The Australian Prudential Regulation Authority (APRA) has released a strengthened prudential standard aimed at mitigating contagion risk within banking groups despite requests from banks to hold off until the Reserve Bank of New Zealand (RBNZ) review of NZ bank capital adequacy requirements is finalised.

Effectively APRA is reducing the ability of the big four Australian groups to inject more capital into their Kiwi subsidiaries meaning the subsidiaries, led by ANZ NZ, may have to reduce the size of dividends paid to their parents.

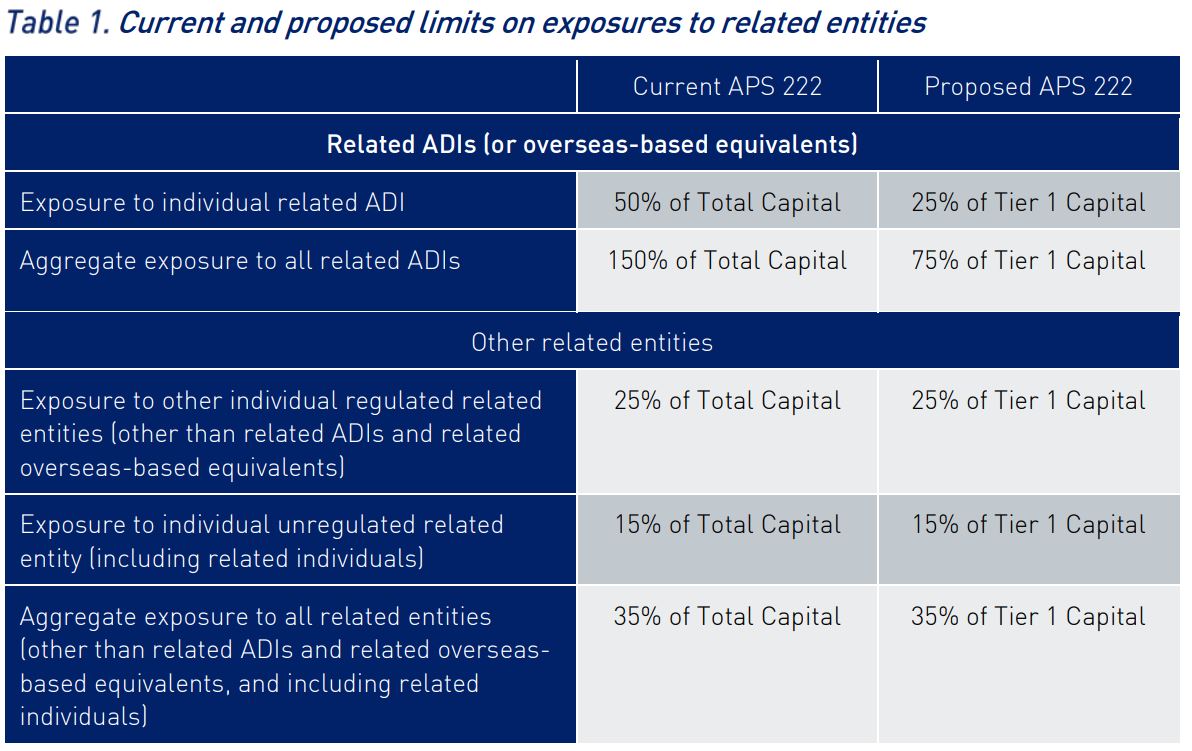

APRA confirmed it's dropping limits for Australian authorised deposit-taking institutions' (ADIs’) exposures to related entities, from 50% of Total Capital to 25% of Tier 1 Capital. It says this will further reduce the risk of problems in one part of a corporate group having a detrimental impact on an ADI.

Announcing the move on Tuesday, APRA noted its changes to related entity limits, in conjunction with the RBNZ’s proposed capital reforms, could affect the ability of Australian banks to expand their NZ operations without additional capital cost.

"Some submissions recommended that changes to prudential limits for exposures to related entities should be deferred until other considerations relevant to the capital framework are clarified, such as the Reserve Bank of New Zealand review of its capital adequacy framework," APRA said.

'APRA is not deferring its changes'

Those to lobby for APRA to delay its move included the Australian Banking Association. However the Aussie regulator pointed out the RBNZ consultation on "materially higher minimum capital requirements" for NZ banks began after the release of APRA's July 2018 discussion paper.

"APRA is not deferring its changes to related entity limits until the RBNZ finalises its proposals. The changes to [prudential standard] APS 222 are important elements of APRA's ADI framework and apply to operations across jurisdictions and structures. APRA recognises that the limits being adopted in APS 222, and indeed the current APS 222 limits, could constrain the ability of some Australian banks to meet additional requirements to support their New Zealand subsidiaries."

APRA also said it's reviewing other relevant elements of its capital framework and will consult on these in the coming months. This includes "the capital treatment of the parent ADI’s equity exposures to subsidiary ADI and insurance companies."

APRA's decision impacts the ANZ Banking Group and its subsidiary ANZ NZ, Commonwealth Bank of Australia (CBA) and its subsidiary ASB, National Australia Bank (NAB) and its subsidiary BNZ, and Westpac Banking Corporation and its subsidiary Westpac NZ. ANZ was first to issue a statement on APRA's decision. This is not surprising. Of the big four Aussie banks ANZ has far and away the biggest exposure to NZ at about a quarter of group earnings compared to about 10% at the other three banking groups.

Asked about the APRA move an RBNZ spokeswoman said; "We are in regular dialogue with APRA. Our capital review consultation will take into account all relevant information, including APRA’s most recent policy announcement. APRA’s decision is one of a range of considerations that will inform our final decisions. Other considerations include submissions received, meetings with stakeholders, and reviews by three external experts. All these inputs will help us to make robust and well-calibrated policies and decisions that best serve New Zealand’s interests."

'Limited capacity to inject capital into ANZ NZ'

In its statement, ANZ said the APRA move means it may have limited capacity to inject capital into ANZ NZ. ANZ said its exposure to ANZ NZ will be "at or around the revised limit" based on its current balance sheet.

"As a result, ANZ NZ may be required to retain a higher proportion of its earnings to meet any potential increased capital requirements and any future capital required in New Zealand may also need to be held at a group level."

However ANZ noted the final impact will be dependent on a number of factors, including the outcome of APRA and RBNZ consultations on required capital, and the size and composition of ANZ’s and ANZ NZ’s balance sheets at the time of implementation.

"While the change announced today is effective January 2021, ANZ NZ notes APRA’s statement that they are open to providing entity-specific transitional arrangements or flexibility on a case by case basis. ANZ NZ expects this flexibility could include the timeframe available and the circumstances under which an exemption may be available, such as periods of funding market disruption," ANZ said. (There's more detail from ANZ here).

As previously reported by interest.co.nz ANZ NZ paid $14.638 billion in dividends between 2009 and 2018. In its submission on the RBNZ's bank capital proposals ANZ NZ acknowledges a key factor in its estimate the proposed increases to bank regulatory capital requirements could shave up to 3% off Gross Domestic Product is because there's a transfer of wealth out of NZ from bank borrowers to banks' foreign shareholders.

ASB's parent CBA also issued a statement saying sufficient capacity exists under the reduced limits to accommodate CBA's exposures to its related entities including the additional capital requirement for NZ banks proposed by the RBNZ. A spokeswoman for BNZ's parent NAB said the APRA change doesn't trigger any extra disclosures from NAB, or BNZ. A Westpac NZ spokesman said the bank has no comment.

Announced in December last year, the RBNZ capital proposals would see NZ banks - led by ANZ NZ, ASB, BNZ and Westpac NZ - required to bolster their capital by about $20 billion over a minimum of five years. ANZ has said ANZ NZ could need between NZ$6 billion and NZ$8 billion of new capital to meet the RBNZ proposals.

For background and detail on the proposals and bank capital in general, and the nuts and bolts of what's proposed, see our three part series here, here and here. Additionally the RBNZ proposes to designate the big four as systemically important banks meaning they'd have capital requirements above and beyond other banks. Also see: RBNZ capital proposals threaten serious disruption to big bank shareholders' halcyon days.

Table 1 below summarises APRA's changes.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

16 Comments

Cue a general tightening of lending standards, as net profit is pumped into increased reserves, and new capital sought locally rather than via the Aussie parent.

"In its statement, ANZ said the APRA move means it may have limited capacity to inject capital into ANZ NZ". Yeah I'm not surprised about ANZ reaction after watch this very recent documentary. Exposing Australia's housing crisis | 60 Minutes Australia https://www.youtube.com/watch?v=AB6yM9puTY0

That was originally entitled "Bricks and Slaughter" and published last year. I recall TTP saying how irresponsible it was for 60 minutes to publish such a piece.

This only serves to highlight what Geof Mortlock (and I) have been saying on here for a while... APRA and RBNZ are simply not talking to each other. Its simply going to leave NZ customers with higher charges and ANZ NZ with a smaller business.

If there is any competition in the banking sector then another bank will step into any void left by ANZ NZ choosing not to provide capital.

If that is not the case then the ability of ANZ NZ to put higher charges to NZ customers is likely to be very limited, it can be reasonably assumed that they have already stiffed NZ customers with the highest fees and charges they can get away with.

" Its simply going to leave NZ customers with higher charges and ANZ NZ with a smaller business."

ANZ NZ with a smaller business is a good thing, if some/most of that business moves to smaller players. More competition in banking can only be good for the consumer, and frankly if it knocks ANZ below the to big to fail threshold that would be bloody great.

Charges as the other poster pointed out are limited by competition..they might desire to increase them, but it should cost them business unless the banks act in cartel like fashion and all raise their fees together.

Will this mean that the Aussie banks in NZ will have to retain their profits here to shore up the capital in line with RBNZ directives ? Then it is a good outcome and we should thank APRA.

Actually.. it'll mean the opposite. Retained earnings would be construed as capital and APRA would rather have the capital at home. It would actually put more pressure on the banks to repatriate earnings to the parent.

Only if it is above the prescribed limit. Even then the Aussies are not that stupid to drain off everything completely, because they know their NZ operations bring them heaps in dividends which is likely to continue.

But all this speculation and uncertainty should be sorted out by APRA & RBNZ getting together to work out a common and aligned strategy to face the coming hard times.

I think we can agree on that SmoKey. Seems like the RBNZ and APRA are so concerned with who gets looked after first when a bank fails. Surely it would make more sense to work together and ensure the capital standards are such that no ANZAC bank fails.

Following the ANZAC analogy, I would much rather see these two stand side by side as opposed to arguing who goes over the top first.

I am afraid that the next GFC may start with what happens on our side of Pacific, China and the Island nations included. Time for better co-ordination between Aussies and NZ, certainly. But the shock jocks are not helping, are they ?

Buffett looking for a home for billions in cash,maybe an offer to ANZ might be just what is required.

Buffet has the Fed in his pocket, he doesn't need any other bank.

If the Australian parent banks are unwilling or unable to inject any cash into their NZ bank subsidiaries, and there is a recession in the next few years resulting in lower bank profits (or even losses), what happens if NZ bank profits are insufficient to meet their RBNZ capital requirements by the deadline?

1) reduce risk weighted assets - which might mean a reduction in lending and business activities in areas where capital charges are high.

2) increase capital from other sources

3) ask RBNZ for an extension

APRA will know more about whats ahead than commentators here.

They are aware NZ is just; if not more, exposed to the overinflated property market than the Aussie market. NZ isnt quite advanced in the cycle as the Aussies. This measure is to reduce their exposure to potential loss making subsidiaries.

Banks operating locally are only lending to high equity clients now. Talk to the property developers. They know.

Real estate price revivals are typically lead from the lower price range, enabling the second home buyers to step up to the next prices bracket and so on. The last cycle was different, and driven by speculative off shore buyers who feed the middle and upper price range. In order to restart the cycle, first home buyers need to be able to afford the entry level property.

As the current entry prices are around the $500k mark, even using your kiwisaver it takes years to accumulate the 10% deposit. There will be some first home buyers that can get their quickly, but not the volume necessary to keep current prices afloat.

Haircuts are coming all round. You're just in denial if you think otherwise. I trust this advice finds as many first home buyers prior to purchase. Existing property owners can take the hits, and should be more prepared to do so.

With this in mind, November can not come fast enough. Banks (especially those controlled by overseas interests) need to increase their capital carrying requirements, so deposit holders funds are at less risk.

If they offer somewhat better and more reasonable rates to savers, Banks here can get more funds from NZ savers, to shore up their long term funding. But in the rush to short term gains, they are relying on cheap foreign funds, which may not remain cheap for long, due to the rating downgrade that may happen to NZ. In a sense this rate to the bottom in rates, is killing the golden goose, so to speak. Absolutely no long term vision for evolving Banking as a nation building activity, by all concerned, the Banks, RBNZ, the Government, et al. They have to just look back at how they got to be so big.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.