2 Labour hate farmers because they own their land, which is clearly unfair as they should own it.

3 Bankers can make more money from the urban debt serfs 'cos they can lend 3 or 4 times as much for a given equity base, thus making 3 or 4 margins not one.

4 Farming is kept in survival mode by the political bias of all parties to favour capital importing over export profitability.

So, we have endless regulations and conversion of farmland to housing and "forestry" (isn't carbon credit forestry just granting dodgy foreign entities the right to tax us?).

It will be interesting to see how this resolves. Pendula have a tendency to swing back eventually, and the more extreme the position in one direction, the more energy there is in the swing. Meat prices are rising rapidly. How expensive does food have to become before we become thankful for the work of those who produce it?

Re: 4 - if we were to pivot to an absurdly low dollar then the cost of imports would explode because of this country's rampant ticket-clipping and standards of living would totally collapse.

Really it's the only thing giving the middle any purchasing power at all.

Or is that whole idea just intellectual Kool-Aid, drip fed to us by those who think they know best?

Oops, dp ....

the results of an asset bubble caused by lax lending standards ,creating self reinforcing credit expansion with little or no difference in earning potential. Farming has this in common with the housing market. If earnings are going up due to customer demand or efficiency you can justify higher assets and higher wages, we got the higher assets with out the earnings, have condemned our children to a life of penury with high housing costs both asset and renting. High capital costs in farming needed to support existing borrowings.

I sat beside some rural ASB managers pre 2008 and they talked of the farmers they had with over 75 mill of debt and there were lots, no farmer should have 75 mill of debt, is friggin crazy stuff, belonging to an alternate reality.

We drop interest rates to support the indebted and they see it as a 'buy' signal, assets go even higher. The fundamental production, was never there to support assets values in housing or farming.

In the mean time the non-productive sector has used the high asset values to go on an unsustainable spending spree, dooming us in a down turn to paying back unfathomable amounts of debt, and impacting on many businesses profitability.

I the process we have created debt magnates, those with multiple houses and multiple farms due to easy credit expansion, self reinforcing the loop of ever increasing values. Less and less people own more and more, unsustainable in any democracy. I don't see any banks dealing with these people, where the potential destruction of our lending sector lies.

The only option so far has been to punish savers, that can only go so far, the process has destroyed profitability of pension plans, insurance companies , ACC and eventually will destroy the banking industry as well.

Top comment: "We drop interest rates to support the indebted and they see it as a 'buy' signal, assets go even higher."

This mess is a failure of Governments' policy settings - banks will just pick whatever fruit hangs lowest. That we have elected successive Governments that embrace asset inflation as the be-all-and-end-all of wealth making, in the absences of productivity, sees us where we are. And you know what? After several decades of Government inaction/failure, there is no way back without a painful 1980's style re-set of the economy. That may have ultimately come to little, but at least we tried.

"In any case, it is unfortunate that large (banks) can effectively take advantage of the market in this way without regard for the wider national interest." Exactly!

An answer: Drop interest rates to 0%; drop LVR's to 70% and 30% ( owner and second asset owner resp) install DTI @ 3.5 and ensure that any and all lending goes towards productive endeavours. If that's farming, first up, fine. But as I'll say yet again, IF banks can't lend to one particular sector for whatever reason, they WILL find a way to lend to others. They have to! Their existence depends on it.

(Final thought: Some part of the economy is going to be hit by sorting this lot out. Given the choice, do we want it to be the rooves over our heads or the food we put on our tables? If you have a roof, you'll be ok at 0% etc. but if there's no food on the table or fillet steak is at $500 per kilo, you may not be)

.... recall the Crafer Farms . . they were able to leverage up to $ 200 m. in debt when Fonterrible paid out $ 7.90 /kg milk solids ... 2 years later , at $ 4.55 /kg , they were bust ... receceivership sales in 2009 of their 22 farms....

Oh ... what a fun time that was .... hey RBNZ , keep the OCR down ... to do it all over again would be orrsome ...

(a low OCR needs to come with other monetary teeth. At the moment it comes with a gentle gumming)

. . as much as one does enjoy a gentle gumming , one suspects that there's gonna be a more vigorous gnashing of teeth if or when the next recession hits ...

They say that when the financial tide goes out we can see who's been swimming naked ... methinks there's gonna be alotta bloated nudies flopping around in the silt and mud ...

"Orrsome". I saw what you did there...

“we drop interest rates to support the indebted and they see that as a ‘buy’ signal.” That is the nub, that is the rub, exactly expressed. And that is the root of the financial disaster that is potential for those that are sucked in to borrow just because they can. To encourage borrowing to encourage spending to encourage the economy is about as self defeating as building a house without foundations. And NZ is going pig deep into it, it seems. For decades successive governments have bemoaned NZr’s poor saving records. Now NZrs are being encouraged to borrow! What exactly changed?

it's the leverage. My neighbours farm just got sold to other neighbour, I hear 4.2 mil. I doubt purchaser had the cash, will have borrowed against existing over valued asset. The banks want to keep these assets high or head office starts asking difficult questions.

Meanwhile we lose another family farm, to a farmer on his way to being TBTF. We desperately need to reform the tax system to stop the speculation in what is seen as safe assets, as they come with very low returns.

Aye and at all levels of commerce. For instance, a panel beater who bought the premises next door. Took a bit to connect it all up and equip, borrowed for all of that because he could and his bank “exec” provide a “plan.” But the market in the locality is getting to be pretty limited, new business is most unlikely. Perhaps a big Insurance agreement? Perhaps sharp quotes? Perhaps, perhaps, perhaps!

$ 4.2 million ? ... c'mon AJ .. that's just chump change if you have a couple of cows and an old Toyota ....

... the moment that Helen Clarke agreed to Fonterrible's establishment as a farmers' co-op we had a TBTF monopoly on our nation's hands ...

Exactly Andrewj. And that financial collapse is getting closer by the day. Sadly many think we are immune here in NZ.... we were ok last time so will be ok next time....

Your comment reminds me about the ancient marker stones in Japan that signalled where previous tsunamis had reached. Yet over time forgotten and ignored. How long since NZ Inc had to deal with really heavy fallout from global economic downturn? There's a bunch of financial types, politicians central and local who have not had to live through it here. How will they cope when we finally get caught up in it?

Maybe the Government should order banks to stop mortgage lending to housing investors other than owner-occupiers and new builds.

I think you mean 'encourage' not order!

And bang on time, Mauldin hits inboxes:

"We can and should take steps to protect our individual families and lives, but that’s not enough. At the national level, I’m beginning to fear only an enormously stressful Great Reset will deliver the deep but necessary sacrifices. "

https://ggc-mauldin-images.s3.amazonaws.com/uploads/pdf/TFTF_Dec_06_201…

Which TBTF the Government/Taxpayers will have to bail out first ? Farmers or Banking ? And when the crux comes, which will be bailed out first ? As they are so intertwined, both will be competing for the bail out. Are there enough resources and political/public will for that ?

It gets more interesting when you realise that farming is a NZ owned (mostly) operation, but banking here is overseas owned.

Who is thinking of drafting a OBR for a Farming crisis ?

Farming productivity gains are getting difficult to find. We used to get real returns, a dollar invested returned 10, then 5 dollars returned 10, and finally where we are today $9 returns ten but keep your fingers crossed the Chinese keep buying and low interest rates keep getting backed by RB and Govt, we sacrifice a generation .

Dairy farmers are looking at an $7 payout and cows are producing between 380 and 420 Kg's of milk solids each. Those cows are producing $2800 of milk each and 2 of them to a hectare. The income is good but the costs are horrendous, no none kept control of the costs, add regulation to that and it becomes a deadly mix.

Of course the banks would rather lend to housing. Thats where we can really see the problem in the economy, the profit motive in the banking system built around the creation of debt.

It's being going on a long time but like always greed is the ultimate undoing. Banks profits are related to debt, the more debt the better the profit. Lower interest rates just require more debt to make the same return, banks can create that with the stroke of a pen.

Our economy is built around this availability of credit. Unfortunately it pushes out creativity and innovation, unevenly benefiting those speculating in unproductive assets over those wanting to set up new business.

Eventually you get to where we are today, which is an impossible reset, without destroying a generation of home buyers. just to shake down the banking industry who have ruined our economy, it's like the end of the movie 'Hunt for Red October.'

We are now all in this together we all have ' skin in this game'.

Yes that old benchmark “productivity.” Old hat topic of interest. Easily forgotten. That is until the dust settles.

Hear that sucking sound as the big 4 banks pulled $5billion+ in profits out of the economy last year.

The only thing that keeps the ponzi alive is ever expanding credit and the banks and RBNZ know that. That is why the banks are squealing as the RBNZ slowly tries to deflate the bubble. Unfortunately, at every turn they are fighting the ponzi cheerleaders and their vested interests.

In the most optimistic scenario the RBNZ will engineer the market to flatline for a decade or more so the debt can slowly and less painfully unwind. Unfortunately, given the international headwinds, I suspect they may be overtaken by greater forces. A global recession will be a very stark reality check for the majority of New Zealander's who bizarrely believe they are immune to the rules of economic cycles and "irrational exhuberance".

. ... the only thing worse than that sucking sound is when they pass out the oranges at the Ryman village and none of the oldies have their false teeth in ....

SSSSSHHHHHLLLLLLUUUUURRRRRPPPPP !

'banks would rather lend to housing'

Our bank is strongly encouraging us to borrow more to finance an expansion opportunity in a largish family owned business. We've decided not to because of the uncertainty created by Ardern's nuclear moment coalition making noises about intervening in our sector but if banks are rationing credit we aren't seeing it.

There is quite a bit of that sort of unsavoury activity about. Especially if the bank perceives that this there is good collateral available. For instance in extended family young relatives have worked really hard for some years to reduce their mortgage, while on the other hand the value of their house has risen. Hence plenty of equity. So the bank is suggesting, not overtly though, not in writing, now is the time for a bigger house, a better car, take an oveseas holiday, you can afford it, you deserve it.

She did you a favour then..

And farmers feel they are being treated as a disposable after-thought. After all, banks get to construct their own discounted risk weightings for housing lending, but must keep a full 100% of risk-weighted capital for rural lending. Clearly banks will prioritise residential housing housing when the rules are set like this.

Inevitable:

by Audaxes | 21st Oct 19, 2:40pm

One of the key arguments behind the RBNZ's bank capital proposals is that through such material increases to regulatory capital the downside from a banking crisis would fall more on bank shareholders and less on taxpayers. Thus despite the existence of the OBR policy and planned introduction of deposit insurance, making banks hold more capital, thereby forcing their owners to have more skin in the game and be less highly leveraged, holds appeal for when the next financial crisis hits.

Banks can achieve a targeted capital adequacy ratio by raising capital or reducing assets. So for any imposed capital adequacy ratio c/a*, a higher cost of capital cc is likely to encourage banks to lower bank credits outstanding CR, in order to lower the denominator of the capital-asset ratio c/a (equation (12)). Link

A reduction in outstanding credit to those sectors that contribute to GDP (higher RWA capital demands) versus those that don't, i.e. house flipping (lower RWA capital demands) could have catastrophic economic outcomes.

Anecdotal evidence has emerged in the form of low LVR (~25.0%) farm owners in receipt of bank requests to pay down the mortgage one way or another.

Let's evolve the discussion in respect of Gareth's, "One of the key arguments behind the RBNZ's bank capital proposals is that through such material increases to regulatory capital the downside from a banking crisis would fall more on bank shareholders and less on taxpayers.", observation above:

In reality the money supply is “created by banks as a byproduct of often irresponsible lending”, as journalist Martin Wolf called it (Wolf, 2013). Thus the ability of capital adequacy ratios to rein in expansive bank credit behaviour is limited: imposing higher capital requirements on banks will not necessarily stop a boom-bust cycle and prevent the subsequent banking crisis, since even with higher capital requirements, banks could still continue to expand the money supply, thereby fuelling asset prices: Some of this newly created money can be used to increase bank capital (Werner, 2010). This was demonstrated during the 2008 financial crisis.

5.2.1. How to create your own capital: the Credit Suisse case study

The link between bank credit creation and bank capital was most graphically illustrated by the actions of the Swiss bank Credit Suisse in 2008. This incident has produced a case study that demonstrates how banks as money creators can effectively conjure any level of capital, whether directly or indirectly, therefore rendering bank regulation based on capital adequacy irrelevant: Unwilling to accept public money to shore up its failing capital, as several other major UK and Swiss banks had done, Credit Suisse arranged in October 2008 for Gulf investors (mainly from Qatar) to purchase in total over £7 billion worth of its newly issued preference shares, thus raising the amount of its capital and thereby avoiding bankruptcy. A similar share issue transaction by Barclays Bank was “a remarkable story of one of the most important transactions of the financial crisis, which helped Barclays avoid the need for a bailout from the UK government”. The details remain “shrouded in mystery and intrigue” (Jeffrey, 2014) in the case of Barclays, but the following facts seem undisputed and disclosed in the case of Credit Suisse, as cited in the press (see e.g. Binham et al., 2013):

The Gulf investors did not need to take the trouble of making liquid assets available for this investment, as Credit Suisse generously offered to lend the money to the Gulf investors. The bank managed to raise its capital through these preference shares. Table 11 illustrates this capital bootstrapping (not considering fees and interest).

Since it is now an established fact that banks newly invent the money that is ‘loaned’ by creating it out of nothing, the loan to the Gulf investor created (in step 1) a simultaneous asset and liability on the bank's balance sheet, whereby the customer's borrowed money appears as the fictitious customer deposit on the liability side, of £7bn. Considering the same change in step 2, but now after the liability swap, we see that the newly issued preference shares boost equity capital: They are paid for with this fictitious customer deposit, simply by swapping the £7bn from item ‘customer deposit’ to item ‘capital’. Credit Suisse is then able to report a significant rise in its equity capital, and hence in its capital/asset ratio. Where did the additional £7bn in capital come from? Credit Suisse had lent it to the investor, using its own preference shares as collateral, and hence had invented its own capital. The risk to the borrower was also limited if the Credit Suisse shares, not other assets, served as collateral. Link

Greater fool shareholders and OBR at risk depositors are always 100% exposed to boom-bust asset price cycles caused by poor bank lending practices.

Blimey! Thanks. Now that is highly educational. One tended to think, obviously naively, that this sort of money go round was in a the sort of arena where you would find the like of Trump, Enron etc. Definitely not.

"Top executives at Barclays agreed to lie about the payment of hundreds of millions of pounds to Qatar in 2008 in order to secure “vital” investments for the bank and avoid a public bailout"

https://www.theguardian.com/business/2019/oct/08/barclays-bosses-lied-a…

That 'hundreds of millions of pounds' wasn't the Capital 'raising' of course. That was £11 billion. It was the 'commission' paid to Qatar for being so good as to lend a hand in a time of need. (and I'll wager, partially backdoored to Barclays officers for their efforts).

And yet it seems the bank has escaped prosecution - Barclays avoids trial over £6bn Qatar rescue package

The Old Boys Network in action, as always. Banks thrive on that code.

An assumption that the judiciary is corrupt doesn't lessen the reality that Barclays Bank has not been found guilty of the charges the Serious Fraud Office brought to trial.

And then they got the world cup. (/tinfoilhat)

Buyer's credit and Seller's credit like these are very common in trades, both domestically and internaionally. Banks at both ends finance such deals.

That it has crept into capital build up is a twist, because no productive asset is created, but corrected by the Central Bank by not recognising it or laying stricter rules to track the origins of actual capital increase by fresh funds. I hope RBNZ is smart enough to do that.

Asb has just dropped half dozen rural managers in SI, Timaru office staffing level halved ? Staff across rest of county also moved on existing staff are also leaving company. Used to be progressive and forward thinking with great team culture, Asb and anz seriously pulling back,the Dutch co op bank may be pick of them moving forward?

RABO spent the last few years dumping vulnerable clients to banks like ANZ and Heartland. Just don't get on the wrong side of them, they are unforgiving.

The second to bottom graph has the wrong title block on it, its the same title as the one below it. Should it be "Year to June 2019"?

yes, sorry

fixed now

"Urban housing is not a productive sector..."

Well, if supply constraints limit opportunity to pursue meaningful careers or employment in cities is that not lost productivity? Gisborne averages $41k of GDP per capita and Wellington about $72k. Shamubeel Eaqub has often argued that lack of access to affordable housing is likely acting as a handbrake on economic growth.

Article in today's Telegraph( UK):

"Its main industry is in freefall. Its political system is descending into chaos. The banking system is in crisis, and consumer demand is stuck in the doldrums. Which country? It is, of course, Germany"

And a good response from a reader, and one we could take on board:

German economy is a powerhouse, the UK can only look at in envy because they want to be an economic powerhouse but don't want to copy their policies. ie. strong takeover laws, state aid for industry and banks that lend BIG money to manufacturing and startups.

They own all their industries, they are not slaves like us, whose Government allows UK industry to be sold off to foreign buyers.

The Germans will go through ups and downs, but they always come back because they control their own destiny, unlike the UK which puts its destiny in foreign control.....the UK economy will never overtake the German one. Won't come close, not happening, The UK economy is built on the housing market and retail....Until the UK has its own powerhouse world-leading car makers, train makers, steel companies and other manufacturers then it will never happen. At the moment we depend on the generosity of foreign industry just like China does. An economy built on sand.

https://www.telegraph.co.uk/business/2019/12/07/germanys-economy-deep-t…

""... will go through ups and downs, but they always come back because they control their own destiny, unlike the UK which puts its destiny in foreign control ..."" Replace 'UK' with 'NZ'.

The 2000's and the days of forged signatures and credit swaps are looking pretty harmless compared to those numbers...good lord, how is the sector going to dig itself out of that?

Farmers are worried. If your business model is built on maxing credit out to the limit you will always be worried.

Try having equity.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.