By David Hargreaves

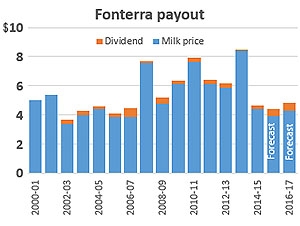

Fonterra has kept its forecast for the milk price to farmers this season unchanged at $4.25, but is picking an improved earnings per share range of 50c to 60c, up from 45c to 55c.

This means if the top of that EPS range was achieved, the payout - as things stand - could be $4.85, up from $4.30 in the past season, but still well shy of the breakeven point for many farmers.

A 3% reduction in milk collection for this season is forecast.

ANZ agri econonmist Con Williams in a commentary on the Fonterra update, said while there was still plenty of water to flow under the bridge the current milk price is only around $3.90/kg MS – "so some decline in the NZD/USD and improvement in international prices is required to achieve this forecast".

Fonterra separately also announced changes to its farmgate milk price manual.

The main change there as outlined in a reasons paper and the new draft manual is that Fonterra will now include the revenue from spot sales of commodity whole and skim milk powders and anhydrous milk fat in its Farmgate Milk Price calculation. This change will be incorporated into the 2016/2017 season Milk Price. Spot sales are referenced to GDT and are direct-to-customer sales in the global commodities market of products with the same specifications as those sold on GDT.

Fonterra said the estimated impact of the change on the farmgate milk price for the 2016/17 season amounted to an increase of 4c to 5c per kilogram of milk solids, based on analysis of the change over the past four years.

Fonterra made its current price forecast on May 26, at which time it also re-affirmed an expected price of just $3.90 for the recently completed season. Farmers are looking at their third consecutive season of potentially below break-even prices. See here for the full dairy payout history.

In the updated milk price statement today, Fonterra chairman John Wilson said the co-operative was aware "how tough the situation on the farm" remained.

"We are focused on delivering as much cash as possible to our farmers by bringing payments forward while maintaining a strong balance sheet," he said.

"This forecast is our best estimate at this early stage of the season. We will continue to update our farmers as we move through the season.”

Wilson said the $4.25 milk price forecast reflected the continuing global uncertainty and the high NZD/USD exchange rate, "which continues to impact the competitiveness of New Zealand dairy exports".

The recent weakening of the Euro currency, combined with the continued strength of the New Zealand dollar, had meant a price advantage for European export dairy products.

“We expect global milk supply and demand to come into balance over the course of this season.

"Farmers globally are producing less milk in response to lower prices and we are forecasting a 3% reduction in our New Zealand milk collection for this season.”

Fonterra chief executive Theo Spierings said the returns from the ingredients, consumer and foodservice businesses continued to grow in-line with Fonterra’s business strategy to convert more milk into higher returning products.

“We are seeing the benefits of our investments in manufacturing over recent years. We now have more flexibility to make the right products at the least cost, delivering better returns for our farmers’ milk.

“Our good progress in continuing to increase value through our consumer and foodservice businesses, particularly in important markets such as China, Malaysia, Indonesia, Sri Lanka, Oceania and Latin America, is reflected in the lift in the earnings per share forecast.

“Constantly improving the performance of our business is an absolute priority and puts us in a strong position to create more value for our farmers. We are generating significant improvements and cash benefits through our ongoing business transformation that contribute to both our Farmgate Milk Price and our earnings,” Spierings said.

Dairy prices

Select chart tabs

20 Comments

It seems more and more that the milk price manual needs a re-write to better reflect Fonterras sales over the past couple of seasons.

Their payout announcements are no longer in line with GDT prices, and increasing the dividend helps farm owners, but neglects sharemilkers.

Agreed.

The denial continues. Suppliers should add a substantial pinch of salt to the sugar coating emanating from NZ's largest (dis)organisation.

Is the balance sheet really that strong?

Magical thinking from Fonterra. There must have been some tremendous accounting acrobatics in order to force this result.

WMP prices have continued to fall, without sufficient NZD movement to offset. Talk of price recovery on the back of reduced European supply and increased Chinese demand is delusional fantasy stuff.

The predominant reason for this nonsense of a price announcement will be an attempt to delay the banks in calling in loans on high risk farms. Will the banks buy it? Probably not.

Yeah you would have to say cheaper interest rates are the key driver here ... otherwise banks wouldn't be so keen on any dividend payout

Begs the question, how much longer will debt financed asset sales in exchange for low return bank liabilities remain a practice acceptable to bank depositors. Are 1930's type bank runs in the offing?

During the five months [Aug 1931 to Dec 1931] when highpowered money rose by $330 million, currency held by the public increased by $720 million. The extra $390 million had to come from bank reserves. Since banks were unwilling and unable to draw down reserves relative to their deposits, the $390 million, amounting to 12 per cent of their total reserves in August 1931, could be freed for currency use only by a multiple contraction of deposits. The multiple worked out to roughly 14, so deposits fell by $5,727 million or by 15 per cent of their level in August 1931. It was the necessity of reducing deposits by $14 in order to make $1 available for the public to hold as currency that made the loss of confidence in banks so disastrous. Here was the famous multiple expansion process of the banking system in vicious reverse. That phenomenon, too, explains how seemingly minor measures had such major effects. Read more

It could be argued that we have seen the first bank run in the rush to invest spare cash in anything with a roof.

There has been an increase in media coverage around the risk of bank deposits and an associated increase in the public awareness of OBR. Although I note that many still think that OBR relates only to Term Deposits. When people realise that OBR applies to every last cent (de minimus notwithstanding) in every unsecured deposit account, all bets are off.

It will be darkly fascinating to see what happens if/when the pyramid shatters and Kiwis lose faith in both bank deposits and mortgages.

A bubble in mattress sales?

China may shatter the dairy industry milk pyramid if it's enmity towards Australia extends to New Zealand, given the former is our historical ally. Which way to jump and how high prime minister?

The state-run Global Times issued a scathing editorial calling for war between Beijing and Canberra if Australia continues to meddle in the South China Sea dispute.

Chinese state-run media declared Australia "an ideal target for China to warn and strike" if it ventured into the contested South China Sea in a scathing call for war laced with insults against the country. Read more

Banks collectively extended Fonterra credit to fund the payment? No matter it's still kicking the can down the road hoping the so far elusive unicorn of recovery will burst forth at a latter date.

I worked a season on a dairy farm in 2007, first time the milk solid price hit $4. The farmer was like a pig in slop. He had won lotto effectively. Look at them now - they are not business managers, their due diligence sucks. they should have planned for this eventuality, as should have the banks. I'm sorry, but I find it hard to sympathise with them.

Old, out of date experience.

Most farms with significant bank debt are on a three-monthly Come-to-Jesus meeting with their bankers, at which meetings current financials and updated forecasts are the prime focus.

Some are forecasting three years out in both cash and accrual terms, again at the explicit behest of the banks.

This is Business Management in spades - most self-employed tradies, by contrast, stick to the monthly bank statement (cash basis) and every so often run out of working capital Unexpectedly....

Considering the downside and history of the market and company is never old and out of date. In 2007 I learned Fonterra was selling it's technology overseas to anyone who would buy it. I realised that if they sold the technology to potential competitors, then sooner or later it would come on line, and NZ would have some problems. Hello World! Look what's happened!

China are now wanting our angus heifers. Advert in todays farming paper.

murray86 - are you trolling? The total payout was $5+ in 2001&2002 and has only being below $4 in in the 2003 season.

Was talking to a provincial town IT business owner - he said he is 80% down on revenue for the last financial year as relies on farmers for his business. This year is looking no better. If I was to follow your thinking I would say he's not a business manager and his due diligence sucks, and he should have planned for that. Bit like all the apprentices that have been laid off due to farmers not spending - their business owners must suck at due diligence too and didn't plan for this eventuality.

In other primary industry news, just heard Mathew Hooton on National claim that McCully to be fired over the Saudi sheep deal. Story's been rumbling for a while but the resumption of parliament should seal the deal.

Reason being that he misled the PM (cabinet). I thought blowing a bundle of taxpayer money for an as yet undisclosed reason (facing possible legal claim my a**e) would be enough.

While Fonterra is entitled to hold the current payout prediction, I can't help but feel sorry for a lack of facts reaching suppliers.

A drop in European milk production was due to what is technically known as a "Crappy Spring" ( http://ec.europa.eu/agriculture/market-observatory/milk/pdf/eu-raw-milk… ) . For every 1 kg MS NZ produces, they produce about 7. So they have a huge effect on our payout.

At the EU milk observatory website you can see that about half of a years worth of skim milk powder exports will be in a storage mountain. (they will have 350,000 t in storage and they export about 770,000t of SMP a year. So sooner or later both the storage program has to cease, and the surplus has to be sold. As Keith Woodford said, that storage program was probably worth 20c/kgMS to Fonterra last year.

I would love to know what specific data both Fonterra and Nathan Penny possess to back the idea that all will be fine by the end of the year. Are Algeria & Venezuela going to go on a WMP buying spree?

I suppose we all love a fairy tale where everybody lives happily ever after.

Tomorrow nights auction will be interesting.

Have a look at http://www.rbnz.govt.nz/financial-stability/financial-stability-report . There is an xl spreadsheet there . Down load that and look at sheet 2.4. One of the columns is GDT index in $NZ. Since February it's been below 100. The last time it sat there for any length of time was under 100 was last year ($4.30kg incl divi) and 2003 ($3.70). It's a great yardstick to see how they are going relative to predicted payout.

or a lot easier to go here

Looking at tab B2, 2007 PE on dairy land - it looks like the credit crisis couldn't have come at a better time - irrational exuberance.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.