By Gareth Vaughan

'Too big to fail' is a saying popularised last decade when what became known as the Global Financial Crisis (GFC) swept the world's financial markets.

Basically it refers to a financial institution so important to the economy of a country that a government or central bank must take measures to prevent it from going belly up. Thus too big to fail financial institutions are often referred to as having an implicit government guarantee for their debts.

As a result of the GFC the American and British governments spent trillions of dollars and pounds of taxpayers' money propping up their countries' respective financial systems believing that the alternative, letting big banks and insurers collapse, was worse. Here in New Zealand our big financial service providers survived the GFC, albeit not without assistance. But more on that later.

The too big to fail dilemma has exercised the minds of many a regulator over the past decade. The Financial Stability Board, an international body that monitors and makes recommendations about the global financial system, has published an annual list of global systemically important banks since 2011. This is designed to address the systemic and moral hazard risks associated with systemically important financial institutions, with higher capital buffers required for entities included on the list since 2016.

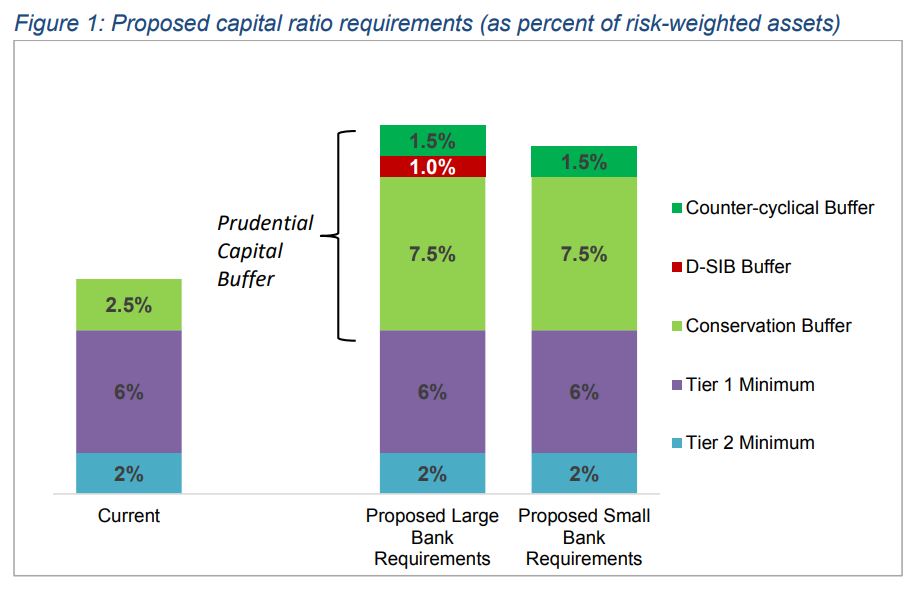

Closer to home as part of its proposed increase to banks' regulatory capital requirements, the Reserve Bank of New Zealand (RBNZ) has developed a framework for domestic systemically important, or too big to fail, banks. The RBNZ says this will cover ANZ NZ, ASB, BNZ and Westpac NZ who combined hold around 88% of both assets and liabilities in the NZ banking system. Given their size, it's proposed these four Australian owned banks will face an additional capital impost above and beyond what's required of other banks.

'They sailed through because everyone else was paddling like mad'

In a recent RNZ interview RBNZ Governor Adrian Orr attacked the often touted line that NZ's big four banks comfortably survived the GFC.

"I keep hearing this analogy 'oh, the Aussie banks sailed through [the GFC], we're safe.' And that's just wrong. They didn't sail through," Orr said. "They were 100% government guaranteed. New Zealand had about [a] $140 billion underwrite for the banks [the Crown retail deposit guarantee scheme], so we had to step in and have that underwrite."

"The Reserve Bank bought $8 billion of assets off the banks themselves to provide liquidity overnight almost blindfolded having to do it, because of the crisis. [There was] $10 billion of wholesale guarantees for their borrowing offshore, and they [the RBNZ] cut interest rates by 575 basis points. And then the banks say 'we sailed through.' Well, they sailed through because everyone else was paddling like mad," Orr said.

He went on to attack the subsidising of banks by governments/taxpayers/broader society, addressing the old chestnut of big corporations, having enjoyed privatising profits in the good times, then socialising losses when the tide goes out.

"This concept of too big to fail means that I can, as the agent not the owner of the capital, keep pushing and pushing and pushing to maximise the return. And if it [the bank] fails well that's bad. But I'm out. I've made my money, I'm gone. Meanwhile society can pick it [the tab] up. Society too quickly forgets the cost of financial crises and the costs are huge. The costs aren't just the financial price of rebuilding the bank. You have lost often a generation of employment opportunities, you have mental health issues, you have societal exclusion. You look at some of the challenges going [on] around the world globally at the moment. A lot of it is the tail end of the financial crisis," Orr said.

In the post-GFC United States the Occupy Wall Street movement sprang up after the Government bailed out banks rather than homeowners and failed to jail bankers. Arguably this contributed to sections of the population losing faith in authorities and the establishment, thus contributing to the election of Donald Trump as president in 2016. Of course we've also witnessed billions of dollars of quantitative easing, or money printing, from central banks, negative interest rates and a European sovereign debt crisis.

Crisis options & safety nets

One bank failure tool the RBNZ has at its disposal is the Open Bank Resolution Policy (OBR). The RBNZ has argued the OBR could facilitate "a rapid and orderly resolution of a bank failure" without changing the basic legal framework around ranking of creditors in a wind-up or insolvency. Under OBR a troubled bank would be placed into statutory management. The statutory manager would freeze the bank’s liabilities including deposits. The idea would be to release customers' transaction accounts as soon as possible.

The way I've always looked at OBR is it might be used if one of NZ's smaller banks got into isolated trouble. However if one of the country's big banks was in trouble, or there was a systemic issue, it's hard to imagine the Government would allow the RBNZ to use OBR. Rather the Government would probably feel the need for a taxpayer funded bailout. Especially if an Aussie owned bank or banks was/were involved and there was pressure from Canberra.

The Government is also looking to introduce a deposit protection regime as part of phase two of the RBNZ Act Review. The proposal is for the regime to include a limit of between $30,000 and $50,000. NZ is currently an outlier among OECD countries in not having deposit protection.

One of the key arguments behind the RBNZ's bank capital proposals is that through such material increases to regulatory capital the downside from a banking crisis would fall more on bank shareholders and less on taxpayers. Thus despite the existence of the OBR policy and planned introduction of deposit insurance, making banks hold more capital, thereby forcing their owners to have more skin in the game and be less highly leveraged, holds appeal for when the next financial crisis hits. A key part of this is addressing the too big to fail, or implicit guarantee, issue. With breaking up too big to fail banks not on the agenda, I believe this is an aspect of the RBNZ bank capital proposals worth cheering. As is the regulator's plan to reduce the favourable capital position the four Australian owned banks enjoy over all other NZ banks.

*The RBNZ table below outlines its proposed changes to bank regulatory capital requirements. Note, D-SIB stands for domestic systemically important bank. Kiwibank, The Co-operative Bank, SBS Bank and TSB argue the D-SIB buffer should be 2% not 1%. For background, context and detail on the proposals and bank capital in general, and the nuts and bolts of what's proposed, see our three part series here, here and here. The final RBNZ decisions in its bank capital review are expected in early December.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

34 Comments

" if one of the country's big banks was in trouble.... the Government would probably feel the need for a taxpayer-funded bailout."

Of course. There really is no other viable alternative. Let, say, ANZ 'go' and there won't be a banking system left to OBR anything else into!

Great article Gareth.

You raise some objective points, like why should these big four banks enjoy a financial advantage above locally owned banks? They shouldn't, especially when they display bully tactics, indicating they would increase the cost to borrowers and/or pull out of NZ.

I was at a seminar recently, where an economist from one of the big four was raising these prospectives. I advised doesnt the market set the price to borrowing; there are other lenders than your yourselves. The other question I asked was why would you pull of a market that gives you a 15% plus return on equity. And how do you justify 15% return anyway, when most large scale businesses are lucky to generate half?

Well, needless to say, he didnt answer the questions and couldnt sit down fast enough.

If you''re not aware of the latest games these US banksters: which own 65% of these big four through nominee companies, follow Trump on Aljazeera and see what power they have over other countries banking systems. They are OUT OF CONTROL!!!

"If you''re not aware of the latest games these US banksters: which own 65% of these big four through nominee companies"

Yeah, That 65% isn't the banks that own it, its customers of those banks. Thats sorta the point of nominee accounts..

Blind Trusts and Nominee Companies were first established under the Austrian Empire in the 1600's, to hide the true wealth and control some people have. Nothing has changed since.

While you might be right, it's not the banks themselves...

As controlling shareholder, who do you think directs their behaviour and has benefitted from it!!!

Thank you Joe Wilkes..

No brainer implement this straightaway.

No Brainer? that usually means its anything but....Orrrrrr is panicking...

Should be 100%, the sooner the better.

Actually, in an energy-descent scenario, the is an argument for increasingly more than 100%.

:)

Such a more reasoned set of arguements than the drivel published the other day attacking RBNZ and Orr.

Well Orr has been rather active attacking the rights of people to express other views.

.. as Fonterrible is arguably " too big to fail " ... yet they're on the cusp of doing so , thanks to managements incompetence and a bloated debt level .... they should diversify into banking ... Fonterrible Dairy Bank ....

Then , ask for a taxpayer funded bail out .... sweeeeet !

It has been suggested to Fonterra, as it would internalise the profit and allow them to run a more sustainable model.

With the suppliers they have, one would suggest they maybe able to offer a lending rate more attractive tha these other vulture capitalists. I understood Rabobank offer this up to the Dutch Farmers, who as a co-op own it.

This is one of the best things that's happened in recent time. Bloated bank profits and bonuses drives their irresponsible behaviour. After gfc they now just think respective countries will just bail them out...what a business model indeed, no risk and all reward.

Alternatively change the law to make all debts are null and securities released if they go tits up... aka put the risk back on them. Would change their risk management behaviour without doubt.

...and get their derivatives exposure back on the balance sheet for all to see!

...and get their derivatives exposure back on the balance sheet for all to see!

If you try to make changes to fast in any market to this extent when its for a forecast a one a 200 year event there is always going to be some push back.

One of the key arguments behind the RBNZ's bank capital proposals is that through such material increases to regulatory capital the downside from a banking crisis would fall more on bank shareholders and less on taxpayers. Thus despite the existence of the OBR policy and planned introduction of deposit insurance, making banks hold more capital, thereby forcing their owners to have more skin in the game and be less highly leveraged, holds appeal for when the next financial crisis hits.

Banks can achieve a targeted capital adequacy ratio by raising capital or reducing assets. So for any imposed capital adequacy ratio c/a*, a higher cost of capital cc is likely to encourage banks to lower bank credits outstanding CR, in order to lower the denominator of the capital-asset ratio c/a (equation (12)). Link

A reduction in outstanding credit to those sectors that contribute to GDP (higher RWA capital demands) versus those that don't, i.e. house flipping (lower RWA capital demands) could have catastrophic economic outcomes.

Anecdotal evidence has emerged in the form of low LVR (~25.0%) farm owners in receipt of bank requests to pay down the mortgage one way or another.

Unintended consequences....perverse incentives abound. Such is the world in which we live.

I really like Orr. To me he seems like a rear bread these days; intelligent, but can think for himself and challenge text book wisdom.

His 50 bps OCR drop was genius in my opinion and made a much bigger dent in interest rates than the endless 25 bps drops were achieving.

It was a committee decision, not his alone.

I prefer to take my slices from the front of the loaf, not the back.

It is strange that the RBNZ has to fight this hard to do its duty, the duty it has been tasked with, that is, regulating banks and ensuring they are always in good trim, with enough capital/reserves to withstand adverse conditions. It is tragic that 4 banks owned by foreign entities feel so entitled to operate here with no regard for the regulator. The RBNZ has to make sure that the financial system remains healthy and Orr needs to be supported in his attempts. I wish the Government of the day would come out vocally on his side, instead of showing an appearance of being cowed down by the Big Aussie Banks.

Nice to see a counter balance to Geof Motlocks spiel last week where he basically said the RBNZ should butt out as the Aussie banks are good people and will look after NZ when the SHTF.

Great article Gareth. Nice to see someone bring it all together, and summarise it succinctly. And yes you have to love Orr - tells it as it is, goes against the political wisdom, moral courage, integrity, stands up to bullies - I can't see how he got his job!

It is just so much simpler to have the capitalist system, where banks can go bankrupt. But anything to avoid that.

Well,Gareth, I can guarantee that Michael Reddell (Croaking Cassandra) will have something to say about the Orr based demands. While I otherwise admire much of his meanderings, I side heavily towards your argument that the Australian banks are just too full of their own importance and if they left one by one other overseas and locals would step into the breech. It still sticks in the craw how ANZ took over and were able to ruin the very high regard that National Bank was held particularly by its then customers plus the egregious imposts they put on their staff to up sell to their clustomers.

.

"I keep hearing this analogy 'oh, the Aussie banks sailed through [the GFC], we're safe.' And that's just wrong. They didn't sail through," Orr said. "They were 100% government guaranteed. New Zealand had about [a] $140 billion underwrite for the bank..

Wow.. plain and clear. !!

my worry is that will the banking sector can lobby to sack him out of the RBNZ post ??

For what it's worth,my view is that there will be some give and take in the final analysis. Orr has invested too much of his own reputation to fail now. I think a compromise will be reached whereby the additional capital requirement will be scaled back and the implementation period extended,perhaps to 7 years.

What nobody should forget is that the banks-at senior level-are simply not to be trusted to act in the best interests of anyone but their major shareholders. if anyone doubts this,just read Bad Banks by Alex Brummer or just look across the Tasman.

Of course,simply requiring them to hold more capital is not sufficient. The major banks should be split up with the Deposit taking side dong no other business and heavily regulated,in effect risk-free,while the Investment bank should be free to undertake any business however risky,be lightly regulated and with no ta-payer bailout possible. This is not a new idea-it was first proposed by the American economist Irving Fisher. It subsequently became known as the Chicago Plan. Since the GFC, it was the subject of a study by the IMF which found that this would lead to greater economic and financial study. Benes and Kumhof 2012.

Yes from an historical perspective going back to statistically, the move back to a high capital reserve is a good thing. Its just the speed and the theory that its for a 1 to a 200 year event that is basically questionable. Orrrrrrr... and other math guys went out on a limb and are now stuck in a battle that defines there careers. T o the point where they are accused of using heavy handed tactics that are not becoming of the office. History will write this story but with a country that is under performing its capital base im afraid it could be a perfect storm for Orrrrr...

When the waves are white caps out past harbour bar its the export traders that set sail and take the risks.

Central bankers never make for sailing the ocean blue....its trade or die ...

We have been through a financial crisis and now the world economy is stuck in a low growth trap. Over time very low interest rates will become increasingly ineffective at creating stimulus to the economy. Banking systems will be more severely at risk in another financial crisis. The US federal reserve lacks the firepower to deal with another dire situation like the subprime mortgage sell off. The NZ goverment would no longer be able to sell off the first 49% of state owned power companies in another financial crisis. Increasing the capitalization of the 4 major banks is an excellent idea, along with OBR and a deposit protection regime.New Zealanders want to feel that our money in bank deposits is safe.

"In a recent RNZ interview RBNZ Governor Adrian Orr attacked the often touted line that NZ's big four banks comfortably survived the GFC.

"I keep hearing this analogy 'oh, the Aussie banks sailed through [the GFC], we're safe.' And that's just wrong. They didn't sail through," Orr said. "They were 100% government guaranteed. New Zealand had about [a] $140 billion underwrite for the banks [the Crown retail deposit guarantee scheme], so we had to step in and have that underwrite."

"The Reserve Bank bought $8 billion of assets off the banks themselves to provide liquidity overnight almost blindfolded having to do it, because of the crisis. [There was] $10 billion of wholesale guarantees for their borrowing offshore, ...."

This is so underappreciated by many people. If the banks did not have the guarantee of the government, then they may not have been able to borrow funds - particularly in the commercial paper market from international investors. Then the banks would have had to cut back on lending, and the economic recession would have been much worse, business bankruptcies would have been higher, unemployment would have been higher, mortgagee sales of property would have been higher and property prices would have fallen much further.

Banks must know that if they lend recklessly or engage in high risk propriety trading activities ( taking trading risk with clients money for self enrichment ) that there is a MORAL HAZARD issue .

Bill Clinton overturned legislation to prevent banks from self -trading under pressure from lobbyists , and the consequences were inevitable as the banks engaged in more a more risky activities.

Banks must know they can fail , and act accordingly , and we DO need proper regulation AND strong capital adequacy.

The fox cannot be trusted to guard the hen-house

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.