Smaller banks held up better than the big banks in Reserve Bank (RBNZ) liquidity stress testing, while solvency stress testing shows banks have more work to do to withstand a one-in-200 year event, which is the benchmark for the new RBNZ capital standards being phased in by 2028.

These were two of the conclusions the RBNZ came to in its annual stress testing of New Zealand banks.

The RBNZ undertook both its regular solvency stress test, challenging the resilience of banks’ capital to a severe downturn, and also put the spotlight on banks’ liquidity and funding resilience through a liquidity stress test ahead of next year's review of the RBNZ's liquidity policy. The solvency stress test included the five largest banks - ANZ NZ, ASB, BNZ Westpac and Kiwibank - and the liquidity stress test featured those five plus Co-operative Bank, Rabobank NZ, Heartland, SBS and TSB.

The RBNZ says the stress test scenarios are hypothetical and don't represent its view of the most likely future path for financial stability risks. And the RBNZ doesn't release individual banks' stress test results.

First liquidity stress test in 18 years

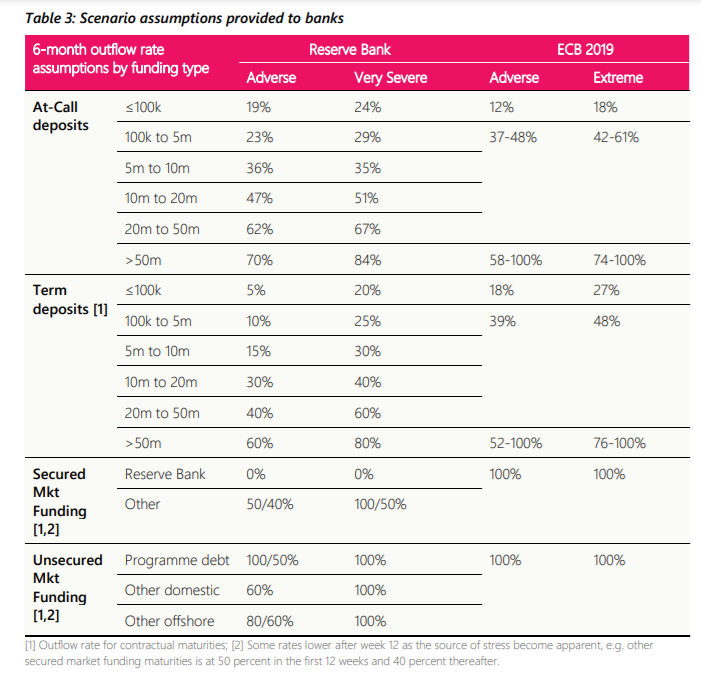

The liquidity stress test was the RBNZ's first banking industry test focused on liquidity since 2003. It featured 'adverse' and 'very severe' scenarios to assess the resilience of banks to a bank-specific event. Disruptions included a cyber-attack, IT systems disruption, or fraud leading to reputational damage, and a significant share of the bank’s funding being withdrawn or no longer available within a short space of time.

"The scenarios included a set of weekly outflow and other assumptions over a six month period, longer than our usual liquidity requirements. Banks applied these assumptions to their March 2021 balance sheet to determine their weekly net cash outflows and liquid asset balances (i.e. cash or assets that can be readily converted to cash) and the survival horizon (the number of weeks before liquid assets can no longer meet their net cash outflows). The very severe scenario assumptions were designed to test the limits of bank’s liquid asset balances in meeting cash outflows without mitigating actions," the RBNZ says.

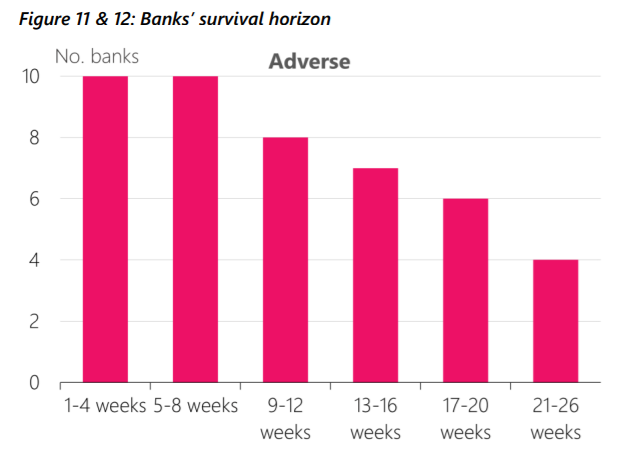

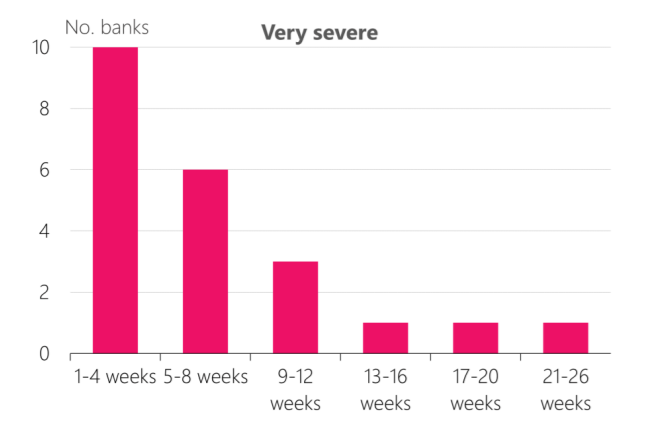

"The results showed that four of the 10 banks in the adverse scenario and only one bank in the very severe scenario had a survival horizon more than six months. The scenario had a greater effect on the larger banks’ customer withdrawals, leading to these banks having a shorter survival horizon than the smaller banks."

"Banks were permitted to use mitigating actions to improve their survival horizon, so long as the actions were already contained within their contingency funding plan. The most common actions taken by banks were to reduce the growth of new business, in some cases stopping lending altogether, use parent bank support, and increase deposit pricing in order to reduce outflows or attract new deposits," the RBNZ says.

The scenarios assumed no systemic stress and that any overseas parent bank was unaffected. The RBNZ sees benefits in repeating liquidity stress testing on a regular basis to monitor longer periods of stress to complement current prudential requirements that require banks to hold sufficient liquid assets to survive stress over one week and one month.

"This exercise will be used as an input into our forthcoming liquidity policy review," the RBNZ says. (Detail of the RBNZ liquidity policy itself is here).

'Larger banks had a much shorter survival horizon'

The stress test assumptions were benchmarked against the RBNZ’s one-month maturity mismatch ratio calculation, the two scenarios contained in the 2019 European Central Bank (ECB) liquidity stress test, plus historical experience and were discussed with the Australian Prudential Regulation Authority.

"The median bank survival horizon is 21 weeks in the adverse scenario and 11 weeks in the very severe scenario. This compared to the ECB exercise of 25 weeks for their adverse scenario and 17 weeks for their extreme shock scenario. The shorter duration experienced in our test was due to a combination of the starting position of banks and the stress assumptions, especially our higher outflow assumptions in the first month of our test which would deplete banks’ liquid assets more quickly," the RBNZ says.

"Larger banks had a much shorter survival horizon in both scenarios than the cohort of smaller banks. In the very severe scenario some of the largest banks fell into deficit fairly quickly following the one-month period of our maturity mismatch ratio. The driver of the difference in outcomes between the large and small banks was the difference in funding compositions. This was also consistent with the ECB finding that ’global systemically important banks are in general hit hardest by the 2019 shocks owing to higher reliance on less stable deposit types and wholesale funding’."

"The average large banks’ share of market funding plus large deposits, which attract the highest outflow rates, was 25% of total funding, compared to only 10% for smaller banks," the RBNZ says.

Large banks were left with a much higher deficit than the smaller banks at the end of the six months. A bank's survival horizon was driven by its opening liquid assets position and its funding composition. The survival horizon was longer if the bank held; a higher level of liquid assets which provides a stronger buffer to offset outflows; a higher proportion of smaller depositors which have a lower outflow rate assumptions than larger depositors with the assumption being that larger depositors are likely to move banks in stress; more fixed-term funding and of longer maturity; and a larger proportion of secured than unsecured wholesale funding.

Banks were allowed to use mitigating actions to address their liquidity deficit if they were already contained within their contingency funding plan.

The main mitigating actions included: a reduction in new lending, which was identified by nearly all banks with some halting lending altogether; large group support, either through borrowing from their parent bank or capital injections; raising deposit rates in order to reduce outflow and even attract new deposits from competitors; and increasing the bank’s capacity to borrow from the RBNZ via extending internal Residential Mortgage-Backed Securities.

"Banks commented that the exercise worked well, notwithstanding some data collection difficulties, and there were a number of benefits they gained for their internal stress testing. The exercise provided a cross check of their internal stress test assumptions; additional scenarios to use; confirmation and testing of their contingency funding plans; use of the more granular data from the liquidity stress test for their internal stress testing; and expansion of their liquidity stress beyond shorter focused time horizons," the RBNZ says.

Banks had to choose mitigating actions without knowing the full impact & length of the shock

The solvency stress test saw the RBNZ co-ordinate a process where the big five banks used their own models to estimate the effect of the stress scenario on their capital. Banks had three to four months to submit their results. The RBNZ then made adjustments to the submissions where bank modelling generated inconsistent outcomes compared to peer banks, RBNZ modelling and experience, and previous stress tests.

"There was minimal difference between the capital outcomes of the banks’ submissions and our desktop model at the aggregate level. However, there were more significant changes at the individual bank level which we discussed with banks," the RBNZ says.

For the first time the solvency stress test was split into two stages, with banks required to choose mitigating actions and submit their results after the first year of the shock without knowledge of the length or severity of the shock, which was subsequently provided in stage two.

"This prevented banks gaining perfect foresight of the scenario and allowed them to exercise greater consideration when selecting their mitigating actions. It also allowed us to incorporate the health of the banking sector after year one of the exercise for stage two of the scenario design," the RBNZ says.

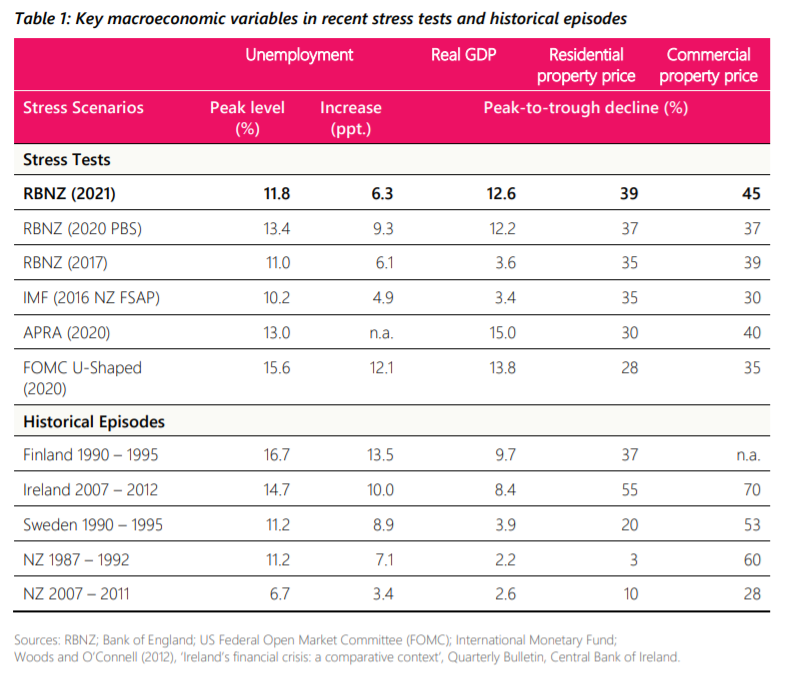

In the first year the NZ economy experiences a severe recession for the first six months as a global COVID-19 resurgence bites, resulting in widespread lockdowns and an economic downturn. Prior to 2020 the RBNZ had never included a pandemic in bank stress testing.

"Economic activity is dragged down by sustained border restrictions both in New Zealand and abroad, domestic lockdowns and social distancing measures, persistent economic uncertainty, subdued consumer and business confidence, and weaker global demand for New Zealand’s exports. The containment measures heavily affect the retail, tourism and hospitality sectors in particular."

"Additionally, a drought strikes the whole of the North Island in the 2021-2022 season. This drought affects both dairy farms and the remainder of the agriculture sector in the North Island. In response, milk production by North Island dairy farms is reduced by 7% from the previous season, while a greater reliance on purchased feed and supplements increases their expenses by 9%," the RBNZ says.

"During year one, house prices fall by 20%, commercial property prices fall by 26%, New Zealand’s real gross domestic product contracts by 8% on average and the unemployment rate reaches 10%. Credit spreads widen due to the increased global uncertainty, which increases overall bank funding costs. Government and Reserve Bank policy responses include a large fiscal support package albeit slightly less than that in 2020, cutting the OCR to -0.50%, and additional purchases of government bonds up to $100 billion as part of our large scale asset purchase programme."

The unemployment rate rises as high as 11.8% and house prices fall by as much as 39%. The scenario is assessed as a one-in-50 to one-in-75 year event, similar to the pessimistic baseline’ scenario in last year’s RBNZ stress test, but less severe than the very severe 2020 scenario.

"The aggregate overall loss rate, total impairment expenses as a percentage of credit balance, was 3.2%. This was lower than the 2020 pessimistic baseline scenario loss rate of 4.0%, due to the banks’ lower loss rates on mortgages and smaller business portfolios in 2021. The collateral for mortgages, and potentially for smaller businesses, has recently strengthened due to the increase in asset prices and stronger balance sheets heading into this year’s stress test," says the RBNZ.

"Impairment expenses contributed a 4.7 percentage point reduction to the change in the aggregate total capital ratio."

'More work needs to be done to ensure banks could withstand a one-in-200 year event'

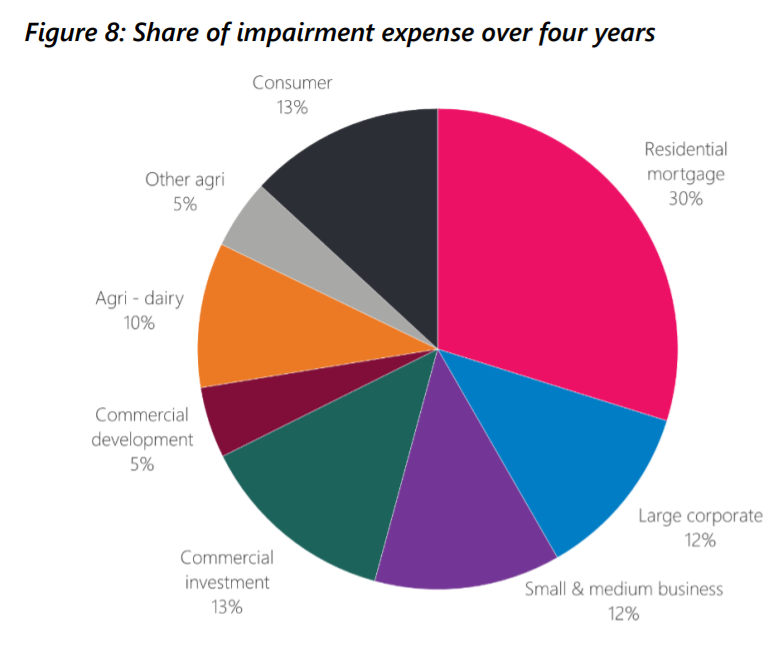

Meanwhile, residential mortgages made up 30% of total impairments, well below the 63% of total bank credit exposures mortgages account for. And the residential mortgage loss rate of 1.5% is lower than other portfolios because borrowers continue making mortgage payments for as long as possible during stress periods, even when they are unable to pay other loans, the RBNZ says.

"The loan-to-value ratio restrictions, and an increase in the equity of home-owning households from house price growth in recent years, contribute to reduced losses for banks on defaulted loans," the RBNZ says.

The aggregate Common Equity Tier 1 capital ratio of the five banks fell by 3.6 percentage points from 12.9% at the start of the stress test to a minimum of 9.3%.

"This is well above the current regulatory bank minimum of 4.5% and shows that banks are sufficiently well capitalised to manage a COVID-19 induced economic downturn and continue to support demand for lending during such a scenario. The results also showed banks to be more resilient than in last year’s pessimistic baseline scenario due to an increase in their capital buffers, assisted by improved profitability and dividend restrictions, and consistent with the forthcoming implementation of the capital review," the RBNZ says.

"However, the 2021 stress test results also indicate that a major stress event would make it difficult for banks to meet higher capital requirements in the lead up to full implementation of the new standards in 2028. These results reinforce the need for banks to continue to build capital and replace non-complying Tier 2 [capital] instruments, which will cease to be compliant under the new rules. Our annual solvency stress tests and banks internal stress testing can be used to monitor this transition risk."

"The results of this stress test show that New Zealand’s banking system has a stronger level of resilience than a year ago, and is well placed to support the economy through severe downturns. However, the current capital levels still lead to banks capital ratios falling to well within the prudential capital buffer under the new capital framework for a scenario calibrated to a one-in-50 to a one-in-75 year event. More work needs to be done to ensure banks could withstand a one-in-200 year event, the benchmark for our capital standards by 2028," the RBNZ says.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

13 Comments

And the RBNZ doesn't release individual banks' stress test results.

Unsecured bank creditors (so called "depositors" in particular) demand to know.

According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

Hi Audaxes. Do you know if Kiwisaver funds are also at risk from an OBR bail-in?

The RBNZ reading material isn't clear (to this layman at least...)

I am already retired.

But I guess the capital asset values are at your risk, but I am confident the bank should be executing your AUM securities trades through an independent third party repository. I have an old NZ Debt Management account at Computershare to register government debt trades in my own name. Cash on deposit at a bank could be an issue - it is co-mingled. But I accept that risk as I am too lazy to buy NZ Government T Bills all the time.

I worked for a US bank in London that funded a non-contributory two thirds final salary scheme, excluding bonuses, in some outside scheme.

Because I was a UK financial authority registered fixed income trader I was free to set up my own fund at Sun Life Insurance and trade the capital and bank contributions, so long as it was not US Treasury bonds, at 0.25% per annum repository cost. I used third party brokers, at little cost because the bank gave them business from another desk, to execute my trades - mainly UK Gilts. Unfortunately that option is not open to most pension savers.

The proceeds are now safely tucked away in a family trust in NZ, some of which are subject to a possible OBR bail-in due to everyday liquidity demands.

Nope, they're completely ring fenced in fund structures that are governed by 3rd party trustees.

The funds management arm of a bank should not be confused with its general operations.

Can someone explain why the banks aren’t drawing more heavily, or seen to have stopped drawing altogether, on the FLP? Are there more catches to it than cheap funding? I’m no economist so looking for a genuine answer.

Simple answer - FLP is a floating rate repurchase agreement priced at OCR - currently on a rising trend to ~2.6%, according to the RBNZ.

by Audaxes | 15th Jul 21, 8:50pm

Under the FLP, the Bank will offer 3-year funding to eligible institutions. The funding will be structured as floating rate Repurchase Transactions priced at the Official Cash Rate (OCR), each for a term of three years.

A review of this accounting diagram Exhibit 2 (secured borrowing) sets out the reality.

At what point do Banks have to mark to market asset tiers where the values have declined? What effect will this have on Banks ability to lend and were will this most impact?

No idea. This was a pressing issue with banks in Japan after the bubble burst. It took approx 10 years for the banking system after the bubble to move to mark-to-market accounting.

Reuters tells us that the former Chair of the Federal Reserve, Ben Bernanke, speaking out of the country in the UAE, makes somewhat of an admission of omission regarding 2008 – that there existed too much “overconfidence.” The timing of that “admission” is priceless (pun intended) given the recent release of the 2008 transcripts that leave no doubt about that. Bernanke was pretty much forced to state the obvious.

But beneath that simple explanation lays the deeper trouble that remains unresolved, as we get QE after QE. It is very illuminating in how the former Chairman sets up the inequity he believes was at play:

That was actually very hard for me to get adjusted to that situation where your words have such effect. I came from the academic background and I was used to making hypothetical examples and … I learned I can’t do that because the markets do not understand hypotheticals.

In other words, he is too smart for the markets since his complex theories are not easily understood by the simpletons that exist far beneath his awe-inspiring intellect. You cannot wipe away the hypotheticals that “subprime is contained” and “the worst is behind us” so easily, unless you really believe that markets are too stupid to follow orders. Again, this is not a unique expression of central bank frustration. The Bank of Japan repeatedly denounces the “stupid” market for not conforming to its genius. The trouble is markets, not central planning; a sentiment very emblematic of Janet Yellen’s ascension.

This is a timeless expression from the economic elite, embedded in the very fabric and foundation of the Federal Reserve (and all modern central banks that now openly practice central planning). Senator Robert Owen, one of the primary founders of the Federal Reserve, remarked more than a century ago that a central bank was needed to keep the common rubes from destroying themselves:

It is the duty of the United States to protect the commercial life of its citizens against this senseless, unreasoning, destructive fear that seizes the depositor when he has been sufficiently hypnotized by the metropolitan press with its indiscreet suggestions.

If common folk were not so dumb, and could actually understand complex hypotheticals, utopian magic would be ubiquitous. You can practically here it in the common refrain of the gold standard in the 1930’s – if central banks had not been tied to this relic, it might only have been just a bad recession. In other words, gold (representing market power) undermined 1930’s centralized virtuosity. Link

Our central banking masters of the universe terrify me Audaxes

Me to.

Did anyone else notice they assumed OCR at -0.5 when the housing market and economy crash in their scenario. That's wishful thinking. They might not be able to drop interest rates if it destroys the currency, if other markets aren't doing the same, as inflation is running out of control. A stagflation stress test would have been more appropriate, and may have had very different results.

Very good point.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.