A spike in housing and rural debt is keeping banks smiling, as falling interest rates dampen their profits.

KPMG’s Financial Institutions Performance Survey (FIPS) for the December quarter, released today, shows the New Zealand banking sector suffered a 12.57% decline in profitability in the three months to December 2015, as its profits fell to $1.11 billion, from $1.27 billion in the September quarter.

On the flipside, its total assets hit a record high of $443.01 billion.

Banks’ lending increased by 2.09% or $7.32 billion over the quarter, to $357.88 billion, with KPMG saying there are no signs of the growth in their loan books slowing.

In fact, ANZ, BNZ, the Commonwealth Bank of Australia (ASB), Heartland Bank, Kiwibank, Southland Building Society, the Co-operative Bank, TSB and Westpac, collectively grew their gross loans by 8.25% from the 2014 to the 2015 December quarter.

KPMG admits the growth is being fuelled by Auckland’s hot property market, coupled with rock-bottom dairy prices, which are hampering farmers’ abilities to make loan repayments and are causing them to make additional drawings.

It points to Reserve Bank (RBNZ) data which shows that as at February 2016, lending to the agricultural sector grew 8.4% year-on-year, while housing lending increased by 7.9% and business lending 6.9%.

Shrinking interest margins

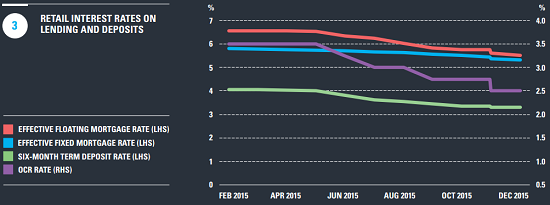

The RBNZ cut the Official Cash Rate by 25 basis points on four occasions in 2015. Having undergone a further cut last month, the rate, ahead of another OCR decision today, was at 2.25%.

While the low interest rate environment’s encouraged borrowing, it’s also seen banks’ interest rate margins fall, softening their profits.

KPMG says “competitive pressures” have seen banks’ interest margins fall 4 basis points over the December quarter, to 2.21%. This is the lowest it’s been since December 2010, when the margin was 2.16%.

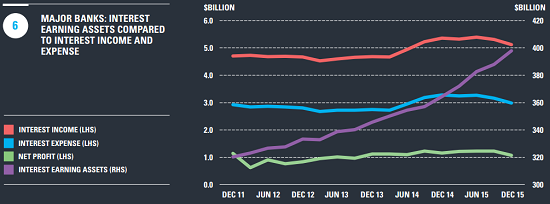

All of the nine banks surveyed by KPMG, other than Heartland, have reported declines in interest income of 2-4%, despite increasing their interest earning asset base by 2.68%.

“Annualised interest income earned over average interest earning assets decreased by 28 basis points from 5.54% to 5.26% this quarter,” KPMG says.

“Falling interest rates also led to lower funding costs, with the overall interest expense having reduced by 5.42%, while interest bearing liabilities grew by 1.43% reflective of the favourable funding conditions experienced in 2015.”

KPMG says annualised interest costs over average interest earning liabilities reduced by 22 bps from 3.72% to 3.50%. "However, we noted that in early 2016, markets became more volatile with executives commenting about an increase in wholesale funding costs for banks."

Heartland 'the frontrunner'

Among the major banks Westpac experienced the most notable easing in net interest margins at 11 bps down to 2.17%, followed by BNZ reporting a decrease of 9 bps down to 2.21%, and Kiwibank with a 6 bps decrease down to 2.07%. Meanwhile ANZ and CBA broadly maintained their margins in the quarter, showing only a 1 bp drop, down to 2.22% and 2.12% respectively.

"Heartland Bank remained the frontrunner and not only continued to report the highest net interest margin in the sector at 5.18%, but also having bucked the trend and lifted its margin by a further 37 bps since September 2015. Heartland Bank achieved this on the back of higher interest income relative to interest earning assets, up by 120 bps to 9.97%, and a 22.19% growth in its gross loans and advances."

KPMG notes that despite banks growing their loan books, their net interest income remained unchanged in the December quarter at $2.25 billion. It says this reflects the highly competitive market, which is seeing banks offer record low interest rates.

“Return on interest earning assets have continued to decline for a fourth consecutive quarter… This continues to be reflective of not only continued margin pressures, but also diminishing returns as banks’ asset bases continue to grow,” says KPMG.

It reports a decrease in non-interest income – ie fees – has also hampered banks’ profitability.

This fell by 31% or $252.63 million, largely due to “a decline in trading income and unfavourable fair value movements of financial instruments experienced by ANZ and BNZ”.

Asset quality strong

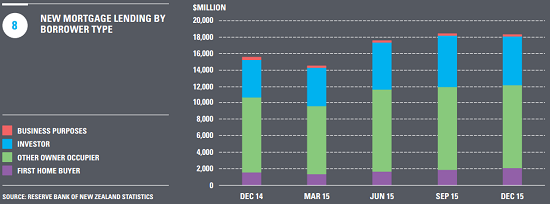

Digging into the detail around the type of lending growth experienced by banks, KPMG reports that new mortgage lending by borrower type has remained "broadly consistent" with the previous quarter, with lending to first home buyers and owner occupiers comprising 67% of new mortgage lending for the December quarter.

It notes that residential mortgage holders have continued to opt for shorter fixed terms, with 34% of residential mortgages being on one-year fixed terms (an increase from the previous quarter), and 24% being on floating rates (a decrease from the previous quarter).

KPMG says despite the growth in their loan books, banks’ asset quality remains strong.

Impaired asset expenses stable

The banks' impaired asset expense relative to gross loans and advances was stable at 0.11%. Meanwhile they reduced their gross impaired assets by 4.64% and past due assets by 11.74%.

“Dairy industry exposure continues to be closely monitored by the banks and the RBNZ, but thus far there does not appear to be a significant deterioration of asset quality reported,” KPMG says.

“Stress tests conducted by the major dairy lenders revealed that on the existing dairy exposures, currently totally circa $38 billion or 10% of banks’ loan books, the projected loan losses could amount to around 8% or $3 billion.

“The RBNZ said that the stress tests showed that most of the impact on banks profitability would occur in the first three years and expected that these losses could be absorbed through earning, as opposed to eroding capital.”

4 Comments

KPMG admits the growth is being fuelled by Auckland’s hot property market, coupled with rock-bottom dairy prices, which are hampering farmers’ abilities to make loan repayments and are causing them to make additional drawings.

It points to Reserve Bank (RBNZ) data which shows that as at February 2016, lending to the agricultural sector grew 8.4% year-on-year, while housing lending increased by 7.9% and business lending 6.9%.

In a nutshell compounding debt growth more than twice that recorded by nominal GDP expansion. I thought ensuring financial stability was the serious part of the RBNZ mandate? Cutting the OCR and standing aside while the debtors pile on more liabilities to fund the servicing costs due on existing debt hardly seems consistent with such duty, or are the finance minister's PTA demands paramount.

Compounding growth is very profitable until defaults occur.

Exactly - if this claim is right:

It's buy, buy, buy for housing investors, as new figures out today show that in March the share of mortgage money borrowed for houses by investors climbed to over 35% of the more than $6.5 billion borrowed. Read more

One small liquidity glitch similar to that currently enveloping the upper end of the New York rental market and it's all over. Falling dominoes know no end.

A cool-down in Manhattan’s apartment-rental market is hitting the bottom line of Equity Residential as the landlord is forced to offer concessions to tenants who suddenly have a lot of competition to choose from.

“New York City just turned very quickly and more deeply than we expected,” Chief Operating Officer David Santee said on a conference call Wednesday to discuss first-quarter earnings. With the city accounting for about 20 percent of the firm’s revenue, “if you can’t achieve 3 or 4 percent rate growth there, then it’s going to impact your full-year growth.” Read more

hardly seems consistent with such duty

only a very very few are able to "change their mind"

http://www.bbc.co.uk/programmes/b0510gvx#play

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.