By Gareth Vaughan

The COVID-19 pandemic, with lockdowns and closed borders, has increased focus on resilience, self sufficiency and community. It has also shone a spotlight on small businesses and regions facing tough economic times for the foreseeable future, in part at least, due to a lack of international tourists.

Against this backdrop is there an opportunity to bolster the resilience and self sufficiency of New Zealand's financial services sector?

One way of doing this could be through providing a leg up for mutually owned building societies and credit unions.

In the context of the overall financial system they're tiddlers. According to Reserve Bank figures, banks had total assets of $630.653 billion at the end of April. As of the end of March, non-bank deposit takers (NBDTs), including finance companies but not the ANZ owned UDC, had total assets of just $2.62 billion, of which $1.07 billion was held by building societies and $1.21 billion credit unions.

Despite their small size within the overall system, the likes of the Nelson Building Society and Wairarapa Building Society, plus the two biggest credit unions Credit Union Baywide and First Credit Union which each have about 60,000 members, are significant players in provincial parts of NZ.

First Credit Union, for example, has its head office in Hamilton, with branches in the likes of Ngaruawahia, Te Aroha and Kawerau which others have "cut and run" from, general manager Simon Scott says.

"We're quite happy servicing [them] but it's a reasonable cost to do that," Scott says.

The Hastings-based Credit Union Baywide grew last year through the acquisition of the struggling Auckland-based Aotearoa Credit Union, the central North Island centric Credit Union Central and the South Island's Credit Union South. Funded almost entirely by retail money, their profits go back into their communities due to their mutual ownership structure with customers/members the owners.

"Credit unions and building societies have very different drivers [from the big banks] by the nature of our business model. Our members are our core reason for being as both owners and customers. In essence, this means our primary motive is about our members and social good, not about maximising profits for shareholders," says Baywide CEO Gavin Earle.

They also "bank" some customers who the banks turn their noses up at, thus boosting financial inclusion by providing access to affordable financial products and services crucial for inclusion in modern society such as transactions, payments, savings, credit and insurance.

"We've got a very big philosophy on access to banking and access to products that means you can be part of your community," says Scott.

CEO Tony Cadigan points to a range of sponsorship and support the Nelson Building Society provides to about 260 community groups including the local rescue helicopter, the regional hospice, a foodbank, and the champion Tasman Mako rugby team.

"We're doing our bit, we really are," Cadigan says. "Without being called a bank we are this community's bank."

'Government should invest'

With access to more capital Cadigan says the Nelson Building Society could grow significantly. It currently has $880 million of assets.

"I would like to see the mutuals work more closely together and potentially share services. E.g. compliance functions," says Cadigan.

Regions such as Marlborough and the West Coast could potentially be attractive places for expansion, he says. However, Cadigan says Nelson Building Society's current focus is on strengthening its balance sheet with a low growth strategy.

Earle says access to capital is the biggest challenge and impediment to growth and building scale.

"Government should invest in the mutual sector who are owned by kiwis to help kiwis. This means we could serve more New Zealanders and see the benefit go direct to them and their communities," Earle says.

"Access to liquidity support from the Reserve Bank or other mechanisms would also assist, rather than having to rely on the big Aussie-owned banks," Earle says. "I’m keen to see some tangible actions from government to assist us at a time when we have real opportunities to help more kiwis."

By being an agency client of a major bank, the bank requires security, which then has to be taken out of the building society or credit union's liquidity and capital calculations.

"I believe the mutuals are an important and underrated part of the NZ financial service sector, with a great story to tell. A story that resonates well with communities in regional NZ," says Cadigan, adding the Reserve Bank "is listening and willing to work with Nelson Building Society, which is very pleasing."

Some NBDTs have tapped into the wage subsidy scheme

Some of the credit union sector had already experienced tough times before COVID-19 hit. Baywide last year acquired Co-op Money NZ, the struggling industry association for member owned credit unions. This was on the heels of Baywide's takeover of Aotearoa Credit Union, Credit Union Central and Credit Union South, which Credit Union Steelsands' members declined to join. The tie-up followed the introduction of an Oracle flexcube core banking system and serious financial strife for Aotearoa Credit Union.

In its May Financial Stability Report the Reserve Bank noted some parts of the financial system entered the COVID crisis already vulnerable.

"Some non-bank deposit takers (NBDTs) have low profitability and are operating with low financial buffers. There has been consolidation in the NBDT sector in recent years and this is expected to continue...The NBDT sector is small, representing 0.6% of total deposits, and has been regulated by the Reserve Bank since 2010," the Reserve Bank says.

The regulator went on to say that liquidity is a risk for NBDTs.

"Many NBDTs are almost wholly funded by retail deposits, with around half of credit unions and building societies’ retail funding at terms of less than 90 days...Many of the profitability challenges faced by the NBDT sector are due to lack of scale, with high operating costs relative to revenue."

"Some NBDTs that depend on customer transaction volumes experienced declines in revenues during [COVID-19] Alert Levels 4 and 3, with a number of NBDTs and related entities having accessed the Government’s Wage Subsidy Scheme...Further consolidation may be necessary to improve both the efficiency and stability of the NBDT sector," the Reserve Bank says.

Those who have received assistance from the Government's wage subsidy schemes to date are detailed in the table below.

| Non-bank deposit taker | Total amount received | Employees |

| Wairarapa Building Society | $91,384.80 | 13 |

| Westforce Credit Union | $201,028.80 | 29 |

| Asset Finance | $119,503.20 | 17 |

| Credit Union Auckland | $116.673.60 | 17 |

| Finance Direct | $56,236.80 | 8 |

| General Finance | $32,318.40 | 5 |

| Gold Bank Finance | $44,918.40 | 8 |

| New Zealand Employees Credit Union | $39,348.00 | 6 |

Sticking points for potential RBNZ support

In terms of potential liquidity support from the Reserve Bank, a Reserve Bank spokesman says there are operational rules, including an application process, described on the Reserve Bank’s website.

"There is no minimum size for counterparties, or restriction of the facilities solely to banks. However, counterparties are generally expected to be active participants in wholesale markets, and have an investment grade credit rating. It is worth noting that credit unions and building societies that met certain criteria were invited to be involved in the Business Finance Guarantee Scheme," the Reserve Bank spokesman says.

"We identified the vulnerability of some NBDTs in the Financial Stability Report to encourage a continued focus by the sector on building future resilience, given the potential for a protracted downturn in the economy. We noted that some NBDTs, and insurers, have relatively small buffers should there be material deterioration in the sectors they serve. On consolidation, We have had discussions with industry, Trustee Supervisors and other regulators but any consolidation will ultimately be up to the individual affected firms," the Reserve Bank spokesman says.

Typically building societies and credit unions aren't active participants in wholesale markets, and many NBDTs are exempt from requiring a credit rating. Of those that have a one, only Liberty Finance with a BBB- rating and the Police and Families Credit Union with BBB, have investment grade ratings.

NBDTs also have minimum capital ratio requirements, being the level of capital in relation to the credit exposures and other risks of the NBDT or its borrowing group. This ratio must be at least 8% for licensed NBDTs with a credit rating from an approved credit rating agency. For licensed NBDTs without a credit rating from an approved rating agency, the minimum capital ratio must be at least 10%.

'Enable us to support SMEs'

The Business Finance Guarantee Scheme supports the provision of new bank loans to viable businesses by the Government taking on the default risk for up to 80% of the loan.

The Business Finance Guarantee Scheme hasn't, however, proved successful. The latest New Zealand Bankers' Association figures show just $86 million has been lent through it to 503 customers. Because of this the Government introduced the Small Business Cashflow Loan Scheme, which is being administered by the Inland Revenue Department (IRD). Through this scheme firms with 50 or fewer full-time staff can borrow up to $100,000 of unsecured lending.

An IRD spokeswoman says the Small Business Cashflow Loan Scheme, which started taking applications on May 12, has now received 87,861 applications with 95% approved. About $1.4 billion has been paid out, with the average loan size approved $16.788.39. Applications for loans through the Scheme are scheduled to close on July 24. However, Minister for Small Business Stuart Nash hasn't ruled out extending this.

Earle argues it doesn't make sense for the Government to be in the business of lending to small and medium sized businesses (SMEs).

"I believe government should invest in NZ mutuals to enable us to support more New Zealanders and SMEs and thereby reduce our exposure to high dependence on the foreign-owned banks," Earle says.

As previously reported by interest.co.nz, building societies and credit unions weren't included in the government-Reserve Bank arrangements announced in March to enable banks to offer mortgage repayment deferrals. However, they have offered them anyway.

The Reserve Bank spokesman says Reserve Bank staff have been in regular communication with the NBDT sector both during and since the COVID-19 lockdown period, proactively monitoring developments.

"A letter sent to the CEOs of banks and NBDTs on 23 April outlined that there is no regulatory barrier to NBDTs providing mortgage deferrals under the Deposit Takers (Credit Ratings, Capital Ratios, and Related Party Exposures) Regulations 2010. The Reserve Bank is comfortable with NBDTs providing deferrals for mortgage lending, or any other type of lending that they provide," the Reserve Bank spokesman says.

What about the Provincial Growth Fund?

Prior to the 2017 election, NZ First leader Winston Peters was calling for a banking inquiry focusing on bank charges, the dominance of Australian owned banks in NZ, and bolstering NZ ownership in the sector.

A key part of NZ First's coalition agreement with Labour is the allocation of $3 billion for investment in regional economic development through the Provincial Growth Fund. Overseen by Regional Economic Development Minister and NZ First MP Shane Jones, could a slice of the Provincial Growth Fund be an avenue for government support for building societies and credit unions?

Arguably doing so would help meet the Provincial Growth Fund criteria of improving resilience, particularly of critical infrastructure, and diversifying the economy. As of March 31 the Australian owned ANZ, ASB, BNZ and Westpac held 89% of both NZ banking system assets and liabilities.

Is banking and financial services critical infrastructure? Especially through support of small business in the provincial heartlands and providing banking in areas where banks are pulling back from?

A spokeswoman for Jones told interest.co.nz any questions about support for financial institutions should be directed to Finance Minister Grant Robertson and the Reserve Bank.

A spokesman for Robertson said: “We’ve not considered them for this [the Provincial Growth Fund], and nor have they applied. The Provincial Growth Fund was set up for supporting project-based work, as opposed to background financial architecture.”

NBDTs & banks could be brought under the same umbrella

Meanwhile, phase two of the Government's ongoing review of the Reserve Bank of New Zealand Act is considering bringing all deposit takers, be they banks, finance companies, building societies or credit unions, under one umbrella, in place of having separate oversight regimes for banks and NBDTs. This could be along the lines of Australia's authorised deposit-taking institutions (ADIs) regime.

First Credit Union's Scott is enthusiastic about this.

"If you look like and feel like and quack like a bank you should be able to be called a bank," Scott says.

However, it's not clear that NBDTs would be able to call themselves banks if they were brought under the same regulatory oversight regime as banks. A government consultation paper says: "An integrated framework should be capable of supporting a variety of business models, provided core regulatory requirements are satisfied."

Under the current Reserve Bank regime the creation of Heartland Bank, after the merger of Marac Finance, CBS Canterbury and the Southern Cross Building Society in January 2011, which then gained banking registration from the Reserve Bank in December 2012, shows non-banks can become a bank. PSIS, now The Co-operative Bank, and the Southland Building Society, now SBS Bank, have also done it. But getting there is a long and challenging road.

NZ owned bank disappointed Reserve Bank capital changes delayed

Meanwhile, smaller NZ owned banks are also finding the COVID-19 world tough. As reported by interest.co.nz earlier this month, The Co-operative Bank, SBS Bank and TSB recorded combined March quarter losses of $12.7 million versus profit of $12.5 million in the March quarter last year.

CEO Donna Cooper says although TSB remains well-funded and capitalised, with liquidity and capital adequacy ratios well above regulatory minimums, the playing field between NZ owned and Australian owned NZ banks isn’t level. TSB is owned by the TSB Community Trust.

"For example, in residential lending we are required to hold on average 45% more capital than Australian-owned banks, for the same risk. That has a significant impact on how we operate compared to the Aussie banks, so we welcomed our regulator’s intentions to try and balance that. However, the implementation of the new capital requirements has now been delayed due to COVID-19. That’s a decision we understand because it enables banks to support customers, however, it does mean New Zealand-owned banks remain disadvantaged," says Cooper.

The new bank capital requirements were put on ice for 12 months at the onset of the COVID-19 crisis. The Reserve Bank proposes to allow banks to use redeemable perpetual preference shares to help meet new capital requirements, which NZ owned banks see as a new source of capital to help fund growth, although the details of these securities are yet to be finalised.

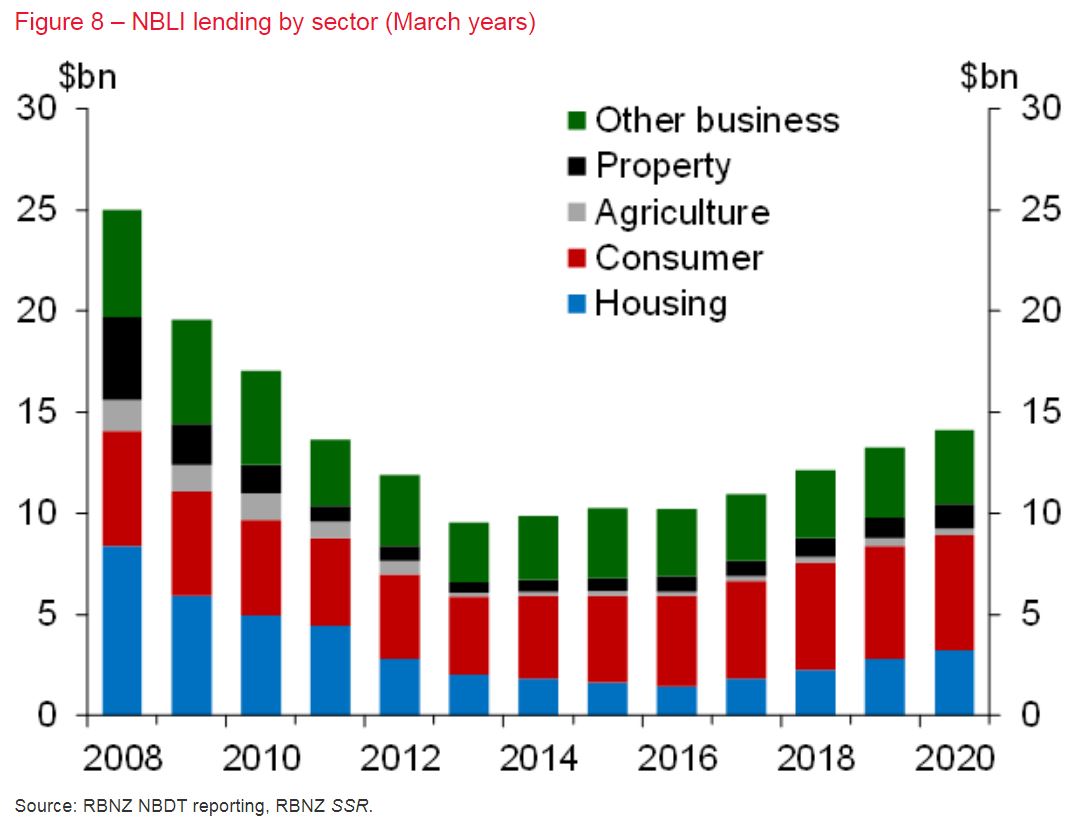

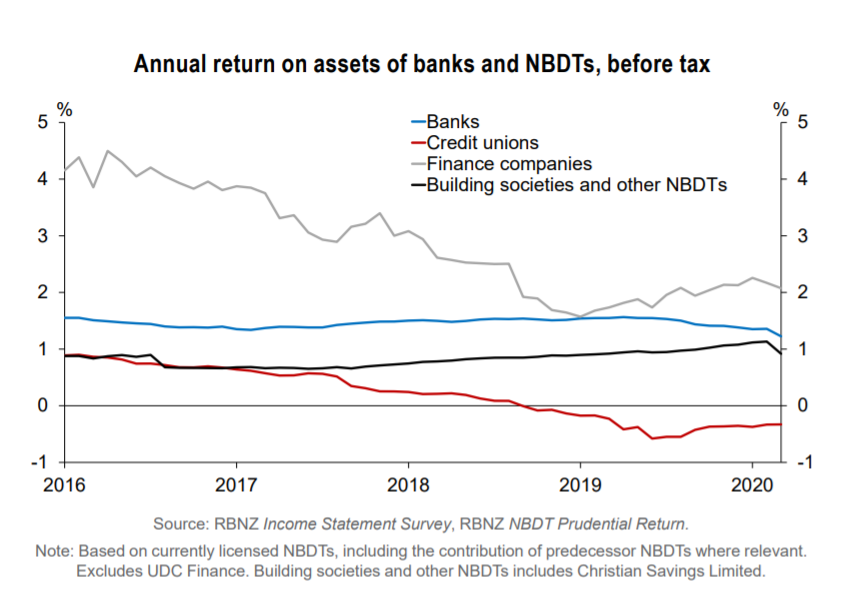

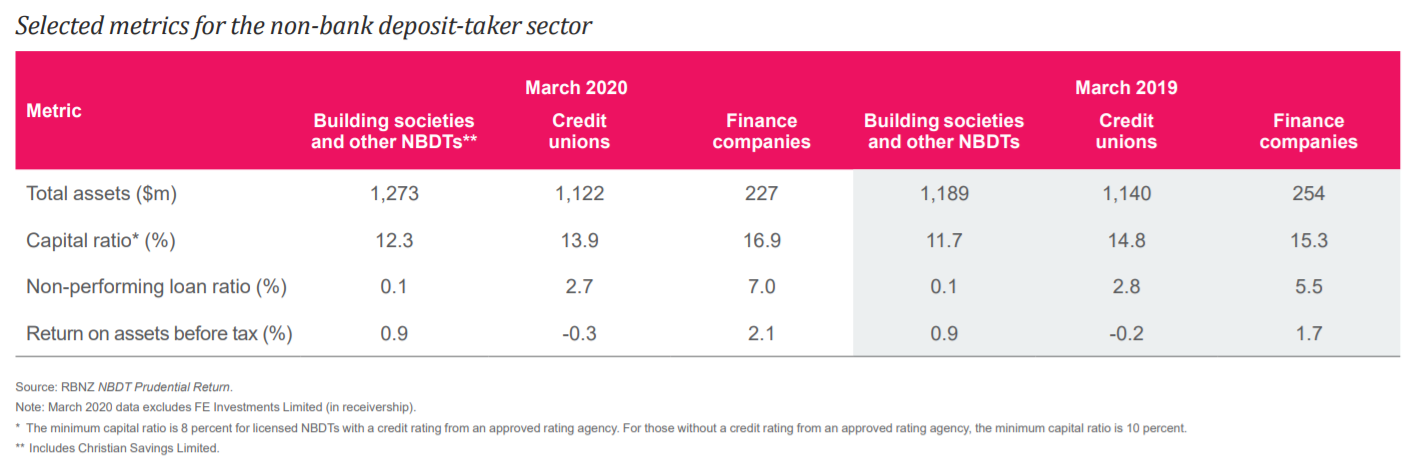

*The charts and tables below come from the Reserve Bank.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

3 Comments

A welcome and much needed development. Thank you Gareth for bringing this initiative to readers' attention.

The Irish experience - http://publicbankingalliance.ie/

The subtext of this is the RBNZ are saying they can't help the NBDTs with $million backhanders because they aren't on-market participants. You would think the Credit Unions and Building Societies would collaborate to set up a single-desk joint-venture market-participant, join the trough and divvy up the spoils

Poor credit unions will get wiped out soon. They have liquidity only which originates from banks. Banks use working capital to create liquidity.

Liquidity can be debased at the blink of an eye by central planners. When cash is removed and we go digital credit unions will not be allowed to exist. Only capital holders ie banks.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.