The largest “cause and effect” variable on the New Zealand economy next year will not be what the Government of Reserve Bank decide on policy changes, it will be the increase in pork, beef, lamb and chicken prices.

Our export commodity prices are forecast to increase further from their already record highs and domestic prices for meat will follow and push up inflation.

The dramatic decline in pork production due to the African swine fever in China is contributing to a global shortfall in meat supplies that can only drive prices higher.

China’s pig herd has been halved and it will take years to rebuild.

A quarter of the world’s pig population has been lost.

As a result, worldwide production of chicken, pork and beef in 2020 will about 6 million tonnes down on this year. Beef, chicken and lamb production cannot be automatically ramped up to replace the pork shortages.

The global food trade has not seen a meat supply shortfall of this magnitude for more than 50 years. It is an extraordinary situation that has not been given the prominence in New Zealand’s media that it deserves. As the swine fever (a viral disease) spreads into Vietnam and Cambodia, the New Zealand and Australian border bio-security authorities will need to be on full alert.

Inside China pork prices have increased 170% over the last year, chicken prices are up 20% and beef up 10%.

What is not known at this time is the socio/political ramifications within China if the urbanised populations cannot buy protein as the price is just far too high. Chinese control of their media means that we may never hear the fully story of public food shortages as substitutes for pork cannot be found quickly enough. It may be over to the Americans to substantially increase beef exports to China as Australia’s herds are down due to drought and the other large global beef producer, Brazil is constrained. Environmentalists have already raised concerns that increased cattle-rearing in Brazil will drive high levels of deforestation in the Brazilian Amazon.

The implications for currency values from this emerging food supply disaster are twofold:-

- Already record high export prices for our beef and lamb are set to move higher still in 2020. Whole milk powder prices are also likely to increase further as China demands imported protein. The divergence of the NZD/USD exchange rate value away from our commodity price index over the last 18 months (due to the uncertainties of the China/US trade war) will widen further unless the NZD exchange rate moves upwards.

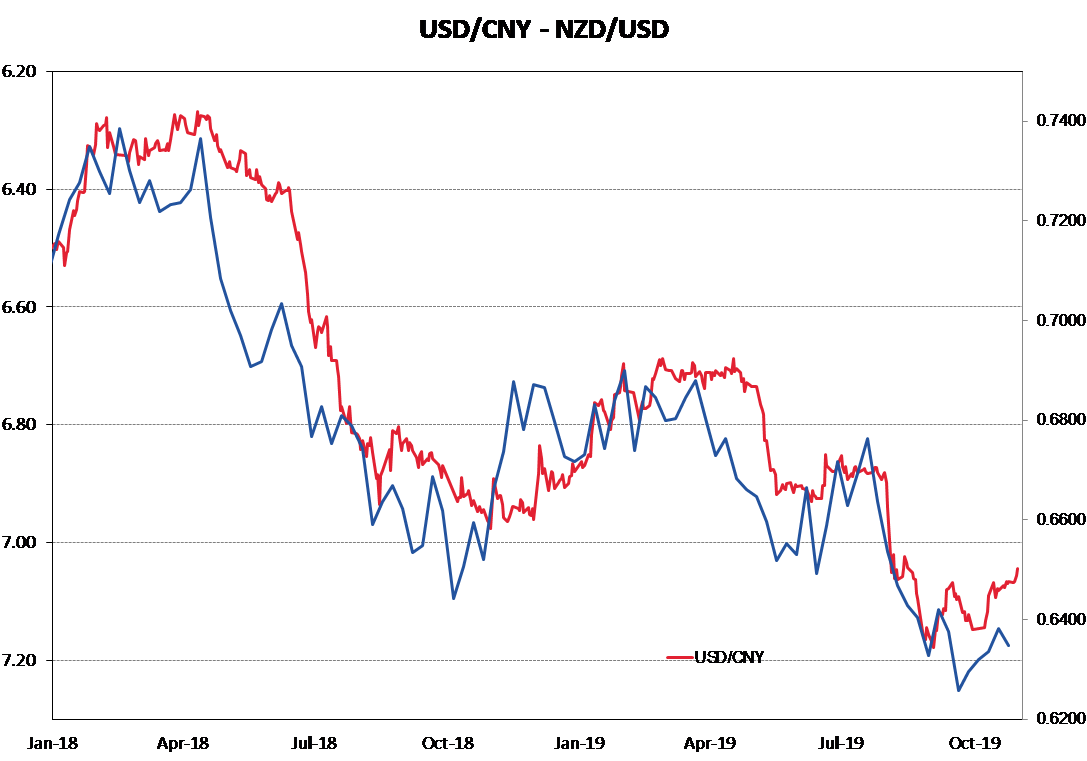

- The People’s Bank of China (PBOC) are already setting stronger Yuan values against the USD on a daily basis. The Yuan was deliberately weakened against the USD over the last 12 months as a retaliatory measure against US import tariffs on Chinese export goods. As the trade war starts to be resolved the Chinese authorities are changing policy away from a weaker Yuan. A stronger Yuan against the USD will make increased imports of beef and sheepmeat less expensive and help control domestic foods prices within China. The Yuan has already appreciated against the USD from 7.1800 in early September to 7.0350 last Friday. Both the NZD/USD and AUD/USD exchange rate are highly correlated to the Yuan (USD/CNY) exchange rate.

Given the new circumstances of a phased trade agreement with the US now being agreed and the need to dramatically increase food imports into China, it would not be too surprising to see the USD/CNY exchange rate return to the 6.7000 area it was trading at back in January to April this year. A 7% appreciation of the Chinese Yuan from here would see the NZD/USD rate return to well above 0.6800.

First test for monetary policy committee members

We may be about to witness the first real test of the expanded RBNZ monetary policy committee which now includes three external members (Caroline Saunders, Bob Buckle and Peter Harris) as well as the four internal RBNZ members, when the next Monetary Policy Statement is released on 13 November.

There have been considerable changes in both the global and local economies since their last statement in early August.

Global financial/investment markets are now reflecting less risk to the world economic outlook as progress is made on the China/US trade dispute and an end-resolution is in place for Brexit (i.e. a “hard Brexit” is not going to occur).

Here in New Zealand, both GDP growth and inflation are now tracking above official RBNZ forecasts.

Additionally, business confidence is finally recovering, and consumer confidence has moved higher again.

The so-called economic “headwinds” never arrived, and the export commodity price outlook now suggests a considerable “tailwind” for the NZ economy looking ahead. Whether the largely academic external members of the RBNZ Monetary Policy committee are up to speed with these recent economic developments will be interesting to observe.

The local interest rate market now has much less conviction about the RBNZ cutting the OCR by another 0.25% from 1.00% on 13 November.

The Australian interest rate market is now barely pricing in another 0.25% reduction over the next two years following the change from the RBA to a more neutral monetary policy stance.

Whatever the RBNZ decision is on 13 November it may be positive for the Kiwi dollar. A 0.25% cut to 0.75% (same as the Aussies) may be interpreted as the last reduction. A “no change” decision would also send the Kiwi dollar higher. A break above the 0.6450 resistance would see the NZD/USD rate higher towards 0.6600 over coming weeks.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

20 Comments

... " emerging food supply disaster " .. really , Rogie ... the Chinese people are nothing if not resourceful and resilient... decades of Communist rule have taught them to harden the F up ...

NZrs are the big softies who'll whinge long and hard about the increasing price of meat ...

Maybe they will switch to plant-based meats - just saying

Or lab-grown meat i.e. flesh sprouted in artificial bio-reactors. Something I'm in favour of, as well.

Yes GBH.

Chat with many a china tourist, tekapo, Akaroa. They will comment how backward and primitive they find nz, though beautiful.

And it is hard to explain why Christchurch is still rebuilding.

Decades of communist rule have certainly given them a dog-eat-dog society. Especially noticeable if you've visited both mainland China and Taiwan.

The conclusions do not seem to follow from article?

Inflation is clearly going to overshoot.

RBNZ will ignore this as Bank of England did in 2012-14, terrified of putting up rates

Also, completely ignored thus far (I covered both USA and China food prices in an article on Linked in some time ago) is crop failure of 50 year magnitude (as in worst) in USA, the bread basket of the world.

Everyone is thinking it seems, that no inflation will come after 11 years trying to create it through useless QE

But it will come after deflation which is where we are now: liquidity trap.

But it will come after deflation which is where we are now: liquidity trap.

Return of capital is more important than return on capital - co-mingled unsecured bank liabilities masquerading as personal deposits don't cut it.

{kind=link}

These shortages and high prices will also affect markets all round the world. Instead of taking the easy, lazy route by supplying China directly, we should use the opportunity to develop a strong presence in all other world markets other than China. We are already far too dependent on China and vulnerable to it's not so subtle bullying. As things stand at the moment we are not much more than a puppet state of China. Can any NZ politician say anything that is even remotely critical of China - No. Not too different from Hong Kong politicians are they? NZ companies should consider how vulnerable they are if China decides to stop purchasing from us as they have subtly suggested every time we do the slightest thing that may not suit them. Remember they are are a totalitarian command economy. Taps can be turned on and off at the whim of the presiding leader.

We should be concentrating our attention on countries that are not power and influence hungry. Ie not China, Russia, USA and possibly even Australia who has aspirations to swagger around like a mini me USA. Concentrate on Europe, Scandinavia, Canada, Japan, other rapidly developing Asian economies. There are some developing countries on the old silk road like Kazakhstan that have huge mineral wealth.

We, the modest nations of the world need to stick together and support each other, otherwise this handful of bullies will just suck us into their orbit and diminish our prosperity and independence.

China wants low value cuts, chicken claws, mutton flaps, its a good strategy to concentrate on high value markets and they can have the offcuts.

China is far too complex for simple answers and solutions. I have a friend in the sea food industry and his biggest competitor is Chinese shelf fish. They export over half million tonnes of scallop flesh alone per year.

Example, US lobster industry.

China is running a war with the USA, USA is at war with China on multiple fronts, food is one of them.

"One point to keep in mind is that China has millions of acres available to produce crawfish, either in conjunction with rice or fish culture, or as a stand alone crop," he advised in an email. "Any export market to China would probably only last a few years, until they were able to catch up internally on their supply-demand imbalance."

https://www.undercurrentnews.com/2018/07/16/usda-chinas-little-lobsters…

https://dimsums.blogspot.com/2019/10/china-food-security-self-sufficien…

Kiwi is looking good for a good rally from here basis Roger's comment's re: econmic figures coming out better than expected etc and continuing silence from Trump re: Tariff/trade war.

However big big item and will be sitting over the market - increasingly comments from China around inablity to agree to a trade deal with the US, as the US is effectively askng for them to give up to many rights etc.

If no serious agreement can be made - it's only a matter of time before Trump tries his usual jawboning techniques - threatening new tariffs etc, which will then send markets and Kiwi lower.

People are relying very much that the trade war is dying down - however no serious agreement as yet and as time goes on by - higher risk that Trump kicks off again and back to where we started etc.

It is not just Trump. The relationship between the USA and China may never be the same. I.e. the USA will not be the mug that they have been in the past. Nancy Pelosi, just the other day, was moaning how Trumps tactics have weakened the USA's bargaining position, so don't expect the Democrats to be any less tough with China. Big proviso however, Joe Biden, he is probably a Chinese vector, given that his son has been bought off with support of his investment company and a position on the board of a big Chinese investment company. I would not mind betting that there will also be a lot of pro Chinese money from Wall st to support him.

Does NZ import much pork and if so why?

Because its cheaper than NZ pork. Low quality imported pork is easy to markup when turned into bacon

About 50% is imported, it doesn't have to meet the same animal welfare standards as pig meat produced in NZ which is one of the reasons it is cheaper.

Yes fundamental shifts are happening as we read. Disaster in the protein chain in China has been building for over a year now. ASF is really making its mark. The USA is still the globes food bowl & has been for 100 years, so this shift in the protein chain demand, could be a game changer. One disaster often leads to others & it wouldn't surprise me if drought or flood doesn't wipe out much of North America's food supplies, adding to the challenge. It's happened before. A combination or series of smaller misfortunes are often key ingredients in a larger crisis.

A question for Roger

Are New Zealanders ready for a significant jump in food costs as a result of these global protein shortages ?

Already we are seeing Beef export prices to the US increased by 25% on a year ago.

Question for Rog. Why are the global protein or lean hogs future markets not seeing what he is and is he buying lean hog futures at these sure to be bargain prices?

I suspect that the drought in Australia- now in year 3 of possibly a 50 year drought will affect global markets for Lamb and Grains presenting NZ with an opportunity to reconfigure the supply chain with cuts so adding value in NZ.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.