Finance Minister Grant Robertson is subtlety urging banks to keep their doors open to borrowers as the impacts of coronavirus get worse.

“The thing I want to guard against is banks using this [coronavirus] as an opportunity to deal with bits of their loan book that they’re finding challenging," Robertson told TVNZ’s Q+A programme on Sunday.

“I don’t think any New Zealand bank would do that.

“But it is important that for example, with the rural sector, which has pressure from drought as well, that actually banks are working with those farmers, working with those communities to make sure that they support them through this.

“Because at the other end, the New Zealand economy has still got strong fundamentals. Our primary sector is still producing goods people want to buy. And I just want banks and all industries - but especially that one - working together.”

Banks' dairy pull-back been happening for some years

Banks have been reducing their exposures to the dairy sector for some time, having lent up a storm in the past.

Just under 8.5% of all new banks loans written in January 2020 went to the dairy sector. This was a fall from 9.5% in January 2018, and 10.0% in January 2016.

According to Reserve Bank figures, dairy farm debt stood at $40.3 billion in January 2020, down from $41.6 billion a year earlier.

ANZ NZ's former CEO David Hisco in 2015 said that after the 2008 Global Financial Crisis, the bank's agri team worked hard to "exit people that we don't want to be with next time we get into a downturn". (ANZ is New Zealand's largest agri lender).

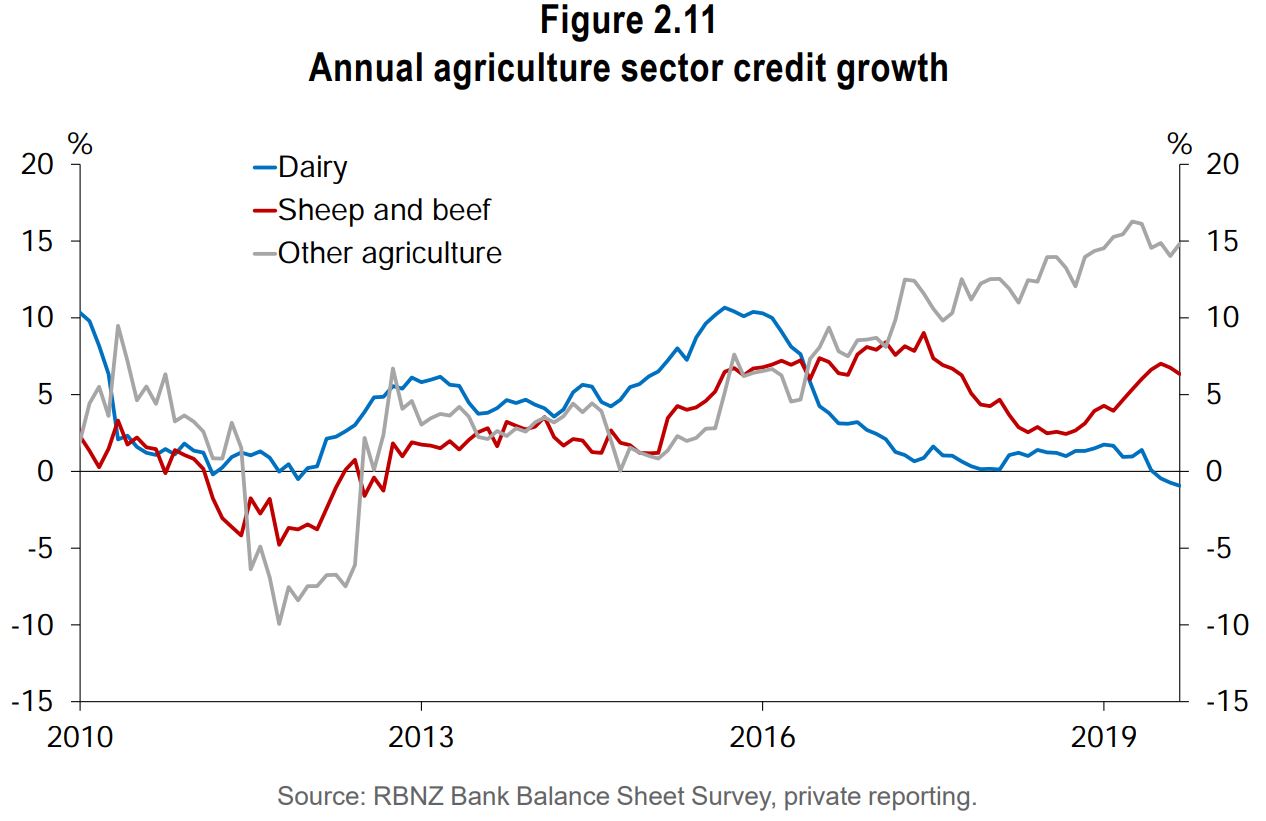

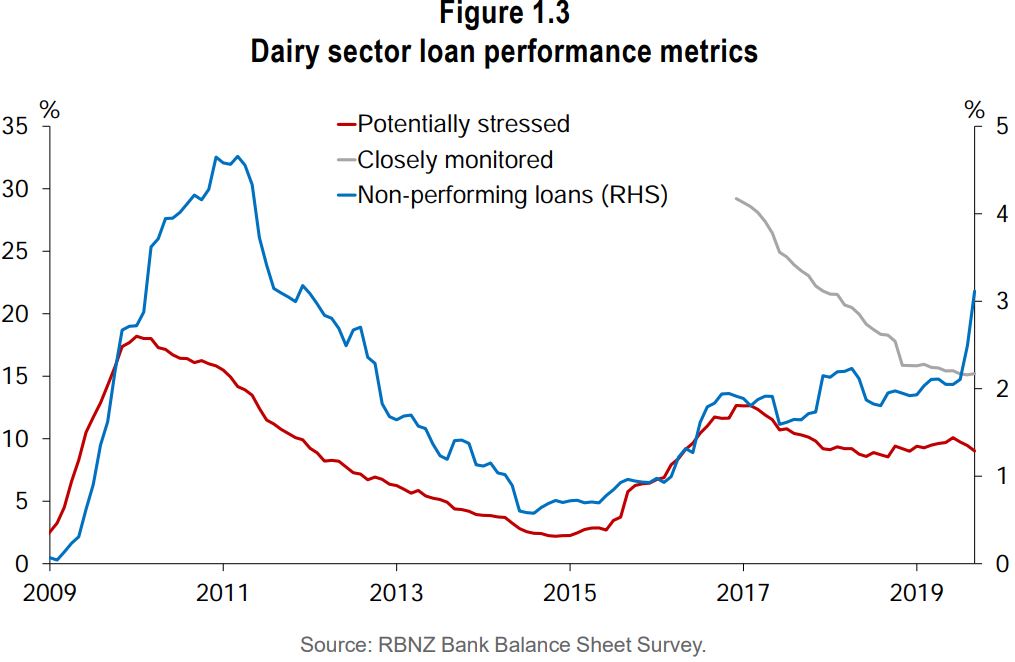

These charts, from the Reserve Bank's latest biannual Financial Stability Report released in November, show the reduction in credit growth and increase in non-performing dairy loans (recently largely driven by banks re-classifying loans rather than a deterioration in underlying loan performance):

Ardern: 'I think sometimes it’s good to get in front of things before they might occur'

Asked by interest.co.nz on Monday whether the Government had any reason to believe banks were using coronavirus as an excuse to further reduce their exposures to the dairy sector, Ardern said: “I think it’s a valid concern that we’ve seen an indebtedness within our agricultural sector; that we as a government are concerned about the ongoing financial wellbeing of our rural communities.

“And I think it’s only right that we continue to remind the banking sector of the obligations they have to the communities that they have lent to.

“None of us would want to see any rationale, any excuse for suddenly creating a difficult situation for those farmers which I think they have obligations to.”

Pressed on what was behind both her and Robertson making these comments, Ardern responded: “I think sometimes it’s good to get in front of things before they might occur.”

On Tuesday, interest.co.nz followed up with Robertson, who commented: “Businesses… and banks know each other well and they need to work together to make sure that they help support liquidity, support cash flow, because they’re actually in the most direct and best position to do that...

“There have been some concerns raised within the rural sector more broadly that they feel that banks might crack down on them. All I was doing [on Q+A] was making the point that we don’t need to do that.

“These are strong sectors. These are ones where there are good relationships between banks and their customers. And I’m just calling on banks and their customers - and indeed, employers and employees - to be talking to each other and making plans.”

Dairy farmers aren't seeing a coronavirus-inspired retreat now

Neither Federated Farmers’ President Katie Milne, nor Vice-President Andrew Hoggard, had seen evidence of banks using coronavirus to accelerate their pull-back from dairy.

The pressing issue for them is the drought and securing funding for feed.

Milne said the dairy sector was also more insulted from the impacts of disrupted supply chains caused by coronavirus than the meat sector for example, as milk powder can be stored.

RBNZ has warned against 'excessive risk aversion'

Robertson’s call for banks not to cut off “bits of their loan book that they’re finding challenging”, echo comments made by the Reserve Bank pre-coronavirus.

It said in November: “The current profile of dairy debt reflects a degree of poor decision-making by borrowers and lenders, but it is important that banks are not overly cautious when implementing new lending policies.

“Lending always entails a degree of risk but excessive risk aversion by financial institutions when risks crystallise can introduce unnecessary pro-cyclicality into the system, and despite the challenges in the sector, most operations will continue to be viable investments unless payouts decrease significantly.”

Interest.co.nz contributor, Keith Woodford, recently pointed out dairy farm values are in decline. He said "banks are now trying to figure out how they can get out of the mess they themselves helped to create. In the meantime, the banks are raising their interest margins on existing loans to compensate for the perceived increase in risk."

Woodford, formerly Professor of Farm Management and Agribusiness at Lincoln University, also argued many dairy farmers' financial positions are highly insecure.

While Fonterra forecasts it will pay farmers between $7 and $7.60 per kilogram of milk solids this season, economists have trimmed their forecasts due to coronavirus and the domestic drought.

Banks acknowledge ways they can help

New Zealand banks are stronger now than they were at the time of the 2008 Global Financial Crisis, as regulators are making them hold more capital and they've become less reliant on short-term offshore wholesale funding.

The New Zealand Bankers’ Association is urging those affected by coronavirus to talk to their banks. It said banks could help by:

- Reducing or suspending principal payments on loans and temporarily moving to interest-only repayments

- Helping with restructuring business loans

- Consolidating loans to help make repayments more manageable

- Providing access to short-term funding

- Referring individual customers to budgeting services.

59 Comments

Labour's Finance minister is renowned for eroding the role of Reserve Bank.

Grant Robertson is the one that should think carefully about some stimulus packages first....

Banks choose to purchase farmer's IOUs, not the government or the RBNZ - the latter could however introduce looser RWA capital requirements. But given banks only put up $8.00 of capital for every $100.00 IOU purchased there is not much wriggle room except to further expose bank IOU risk to depositors. The government needs to address the concerns of the latter rather than attempt to kick the can down the road.

Banks choose to purchase farmer's IOUs, not the government or the RBNZ....

Nail on head.

This is ridiculous. The government cannot in anyway decree what criteria banks require for collateral. On the other hand they can of course legislate priorities by restricting certain areas which would take things back to Muldoon and before. But to say you must lend to a certain sector regardless of risk is unheard of. Is the government then going to underwrite the loans? If so who then decides who is in and who is out? This government is haphazard and reacting on the hoof with club feet.

If so who then decides who is in and who is out?

Determined at central bank head office (BIS) and implemented locally with adjustments by the RBNZ - collateralised residential property lending leads the group with the lowest RWA capital demands - hence 60 % of bank lending is extended to the most creditworthy third of households for that purpose. Basically communist diktat.

“I think sometimes it’s good to get in front of things before they might occur.”

Hmmm how about compulsory quarantine of those people coming from China, Iran and South Korea instead of letting them go home to self quarantine.... That might have gotten in front of things..

Now we have real risk of community spread here in NZ

It a bit dry, forecast for 25 mls tomorrow but thats gone, looking like nothing more till the middle of the month. My fields are like flour, the bike puts up clouds of dust. Friend drives a for local trucking firm and he only got 25 hours work last week.

Yep it's going to get a lot worse with every week of the fall we miss, every week that little bit closer to winter.

So guy's when do I buy stock for my near empty farm? I didn't plan for this.

..skip the stock and grow some carbon. Sit back and cash the cheques, take up an internship the intdotcodotnz. Is that an option??

I thought about growing poplars they have to be no more than 22 meters apart, I can still graze under them and the taxpay sends me a cheque every month. Just the things that are too good to be true often don't weather well.

A fully stocked hectare of pine will sequester approximately 25 tonnes of C02 on average over their lifespan. I don’t think poplars will be much of a money spinner aside from helping your pasture and stock via shading and fodder.

It takes about four years before trees start to bring in decent carbon income as well. Can be worth while but there are definitely ins and outs to the whole thing.

"Friend drives a for local trucking firm and he only got 25 hours work last week."

If they have a 40 hour week, then that is a drop in income of 38%.

he can pick up work once the apple season starts.

Have you thought about getting the community together and building a dam to store water ? It could provide water for all the Townsfolk in Hawkes Bay,keep water flowing in the rivers in times like now and also be a source of irrigation water for farmers and horticulturists.

Be great if they could do it for 12c an M3 or less. I talked to an irrigator in Canterbury last week and that's around what he is paying. He's growing specialist seeds and is working for him, said he wouldn't want to be paying much more though.

Wairarapas proposed dam is .40c an M3, which I would think would broke most in the scheme,the cost overruns on the Nelson dam give an indication of potential cost blow outs. I would expect to have a contracted price, long term and locked in, before they started building, which means ratepayers would have to be on the hook for cost overruns.

HB's biggest problem is HBRC massively overallocated water takes to inefficient use dairy farmers, some consents over 10 million M3 and from shallow bores or surface takes.

It would also have to be done in a way that didn't breach nutrient limits , on my place that would be extremely hard. N limits would negate any advantage from irrigation, E coli limits for swimming are 260 and the stream here already runs as high as 570,000.

I also don't think any dam would be able to meet water takes in a year like this, any dam would have been dry by mid Jan.

My N cap has been set by hbrc at 10.

I assume those dairy farmers followed the law and now have property rights that they have full entitlement to. To say that water storage is a waste of time and too expensive is ridiculous. I note that a lot of maori land that has not been developed has had it's value destroyed by a dicky computer programme too and those guys are not going to take it sitting down,.I hope you get a good rain ASAP.

You seem to be confused, a consent to take water is not ownership, there may be a contractual element, but there is a mountain of fine pint on your consent.

I believe there is a Meta game going on under the surface. That is the ownership of fresh water resources in the hands of a few large corporates and elites. Regional councils appear to be involved, to see it in action I suggest you look into water bottling consents in HB.

If you set up a large dam that's going to be unaffordable if costs over run, then sell it to average farmers who then go broke or have stressed sales those farmers have born the brunt of the costs and it's now reflected in their asset values, it creates opportunities for others once the cost of the asset has has been adjusted.

I should add that I already have an irrigation consent.

Long term the banks want out, they know dairy will be replicated by low cost alternatives - in spite of the aghast outrages.

"Scientists at Ghent University in Belgium are experimenting with larva fat to replace butter in waffles, cakes and cookies, saying using grease from insects is more sustainable than dairy produce"

https://www.theguardian.com/environment/2020/feb/28/larva-fat-sustainab…

But is it as nutritious or appealing? I agree farming for production sake is under threat by cellular production for those that don’t mind consuming gmo product. However as I’ve posited to AndrewJ in another thread could such production threat be an opportunity for NZ to differentiate its product based on grass based nutrition added value and sustainable models?

I am loving my larvae 'ice cream' sooo creamy, it's like heaven is having a party in my mouth.

how many larvae in a latte?

No cholesterol, no lactose, I haven't felt this good since I ate fruitbat soup in Wuhan.

Larva fat, that's bloody disgusting.

What is wrong with people.

We grow good quality meat, veg, fruits and seafood here in our country.

Bunch of weirdo's thinking these foods are the future.

You can have it, I won't thankyou.

Rastus and Omnologo may be onto something here. I think insect-substitution for dairy will come about naturally as climate change gains momentum. As our flora succumbs to heat stress domesticated fauna such as the sheep and the cow will also disappear; but a new opportunity will then present itself:

This new agricultural era has already begun with the death of our Kauri trees. More trees will follow until the land is awash with rotting and rotten trees and other flora. This situation will provide the perfect habitat for the proliferation of our own edible insect: the Huhu bug which, I regret, I have tried only once in my life. Maori deemed the Huhu a delicacy and modern science has established that it is extremely nutritious.....more so than meat. I would advise our farmers to start substituting trees for paddocks straight away as research has determined that we only have 30 years at the outside before all flora begins to irreversibly decompose in this land. Thus a new agricultural industry will arise with huge export potential to China in particular where gastronomes abound seeking out novel nutriments. Entrepreneurs should register patents and trademarks as soon as possible; in fact I have already submitted an application for the trademark HB2 (Huhu Bug 2) to piggyback on our currently very successful, but ultimately doomed, A2 milk.

And don't worry about no more carbon removal by trees...the forests will still be here but they will be located in the current Antarctic.

We only have 12 months because the increase from a relatively small 0.03% of CO2 in the air into a whopping 0.04% CO2 in the air will cause everything and everyone to die. We must take action now so that global temperatures can stay stable forever.

Our one industry with any real global presence is finding our banks no longer want to lend to them owing to concerning indebtedness.

We don’t seem well prepared to withstand any shocks.

I don't think our banks are well placed to deal with shocks. Even the comment below points out they have overloaded on residential lending. At 70% they are not diversified.

I don't think our banks are well placed to deal with shocks. Even the comment below points out they have overloaded on residential lending. At 70% they are not diversified.

In a bygone era they may have been focused on partnering industry. This is the big difference between Japan and Anglo Saxonia (well at least in NZ). The Japanese banks still exist to support industry and the relationship is symbiotic.

They are not our banks. They are majorly owned by distant Hedge funds and Investment banks.

Exactly. The only bank I can think of that is somewhat better diversified is BNZ, where their business/agri lending makes up about 50% of "standard" loans (i.e. not wholesale or derivative exposures). When you look at some smaller banks, it's more like 80%+ residential......

If you are talking about JK/ANZ & the rest of OZ/NZ banks, if I were you at least in this impending look out doom & gloom, I would like to still eat the produce etc. (try not from made in China) - thus our more than century old, yet got more global market capitalisation as compare to that local boys above, would be my preferred choice as they concentrate on production land based lending - you name them, I would get censored here, as deem a promo or conflict of interest.

That is utter crap. If your equity is over 50 % there are banks out there keen to lend to dairy farmers. The old addage that if you have a dollar you can borrow a dollar is still relevant. Same with commercial property.

Some real issues here. NZ banks' primary business is based on assets that lie with with residential mortgages (approx 70%), not business lending. Robertson is talking like he has no idea of the the structure of the banking industry. Perhaps the govt needs to be the lender to the dairy farming sector if it wants to deal with this issue.

As a shareholder in those banks I would urge them to proceed with extreme caution given the increasing risk of a recession and lack of fiscal relief. We've had a very good run of credit expansion since the financial crisis but all economies need to restructure from time to time.

Not sure what that means. If you're talking about letting the dairy industry go, I think you'll find there will be strong opposition, even if only for sentimental reasons.

Banks cant win can they... beaten up on one hand and told to hold more capital... and now the government is asking for them to please keep lending and supporting the economy. Who'd be a banker?

At the higher echelons, scociopaths.

they were sociopaths when they were born, then morphed into psychopaths

The year on year record profits help soften the blow.

According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

The citizens are underwriting the whole endeavour for virtually nothing after inflation, whilst foregoing decent regular wages to do so. Banks are derelict in their duty to fund productive enterprise because official central bank regulatory capital requirements favour residential property lending for the creditworthy few.

{kind=link}

The property market plays a huge part in the NZ economy, employment and export dollars. The banks are doing the best thing by supporting this important industry and giving kiwis a roof over their heads.

Haha I love your comments.

"citizens are underwriting the whole endeavour".. pls explain

Why not reducing or suspending interest payments on loans and temporarily moving to principal-only repayments?

Why temporarily?

We are at a stage now, where the chances of interest being paid back are dwindling exponentially. So why not create the needed change?

Tired of these mealie mouthed politicians, especially finance ministers. Banks are not benevolent societies. If I was a bank CEO I'd give Robertson a two fingered salute. If Robertson is really that concerned then he can use taxpayer money and prop up the odd farm. I'm a depositor so I certainly don't want my funds at risk by slack lending.

Banks are not benevolent societies.

No they are not, but they are killing it in the return on capital stakes, with next to no skin in the game, at depositor's expense.

Don't disagree but its up to the regulators to set the ground rules and regs. Only just starting on better rules and regs.

It's up to the voters, but unfortunately individual political party membership has dwindled into obscurity, while corporate donor-ship has ballooned. It's now one dollar one vote influence at best.

Banks are not benevolent societies

They like to portray themselves as such. Reality is that the Anglo Saxon banking model ('lending into existence' with limited accountability) is the biggest rort in modern economic history.

Your funds aren't at risk from slack lending. Your funds are at risk because the banks use you to back their endeavors not their own money. They pay you a measly 2.5% while taking a massive 15-20% return.

So you think they should be able to operate freely as independent businesses under a capitalist system?

Me too. But I also think they have to accept the other side of the coin, which is that when they lend too much, they go under. Their shareholders lose their investments. None of this bailing-out nonsense.

Smell the fear.

Farming...what is that anyway? A sector on its way to the boning yard just like locally assembled Holdens in Australia...close a few farms and build houses on them instead....no one will cry. On my NZX alone this week nearly all my holdings supported their share price with buyback actions...and people whinge about low interest rates pushing up house prices....

The less we have to export the more we rely on our false internal economy of selling things to each other for increasing values to feel rich. Farming won’t be going anywhere anytime soon and nor would it be a good thing if it did.

Hmn.. I would be worried when they gave hints like this.. Covid19, slowdown, OCR down, but yet the banks started increase the deposit rate for 6mths onwards.. tax payer bail out? OBR? - damn, the long I stare at this bug on projected electron microscopic display.. the tricky part for theorising of slowing it down by manipulating certain avail inhibitors, yep.. human body is soo much clever on adaptation.. but this one really discriminate against the elderly.. I wonder.. hmm hmm.. Oh! may be the lowering OCR? will accelerate those worlds nations cyclic close down border for purpose of isolation, slowing goods movement. Menure to stimulate growth.. yea that's it.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.